Updated on January 31st, 2023 by Samuel Smith

The Dividend Aristocrats prove that when it comes to investing, boring isn’t always a bad thing. The Dividend Aristocrats are a group of 68 companies in the S&P 500 Index that have at least 25 consecutive years of dividend increases.

We are big fans of the Dividend Aristocrats and believe investors can generate superior returns from these high-quality dividend stocks. For this reason, we created a full spreadsheet of all 68 Dividend Aristocrats–complete with important financial metrics that matter most to investors–which you can download by clicking the link below:

We review all 68 Dividend Aristocrats on a yearly basis. The next stock in the series is industrial manufacturer Pentair plc (PNR).

Pentair does not have an exciting business model. It most likely will not be featured as the next hot growth stock any time soon. Instead, it is a slow-and-steady dividend stock that has created substantial shareholder wealth over the past several decades.

Pentair has increased its dividend for a very impressive 47 years in a row. It last increased its dividend by 4.8% in December 2022. The company’s dividend is also very safe. Pentair is a high-quality business, which provides investors with steady dividend growth.

Business Overview

Pentair is based in the U.K. but has large operations across Europe and in the U.S., among other international regions. The company was formed in 1966. In 1968, Pentair acquired Peavey Paper Mills, which gave it a top position in paper products. Paper fueled the company’s growth over the next decade, until management decided to diversify into other product categories.

Pentair’s first investment outside of paper products was the acquisition of Porter-Cable, a manufacturer of portable electronic power tools. In the decades since, Pentair has continued to diversify its product line with bolt-on acquisitions.

The company recently spun off its Technical Solutions business and now operates as a pure-play water solutions company. The pure-play water company now generates just over $4.1 billion in revenue and focuses on improving the availability and quality of water.

The spin-off was competed in the second quarter of 2018 and the new business is now called nVent Electric, trading under the ticker NVT. After the spin-off, Pentair now operates as a pure-play water solutions company that operates in 3 segments: Pool, Water Solutions, and Industrial & Flow Technologies.

