Updated on December 19th, 2023 by Bob Ciura

Spreadsheet data updated daily

Utility stocks can make excellent investments for long-term dividend growth investors.

Durable, regulatory-based competitive advantages allow these companies to consistently raise their rates over time. In turn, this allows them to raise their dividend payments year in and year out.

Even better, many utility stocks have above-average dividend yields, providing a compelling combination of income now and growth later for long-term investors.

Because of these favorable industry characteristics, we’ve compiled a list of utility stocks. The list is derived from the major utility sector exchange-traded funds JXI and XLU.

You can download the list of all utility stocks (along with important financial ratios such as dividend yields and payout ratios) by clicking on the link below:

Keep reading this article to learn more about the benefits of investing in utility stocks.

Table Of Contents

The following table of contents provides for easy navigation:

- How To Use The Utility Stocks List

- Why Utility Dividend Stocks Make Attractive Investments

- The Top 10 Utility Stocks Now

- Top Utility Stock #10: National Fuel Gas (NFG)

- Top Utility Stock #9: Alliant Energy (LNT)

- Top Utility Stock #8: Portland General Electric (POR)

- Top Utility Stock #7: ALLETE, Inc. (ALE)

- Top Utility Stock #6: Brookfield Renewable Partners LP (BEP)

- Top Utility Stock #5: Ameren Corporation (AEE)

- Top Utility Stock #4: Brookfield Infrastructure Partners (BIP)

- Top Utility Stock #3: Evergy, Inc. (EVRG)

- Top Utility Stock #2: Eversource Energy (ES)

- Top Utility Stock #1: NextEra Energy Partners LP (NEP)

How To Use The Utility Dividend Stocks List To Find Investment Ideas

Having an Excel database of all the dividend-paying utility stocks combined with important investing metrics and ratios is very useful.

This tool becomes even more powerful when combined with knowledge of how to use Microsoft Excel to find the best investment opportunities.

With that in mind, this section will provide a quick explanation of how you can instantly search for utility stocks with particular characteristics, using two screens as an example.

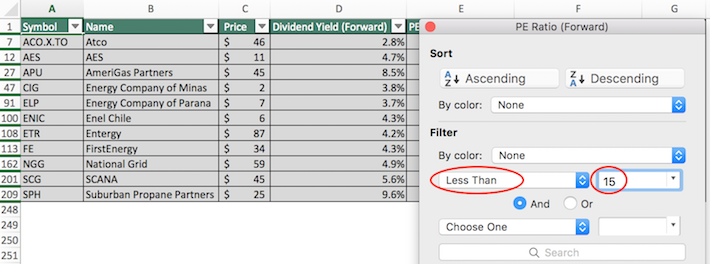

The first screen that we will implement is for utility stocks with price-to-earnings ratios below 15.

Screen 1: Low P/E Ratios

Step 1: Download the Utility Dividend Stocks Excel Spreadsheet List at the link above.

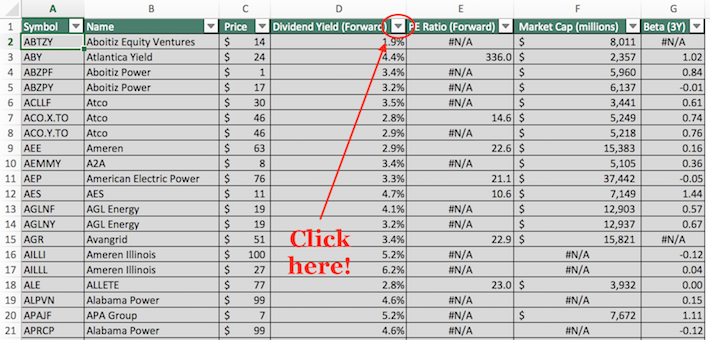

Step 2: Click the filter icon at the top of the price-to-earnings ratio column, as shown below.

Step 3: Change the filter field to “Less Than” and input “15” into the field beside it.

The remaining list of stocks contains dividend-paying utility stocks with price-to-earnings ratios less than 15. As you can see, there are relatively few securities (at the time of this writing) that meet this strict valuation cutoff.

The next section demonstrates how to screen for large-cap stocks with high dividend yields.

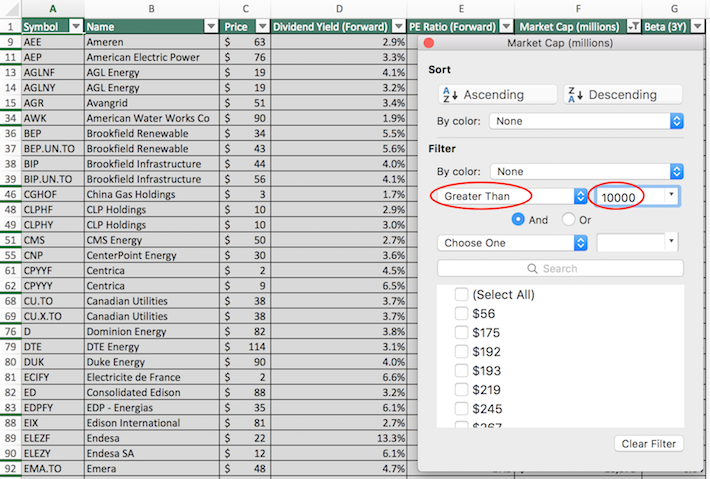

Screen 2: Large-Cap Stocks With High Dividend Yields

Businesses are often categorized based on their market capitalization. Market capitalization is calculated as stock price multiplied by the number of shares outstanding and gives a marked-to-market perception of what people think a business is worth on average.

