Updated on February 14th, 2023 by Nathan Parsh

The Dividend Aristocrats consist of companies that have raised their dividends for at least 25 years in a row. Many of the companies have turned into huge multinational corporations over the decades, but not all of them. You can see the full list of all 68 Dividend Aristocrats here.

We created a full list of all Dividend Aristocrats, along with important financial metrics like price-to-earnings ratios and dividend yields. You can download your copy of the Dividend Aristocrats list by clicking on the link below:

Emerson Electric (EMR) has raised its dividend for 65 consecutive years, and thus it has one of the longest dividend growth streaks in the investing universe. This also qualifies the company as a Dividend King. There are only four companies that have longer dividend growth streaks than Emerson.

The company has achieved such an exceptional dividend growth record thanks to its strong business model, its decent resilience to downturns and its somewhat conservative payout ratio. These factors provide a margin of safety during recessions. In this article, we’ll review Emerson’s prospects as an investment today.

Business Overview

Emerson Electric was founded in Missouri in 1890. Since then, it has evolved from a regional manufacturer of electric motors and fans into a technology and engineering company, providing solutions to industrial, commercial and individual customers.

It is a global leader with a presence in more than 150 countries, and operates in two segments: Automation Solutions and Commercial & Residential Solutions.

The Automation Solutions segment, which generates ~65% of the total revenue, offers industrial equipment and software to the oil and gas industry, refining, power generation as well as other industries.

The Commercial & Residential Solutions segment, which generates the remaining 35% of the total revenue, offers residential and commercial heating and air conditioning products.

Emerson generates the majority of its revenue from the oil and gas industry. As this industry is infamous for the dramatic swings of commodity prices, Emerson is highly sensitive to the industry cycles.

This helps explain the 34% decrease in Emerson’s earnings per share from 2014 to 2016, which coincided with the fierce downturn in the energy sector caused by the collapse of oil and gas prices during that period.

Emerson faced another downturn in 2020, due to the coronavirus crisis. The pandemic caused a collapse in global demand for industrial products this year, which in turn caused a major downturn in the energy sector.

Fortunately, business conditions have improved in the near-term as the global economy has recovered from the pandemic.

Source: Investor Presentation

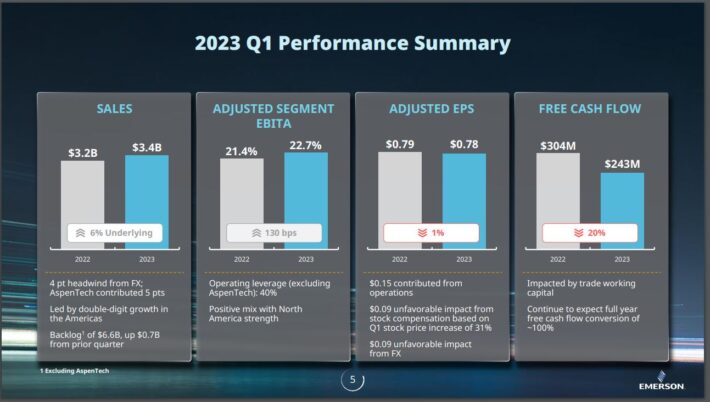

Emerson reported first quarter earnings on February 8th, 2023, and results were mixed. Adjusted earnings-per-share came to $0.78, which compared unfavorably to $1.05 in the prior year was $0.09 less than expected. Revenue did grow almost 7% to $3.37 billion, but this was $60 million below estimates.

Pretax operating margin was 12.5% of revenue, which was down 1730 basis points from the prior year.

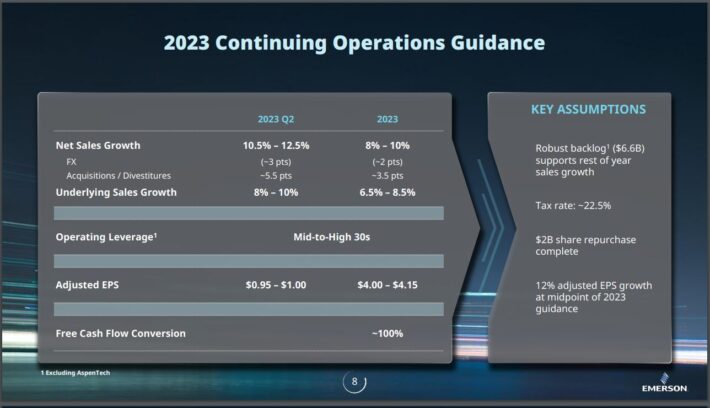

Emerson did provide an outlook for the remainder of the year as well.

Source: Investor Presentation

Net sales growth is expected to be in the low double-digit for the current quarter, with full year guidance expecting solid gains as well. Adjusted earnings-per-share are projected to be in a range of $4.00 to $4.15 for fiscal year 2023, which would be lower by 23% from the prior fiscal year.

