Updated on January 18th, 2023 by Nikolaos Sismanis

While inflation has somewhat eased lately, it remains at highly elevated levels due to the immense fiscal stimulus packages offered by the government in response to the pandemic a couple of years back, the ongoing invasion of Russia in Ukraine, and a hot jobs market.

High inflation exerts great pressure on income-oriented investors, as it erodes the real value of their portfolios. As a result, many income-oriented investors will choose to resort to high-yield stocks, in order to maintain positive actual returns.

M.D.C. Holdings (MDC) is part of our ‘High Dividend 50’ series, where we cover the 50 highest yielding stocks in the Sure Analysis Research Database.

We have created a spreadsheet of stocks (and closely related REITs and MLPs, etc.) with dividend yields of 5% or more…

You can download your free full list of all securities with 5%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

In this article, we will analyze the prospects of M.D.C. Holdings (MDC), which is offering a 5.6% dividend yield with a payout ratio of about 24%.

Business Overview

M.D.C. Holdings has two primary operations, home building, and financial services. Its home-building operation purchases finished lots or develops lots to the extent necessary for the construction and sale of single-family detached homes to home buyers under the name “Richmond American Homes.” Its financial services operation issues mortgage loans primarily for the home buyers of the company while it also sells insurance coverage.

Due to the nature of its business, M.D.C. Holdings has always been highly vulnerable to recessions, as demand for new homes plunges during rough economic periods. In the Great Recession, the quarterly sales of M.D.C. Holdings plunged 99% within just a few quarters, and the company incurred hefty losses.

During COVID-19, despite the disruptions caused by the pandemic, the work-from-home economy, and low interest rates resulted in a growing demand for homes, M.D.C. performed quite fantastically. In fact, the home builder grew its earnings per share by 50% in that year, from $3.56 to $5.33.

The company’s momentum lasted through 2021 as well, with earnings-per-share skyrocketing to $8.13.

During 2022, the residential real estate market started facing headwinds, as last year’s home-buying frenzy started to cool and interest rates began their way upwards.

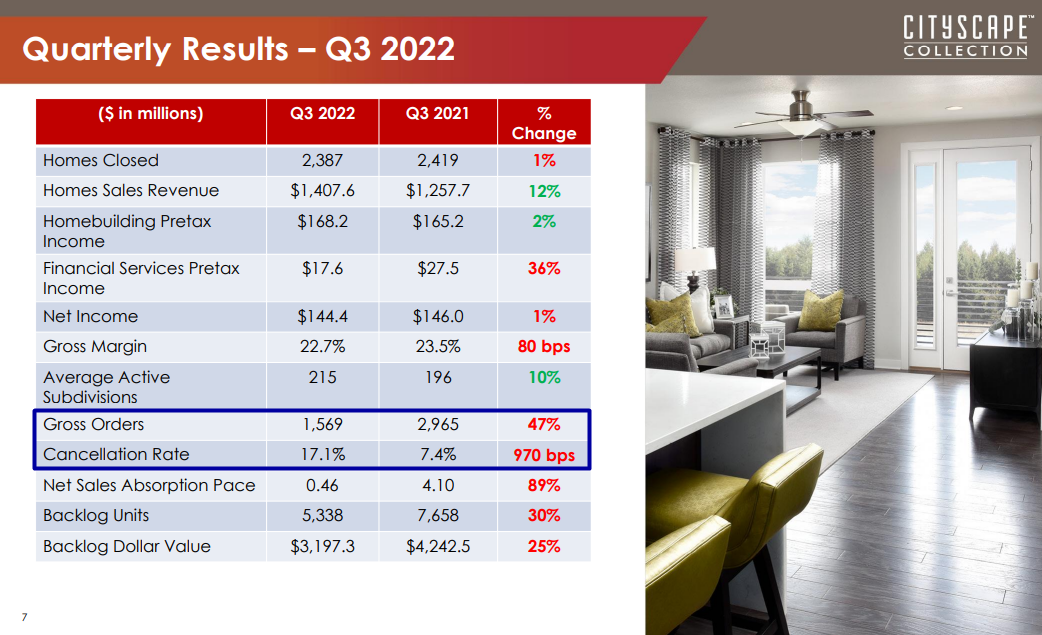

This was illustrated in M.D.C.’s Q3 2022 results, in which the company reported a 47% year-over-year decline in unit orders. Cancellations as a percentage of beginning backlog also increased 970 basis points to 17.1% from 7.4% year-over-year as well.