Large-cap stocks are loosely defined as businesses with a market capitalization above $10 billion and are perceived as lower risk than their smaller counterparts. Accordingly, screening for large-cap stocks with high dividend yields could provide interesting investment opportunities for conservative, income-oriented investors.

Here’s how to use the Utility Dividend Stocks Excel Spreadsheet List to find such investment opportunities.

Step 1: Download the Utility Dividend Stocks Excel Spreadsheet List at the link above.

Step 2: Click the filter icon at the top of the Market Cap column, as shown below.

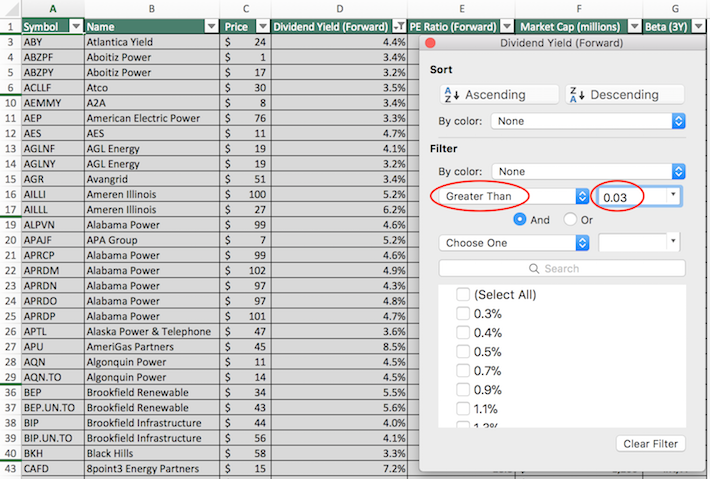

Step 3: Change the filter setting to “Greater Than”, and input 10000 into the field beside it. Note that since market capitalization is measured in millions of dollars in this Excel sheet, filtering for stocks with market capitalizations greater than “$10,000 millions” is equivalent for screening for those with market capitalizations exceeding $10 billion.

Step 4: Close that filter window (by exiting it, not by clicking ‘clear filter’) and click on the filter icon for the “dividend yield” column, as shown below.

Step 5: Change the filter setting to “Greater Than” and input 0.03 into the column beside it. Note that 0.03 is equivalent to 3%.

The remaining stocks in this list are those with market capitalizations above $10 billion and dividend yields above 3%. This narrowed investment universe is suitable for investors looking for low-risk, high-yield securities.

You now have a solid fundamental understanding of how to use the Utility Dividend Stocks Excel Spreadsheet List to its fullest potential. The remainder of this article will discuss the characteristics that make the utility sector attractive for dividend growth investors.

Why Utility Dividend Stocks Make Attractive Investments

The word “utility” describes a wide variety of business models but is usually used as a reference to electric utilities — companies that engage in the generation, transmission, and distribution of electricity.

Other types of utilities include propane utilities and water utilities.

So why do these businesses make for attractive investments?

Utilities usually conduct business in highly regulated markets, complying with rules set by federal, state, and municipal governments.

While this sounds highly unattractive on the surface, what it means in practice is that utilities are basically legal monopolies.

The strict regulatory environment that utility businesses operate in creates a strong and durable competitive advantage for existing industry participants.

For this reason, electric utilities are among the most popular stocks for long-term dividend growth investors — especially because they tend to offer above-average dividend yields.

Indeed, the regulatory-based competitive advantages available to utility stocks give them the consistency to raise their dividends regularly.

Simply put, utility stocks are some of the most dependable dividend stocks around.

To provide a few examples, the following utility stocks have exceptionally long streaks of consecutive dividend increases:

- Consolidated Edison (ED) — more than 25 years of consecutive dividend increases

- American States Water (AWR) — a water utility — more than 50 years of consecutive dividend increases

- SJW Group (SJW) — another water utility — more than 50 years of consecutive dividend increases

The long streak of consecutive dividend increases is possible only because of their unique industry-specific competitive advantages.

Clearly, the utility sector is very stable. People are going to need electricity and water in ever-increasing amounts for the foreseeable future.

One characteristic that does not describe utility stocks is high growth. One of the regulatory constraints imposed upon utility companies is the pace at which they can increase the fees paid by their customers.

These rate increases are usually in the low-single-digits, which provides a cap on the revenue growth experienced by these companies.

Utility stocks typically don’t offer strong total returns, but there are exceptions.

The Top 10 Utility Stocks Now

Taking all of the above into consideration, the following section discusses our top 10 list of North American utility stocks today, based on their expected annual returns over the next five years.

The rankings in this article are derived from our expected total return estimates from the Sure Analysis Research Database.

The 10 utility stocks with the highest projected five-year total returns are ranked in this article, from lowest to highest.

Related: Watch the video below to learn how to calculate expected total return for any stock.

Rankings are compiled based upon the combination of current dividend yield, expected change in valuation, as well as expected annual earnings-per-share growth.

This determines which utility stocks offer the best total return potential for shareholders.

Top Utility Stock #10: National Fuel Gas (NFG)

- 5-year expected annual returns: 11.4%

National Fuel Gas Co. is a diversified energy company that operates in five business segments: Exploration & Production, Pipeline & Storage, Gathering, Utility, and Energy Marketing. The largest segment of the company is Exploration & Production. With 53 years of consecutive dividend increases, National Fuel Gas qualifies to be a Dividend King.

In early November, National Fuel Gas reported (11/1/23) financial results for the fourth quarter of fiscal 2023. The company grew its production 7% over the prior year’s quarter thanks to the development of core acreage positions in Appalachia. However, the average realized price of natural gas fell -18%, from $2.84 to $2.33.

As a result, adjusted earnings-per-share declined -34%, from $1.19 to $0.78, and missed the analysts’ consensus by $0.07. The company has beaten the analysts’ estimates in 15 of the last 18 quarters.

