Published on March 13th, 2023 by Aristofanis Papadatos

CT Real Estate Investment Trust (CTRRF) has three appealing investment characteristics:

#1: It is a REIT so it has a favorable tax structure and pays out the majority of its earnings as dividends.

Related: List of publicly traded REITs

#2: It is a high yield stock based on its 5.3% dividend yield.

Related: List of 5%+ yielding stocks

#3: It pays dividends monthly instead of quarterly.

Related: List of monthly dividend stocks

You can download our full list of monthly dividend stocks (along with relevant financial metrics like dividend yields and payout ratios), which you can access below:

CT Real Estate Investment Trust’s trifecta of favorable tax status as a REIT, a high yield, and a monthly dividend make it appealing to individual investors.

But there’s more to the company than just these factors. Keep reading this article to learn more about CT Real Estate Investment Trust.

Business Overview

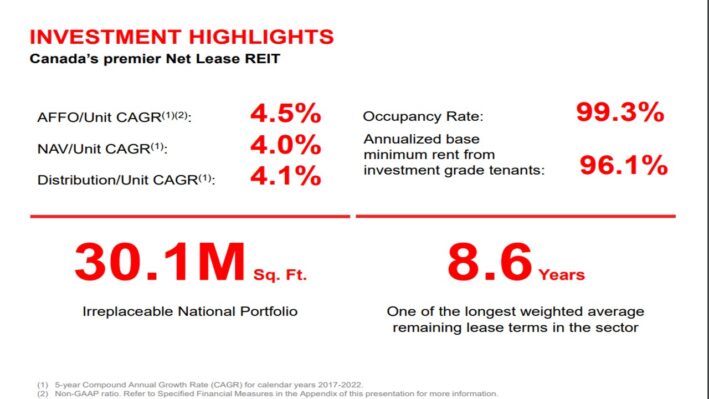

CT Real Estate Investment Trust (CT REIT) is a closed-end real estate investment trust that owns commercial properties primarily located in Canada. Its portfolio is comprised of over 370 properties totaling approximately 30 million square feet of gross leasable area, consisting primarily of net lease retail properties located across Canada.

CT REIT is a leading net lease REIT in Canada that greatly benefits from its relationship with Canadian Tire Corporation, its most significant tenant and controlling unitholder. This close association and alignment is a key competitive advantage, which provides important insight into real estate acquisitions and development opportunities. Such opportunities, combined with predictable rent hikes, are the primary growth drivers of CT REIT.

CT REIT exhibits strong performance metrics. Its asset portfolio currently has an exceptionally high occupancy rate of 99.3%.

Source: Investor Presentation

In addition, the REIT receives 96.1% of its annualized base rent from investment-grade tenants while it has an 8.6-year average duration of remaining leases, one of the longest periods in the REIT universe.

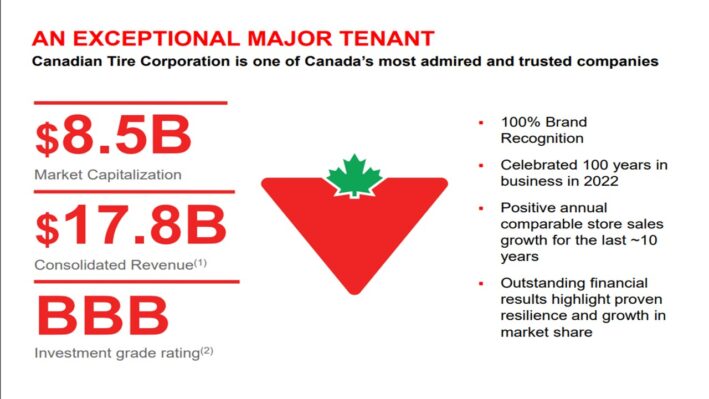

Canadian Tire Corporation, which is the major tenant of CT REIT, has a history of 101 years and has grown its comparable store sales for ten consecutive years.