Source: Investor Presentation

Nevertheless, the average selling price of net orders remained 8% higher compared to Q3-2021.

The company continues to see declining demand for its homes, with recession fears having grown amongst home buyers. That said, due to the existing backlog of orders, management expects to achieve Q4 home deliveries between 2,200 to 2,500 at an average selling price of $570,000 and $580,000.

So despite M.D.C.’s earnings-per-share likely to plunge in 2023, as illustrated by cancellations and lack of stimulating home orders, the tailwinds from its prior backlog combined with a relatively strong performance during the first half of 2022, should result in earnings-per-share close to $8.37 based on our estimates.

This should imply another record year for the company in terms of its profitability.

Growth Prospects

Due to the nature of its business, M.D.C. Holdings has exhibited a volatile performance record with dramatic swings. However, the company has grown its earnings per share for eight consecutive years, with its 5-year compound annual growth rate standing at about 31%.

Of course, investors should not expect M.D.C. Holdings to maintain such a high growth rate in the upcoming years. The company’s most recent quarterly report continued to display strong signs of a slowdown in demand for new houses, with the dollar value of net new orders declining 88% to $152.8 million in Q3, compared to $1.31 billion last year.

The declining demand for homes is driven by a sharp increase in interest rates combined with a more uncertain economic outlook that has taken a toll on consumer confidence.

In addition, the Fed has been raising interest rates aggressively in an effort to get inflation under control. Higher rates are likely to suppress demand for new homes as long as the Fed remains hawkish.

In our view, these challenges are likely to persist in the coming years. Accordingly, we expect the company’s earnings to decline by a negative CAGR of about 7% in the medium term of what will likely be a base of record EPS this year.

Competitive Advantages

M.D.C. Holdings offers affordable prices and a built-to-order model, which resonates well with the desire of consumers for new home customization. This is a significant competitive advantage. In addition, the company has proved extremely resilient throughout the coronavirus crisis.

However, investors should not jump to the conclusion that M.D.C. Holdings is immune to recessions. As evidenced by the Great Recession, the home builder is highly vulnerable to recessions. It proved resilient during the pandemic thanks to the short duration of the recession and the unprecedented fiscal stimulus packages, which led to a sharp recovery of the economy.

On the contrary, the Great Recession was the worst financial crisis of the last 80 years and included a collapse of the home market as well. In other words, it was the worst possible business environment for M.D.C. Holdings.

As long as the economy remains healthy, M.D.C. Holdings is likely to keep thriving, but the company will be affected whenever the next recession shows up.

Dividend Analysis

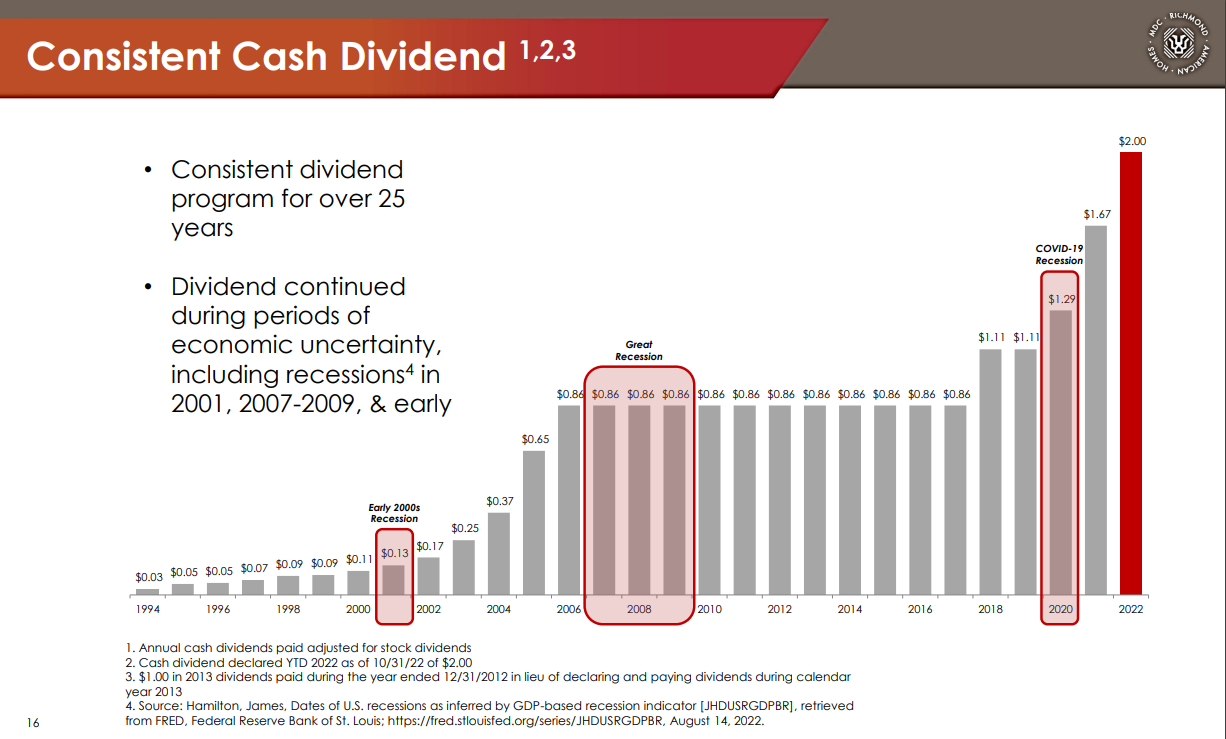

Despite the cyclical nature of its industry, M.D.C. Holdings features a compelling dividend record. The company has grown its dividend whenever it reached a new profitability plateau and has never cut its quarterly payouts since 1994, despite the multiple harsh economic environments during the period.

Source: Investor Presentation

M.D.C. Holdings is currently offering an attractive 5.6% dividend yield. Even better, thanks to its blowout earnings, the stock has a payout ratio of only 24%.

Even though we expect earnings-per-share to decline materially in the medium term from the record levels of 2021-2022, the dividend should not be in danger.

We also praise management for maintaining a healthy balance sheet, which is paramount in this highly cyclical business.

The company pays negligible interest expense, and its net debt of $748 million implies a net-debt-to-capital ratio of just 19.9%. Therefore, although M.D.C. Holdings is vulnerable to economic downturns, its 5.6% dividend has a wide margin of safety.

Final Thoughts

M.D.C. Holdings is on track to post record or near-record earnings for the eighth consecutive year in 2022, thanks to 2021’s tailwinds rolling forward.

The residential real estate market has already started to show significant signs of weakness, including growing cancelations and a lack of new home orders, which should result in declining earnings-per-share in the coming years.

This is the reason behind the extremely low forward price-to-earnings ratio of 4.3 of the stock. That said, we expect the company to sustain its $2.00 annual dividend, which currently yields about 5.6%.

Overall, the stock is attractively valued from a long-term perspective right now, but it is suitable only for investors who can stomach high stock price volatility and extended periods of potential paper losses.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

- 20 Highest-Yielding BDCs

- 20 Highest-Yielding MLPs

- 20 Highest Yielding Dividend Kings

- 20 Best Ultra High-Dividend Stocks

- 20 High-Dividend Stocks Under $10

- 20 Undervalued High-Dividend Stocks

- 20 Highest-Yielding Dividend Aristocrats

- 20 Highest Yielding Monthly Dividend Stocks

- 20 Highest-Yielding Small Cap Dividend Stocks

- 20 Safe High Dividend Blue-Chip Stocks With Low Volatility

- 12 Long-Term High-Dividend Stocks To Buy And Hold For Decades

- 12 Consistently High Paying Dividend Stocks With Growth Potential

- 10 Super High Dividend REITs

- 10 Highest Yielding Dividend Champions

- 10 Highest Yielding Dow 30 Stocks | Dogs Of The Dow

- 10 High-Yield Dividend Stocks Trading Below Book Value

- 9 Highest Yielding Royalty Trusts

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Monthly Dividend Stocks: Individual securities that pay out every month

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more