Updated on June 22nd, 2026 by Bob Ciura

High dividend stocks are attractive for income investors. With the S&P 500 average yield at just 1.1%, it has gotten harder to find suitable yields in the stock market.

Fortunately, there are still plenty of quality high dividend stocks to choose from. With that in mind, we have created a free list of over 200 high dividend stocks with dividend yields above 4%.

You can download your copy of the high dividend stocks list below:

However, investors should remember that extremely high yields can be deceiving. There are many examples of high dividend stocks reducing or eliminating their dividends.

As a result, investors should look for high dividend stocks that also have sustainable payouts. This means investors will receive the benefits of high income for many years.

The 10 high dividend stocks below were found based on a qualitative assessment of their individual business models and future growth prospects.

Table of Contents

- High Dividend Stock For The Long Run #10: PepsiCo Inc. (PEP)

- High Dividend Stock For The Long Run #9: Bristol-Myers Squibb (BMY)

- High Dividend Stock For The Long Run #8: T. Rowe Price Group (TROW)

- High Dividend Stock For The Long Run #7: Hormel Foods (HRL)

- High Dividend Stock For The Long Run #6: Clorox Co. (CLX)

- High Dividend Stock For The Long Run #5: Prudential Financial (PRU)

- High Dividend Stock For The Long Run #4: Realty Income (O)

- High Dividend Stock For The Long Run #3: Sanofi (SNY)

- High Dividend Stock For The Long Run #2: Enterprise Products Partners LP (EPD)

- High Dividend Stock For The Long Run #1: Altria Group (MO)

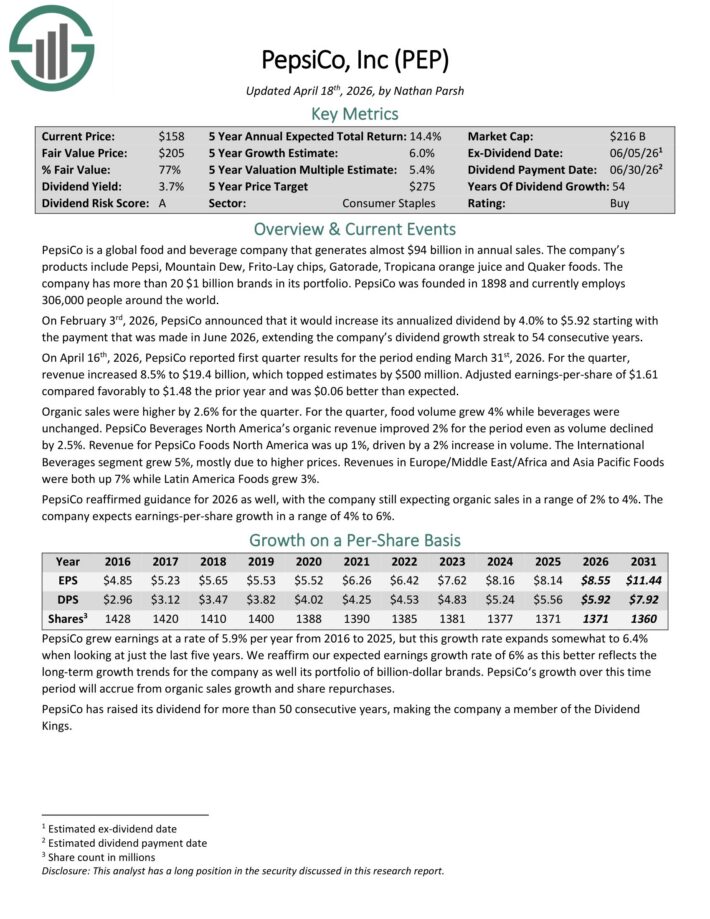

High Dividend Stock For The Long Run #10: PepsiCo Inc. (PEP)

- Dividend Yield: 4.2%

PepsiCo is a global food and beverage company that generates almost $94 billion in annual sales. The company’s products include Pepsi, Mountain Dew, Frito-Lay chips, Gatorade, Tropicana orange juice and Quaker foods.

The company has more than 20 $1 billion brands in its portfolio. PepsiCo was founded in 1898 and currently employs

306,000 people around the world.