Source: Investor Presentation

It also has annual revenues of $17.8 billion and a BBB credit rating. The merits of having a major tenant with strong business performance and a solid financial position are obvious.

Growth Prospects

CT REIT is ideally positioned to leverage its relationship with Canadian Tire Corporation and pursue third-party net lease opportunities to complement organic growth. It also benefits from average annual rent hikes of about 1.5%.

SINCE ITS IPO, CT REIT has acquired and leased more than 2 million square feet of industrial properties to Canadian Tire Corporation. In addition, there are another 15-20 properties of Canadian Tire Corporation, which are likely to meet the investment criteria of CT REIT.

In 2022, CT REIT invested $260 million in growth projects and thus enhanced its gross leasable area by nearly 1 million square feet. Moreover, the REIT has a solid growth pipeline. It currently has an investment program of $375 million, which covers 1.28 million square feet of development.

Despite its growth drivers and its consistent business performance, CT REIT is a slow-growth REIT. To be sure, the trust has grown its adjusted FFO per share by 3.6% per year on average over the last eight years. As there are no signs of accelerating business performance, it is prudent for investors to expect a similar growth rate going forward. We expect 3.0% average annual growth of FFO per share over the next five years.

Dividend & Valuation Analysis

In contrast to many REITs, which cut their dividends in 2020-2021 due to the coronavirus crisis, CT REIT proved resilient to that downturn thanks to its robust business model. The REIT grew its FFO per share by 4% in 2020 and by 7% in 2021, and thus it raised its dividend (in USD) by 5% in 2020 and by another 5% in 2021.

Moreover, CT REIT is currently offering a 5.3% dividend yield. Thanks to its defensive business model, its reasonable (for a REIT) payout ratio of 74%, and its interest coverage of 3.7, the trust is not likely to cut its dividend in the absence of a severe recession.

Furthermore, CT REIT has no unsecured debt maturities until June-2025, while 94% of its debt is at fixed rates. As a result, the REIT is somewhat protected from the adverse environment of rising interest rates. It also has a weighted average interest rate of 3.99%, which is manageable under normal business conditions.

On the other hand, it is important to note that CT REIT has a weak balance sheet, with a leverage ratio (Net Debt to EBITDA) of 6.9. It also has an average annual dividend growth rate of just 1.5% over the last eight years. Additional dividend growth would only enhance investors’ yield on cost. However, investors should not expect meaningful dividend growth going forward.

In reference to the valuation, CT REIT is currently trading for 14.5 times its adjusted FFO per share in the last 12 months. Given the modest growth rate of the trust, we assume a fair price-to-FFO ratio of 12.0 for the stock. Therefore, the current FFO multiple is higher than our assumed fair price-to-FFO ratio. If the stock trades at its fair valuation level in five years, it will incur a -3.7% annualized drag in its returns.

Taking into account the 3% annual FFO-per-share growth, the 5.1% dividend, and a -3.7% annualized contraction of valuation level, CT REIT could offer just a 4.4% average annual total return over the next five years. This is a lackluster expected return, and hence investors should wait for a more opportune entry point.

Final Thoughts

CT REIT has exhibited consistent and reliable business performance over the last eight years. It also proved markedly resilient throughout the coronavirus crisis, defending its dividend in sharp contrast to many other REITs. As the stock is also offering a 5.3% dividend yield with a decent payout ratio of 74%, it is an attractive candidate for the portfolios of income-oriented investors.

On the other hand, investors should be aware that CT REIT is a slow-growth REIT, and hence it is prudent to try to have a wide margin of safety in reference to the valuation of the stock. CT REIT appears almost fairly valued right now. Therefore, investors should wait for a meaningful correction of the stock, towards $10, before purchasing the stock.

Moreover, CT REIT is characterized by exceptionally low trading volume. This means that it is hard to establish or sell a large position in this stock.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more