Click here to download our most recent Sure Analysis report on NFG (preview of page 1 of 3 shown below):

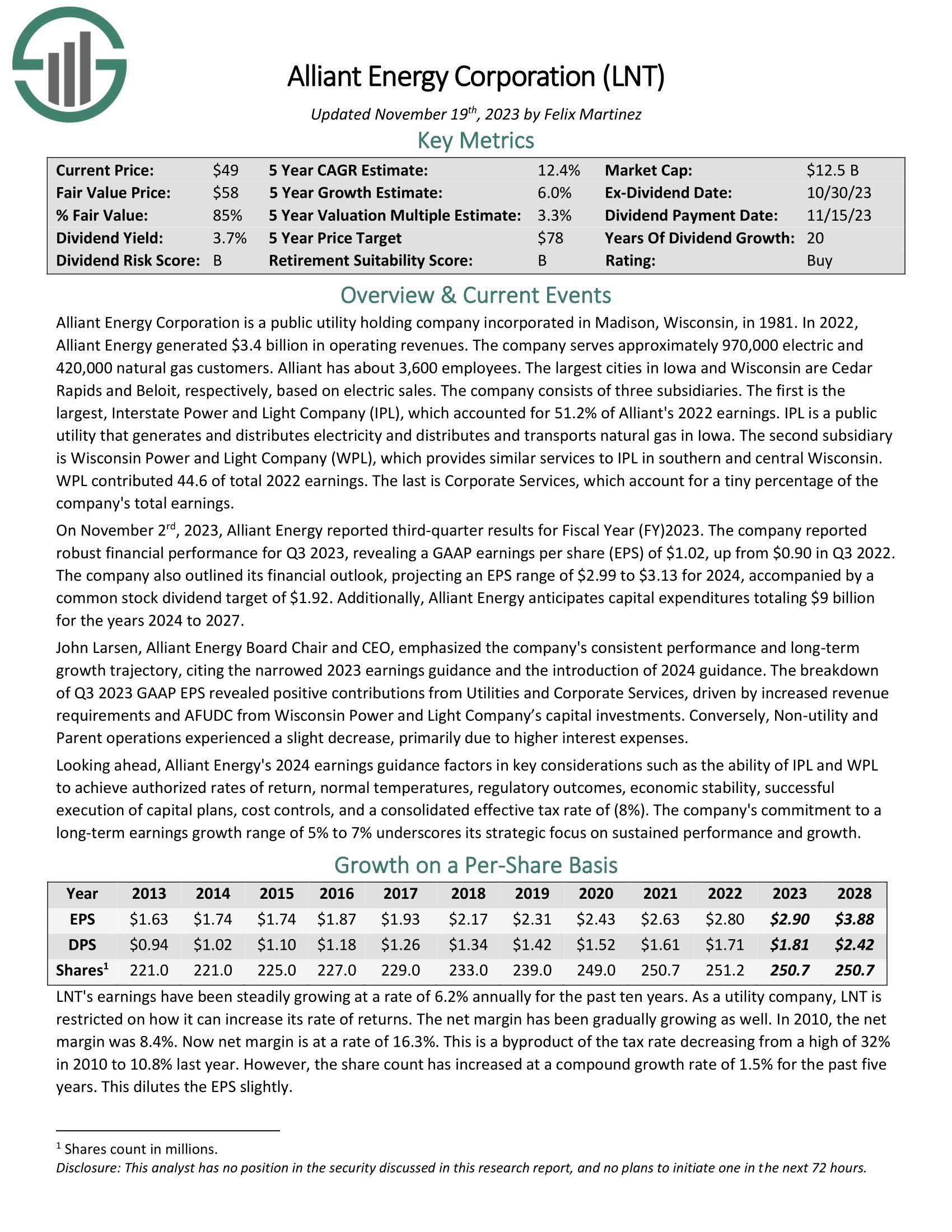

Top Utility Stock #9: Alliant Energy (LNT)

- 5-year expected annual returns: 11.7%

Alliant Energy Corporation is a public utility holding company incorporated in Madison, Wisconsin, in 1981. In 2022, Alliant Energy generated $3.4 billion in operating revenues. The company serves approximately 970,000 electric and 420,000 natural gas customers. Alliant has about 3,600 employees.

On November 2rd, 2023, Alliant Energy reported third-quarter results for Fiscal Year (FY) 2023. The company reported robust financial performance for Q3 2023, revealing a GAAP earnings per share (EPS) of $1.02, up from $0.90 in Q3 2022. The company also outlined its financial outlook, projecting an EPS range of $2.99 to $3.13 for 2024, accompanied by a common stock dividend target of $1.92. Additionally, Alliant Energy anticipates capital expenditures totaling $9 billion for the years 2024 to 2027.

Click here to download our most recent Sure Analysis report on LNT (preview of page 1 of 3 shown below):

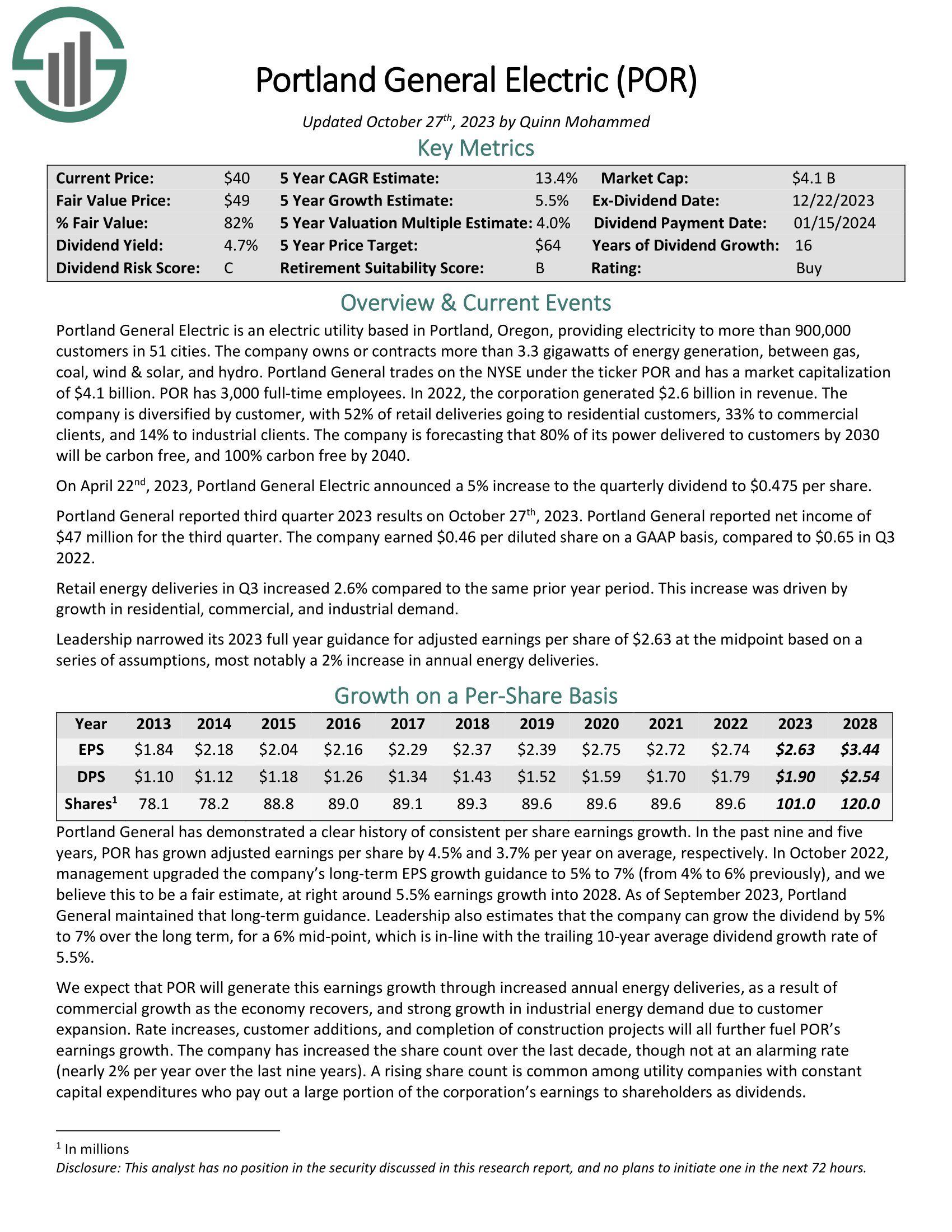

Top Utility Stock #8: Portland General Electric Company (POR)

- 5-year expected annual returns: 11.9%

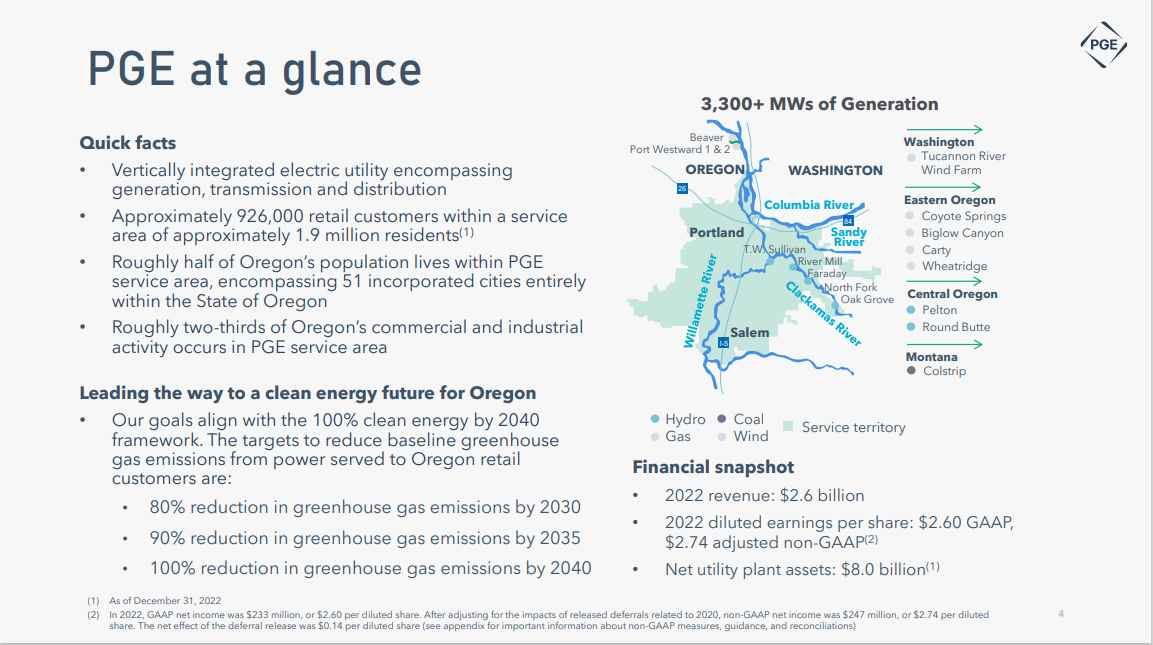

Portland General Electric is an electric utility based in Portland, Oregon, providing electricity to more than 900,000 customers in 51 cities. The company owns or contracts more than 3.3 gigawatts of energy generation, between gas, coal, wind & solar, and hydro.

Source: Investor Presentation

The company is diversified by customer, with 52% of retail deliveries going to residential customers, 33% to commercial clients, and 14% to industrial clients. The company is forecasting that 80% of its power delivered to customers by 2030 will be carbon free, and 100% carbon free by 2040.

Portland General reported third quarter 2023 results on October 27th, 2023. Portland General reported net income of $47 million for the third quarter. The company earned $0.46 per diluted share on a GAAP basis, compared to $0.65 in Q3 2022. Retail energy deliveries in Q3 increased 2.6% compared to the same prior year period. This increase was driven by growth in residential, commercial, and industrial demand.

Click here to download our most recent Sure Analysis report on Portland General Electric Company (preview of page 1 of 3 shown below):

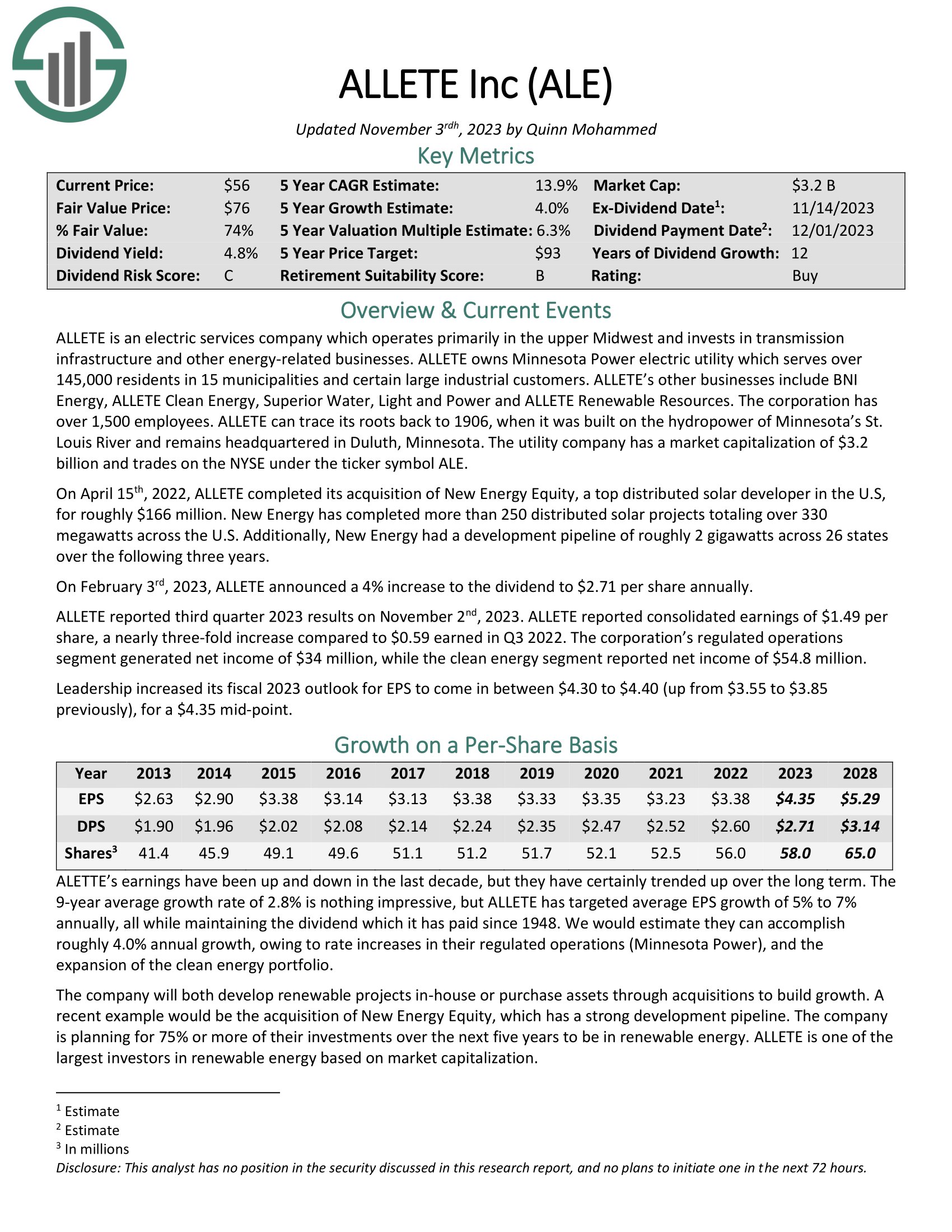

Top Utility Stock #7: ALLETE, Inc. (ALE)

- 5-year expected annual returns: 12.3%

ALLETE is an electric services company which operates primarily in the upper Midwest and invests in transmission infrastructure and other energy-related businesses. ALLETE owns Minnesota Power electric utility which serves over 145,000 residents in 15 municipalities and certain large industrial customers. ALLETE’s other businesses include BNI Energy, ALLETE Clean Energy, Superior Water, Light and Power and ALLETE Renewable Resources.

ALLETE reported third quarter 2023 results on November 2nd, 2023. ALLETE reported consolidated earnings of $1.49 per share, a nearly three-fold increase compared to $0.59 earned in Q3 2022. The corporation’s regulated operations segment generated net income of $34 million, while the clean energy segment reported net income of $54.8 million.