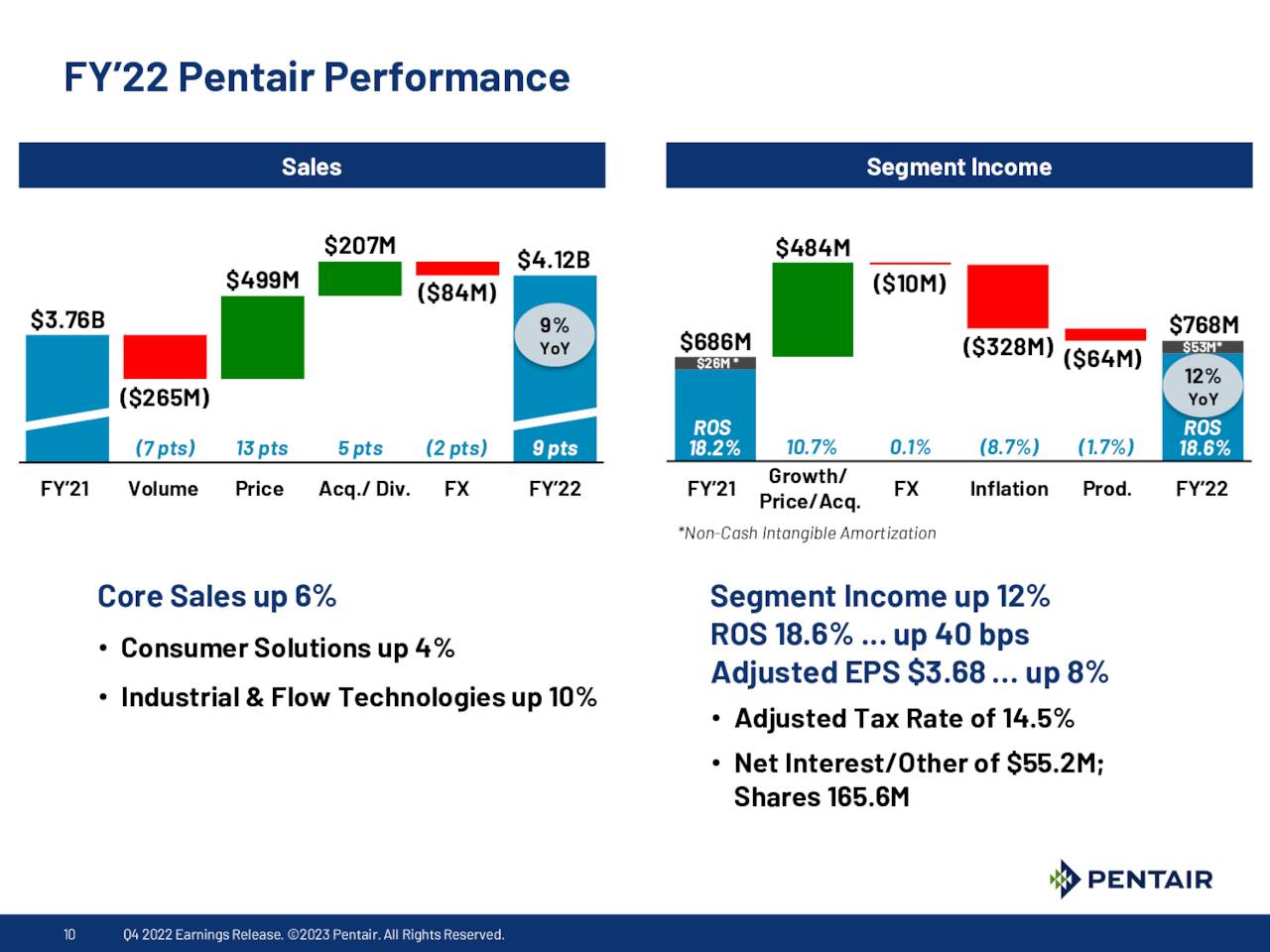

2022 was another year of growth for Pentair.

Source: Investor Presentation

Pentair reported its fourth-quarter and full year earnings results on January 31st. Quarterly revenue of $1 billion increased 1% year-over-year. Core sales (excluding currency, acquisitions, and divestments) decreased 3% for the quarter. Earnings-per-share decreased 6% for the quarter. For the full year, earnings-per-share increased 8% to $3.68.

The company expects 2023 to be year of poor growth, with EPS expected in a range of $3.50 to $3.70. At the midpoint, EPS would decline 2.2% in 2023.

Growth Prospects

Between 2008 and 2017 (before the nVent spin-off) Pentair grew its earnings-per-share by 5.5% annually. Adjusted for the impact of the last financial crisis – an unusually harsh recession which made Pentair’s earnings-per-share decline by slightly more than 30% between 2008 and 2009 – Pentair’s long-term earnings-per-share growth rate would have been even higher.

Pentair management believes that a long-term earnings-per-share growth rate of 10% is possible, but we are a bit more conservative. We believe it is better to expect a 6% earnings-per-share growth rate from Pentair over the coming years.

The company should be able to achieve this growth through rising revenues, which will be possible thanks to organic growth and acquisitions, and through tailwinds from margin expansion and share repurchases, which will lead to further declines in Pentair’s share count.

Pentair will benefit from a number of structural tailwinds, such as the aging water infrastructure in the U.S. Pentair continues to see very strong organic growth on a consolidated basis as Aquatic Systems performs well. Acquisitions will also help boost the company’s growth.

Competitive Advantages & Recession Performance

One of the competitive factors that has fueled Pentair’s impressive growth is its lean cost structure. This is no accident; Pentair has employed a strategy called Pentair Integrated Management System, or PIMS, which has enabled its high profit margins.

PIMS enables leaner manufacturing processes and drives efficiency throughout the company’s supply chain and distribution. Even though the effort is years old at this point, it continues to permeate the company’s strategy today. The impact is a culture and mindset with a relentless focus on cutting costs from its model.

Source: Investor Presentation

The PIMS is an organization-wide system. It effects talent management by providing employees with the proper incentives and providing all employees with individual responsibility down to the operator level.

Within the PIMS system, the ‘Lean Enterprise’ system helps to increase profit margins. It drives margin expansion by increasing productivity at manufacturing sites and helps identify acquisition targets with the highest cost savings opportunities.

Its competitive advantages and high margins allowed the company to remain profitable during the Great Recession during 2007-2009:

- 2007 earnings-per-share of $2.08

- 2008 earnings-per-share of $2.20 (5.8% increase)

- 2009 earnings-per-share of $1.47 (33% decline)

- 2010 earnings-per-share of $2.00 (36% increase)

As a global industrial manufacturer, Pentair is not immune from recessions. However, it quickly bounced back. Pentair’s earnings-per-share reached a new high in 2011. Given that Pentair is now a pure-play water treatment company, we expect the next recession will have a milder impact on the company’s earnings.

Pentair is now focused on services that can be considered needs and not wants, so we believe the company’s recession resistance has improved in recent years.

Valuation & Expected Returns

Based on expected earnings-per-share of $3.60 for 2023, Pentair has a price-to-earnings ratio of 15.4. Our fair value estimate is a P/E of 16, which is well below its 10-year average.

Given this, we see the stock as undervalued, and an increase in the price-to-earnings ratio could positively impact shareholder returns by 0.8% annually through 2028. Additionally, EPS growth (estimated at 6% per year) and the 1.7% dividend yield will contribute to total returns.

In total, we see annual returns of 8.5% accruing to shareholders of Pentair, consisting of the 1.7% dividend yield, 6% earnings-per-share growth, as well as a 0.8% positive return from an expanding valuation multiple.

An expected return near 8.5% is good but not great. Combine this with the very strong history of dividend increases, and Pentair appears to be a solid long-term investment. However, the yield of 1.7% may be unappealing for yield-focused investors.

Final Thoughts

Pentair has a strong business model, and competitive advantages. These qualities have fueled its steady dividend growth over the past four decades and we don’t see any reason to believe that won’t continue for many years to come.

Pentair shares are trading with a modest margin of safety and the company has a solid long-term outlook, culminating in estimated total annualized returns of 8.5%. The company should be able to continue increasing its dividend each year. As a result, we rate shares of Pentair a Hold right now and a buy on any meaningful dips.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: