Updated on February 10th, 2023 by Nathan Parsh

The Dividend Aristocrats are among the highest-quality dividend growth stocks an investor can buy. The Dividend Aristocrats have increased their dividends for 25+ consecutive years.

Becoming a Dividend Aristocrat is no small feat. Beyond certain market capitalization and trading volume requirements, Dividend Aristocrats must have raised their dividends each year for at least 25 years, and be included in the S&P 500 Index.

This presents a high hurdle that relatively few companies can clear. For example, there are currently 68 Dividend Aristocrats out of the 500 companies that comprise the S&P 500 Index.

We created a complete list of all 68 Dividend Aristocrats, along with important financial metrics like dividend yields and price-to-earnings ratios. You can download an Excel spreadsheet of all 68 Dividend Aristocrats by clicking the link below:

An even smaller group of stocks have raised their dividends for 50+ years in a row. These are known as the Dividend Kings.

Genuine Parts (GPC) has increased its dividend for 66 consecutive years, giving it one of the longest dividend growth streaks in the market. You can see all 48 Dividend Kings here.

There is nothing overly exciting about Genuine Parts’ business model, but its steady annual dividend increases prove that a “boring” business can be just what income investors need for long-term dividend growth.

Business Overview

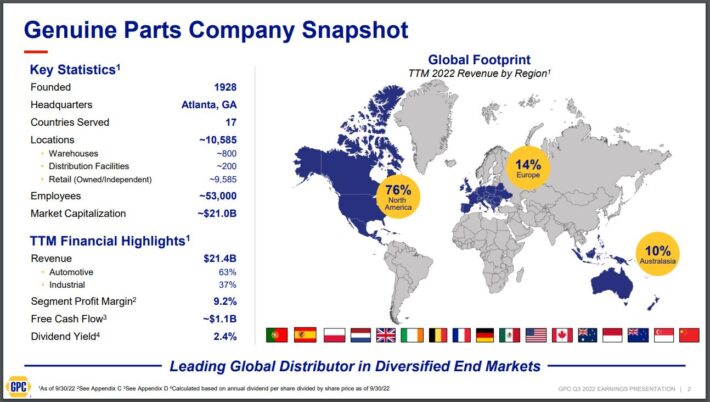

Genuine Parts traces its roots back to 1928 when Carlyle Fraser purchased Motor Parts Depot for $40,000. He renamed it, Genuine Parts Company. The original Genuine Parts store had annual sales of just $75,000 and only 6 employees.

Today, Genuine Parts has the world’s largest global auto parts network. Genuine Parts generated $18.9 billion in annual revenue. Genuine Parts is a distributor of automotive replacement parts, industrial replacement parts, office products, and electrical materials.

Source: Investor Presentation

It operates four segments, led by automotive parts, which houses the NAPA brand.

The industrial parts group sells industrial replacement parts to MRO (maintenance, repair, and operations) and OEM (original equipment manufacturer) customers. Customers are derived from a wide range of segments, including food and beverage, metals and mining, oil and gas, and health care.

The office products segment distributes business products in the U.S. and Canada. Customers include office products dealers, office supply stores, college bookstores, office furniture dealers, and more.

Genuine Parts also distributes electrical and electronic materials to original equipment manufacturers and industrial assembly firms.

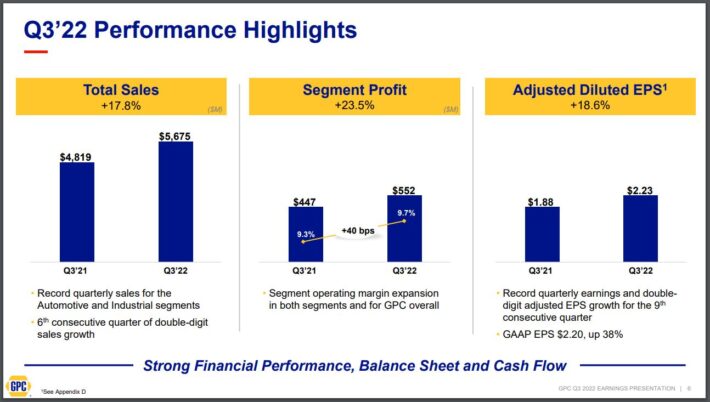

Genuine Parts reported third quarter earnings results on October 20th, 2022.

Source: Investor Presentation

Revenue was $5.68 billion in Q3, up 17.8% from the same period a year ago. The improvement is attributable to a 12.7% increase in comparable sales and a 9.1% benefit from acquisitions, partially offset by a 4% headwind from unfavorable currency exchange.

Net income from continuing operations came to $312 million on an adjusted basis, up from $229 million in the same period of 2021. On a per-share basis, earnings were $2.20, up 38% from $1.59 in the year-ago period.

2020 was a difficult year for Genuine Parts, as the coronavirus pandemic dragged the U.S. economy into recession. Still, Genuine Parts remained highly profitable during and after this period, which allowed it to continue raising its dividend. And, the meaningful improvement seen in the third quarter of the year bodes well for continued growth moving forward.