Growth Prospects

Emerson has pursued growth by expanding its customer base but also by acquiring many companies. In fact, the company acquires and divests parts of its business regularly to create an optimal portfolio mix.

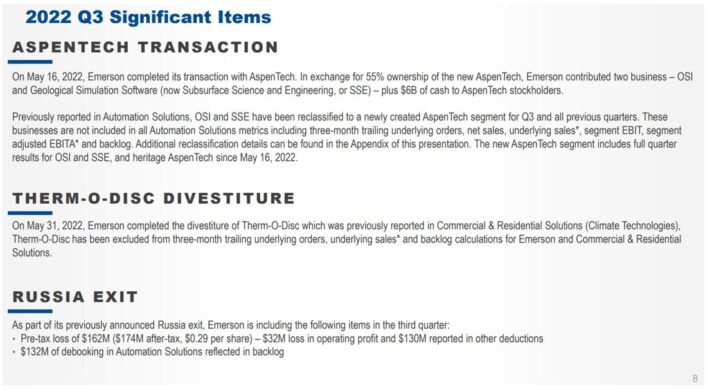

The company was quite busy on this front last fiscal year.

Source: Investor Presentation

The Aspentech transaction is huge for Emerson, and gives the acquirer access to Aspentech’s double-digit annual earnings growth. In addition, Emerson divested its Therm-O-Disc business, and sold its Russia business following that country’s invasion of Ukraine.

More recently, Emerson announced publicly that they had increased their offer to buy National Instruments (NATI), a computer hardware company, for $53 per share.

That said, it is critical to note that Emerson only managed marginal earnings-per-share growth from 2011 to 2020. This is a reminder of Emerson’s dependence on the oil and gas industry, which is highly cyclical. This exposure can bring extraordinary returns during booming years but it can also erase many years of growth during a severe downturn. Emerson is trying to diversify away from this, and that has driven many portfolio actions in recent years. We believe this diversification is critical to Emerson’s future success.

Thanks to its recent acquisitions and modest organic growth, we expect Emerson to grow its earnings per share at a 6.0% average annual rate over the next five years. This growth will be comprised partly of revenue growth, but also share repurchases.

Competitive Advantages & Recession Performance

As Emerson has served its customers for several decades, it has built great expertise in the markets it serves. In addition, thanks to its large scale and its dominant global presence, it has a great reputation. This provides the company with a significant competitive advantage.

On the other hand, due to its reliance on industrial and commercial customers, Emerson is vulnerable to recessions and downturns in the energy sector. In the Great Recession, its earnings per share were as follows:

- 2007 earnings-per-share of $2.66

- 2008 earnings-per-share of $3.11 (17% increase)

- 2009 earnings-per-share of $2.27 (27% decline)

- 2010 earnings-per-share of $2.60 (15% increase)

- 2011 earnings-per-share of $3.24 (25% increase)

Emerson got through the Great Recession with just one year of decline in its earnings per share. That performance was certainly impressive.

Emerson was more heavily affected in the downturn of the energy sector, which was caused by the collapse of the price of oil from $100 in mid-2014 to $26 in early 2016. Its earnings per share decreased 34%, from $3.75 in 2014 to $2.46 in 2016, and only eclipsed that level for the first time in 2021.

Given its sensitivity to the economic cycles, it is impressive that Emerson has grown its dividend for 65 consecutive years. The exceptional dividend record can be attributed to the aforementioned decent resilience of the company during downturns.

Another reason is the conservative payout ratio, which should come in at about 40% for this year, which provides a material margin of safety to the dividend during economic downturns.

Valuation & Expected Returns

Based on expected adjusted EPS of $4.08 for fiscal 2023, Emerson is currently trading at 21.1 times its expected EPS. This earnings multiple is above our estimate of fair value at 19 times earnings. This implies a 2.1% annual headwind should it reach 19 times earnings again.

Therefore, we project total annual returns of 6% over the next five years, as 6% earnings growth and the starting yield of 2.4% are partially offset by a low single-digit headwind from multiple reversion.

Final Thoughts

Emerson has an impressive dividend growth record, particularly given its heavy reliance on industrial and commercial customers, who struggle during recessions or downturn in the energy sector. The strong dividend yield of the stock and its reliable dividend growth render the stock suitable for some income-oriented investors.

We see the stock as somewhat overvalued today. While the dividend growth streak is notable, the total return potential for the stock is mediocre at this point. As a result, Emerson earns a hold rating due to projected returns.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

- The 2022 High ROIC Stocks List: The top 10 stocks with high returns on invested capital.

- The 2022 High Beta Stocks List: The 100 stocks in the S&P 500 Index with the highest beta.

- The 2022 Low Beta Stocks List: The 100 stocks in the S&P 500 Index with the lowest beta.

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: