Published on January 13th, 2023 by Josh Arnold

There are certain sectors of stocks that tend to lend themselves to being great sources of income. In general, low growth and low capex needs are generally characteristics of strong income stocks, because companies with those characteristics lack ample growth investment opportunities for their capital. That frees the management team up to instead return capital to shareholders via dividends. Financials are a great source of dividend stocks, but there is more to finance than banks. Investment managers often offer sizable dividend yields, such as the subject of this article.

That stock is Artisan Partners Asset Management Inc. (APAM), a company with a market cap of less than $3 billion, but a very high yield. In fact, the 6.5% current yield is good enough to land Artisan on our list of high-yield stocks.

Artisan Partners is part of our ‘High Dividend 50‘ series, where we cover the 50 highest yielding stocks in the Sure Analysis Research Database.

This list contains about 200 stocks with yields of at least 5%, meaning they all yield at least three times that of the S&P 500.

You can download your free full list of all securities with 5%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

Below, we’ll analyze the prospects of Artisan as an investment opportunity today.

Business Overview

Artisan is a publicly-owned investment manager. The company provides investment services to pension and profit sharing plans, trusts, endowments, charitable organizations, governments, private funds, mutual funds, and more. It manages equity and fixed income portfolios that have investments from all over the world. The company focuses on traditional fundamental analysis to find and select investment opportunities for its funds.

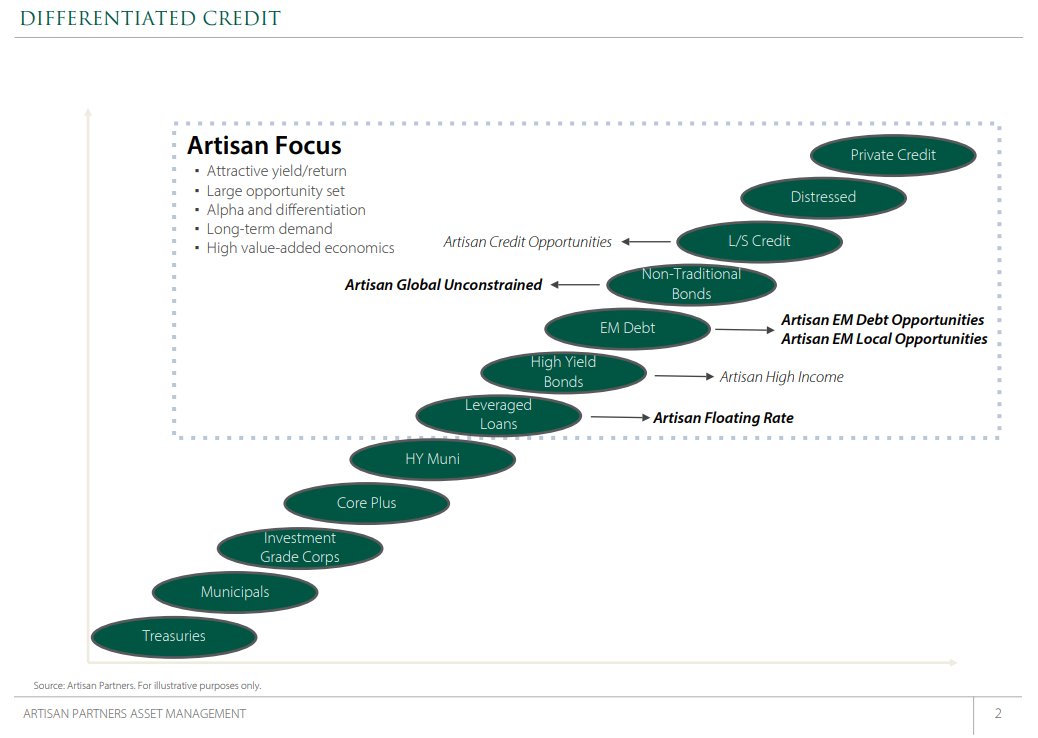

Source: Investor presentation, page 2

In terms of Artisan’s credit focus, it is in the bottom half of the credit risk ladder, as seen above. This affords Artisan much higher yields than investors focused on government and high-grade corporate issues, for instance, but it also carries with it increased risk. Artisan seeks to manage that trade off between risk and reward to generate returns for shareholders.

Artisan was founded in 1994 and is based in the US. The company produces just under a billion dollars of annual revenue, and trades with a market cap of $2.7 billion.

Artisan posted third quarter earnings on November 1st, 2022, and results came in weaker than expected. Adjusted earnings-per-share came to 70 cents, which plummeted from $1.33 in adjusted earnings-per-share in the year-ago period. Likewise, revenue fell sharply, declining 26% year-over-year to $234 million.

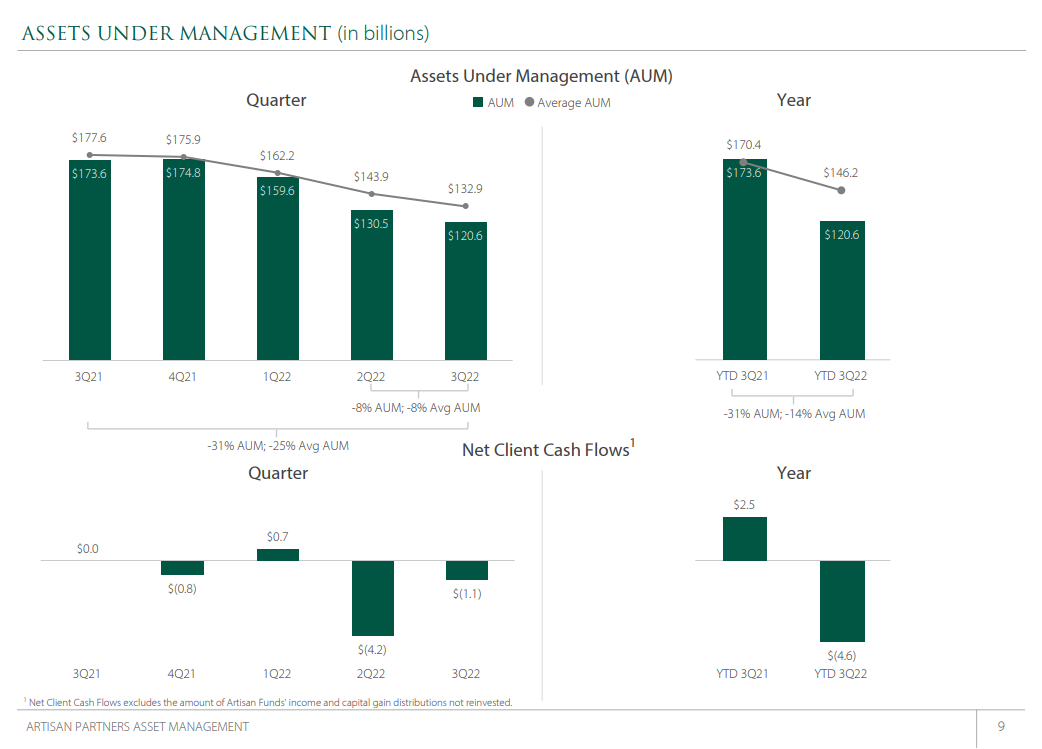

Assets under management, which is the primary way that Artisan generates fees, declined 31% year-over-year to $121 billion. That was attributable primarily to the decline in global stock markets. In addition, Artisan saw $5.4 billion in net client cash outflows, as well as $2.4 billion in capital gains distributions that clients chose not to reinvest.

Operating expenses came to $156 million, down $18 million year-over-year, which was attributable to a decline in incentive compensation, as well as third-party distribution expenses. These were offset slightly by higher occupancy, technology, fixed compensation, and travel costs.

Adjusted operating margin fell sharply year-over-year from 45.2% of revenue to 32.9%. Asset managers tend to have volatile operating margins because the leverage they achieve on operating expenses with growth in assets under management is strong. That works in both directions, however, and the global stock market downturn of 2021 took a significant toll on Artisan’s profitability.

With the fourth quarter yet to be reported, we estimate full-year adjusted earnings-per-share of $3.05 for Artisan.

Growth Prospects

Given the fact that Artisan is nearly wholly reliant upon rising assets under management to generate fees and earnings, its earnings growth history is predictably spotty. It’s normal for Artisan to see rather sizable gains and losses from year to year, but importantly, the company has remained solidly profitable throughout the last decade. We note Artisan has seen net client outflows frequently in the past several quarters, which hurts its ability to grow longer-term. Instead, the company is very reliant upon the values of global stock and bond markets, both of which had awful years in 2021.

Given these factors, we are currently estimating -2% earnings contraction on average in the years to come, as we see competitive headwinds persisting, and as we find the net client outflows to be somewhat worrisome. On the plus side, the company is controlling operating expenses, and the outflows have thus far been small and manageable. Still, we think Artisan has a tough road ahead in terms of growing earnings from the ~$3 per share level estimated for 2022.

Competitive Advantages

Unfortunately for Artisan, we don’t see where it has much of a competitive advantage. There are countless investment managers available to those looking to invest their capital, and many of them have enormous scale and brand recognition advantages over Artisan. The company notes its funds perform relatively well, but it simply hasn’t resonated with customers.

Source: Investor presentation, page 9

There is perhaps no better illustration of this lack of advantage than the above data on outflows and assets under management. We believe that if Artisan had a competitive advantage, it would be attracting additional investor capital, not losing it. While we believe Artisan is a competent investment manager, we cannot look past the fact that customers are net sellers of the company’s funds.

Dividend Analysis

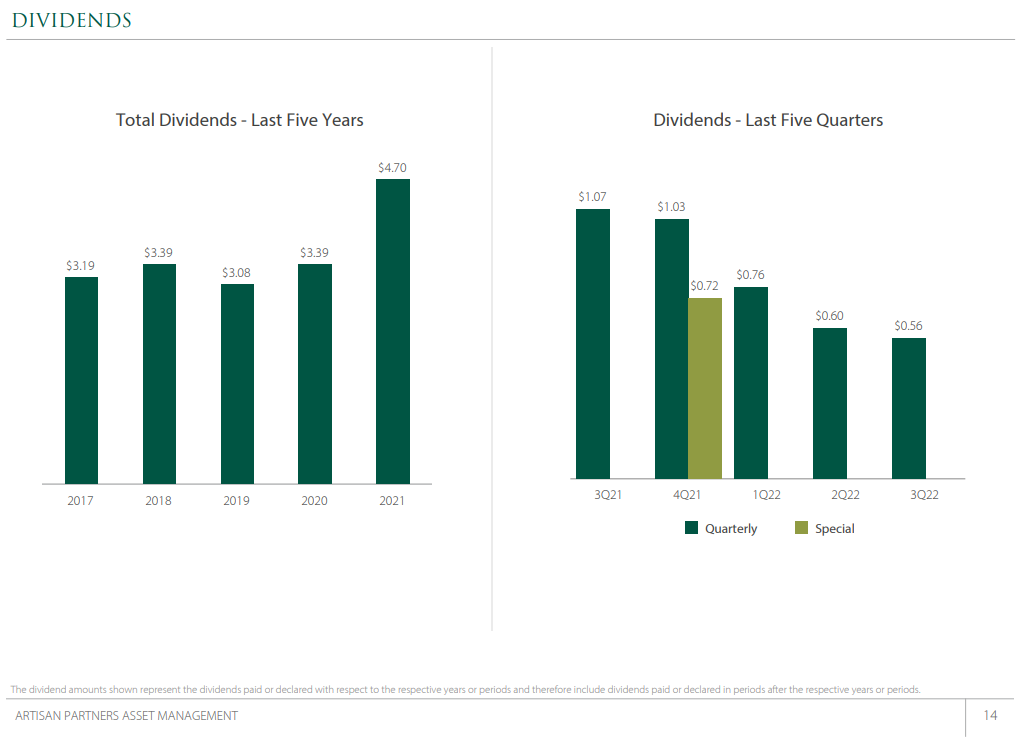

Artisan has paid dividends to shareholders for nine consecutive years, which is the amount of time it has been publicly-traded. However, it does not have a dividend growth streak given the unique, variable nature of its dividend policy. Management aims to pay out 80% of the cash the company generates for the year, but given the volatile nature of its earnings performance, 80% of cash generated can be wildly different from year to year. It also means that the company pays a regular quarterly dividend, and then typically pays a special dividend at the end of the year.

Source: Investor presentation, page 14

The quarterly dividends are variable in size, as are the special dividends, so it is nearly impossible to know from year to year what the total payout might be. However, to its credit, Artisan’s total dividends have been huge for the past five years, with the period of 2017 to 2021 producing a total of $17.75 in cash distributions to shareholders. With the share price at $34 today, that implies shareholders received fully half of today’s share price in dividends in just five years.

Artisan’s payout has exceeded 100% of earnings at times in the past, but we see it under 90% for the foreseeable future. That’s very high, and it means the dividend is susceptible to cuts. However, Artisan’s policy is to pay a variable dividend each year, so cuts are normal and should be expected from time to time.

Where Artisan excels is in the total yield it provides investors, as the current quarterly dividend alone is worth 6.5%, while any special dividends add to that total yield. That makes Artisan a very strong income stock, provided investors aren’t looking for dividend growth, and are okay with the payout being cut and raised constantly.

Final Thoughts

Artisan Partners Asset Management has proven itself to be a very strong income stock in recent years, returning half of its current share price to shareholders in cash dividends in just the past five years. However, we see the earnings growth outlook as murky, and given the variable dividend policy, that means lower dividends are quite possible.

We like the current yield, particularly if the global equity markets turn higher in 2023, as that will raise the company’s assets under management, and therefore, earnings. However, for now, the payout looks somewhat at risk, and we are cautious on Artisan as a result, despite the big yield.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

- 20 Highest-Yielding BDCs

- 20 Highest-Yielding MLPs

- 20 Highest Yielding Dividend Kings

- 20 Best Ultra High-Dividend Stocks

- 20 High-Dividend Stocks Under $10

- 20 Undervalued High-Dividend Stocks

- 20 Highest-Yielding Dividend Aristocrats

- 20 Highest Yielding Monthly Dividend Stocks

- 20 Highest-Yielding Small Cap Dividend Stocks

- 20 Safe High Dividend Blue-Chip Stocks With Low Volatility

- 12 Long-Term High-Dividend Stocks To Buy And Hold For Decades

- 12 Consistently High Paying Dividend Stocks With Growth Potential

- 10 Super High Dividend REITs

- 10 Highest Yielding Dividend Champions

- 10 Highest Yielding Dow 30 Stocks | Dogs Of The Dow

- 10 High-Yield Dividend Stocks Trading Below Book Value

- 9 Highest Yielding Royalty Trusts

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Monthly Dividend Stocks: Individual securities that pay out every month

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more