We expect Genuine Parts to earn $8.15 per share for 2022, which would be a nearly 18% improvement from the prior year.

Growth Prospects

Genuine Parts is primed for success, as the environment for auto replacement parts is highly positive. Consumers are holding onto their cars longer and are increasingly making minor repairs to keep cars on the road for longer, rather than buying new cars. As average costs of vehicle repair increase as the car ages, this directly benefits Genuine Parts.

According to Genuine Parts, vehicles aged six years or older now represent over ~70% of cars on the road. This bodes very well for Genuine Parts.

In addition, the market for automotive aftermarket products and services is significant. Genuine Parts has a sizable portion of the $200 billion and growing automotive aftermarket business.

One way Genuine Parts has captured market share in this space has historically been acquisitions. It frequently acquires smaller companies, in the U.S. and in the international markets, to boost market share in existing categories or expand in new areas. Genuine Parts has made several acquisitions over the course of its history.

For example, Genuine Parts acquired Alliance Automotive Group for $2 billion. Alliance is a European distributor of vehicle parts, tools, and workshop equipment. This was an attractive acquisition, as Alliance Automotive holds a top 3 market share position in Europe’s largest automotive aftermarkets: the U.K., France, and Germany.

Deals completed over the past few years have added significantly to Genuine Parts’ annual sales and profits. The company has consistently generated growth over the long term. Future earnings growth is still attainable, through organic growth, acquisitions, and share repurchases.

More recently, Genuine Parts completed its $1.3 billion all-cash purchase of Kaman Distribution Group, which is a leading power transmission, automation, and fluid power company, on January 4th, 2022.

This deal added meaningfully to Q3 results.

We expect 8% annual EPS growth over the next five years for Genuine Parts.

Competitive Advantages & Recession Performance

The biggest challenge facing the retail industry right now, is the threat of e-commerce competition. But automotive parts retailers such as NAPA are not exposed to this risk.

Automotive repairs are often complex, challenging tasks. NAPA is a leading brand, thanks in part to its reputation for quality products and service. It is valuable for customers to be able to ask questions to qualified staff, which gives Genuine Parts a competitive advantage.

Genuine Parts has a leadership position across its businesses. All four of its operating segments represent the #1 or #2 brand in its respective category. This leads to a strong brand, and steady demand from customers.

Genuine Parts’ earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share of $2.98

- 2008 earnings-per-share of $2.92 (2.0% decline)

- 2009 earnings-per-share of $2.50 (14% decline)

- 2010 earnings-per-share of $3.00 (20% increase)

Earnings-per-share declined significantly in 2009, which should come as no surprise. Consumers tend to tighten their belts when the economy enters a downturn.

That said, Genuine Parts remained highly profitable throughout the recession, and returned to growth in 2010 and beyond. The company remained highly profitable in 2020, despite the economic damage caused by the coronavirus pandemic. There will always be a certain level of demand for automotive parts, which gives Genuine Parts’ earnings a high floor.

Valuation & Expected Returns

Based on the most recent closing price of ~$173 and our expectation for 2022 earnings-per-share of $8.15, Genuine Parts has a price-to-earnings ratio of 21.2. Our fair value estimate for Genuine Parts is a price-to-earnings ratio of 18. As a result, Genuine Parts is overvalued at the present time. Multiple contraction would negatively impact future returns by 3.2% per year over the next five years.

Genuine Parts’ future earnings growth and dividends will more than offset this potential headwind.

We expect Genuine Parts to grow its earnings-per-share by 8% annually over the next five years. The stock also has a 2.1% current yield, which is higher than the average yield of the S&P 500 Index. And, Genuine Parts raises its dividend each year, including a recent 9.8% increase in February of 2022.

Genuine Parts has a highly sustainable dividend. The company has paid a dividend every year since it went public in 1948. The dividend is likely to continue growing for many years to come. That said, investors should also consider the impact of valuation when it comes to a stock’s total returns.

Genuine Parts’ total annual returns would consist of the following:

- 8% earnings growth

- 2.1% dividend yield

- -3.2% valuation reversion

In total, Genuine Parts is expected to offer a total annual return of 6.5% over the next five years. This is a mediocre rate of return in our opinion despite the company’s impressive dividend growth streak. Shares earn a hold rating as a result of potential returns.

Final Thoughts

Genuine Parts does not get much coverage in the financial media. It is far from the high-flying tech startups that typically receive more attention. However, Genuine Parts is a very appealing stock for investors looking for stable profitability and reliable dividend growth.

The company has a long runway of growth ahead, due to favorable industry dynamics. It should continue to raise its dividend each year, as it has for the past 66 years.

Given its history of dividend growth, Genuine Parts is suitable for investors desiring income, as well as steady dividend increases each year. Investors looking for more in the way of total returns will likely want to wait for a more attractive entry point.

If you are interested in finding more high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The 20 Highest Yielding Dividend Aristocrats

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 40 stocks with 50+ years of consecutive dividend increases.

- The 20 Highest Yielding Dividend Kings

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The 20 Highest Yielding Monthly Dividend Stocks

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: