The Sure Passive Income Newsletter helps you build rising passive income for retirement and/or financial freedom.

The stocks we recommend in the Sure Passive Income Newsletter are meant to be purchased once and never sold.

Our ~15 person analyst team finds high quality dividend growth stocks to buy and hold forever by analyzing more than 850 income securities every quarter in the Sure Analysis Research Database.

“So I think it was just looking at different companies, and I always thought if you looked at 10 companies, you’d find 1 that’s interesting, if you’d look at 20, you’d find 2, or if you look at 100 you’ll find 10. The person that turns over the most rocks wins the game. And that’s always been my philosophy.”

– Investing legend Peter Lynch

Data from Sure Analysis power the Sure Passive Income Newsletter‘s security selection process.

The end result is a concise list of our Top 10 buy and hold forever securities for rising passive income published each month in the Sure Passive Income Newsletter.

Click here to start your 7-day free trial of the Sure Passive Income Newsletter now

Notes: 7-Day free trial, then $199/year. You will instantly receive the current edition after joining.

How We Find The 10 Best Buy & Hold Forever Stocks For Rising Passive Income Each Month

The Sure Passive Income Newsletter find the top 10 best buy and hold stocks for rising passive income each month. We accomplish this by analyzing more than 850+ income securities every quarter, over the same metrics that matter.

This is not a quick ‘shoot from the hip’ list. It’s real research done systematically by our analyst team. We do the ‘heavy lifting’ to find you the best buy and hold forever securities for rising passive income.

We take the data from all of this analysis, combined with other data sources, to rank our universe of securities for the Sure Passive Income Newsletter. The exact ranking methodology is shown below.

Click here to start your 7-day free trial of the Sure Passive Income Newsletter now

Notes: 7-Day free trial, then $199/year. You will instantly receive the current edition after joining.

How To Build Your Buy & Hold Forever Rising Passive Income Portfolio With The Sure Passive Income Newsletter

The Sure Passive Income Newsletter has everything you need to build your rising passive income portfolio. This includes our Top 10 buys each month, actionable sells as needed (we have yet to issue a single sell), and our portfolio building guide.

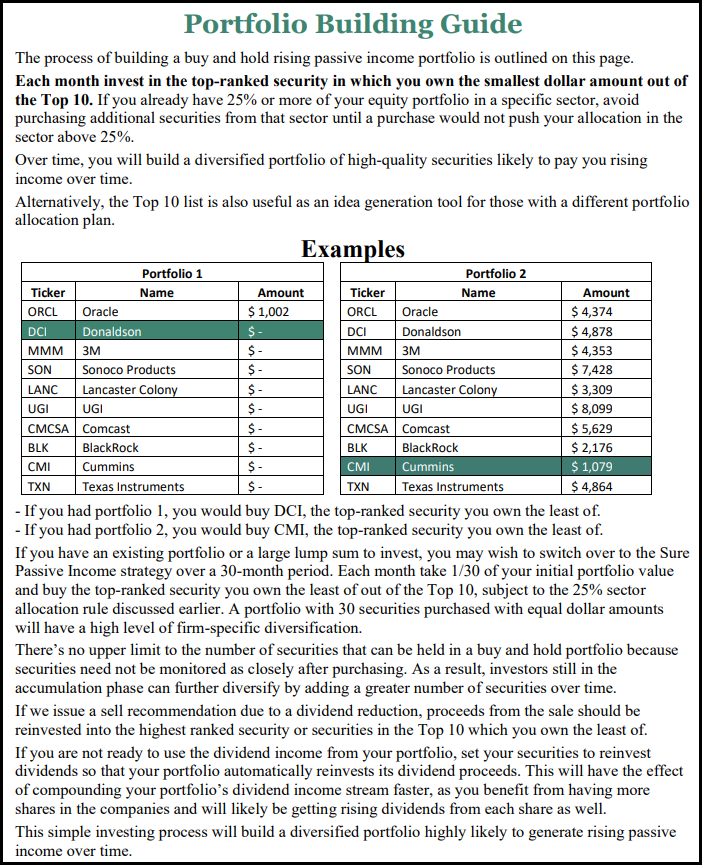

The Sure Passive Income Newsletter portfolio building guide is shown below. It is included in every edition of the Sure Passive Income Newsletter.

Note: The recommendations in the image below are not current.

“I simply to express my gratitude for the Sure Passive Income Newsletter. I have acquired $1,000 of each new Top Ten entry since the newsletter began and added another $1,000 into existing positions the two times there were no new appearances in the Top Ten. This collection of stocks is excellent. No wild swings, very good performance since inception and the dividends are climbing. Even on the days where there is a divergence between value stocks and growth stocks, this portfolio tends to do well regardless of what the market is favoring on a particular day – a testament to the fact that while the stocks are larger companies with strong dividend histories, they also exhibit characteristics of companies that are still growing at a significant rate.”

– Sure Passive Income Newsletter member

Click here to start your 7-day free trial of the Sure Passive Income Newsletter now

Notes: 7-Day free trial, then $199/year. You will instantly receive the current edition after joining.

The Sure Dividend Golden Rule Commitment

The Sure Passive Income Newsletter is backed by the Sure Dividend Golden Rule Commitment.

The Sure Dividend Golden Rule Commitment is our guarantee to treat our customers the way we’d want to be treated.

“Your skills and experience and brain has done so much for me and thousands of others. In reality though, it’s your transparency and integrity that sets you apart from the rest of the investment companies. Yes you are one of the few in the investment industry, who really does live by the Golden Rule. You are the last honest investment teacher. Never change. We’ll keep sending fellow retail customers to you only.”

– Sure Dividend member

Here’s what you get when you join the Sure Passive Income Newsletter:

- 7 Day Free Trial – You aren’t billed for seven days. If the Sure Passive Income Newsletter isn’t right for you, just email us (support@suredividend.com) or log in to the member’s area to cancel and you won’t be charged.

- 60 Day Full Refund Grace Period – If the Passive Income Newsletter isn’t right for you, just email us (again, support@suredividend.com) anytime during the first 60 days from the date you joined and you will receive a full refund; no explanation needed.

- Prorated Refunds After 60 Days – If you feel the Passive Income Newsletter isn’t right for you after the 60 day full refund grace period, just email us (once again, support@suredividend.com) to cancel and you will receive a prorated refund for unused time on your plan.

- Top-Notch Customer Service – Our customer service is handled by key team members. It’s not outsourced or farmed off to people who don’t understand the intricacies of dividend investing. Feel free to ask detailed investing questions. In almost all cases we will answer in one business day or less. As a newsletter provider, we can’t and won’t provide personalized investment advice.

The Sure Dividend Golden Rule Commitment is here because we care about our readers’ success. We are now trusted by more than 8,000 premium members.

Sure Dividend helps individual investors build high-quality dividend growth portfolios for the long run. Part of the way we accomplish this is through fair business terms and quality customer support.

If you don’t feel the newsletter is the right fit for you, just notify us via email at support@suredividend.com to opt-out within your 60 day full refund grace period and you will receive a full refund.

“You and your team run the BEST research program in the country.”

– Sure Dividend member

Click here to start your 7-day free trial of the Sure Passive Income Newsletter now

Notes: 7-Day free trial, then $199/year. You will instantly receive the current edition after joining.

If you have any questions at all, please feel free to email us at support@suredividend.com.

Notes: Some testimonials have been edited for privacy and grammar. Testimonials were written by people who were members at the time of writing the testimonial. We have far more positive testimonials than what is shown in this article. You can see them here.