Click here to download our most recent Sure Analysis report on Allete, Inc. (preview of page 1 of 3 shown below):

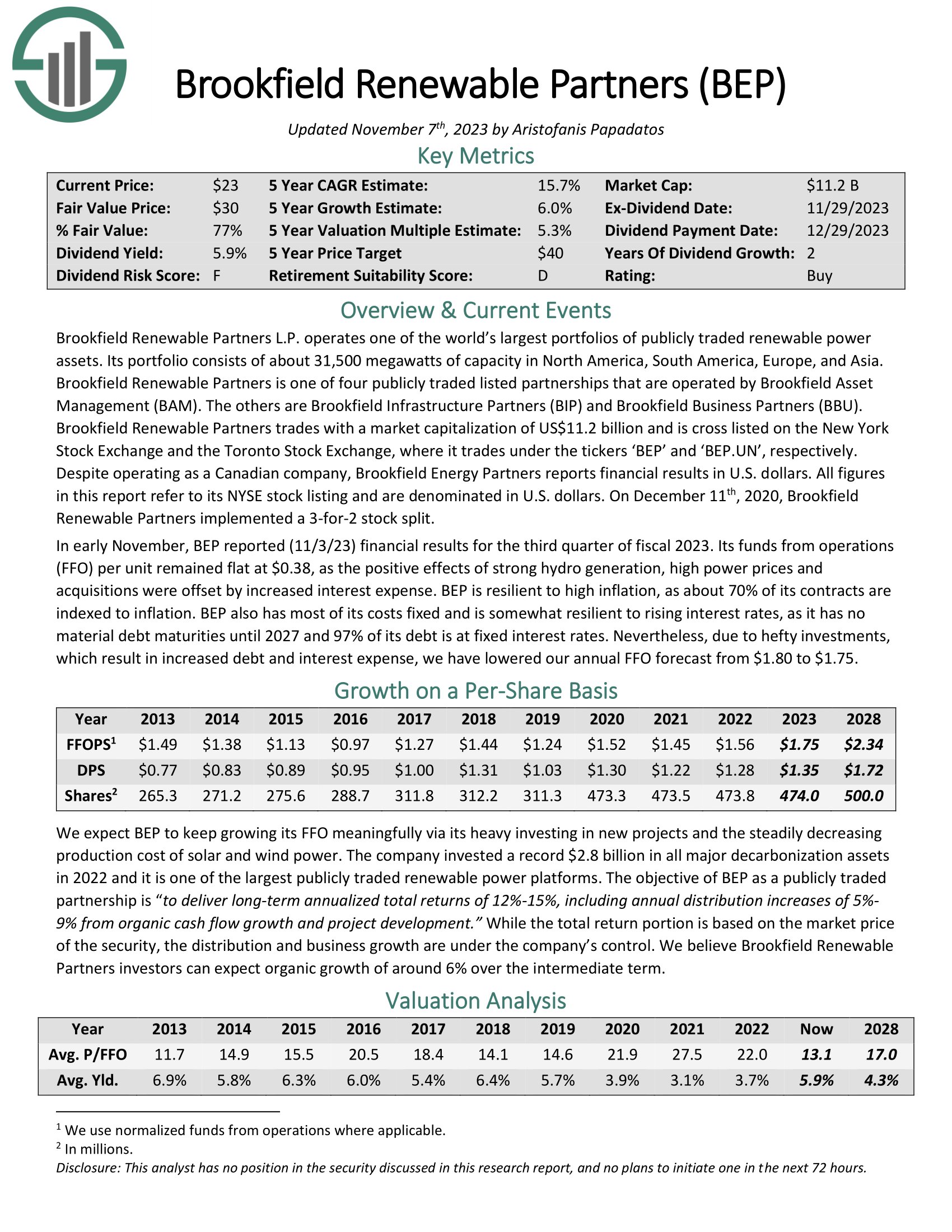

Top Utility Stock #6: Brookfield Renewable Partners LP (BEP)

- 5-year expected annual returns: 12.8%

Brookfield Renewable Partners is one of four publicly traded listed partnerships that are operated by Brookfield Asset Management (BAM). The others are Brookfield Infrastructure Partners (BIP) and Brookfield Business Partners (BBU). Brookfield Renewable Partners trades with a market capitalization of $11.6 billion and is cross listed on the New York Stock Exchange and the Toronto Stock Exchange, where is trades under the tickers ‘BEP’ and ‘BEP.UN’.

In early November, BEP reported (11/3/23) financial results for the third quarter of fiscal 2023. Its funds from operations (FFO) per unit remained flat at $0.38, as the positive effects of strong hydro generation, high power prices and acquisitions were offset by increased interest expense. BEP is resilient to high inflation, as about 70% of its contracts are indexed to inflation. BEP also has most of its costs fixed and is somewhat resilient to rising interest rates, as it has no material debt maturities until 2027 and 97% of its debt is at fixed interest rates.

Click here to download our most recent Sure Analysis report on Brookfield Renewable Partners (preview of page 1 of 3 shown below):

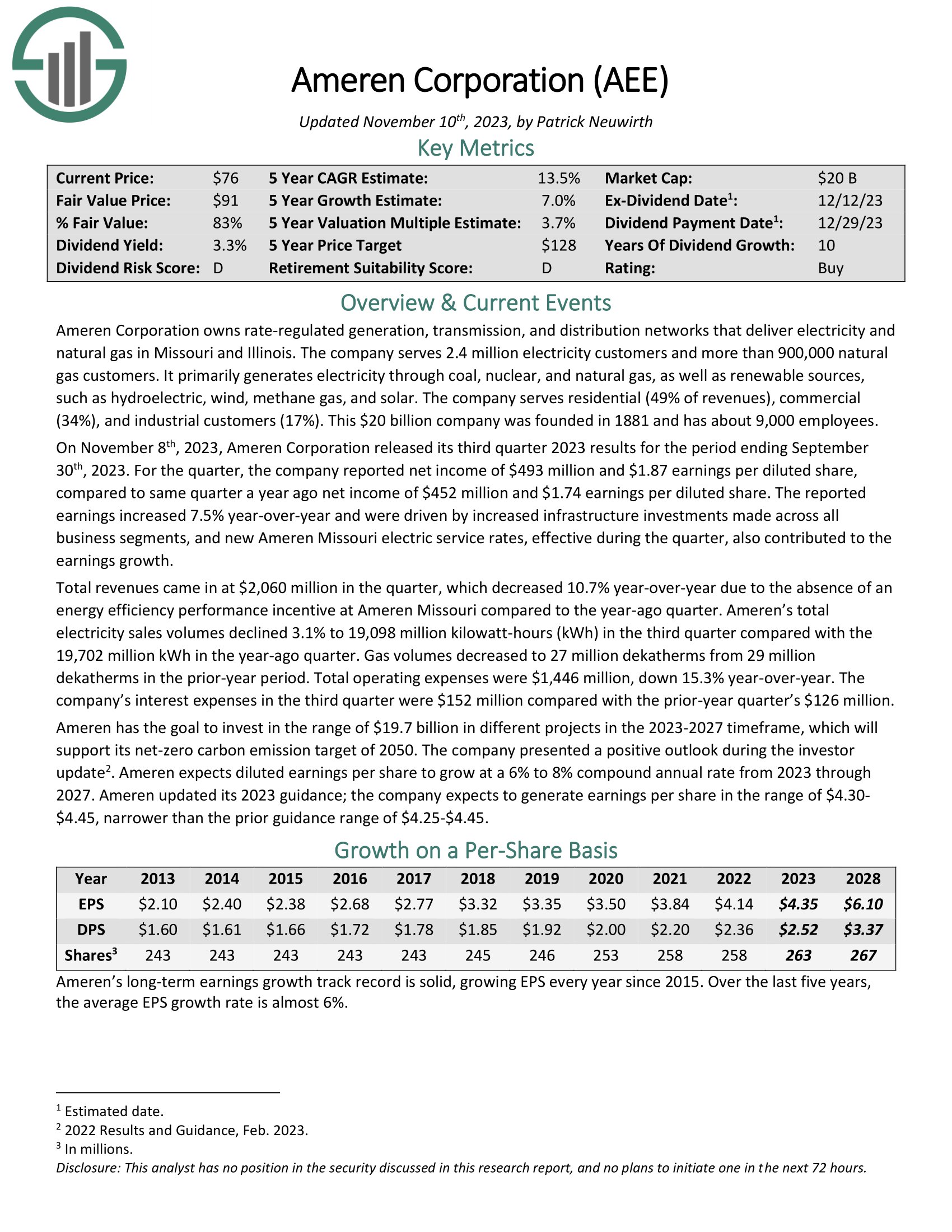

Top Utility Stock #5: Ameren Corporation (AEE)

- 5-year expected annual returns: 14.9%

Ameren Corporation owns rate-regulated generation, transmission, and distribution networks that deliver electricity and natural gas in Missouri and Illinois. The company serves 2.4 million electricity customers and more than 900,000 natural gas customers.

It primarily generates electricity through coal, nuclear, and natural gas, as well as renewable sources, such as hydroelectric, wind, methane gas, and solar. The company serves residential (49% of revenues), commercial (34%), and industrial customers (17%). This $20 billion company was founded in 1881 and has about 9,000 employees.

On November 8th, 2023, Ameren Corporation released its third quarter 2023 results for the period ending September 30th, 2023. For the quarter, the company reported net income of $493 million and $1.87 earnings per diluted share, compared to same quarter a year ago net income of $452 million and $1.74 earnings per diluted share.

The reported earnings increased 7.5% year-over-year and were driven by increased infrastructure investments made across all business segments, and new Ameren Missouri electric service rates, effective during the quarter, also contributed to the earnings growth.

Click here to download our most recent Sure Analysis report on AEE (preview of page 1 of 3 shown below):

Top Utility Stock #4: Brookfield Infrastructure Partners L.P. (BIP)

- 5-year expected annual returns: 15.2%

Brookfield Infrastructure Partners is one of the largest global owners and operators of infrastructure networks that includes operations ins sectors such as energy, water, freight, passengers, and data. Brookfield Infrastructure Partners is one of four publicly-traded listed partnerships that is operated by Brookfield Asset Management. Brookfield Infrastructure Corp (BIPC) was spun off in early 2020 for investors who prefer to invest in a corporation.

BIP reported solid Q3 2023 results on 11/1/23. Funds from operations rose 6.7% year over year to $560 million, supported by strong base business performance and the contribution of ~$1 billion of capital deployed in new acquisitions over the past year, partially offset by the impact of nearly $2 billion in asset sales. Organic growth was near the high-end of its 6-9% target range, benefiting from elevated levels of inflation across its transport and utilities segments. FFO per unit climbed 7.4% to $0.73.

Click here to download our most recent Sure Analysis report on Brookfield Infrastructure Partners (preview of page 1 of 3 shown below):

Top Utility Stock #3: Evergy Inc. (EVRG)

- 5-year expected annual returns: 15.3%

Evergy is an electric utility holding company incorporated in 2017 and headquartered in Kansas City, Missouri. Through its subsidiaries Evergy Kansas, Evergy Metro and Evergy Missouri West, the company serves approximately 1.4 million residential customers, nearly 200,000 commercial customers and 6,900 industrial customers and municipalities in Kansas and Missouri.

