Updated on February 13th, 2023 by Quinn Mohammed

For superior long-term returns, investors should focus on high-quality dividend growth stocks. This comes to mind when reviewing the Dividend Aristocrats, a select group of 68 companies in the S&P 500 Index with at least 25 consecutive years of dividend increases.

We have created a free Excel list of all 68 Dividend Aristocrats, along with relevant financial metrics such as P/E ratios and dividend payout ratios.

You can download the full list by clicking on the link below:

We review all 68 Dividend Aristocrats each year. The 2023 Dividend Aristocrats In Focus series continues with a review of beverage giant The Coca-Cola Company (KO).

Not only is Coca-Cola a Dividend Aristocrat, it is a Dividend King as well. The Dividend Kings have increased their dividends for 50+ consecutive years. You can see all the Dividend Kings here.

Coca-Cola has a dividend yield of 3.0%, which is considerably higher than the S&P 500 Index average yield of 1.6%. In addition, Coca-Cola is likely to continue raising its dividend each year.

But this is a difficult time for Coca-Cola given consumer preferences have been changing for years away from traditional sparkling beverages. Indeed, soda consumption continues to wane in the U.S, where the company’s market share is dominant. Because Coca-Cola’s earnings growth has slowed, the stock continues to appear overvalued. However, it remains a high-quality business with strong brands, and an attractive, growing dividend, and market-beating yield.

Related: Dogs of the Dow: the highest yielding Dow Jones 30 stocks.

In addition, it has been diversifying away from sparkling beverages in recent years and those efforts have paid off. This article will examine Coca-Cola’s investment prospects in detail.

Business Overview

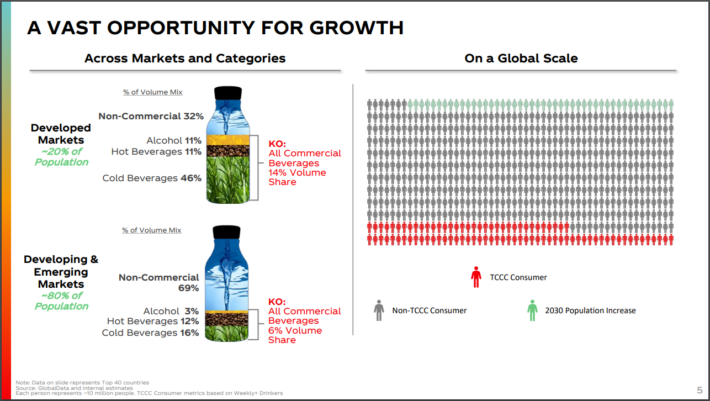

Coca-Cola is the world’s largest beverage company, as it owns or licenses more than 500 unique non-alcoholic brands and 200 master brands. Since the company’s founding in 1886, it has spread to more than 200 countries worldwide. It currently has a market capitalization of more than $257 billion, making it a mega-cap stock.

Its brands account for about 2 billion servings of beverages worldwide every day, producing more than $42 billion in annual revenue.

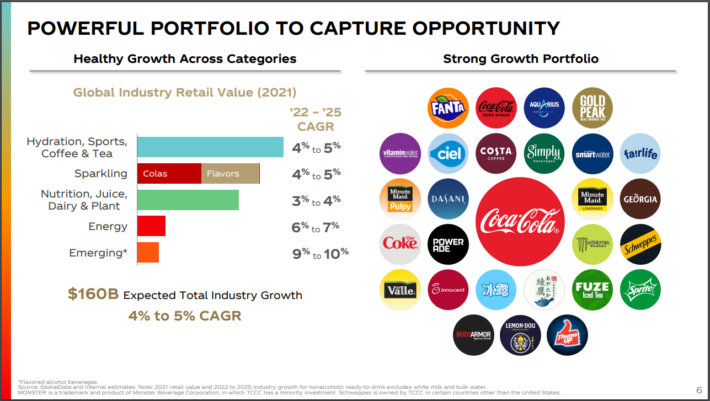

The sparkling beverage portfolio includes the flagship Coca-Cola brand, as well as other soda brands like Diet Coke, Sprite, Fanta, and more. The still beverage portfolio includes water, juices, coffee drinks, and ready-to-drink teas, such as Dasani, Minute Maid, Vitamin Water, and Honest Tea.

Source: Investor Relations

Coca-Cola dominates sparkling soft drinks. The company is attempting to maintain and even improve this dominant position with product extensions of existing popular brands, including reduced and zero-sugar versions of brands like Sprite and Fanta.

This is a challenging time for Coca-Cola. Sales of soda are slowing down in developed markets like the U.S., where soda consumption has steadily declined for years.

Declining soda consumption is a significant threat for the company. While Coca-Cola’s total volumes certainly still rely upon sparkling beverages such as soda, the company has gone to great lengths in recent years to diversify away from its core products, understanding that the long-term growth prospect for sparkling beverages isn’t particularly inspiring. Coca-Cola has acquired multiple still beverage brands in recent years.

Coca-Cola reported third quarter earnings on October 25th, 2022, and results were better than expected on both the top and bottom lines. Earnings-per-share on an adjusted basis $0.69, beating expectations by $0.05. Revenue was up 11% year-over-year to $11.1 billion, which was $600 million ahead of estimates.

Organic sales were up 16%, which was almost double the expected 9.8% gain.

Operating margin was 29.5% of sales, down from 30.0% year-over-year. This was a result of the BodyArmor acquisition, higher operating costs, and an increase in marketing investments.

The company expects organic revenue growth of 14% to 15% for this year. And we estimate $2.50 in earnings-per-share for 2022.

Growth Prospects

In an effort to return to growth, Coca-Cola has invested heavily outside of soda, in areas like juices, coffee, teas, dairy, and water, to appeal to changing consumer preferences. Due to the success of its growth initiatives, we continue to see Coca-Cola as having a favorable long-term growth outlook.

One reason we like the stock is because it competes in an industry that continues to grow globally in excess of the rate of broad economic growth. This leads to strong levels of overall growth in the industry, which Coca-Cola has certainly been capitalizing on in recent years.

In addition, the ready-to-drink category is sold through highly-diversified channels and continues to have mid-single digit projected growth rates, both for Coca-Cola and the industry. This is particularly true for still beverages like tea, coffee, and water. Coca-Cola’s years-old strategy to diversify away from sparkling beverages is due to this and it is undoubtedly bearing fruit.

Coca-Cola also continues to acquire brands in order to grow, including its acquisition of Costa, a coffee brand based in the UK.

Source: Investor Relations

This is certainly an out-of-the-box buy for a sparkling beverage behemoth, but Coca-Cola is doing what it takes to secure its future. In the relatively short time Coca-Cola has owned the coffee brand, it has expanded its offerings, including combining Coca-Cola and coffee in ready-to-drink packages.

Finally, we continue to like the divestiture of the company’s bottling operations. This has resulted in some pretty significant revenue declines over the years, but the end goal is much higher margins. Revenue turned higher during the pandemic, and margins are much higher than pre-divestiture.

Taking all of this into account, in addition to the company’s buyback program and productivity improvement efforts, we see total earnings-per-share growth of 6% annually over the next five years.

Competitive Advantages & Recession Performance

Coca-Cola enjoys two distinct competitive advantages, which are its strong brand and global scale. According to Forbes, Coca-Cola is the sixth-most valuable brand in the world, worth over $64 billion.

In addition, Coca-Cola has an unparalleled distribution network. It has the largest beverage distribution system in the world. A new entrant would be hard pressed to recreate this distribution system, even with billions of dollars to invest.

These advantages allow Coca-Cola to remain highly profitable, even during recessions. The company held up very well during the Great Recession:

- 2007 earnings-per-share of $1.29

- 2008 earnings-per-share of $1.51 (17% increase)

- 2009 earnings-per-share of $1.47 (3% decline)

- 2010 earnings-per-share of $1.75 (19% increase)

Not only did Coca-Cola survive the Great Recession, it thrived. Coca-Cola grew earnings-per-share by 36% from 2007-2010. This shows the durability and strength of Coca-Cola’s business model. The company’s dividend also appears very safe, even after 60 years of consecutive increases.

Coca-Cola remained profitable throughout the coronavirus pandemic, though earnings were negatively impacted as public venues closed. The company rebounded sharply though. We would expect Coca-Cola to perform well during any future recessions.

Valuation & Expected Returns

We expect Coca-Cola to generate adjusted EPS of $2.50 for 2022. Based on this, Coca-Cola stock trades for a price-to-earnings ratio of 23.8. This is above our fair value estimate of 23 times earnings, which means the stock is somewhat overvalued. A declining P/E multiple could reduce annual returns by -0.5% over the next five years.

The stock will generate positive returns through future earnings-per-share growth (estimated at 6%) plus the 3.0% dividend yield. Putting all of this together, we expect total annualized returns of 8.1% through 2027.

However, the stock is currently overvalued, the corresponding contraction of the valuation multiple is expected to reduce total returns over the next five years. The overall result is that we expect Coca-Cola stock to generate decent, albeit unspectacular, shareholder returns at the current share price, and we rate it a hold.

Final Thoughts

Coca-Cola has made great strides repositioning its portfolio to meet changing consumer tastes. It has built a large portfolio of juices, coffees, and teas, to cater to a more health-conscious consumer.

There is more work to be done to diversify away from sparkling beverages, and we see solid growth prospects looking ahead.

We rate the stock a hold since it is overvalued, but the stock remains a strong choice for income investors due to its above average dividend yield and long history of annual dividend increases. These qualities make Coca-Cola a time-tested Dividend Aristocrat, and a blue-chip stock.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Best DRIP Stocks: The top 15 Dividend Aristocrats with no-fee dividend reinvestment plans.

- The 2022 High ROIC Stocks List: The top 10 stocks with high returns on invested capital.

- The 2022 High Beta Stocks List: The 100 stocks in the S&P 500 Index with the highest beta.

- The 2022 Low Beta Stocks List: The 100 stocks in the S&P 500 Index with the lowest beta.

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: