Updated on April 8th, 2024 by Bob Ciura

Spreadsheet data updated daily

Master Limited Partnerships – or MLPs, for short – are some of the most misunderstood investment vehicles in the public markets. And that’s a shame, because the typical MLP offers:

- Tax-advantaged income

- High yields well in excess of market averages

- The bulk of corporate cash flows returned to shareholders through distributions

An example of a ‘normal’ MLP is an organization involved in the midstream energy industry. Midstream energy companies are in the business of transporting oil, primarily though pipelines. Pipeline companies make up the vast majority of MLPs.

Since MLPs widely offer high yields, they are naturally appealing for income investors. With this in mind, we created a full downloadable list of nearly 100 MLPs in our coverage universe.

You can download the Excel spreadsheet (along with relevant financial metrics like dividend yield and payout ratios) by clicking on the link below:

This comprehensive article covers MLPs in depth, including the history of MLPs, unique tax consequences and risk factors of MLPs, as well as our 7 top-ranked MLPs today.

The table of contents below allows for easy navigation of the article:

Table of Contents

- The History of Master Limited Partnerships

- MLP Tax Consequences

- Advantages & Disadvantages of Investing in MLPs

- The 7 Best MLPs Today

#7: Star Group LP (SGU)

#6: AllianceBernstein Holding LP (AB)

#5: Alliance Resource Partners LP (ARLP)

#4: Icahn Enterprises LP (IEP)

#3: NextEra Energy Partners (NEP)

#2: Brookfield Energy Partners LP (BEP)

#1: Brookfield Infrastructure Partners LP (BIP) - MLP ETFs, ETNs, & Mutual Funds

- Final Thoughts

The History of Master Limited Partnerships

MLPs were created in 1981 to allow certain business partnerships to issue publicly traded ownership interests.

The first MLP was Apache Oil Company, which was quickly followed by other energy MLPs, and then real estate MLPs.

The MLP space expanded rapidly until a great many companies from diverse industries operated as MLPs – including the Boston Celtics basketball team.

One important trend over the years, is that energy MLPs have grown from being roughly one-third of the total MLP universe to containing the vast majority of these securities.

Moreover, the energy MLP universe has evolved to be focused on midstream energy operations. Midstream partnerships have grown to be roughly half of the total number of energy MLPs.

MLP Tax Consequences

Master limited partnerships are tax-advantaged investment vehicles. They are taxed differently than corporations. MLPs are pass-through entities. They are not taxed at the entity level.

Instead, all money distributed from the MLP to unit holders is taxed at the individual level.

Distributions are ‘passed through’ because MLP investors are actually limited partners in the MLP, not shareholders. Because of this, MLP investors are called unit holders, not shareholders.

And, the money MLPs pay out to unit holders is called a distribution (not a dividend).

The money passed through from the MLP to unit holders is classified as either:

- Return of Capital

- Ordinary Income

MLPs tend to have lots of depreciation and other non-cash charges. This means they often have income that is far lower than the amount of cash they can actually distribute. The cash distributed less the MLPs income is a return of capital.

A return of capital is not technically income, from an accounting and tax perspective. Instead, it is considered as the MLP actually returning a portion of its assets to unit holders.

Now here’s the interesting part… Returns of capital reduce your cost basis. That means taxes for returns of capital are only due when you sell your MLP units. Returns of capital are tax-deferred.

Note: Return of capital taxes are also due in the event that your cost basis is less than $0. This only happens for very long-term holding, typically around 10 years or more.

Each individual MLP is different, but on average an MLPs distribution is usually around 80% to 90% a return of capital, and 10% to 20% ordinary income.

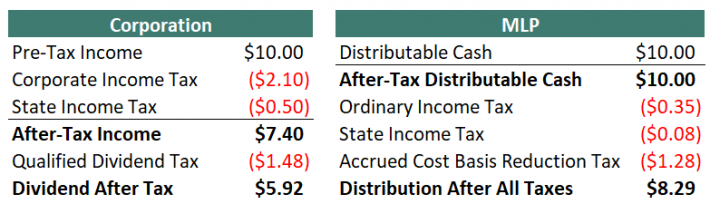

This works out very well from a tax perspective. The images below compare what happens when a corporation and an MLP each have the same amount of cash to send to investors.

Note 1: Taxes are never simple. Some reasonable assumptions had to be made to simplify the table above. These are listed below:

- Corporate federal income tax rate of 21%

- Corporate state income tax rate of 5%

- Qualified dividend tax rate of 20%

- Distributable cash is 80% a return of capital, 20% ordinary income

- Personal federal tax rate of 22% less 20% for passive entity tax break

(19.6% total instead of 22%) - Personal state tax rate of 5% less 20% for passive entity tax break

(4% total instead of 5%) - Long-term capital gains tax rate of 20% less 20% for passive entity tax break

(16% total instead of 20%)

Note 2: The 20% passive income entity tax break will expire in 2025.

Note 3: In the MLP example, if the maximum personal tax rate of 37% is used, the distribution after all taxes is $8.05.

Note 4: In the MLP example, the accrued cost basis reduction tax is due when the MLP is sold, not annually come tax time.

As the tables above show, MLPs are far more efficient vehicles for returning cash to shareholders relative to corporations. Additionally, in the example above $9.57 out of $10.00 distribution would be kept by the MLP investor until they sold because the bulk of taxes are from returns of capital and not due until the MLP is sold.

Return of capital and other issues discussed above do not matter when MLPs are held in a retirement account.

There is a different issue with holding MLPs in a retirement account, however. This includes 401(k), IRA, and Roth IRA accounts, among others.

When retirement plans conduct or invest in a business activity, they must file separate tax forms to report Unrelated Business Income (UBI) and may owe Unrelated Business Taxable Income (UBTI). UBTI tax brackets go up to 37% (the top personal rate).

MLPs issue K-1 forms for tax reporting. K-1s report business income, expense, and loss to owners. Therefore, MLPs held in retirement accounts may still qualify for taxes.

If UBI for all holdings in your retirement account is over $1,000, you must have your retirement account provider (typically, your brokerage) file Form 990-T.

You will want to file form 990-T as well if you have a UBI loss to get a loss carryforward for subsequent tax years. Failure to file form 990-T and pay UBIT can lead to severe penalties.

Fortunately, UBIs are often negative. It is a fairly rare occurrence to owe taxes on UBI.

The subject of MLP taxation can be complicated and confusing. Hiring a tax professional to aid in preparing taxes is a viable option for dealing with the complexity.

The bottom line is this: MLPs are tax-advantaged vehicles that are suited for investors looking for current income. It is fine to hold them in either taxable or non-taxable (retirement) accounts.

Since retirement accounts are already tax-deferred, holding MLPs in taxable accounts allows you to ‘get credit’ for the full effects of their unique structure.

4 Advantages & 6 Disadvantages of Investing in MLPs

MLPs are a unique asset class. As a result, there are several advantages and disadvantages to investing in MLPs. Many of these advantages and disadvantages are unique specifically to MLPs.

Advantages of MLPs

Advantage #1: Lower taxes

MLPs are tax-advantaged securities, as discussed in the “Tax Consequences” section above. Depending on your individual tax bracket, MLPs are able to generate around 40% more after-tax income for every pre-tax dollar they decide to distribute, versus Corporations.

Advantage #2: Tax-deferred income through returns of capital

In addition to lower taxes in general, 80% to 90% of the typical MLPs distributions are classified as returns of capital. Taxes are not 0wed (unless cost basis falls below 0) on return of capital distributions until the MLP is sold.

This creates the favorable situation of tax-deferred income.

Tax-deferred income is especially beneficial for retirees as return on capital taxes may not need to be paid throughout retirement.

Advantage #3: Diversification from other asset classes

Investing in MLPs provides added diversification in a balanced portfolio. Diversification can be measured by the correlation in return series between asset classes.

MLPs are excellent diversifiers, having either a near zero or negative correlation to corporate bonds, government bonds, and gold.

Additionally, they have a correlation coefficient of less than 0.5 to both REITs and the S&P 500. This makes MLPs an excellent addition to a diversified portfolio.

Advantage #4: Typically very high yields

MLPs tend to have high yields far in excess of the broader market. As of this writing, the S&P 500 yields ~2.1%, while the Alerian MLP ETF (AMLP) yields over 25%. Many individual MLPs have yields above 10%.

Disadvantages of MLPs

Disadvantage #1: Complicated tax situation

MLPs can create a headache come tax season. MLPs issue K-1’s and are generally more time-consuming and complicated to correctly calculate taxes than ‘normal’ stocks.

Disadvantage #2: Potential additional paperwork if held in a retirement account

In addition, MLPs create extra paperwork and complications when invested through a retirement account because they potentially create unrelated business income (UBI). See the “Tax Consequences” section above for more on this.

Disadvantage #3: Little diversification within the MLP asset class

While MLPs provide significant diversification versus other asset classes, there is little diversification within the MLP structure.

The vast majority of publicly traded MLPs are oil and gas pipeline businesses. There are some exceptions, but in general MLP investors are investing in energy pipelines and not much else.

Because of this, it would be unwise to allocate all or a majority of one’s portfolio to this asset class.

Disadvantage #4: Incentive Distribution Rights (IDRs)

MLP investors are limited partners in the partnership. The MLP form also has a general partner.

The general partner is usually the management and ownership group that controls the MLP, even if they own a very small percentage of the actual MLP.

Incentive Distribution Rights, or IDRs, are used to ‘incentivize’ the general partner to grow the MLP.

IDRs typically allocate greater percentages of cash flows to go to the general partner (and not to the limited partners) as the MLP grows its cash flows.

This reduces the MLPs ability to grow its distributions, putting a handicap on distribution increases.

It should be noted that not all MLPs have IDRs, but the majority do.

Disadvantage #5: Elevated risk of distribution cuts due to high payout ratios

One of the big advantages of investing in MLPs is their high yields. Unfortunately, high yields very often come with high payout ratios.

Most MLPs distribute nearly all of the cash flows they make to unit holders. In general, this is a positive.

However, it creates very little room for error.

The pipeline business is generally stable, but if cash flows decline unexpectedly, there is almost no margin of safety at many MLPs. Even a short-term disturbance in business results can necessitate a reduction in the distribution.

Disadvantage #6: Growth Through Debt & Share Issuances

Since MLPs typically distribute virtually all of their cash flows as distributions, there is very little money left over to actually grow the partnership.

And most MLPs strive to grow both the partnership, and distributions, over time. To do this, the MLP’s management must tap capital markets by either issuing new units or taking on additional debt.

When new units are issued, existing unit holders are diluted; their percentage of ownership in the MLP is reduced.

When new debt is issued, more cash flows must be used to cover interest payments instead of going into the pockets of limited partners through distributions.

If an MLPs management team starts projects with lower returns than the cost of their debt or equity capital, it destroys unit holder value. This is a real risk to consider when investing in MLPs.

The 7 Best MLPs Today

The 7 best MLPs are ranked and analyzed below using expected total returns from the Sure Analysis Research Database. Expected total returns consist of 3 elements:

- Return from change in valuation multiple

- Return from distribution yield

- Return from growth on a per-unit basis

Investors should note that the top MLPs list was not screened on a qualitative assessment of a company’s dividend risk. The focus is expected annual returns over the next five years.

That said, MLPs with current distribution yields below 2% were not considered. This screen makes the list more attractive to income investors.

Continue reading for detailed analysis on each of our top MLPs, ranked according to expected 5-year annual returns.

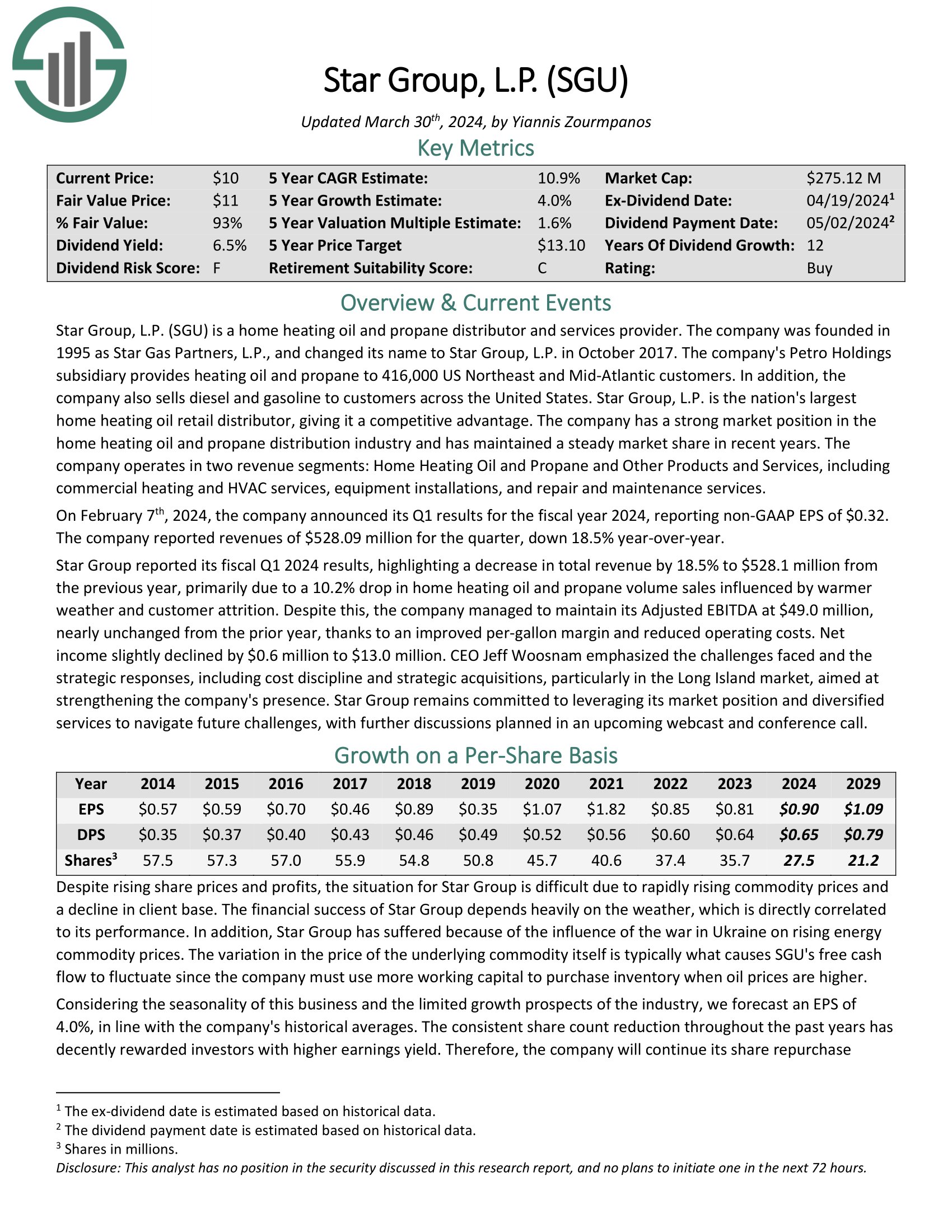

MLP #7: Star Group LP (SGU)

- 5-year expected annual returns: 11.6%

Star Group is a home heating oil and propane distributor and services provider. The company’s Petro Holdings subsidiary provides heating oil and propane to 416,000 US Northeast and Mid-Atlantic customers. In addition, the company also sells diesel and gasoline to customers across the United States. Star Group, L.P. is the nation’s largest home heating oil retail distributor, giving it a competitive advantage.

On February 7th, 2024, the company announced its Q1 results for the fiscal year 2024, reporting non-GAAP EPS of $0.32. The company reported revenues of $528.09 million for the quarter, down 18.5% year-over-year. Star Group reported its fiscal Q1 2024 results, highlighting a decrease in total revenue by 18.5% to $528.1 million from the previous year, primarily due to a 10.2% drop in home heating oil and propane volume sales influenced by warmer weather and customer attrition.

Click here to download our most recent Sure Analysis report on SGU (preview of page 1 of 3 shown below):

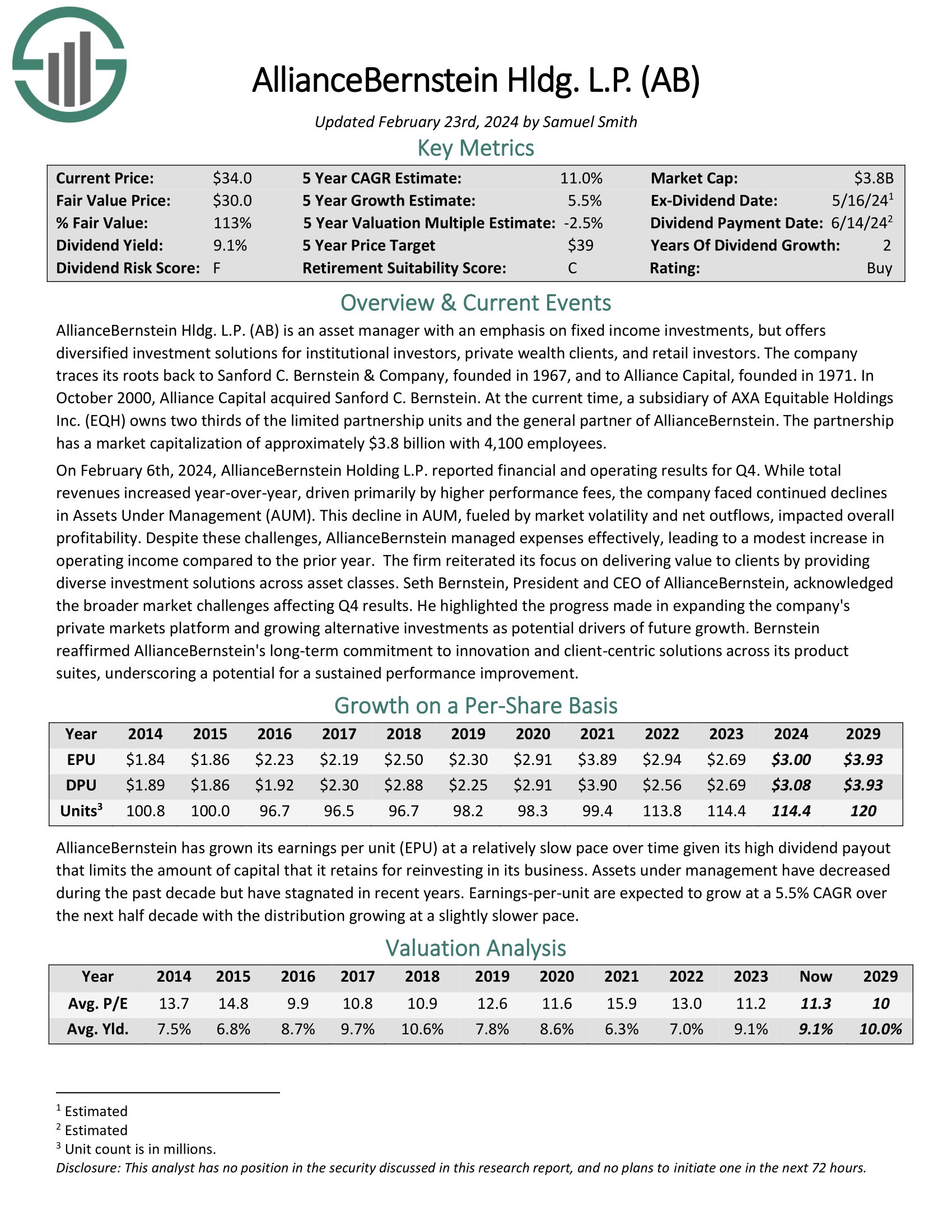

MLP #6: AllianceBernstein Holding LP (AB)

- 5-year expected annual returns: 10.9%

AllianceBernstein Hldg. L.P. is an asset manager with an emphasis on fixed income investments, but offers diversified investment solutions for institutional investors, private wealth clients, and retail investors. The company traces its roots back to Sanford C. Bernstein & Company, founded in 1967, and to Alliance Capital, founded in 1971.

On February 6th, 2024, AllianceBernstein Holding L.P. reported financial and operating results for Q4. While total revenues increased year-over-year, driven primarily by higher performance fees, the company faced continued declines in Assets Under Management (AUM). This decline in AUM, fueled by market volatility and net outflows, impacted overall profitability. Despite these challenges, AllianceBernstein managed expenses effectively, leading to a modest increase in operating income compared to the prior year.

Click here to download our most recent Sure Analysis report on AB (preview of page 1 of 3 shown below):

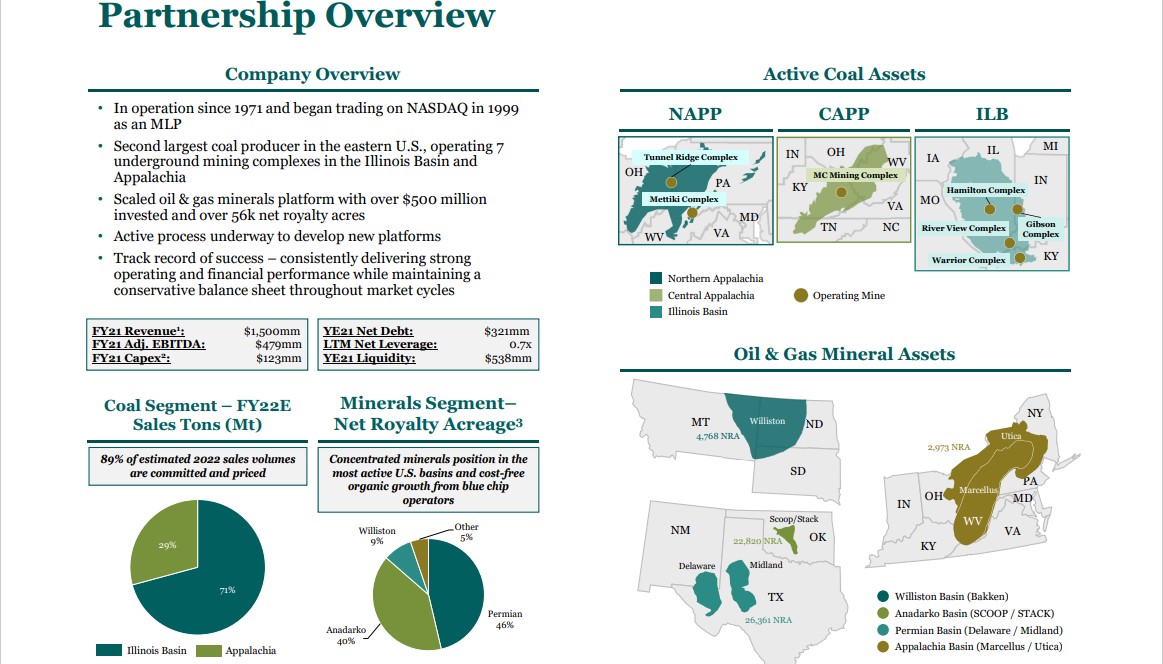

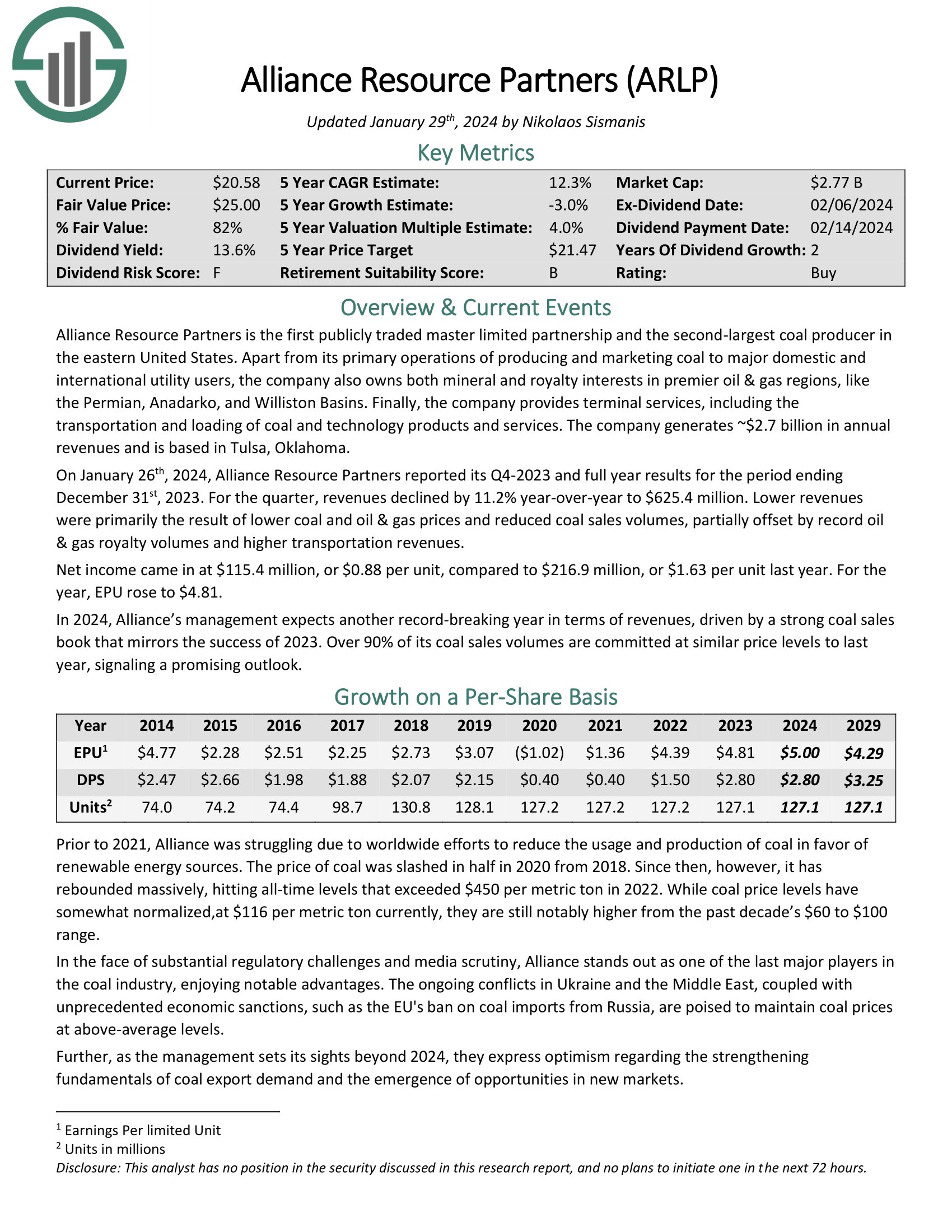

MLP #5: Alliance Resource Partners LP (ARLP)

- 5-year expected annual returns: 13.2%

Alliance Resource Partners is the second-largest coal producer in the eastern United States. Apart from its primary operations of producing and marketing coal to major domestic and international utility users, the company also owns both mineral and royalty interests in premier oil & gas regions, like the Permian, Anadarko, and Williston Basins.

Finally, the company provides terminal services, including the transportation and loading of coal and technology products and services. The company generates ~$1.6 billion in annual revenues and is based in Tulsa, Oklahoma.

On January 26th, 2024, Alliance Resource Partners reported its Q4-2023 and full year results for the period ending December 31st, 2023. For the quarter, revenues declined by 11.2% year-over-year to $625.4 million. Lower revenues were primarily the result of lower coal and oil & gas prices and reduced coal sales volumes, partially offset by record oil & gas royalty volumes and higher transportation revenues.

Click here to download our most recent Sure Analysis report on Alliance Resource Partners (preview of page 1 of 3 shown below):

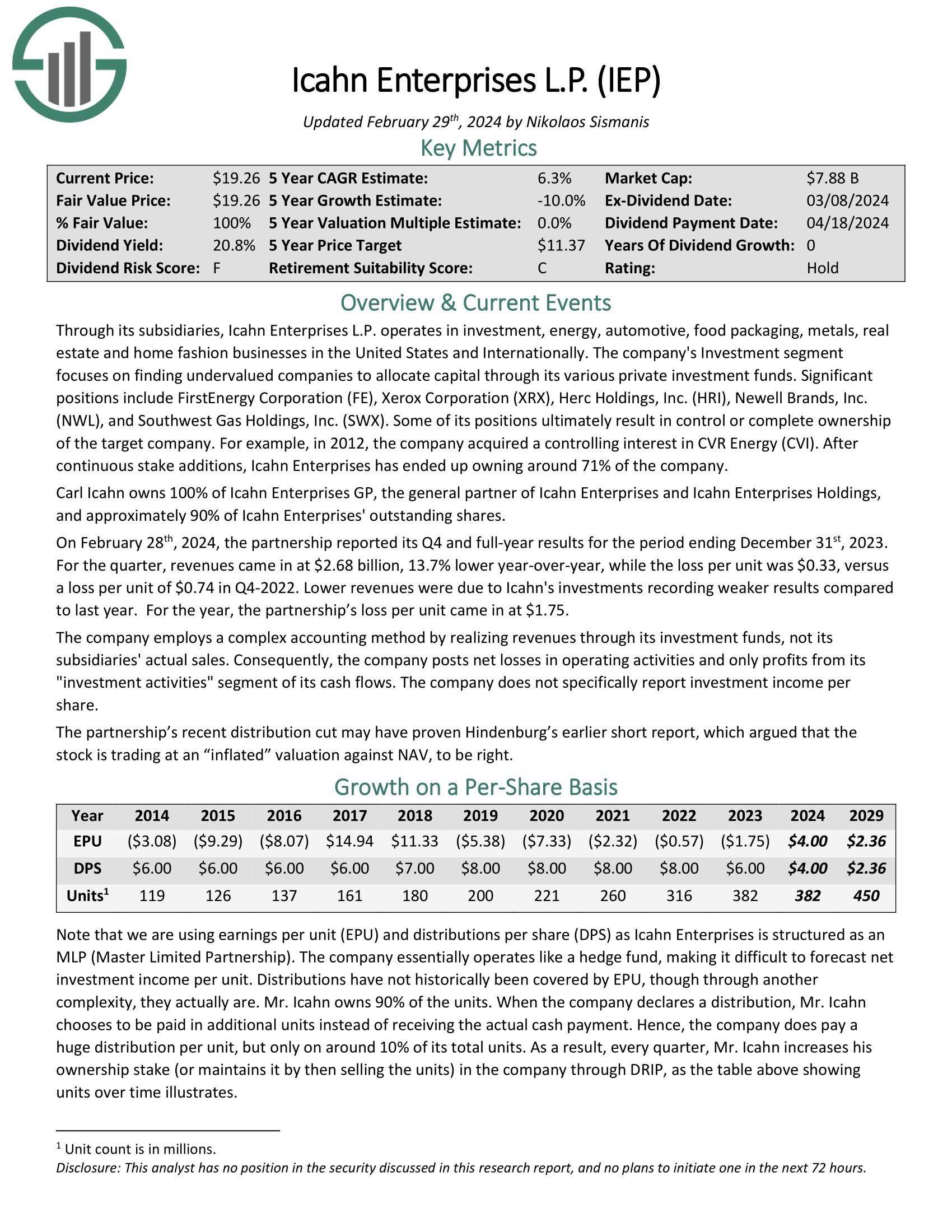

MLP #4: Icahn Enterprises LP (IEP)

- 5-year expected annual returns: 12.8%

Icahn Enterprises L.P. operates in investment, energy, automotive, food packaging, metals, real estate and home fashion businesses in the United States and Internationally. The company’s Investment segment focuses on finding undervalued companies to allocate capital through its various private investment funds.

Significant positions include FirstEnergy Corporation (FE), Xerox Corporation (XRX), Herc Holdings, Inc. (HRI), Newell Brands, Inc. (NWL), and Southwest Gas Holdings, Inc. (SWX). Some of its positions ultimately result in control or complete ownership of the target company.

On February 28th, 2024, the partnership reported its Q4 and full-year results for the period ending December 31st, 2023. For the quarter, revenues came in at $2.68 billion, 13.7% lower year-over-year, while the loss per unit was $0.33, versus a loss per unit of $0.74 in Q4-2022.

Click here to download our most recent Sure Analysis report on IEP (preview of page 1 of 3 shown below):

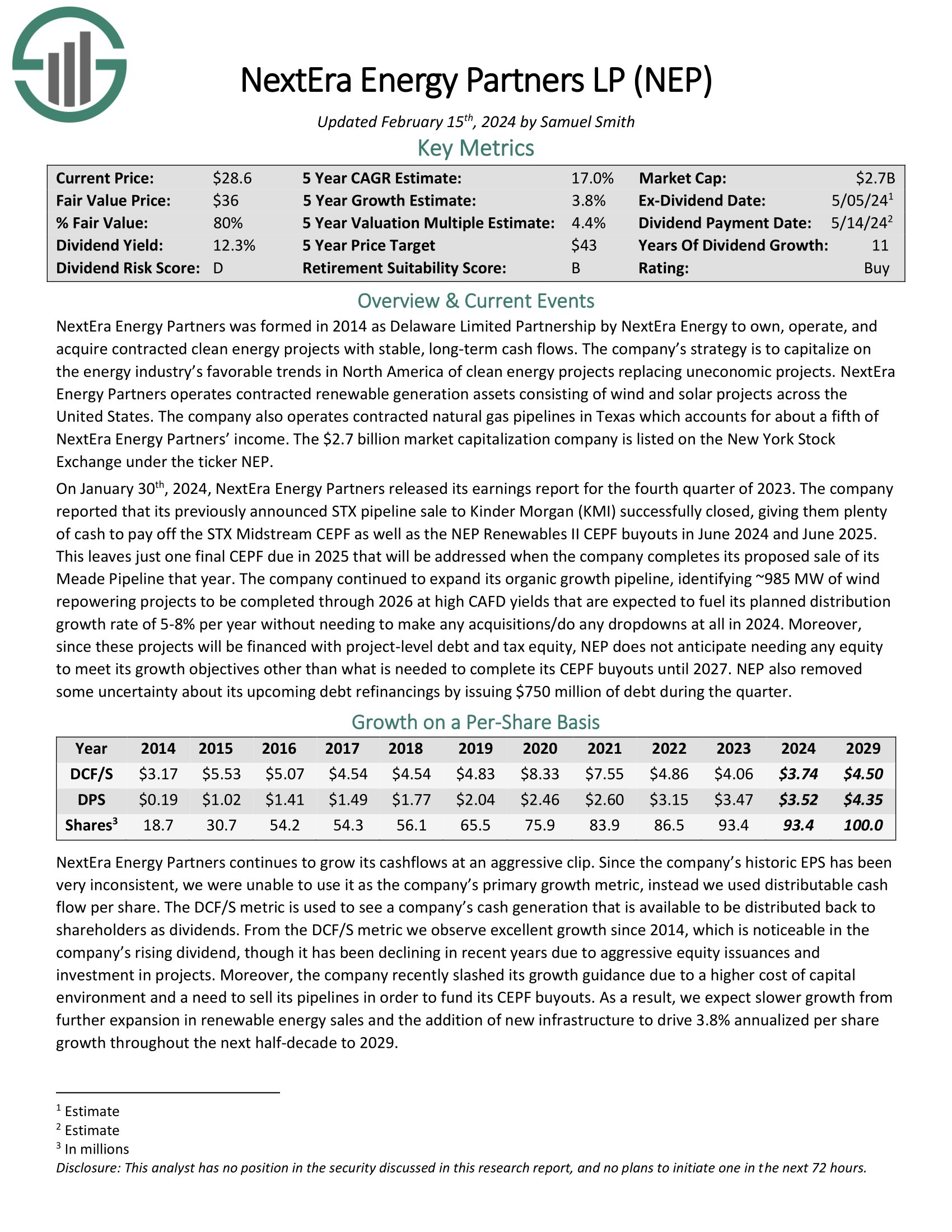

MLP #3: NextEra Energy Partners (NEP)

- 5-year expected annual returns: 16.7%

NextEra Energy Partners was formed in 2014 as Delaware Limited Partnership by NextEra Energy to own, operate, and acquire contracted clean energy projects with stable, long-term cash flows. The company’s strategy is to capitalize on the energy industry’s favorable trends in North America of clean energy projects replacing uneconomic projects.