In early November, Evergy reported (11/7/23) financial results for the third quarter of fiscal 2023. The company was hurt by unfavorable weather, lower weather-normalized demand and higher interest expense and depreciation. As a result, its adjusted earnings-per-share dipped -6% over the prior year’s quarter, from $2.00 to $1.88, though they exceeded the analysts’ consensus by $0.04.

Click here to download our most recent Sure Analysis report on Evergy Inc. (preview of page 1 of 3 shown below):

Top Utility Stock #2: Eversource Energy (ES)

- 5-year expected annual returns: 17.3%

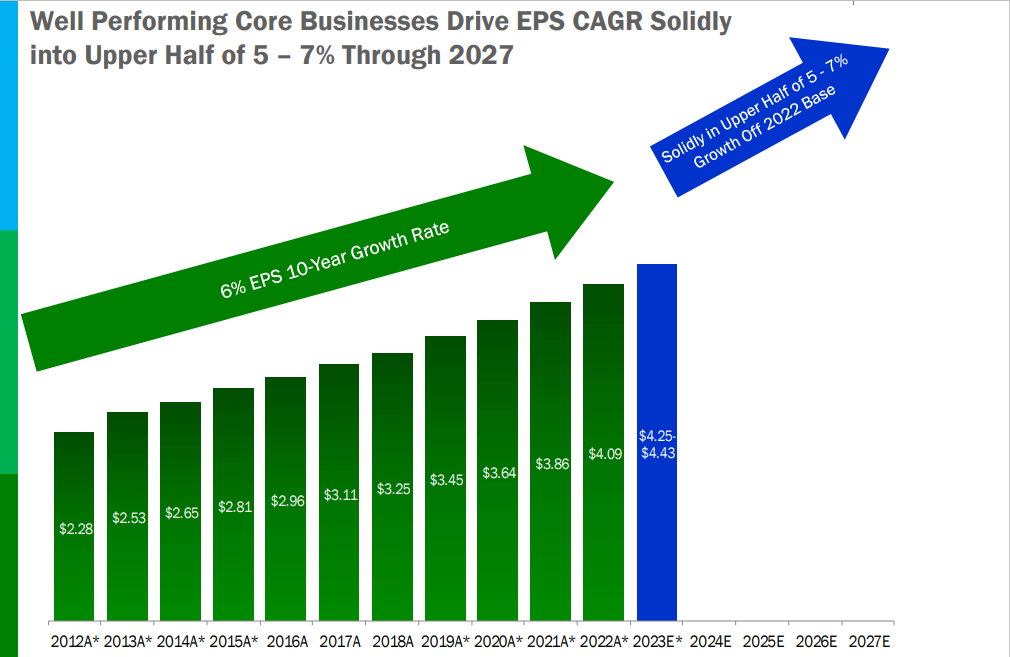

Eversource Energy is a diversified holding company with subsidiaries that provide regulated electric, gas, and water distribution service in the Northeast U.S. The company’s utilities serve more than 4 million customers after acquiring NStar’s Massachusetts utilities in 2012, Aquarion in 2017, and Columbia Gas in 2020.

Eversource has a long history of generating steady growth over time.

Source: Investor Presentation

On November 6th, 2023, Eversource Energy released its third quarter 2023 results for the period ending September 30th, 2023. For the quarter, the company reported revenue of $2.79 billion, a decrease of 13.2% compared to $3.22 billion in the same quarter of last year. The company reported earnings of $339.7 million and earnings-per-share of $0.97 compared with earnings of $349.4 million and earnings-per-share of $1.00 in the prior year.

The company reported earnings of $15 million and earnings-per-share of $0.04 compared with earnings of $292 million and earnings-per-share of $0.84 in the prior year.

Click here to download our most recent Sure Analysis report on ES (preview of page 1 of 3 shown below):

Top Utility Stock #1: NextEra Energy Partners LP (NEP)

- 5-year expected annual returns: 19.7%

NextEra Energy Partners was formed in 2014 as Delaware Limited Partnership by NextEra Energy to own, operate, and acquire contracted clean energy projects with stable, long-term cash flows. The company’s strategy is to capitalize on the energy industry’s favorable trends in North America of clean energy projects replacing uneconomic projects.

NextEra Energy Partners operates 34 contracted renewable generation assets consisting of wind and solar projects in 12 states across the United States. The company also operates contracted natural gas pipelines in Texas which accounts for about a fifth of NextEra Energy Partners’ income.

On October 24, 2023, NextEra Energy Partners released its earnings report for the third quarter of 2023. The company reported quarterly earnings of $0.57 per share, surpassing the consensus estimate of $0.48 per share, but falling short of the $0.93 per share reported a year ago.

Click here to download our most recent Sure Analysis report on NEP (preview of page 1 of 3 shown below):

Final Thoughts

The utility sector is a great place to find high-quality dividend stocks suitable for long-term investment.

It is not, however, the only place to find attractive investments.

If you’re willing to venture outside of the utility industry for investment opportunities, the following Sure Dividend databases are very useful:

- The Dividend Aristocrats: dividend growth stocks with 25+ years of consecutive dividend increases

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 54 stocks with 50+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks: Monthly dividend stocks with the highest current yields.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Complete List of Russell 2000 Stocks: arguably the world’s best-known benchmark for small-cap U.S. stocks.

- The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

If you’re looking for other sector-specific dividend stocks, the following Sure Dividend databases will be useful:

- The Complete List Of Technology Stocks

- The Complete List Of Communication Services Stocks

- The Complete List Of Consumer Staples Stocks

- The Complete List Of Consumer Discretionary Stocks

- The Complete List Of Healthcare Stocks

- The Complete List Of Financial Stocks

- The Complete List Of Real Estate Stocks

- The Complete List Of Energy Stocks

- The Complete List Of Materials Stocks

- The Complete List Of Industrial Stocks