NextEra Energy Partners operates contracted renewable generation assets consisting of wind and solar projects across the United States. The company also operates contracted natural gas pipelines in Texas.

On January 30th, 2024, NextEra Energy Partners released its earnings report for the fourth quarter of 2023. The company reported that its previously announced STX pipeline sale to Kinder Morgan (KMI) successfully closed, giving them plenty of cash to pay off the STX Midstream CEPF as well as the NEP Renewables II CEPF buyouts in June 2024 and June 2025.

Click here to download our most recent Sure Analysis report on NEP (preview of page 1 of 3 shown below):

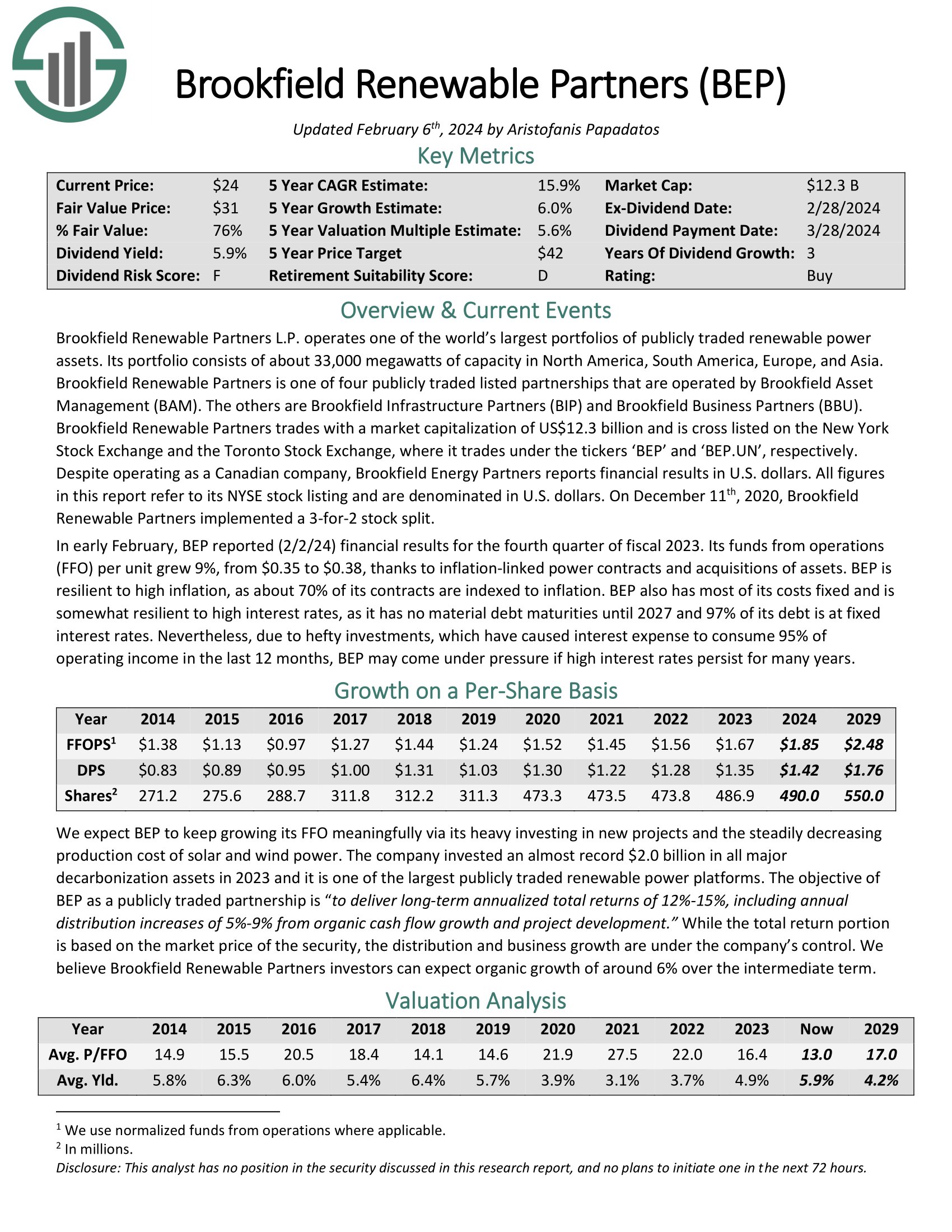

MLP #2: Brookfield Energy Partners LP (BEP)

- 5-year expected annual returns: 17.2%

Brookfield Renewable Partners L.P. operates one of the world’s largest portfolios of publicly traded renewable power assets. Its portfolio consists of about 31,300 megawatts of capacity in North America, South America, Europe, and Asia.

Brookfield Renewable Partners is one of four publicly traded listed partnerships that are operated by Brookfield Asset Management (BAM). The others are Brookfield Infrastructure Partners (BIP) and Brookfield Business Partners (BBU).

In early February, BEP reported (2/2/24) financial results for the fourth quarter of fiscal 2023. Its funds from operations per unit grew 9%, from $0.35 to $0.38, thanks to inflation-linked power contracts and acquisitions of assets. BEP is resilient to high inflation, as about 70% of its contracts are indexed to inflation.

Click here to download our most recent Sure Analysis report on Brookfield Renewable Partners (preview of page 1 of 3 shown below):

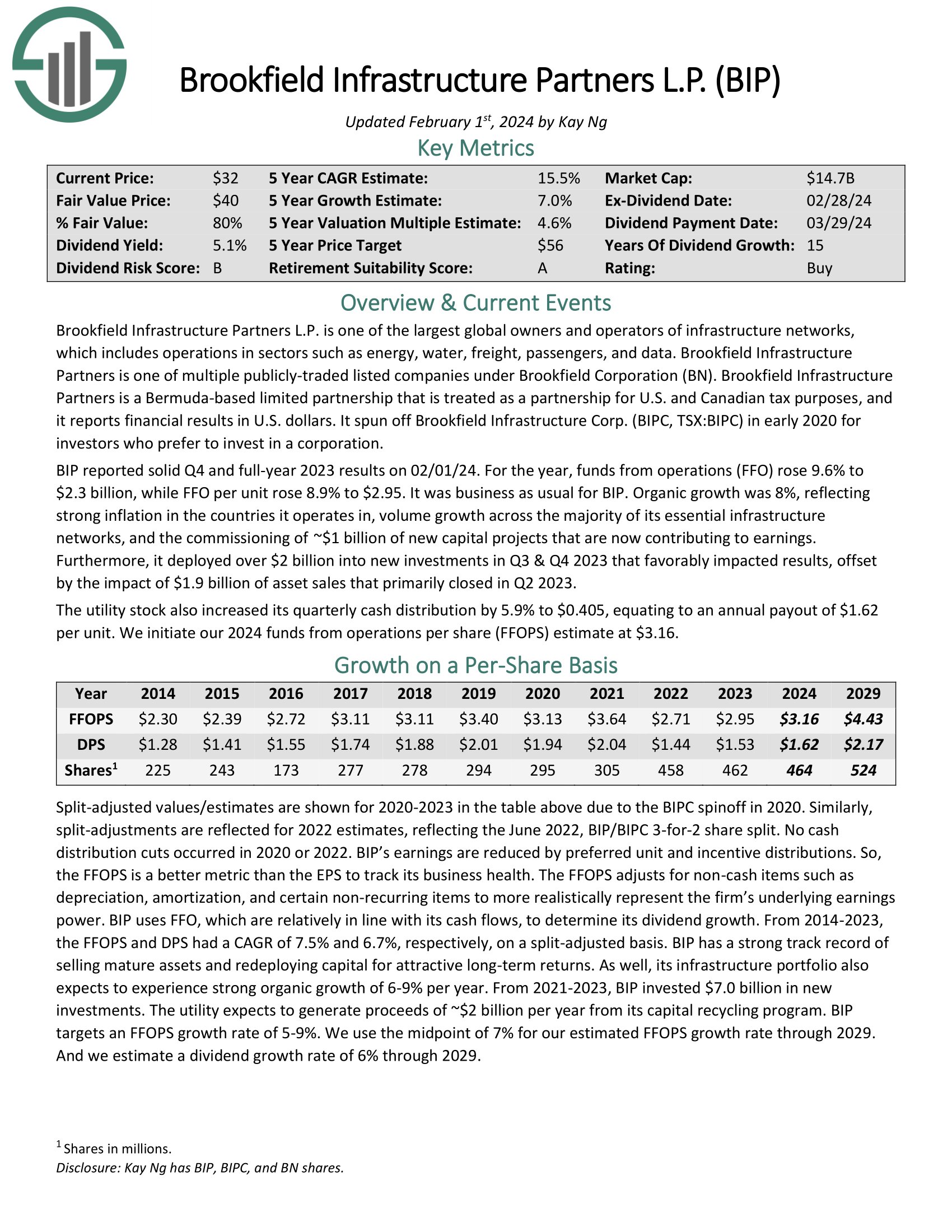

MLP #1: Brookfield Infrastructure Partners LP (BIP)

- 5-year expected annual returns: 17.9%

Brookfield Infrastructure Partners L.P. is one of the largest global owners and operators of infrastructure networks, which includes operations in sectors such as energy, water, freight, passengers, and data. Brookfield Infrastructure Partners is one of four publicly-traded listed partnerships that is operated by Brookfield Asset Management (BAM).

BIP reported solid Q4 and full-year 2023 results on 02/01/24. For the year, funds from operations rose 9.6% to $2.3 billion, while FFO per unit rose 8.9% to $2.95. It was business as usual for BIP. Organic growth was 8%, reflecting strong inflation in the countries it operates in, volume growth across the majority of its essential infrastructure networks, and the commissioning of ~$1 billion of new capital projects that are now contributing to earnings.

Click here to download our most recent Sure Analysis report on Brookfield Infrastructure Partners (preview of page 1 of 3 shown below):

MLP ETFs, ETNs, & Mutual Funds

There are 3 primary ways to invest in MLPs:

- By investing in units of individual publicly traded MLPs

- By investing in a MLP ETF or mutual fund

- By investing in a MLP ETN

Note: ETN stands for ‘exchange traded note’

The difference between investing directly in a company (normal stock investing) versus investing in a mutual fund or ETF is very clear. It is simply investing in one security versus a group of securities.

ETNs are different. Unlike mutual funds or ETFs, ETNs don’t actually own any underlying shares or units of real businesses. Instead, ETNs are financial instruments backed by the financial institution (typically a large bank) that issued them. They perfectly track the value of an index. The disadvantage to ETNs is that they expose investors to the possibility of a total loss if the backing institution were to go bankrupt.

The advantage to investing in a MLP ETN is that distribution income is tracked, but paid via a 1099. This eliminates the tax disadvantages of MLPs (no K-1s, UBTI, etc.). This unique feature may appeal to investors who don’t want to hassle with a more complicated tax situation. The J.P. Morgan Alerian MLP ETN makes a good choice in this case.

Purchasing individual securities is preferable for many, as it allows investors to concentrate on their best ideas. But ETFs have their place as well, especially for investors looking for diversification benefits.

Final Thoughts

Master Limited Partnerships are a misunderstood asset class. They offer diversification, tax-advantaged and tax-deferred income, high yields, and have historically generated excellent total returns.

You can download your free copy of all MLPs by clicking on the link below:

The asset class is likely under-appreciated because of its more complicated tax status.

MLPs are generally attractive for income investors, due to their high yields.

As always, investors need to conduct their own due diligence regarding the unique tax effects and risk factors before purchasing MLPs.

The MLPs on this list could be a good place to find long-term buying opportunities among the beaten-down MLPs. To see the highest-yielding MLPs, click here.

Additionally, MLPs are not the only way to find high levels of income. The following lists contain many more stocks that regularly pay rising dividends.

- The Dividend Aristocrats List: 68 stocks in the S&P 500 Index with 25+ years of consecutive dividend increases.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 54 stocks with 50+ years of consecutive dividend increases.

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.