On February 3rd, 2026, PepsiCo increased its annualized dividend by 4.0% to $5.92 starting with the payment that was made in June 2026, extending the company’s dividend growth streak to 54 consecutive years.

On April 16th, 2026, PepsiCo reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue increased 8.5% to $19.4 billion, which topped estimates by $500 million.

Adjusted earnings-per-share of $1.61 compared favorably to $1.48 the prior year and was $0.06 better than expected.

Organic sales were higher by 2.6% for the quarter. For the quarter, food volume grew 4% while beverages were unchanged.

PepsiCo Beverages North America’s organic revenue improved 2% for the period even as volume declined by 2.5%. Revenue for PepsiCo Foods North America was up 1%, driven by a 2% increase in volume.

The International Beverages segment grew 5%, mostly due to higher prices. Revenue in Europe/Middle East/Africa and Asia Pacific Foods were both up 7% while Latin America Foods grew 3%.

PepsiCo reaffirmed guidance for 2026 as well, with the company still expecting organic sales in a range of 2% to 4%. The company expects earnings-per-share growth in a range of 4% to 6%.

Click here to download our most recent Sure Analysis report on PEP (preview of page 1 of 3 shown below):

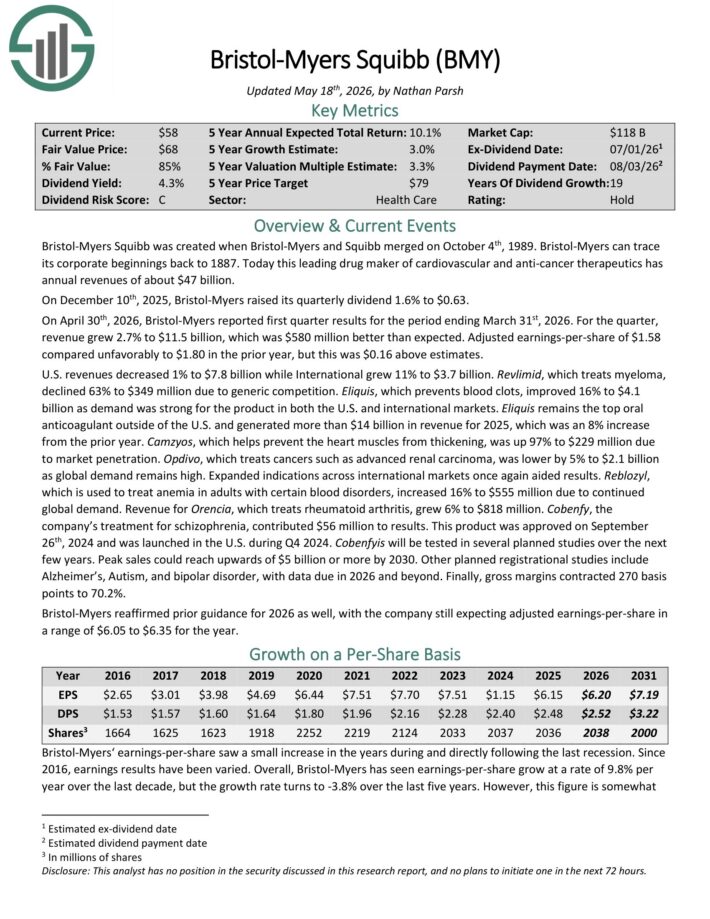

High Dividend Stock For The Long Run #9: Bristol-Myers Squibb (BMY)

- Dividend Yield: 4.7%

Bristol-Myers Squibb is a leading drug maker of cardiovascular and anti-cancer therapeutics with annual revenues of about $47 billion.

On December 10th, 2025, Bristol-Myers raised its quarterly dividend 1.6% to $0.63.

On April 30th, 2026, Bristol-Myers reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue grew 2.7% to $11.5 billion, which was $580 million better than expected.

Adjusted earnings-per-share of $1.58 compared unfavorably to $1.80 in the prior year, but this was $0.16 above estimates.

Sales of Eliquis, which prevents blood clots, improved 16% to $4.1 billion as demand was strong for the product in both the U.S. and international markets.

Eliquis remains the top oral anticoagulant outside of the U.S. and generated more than $14 billion in revenue for 2025, which was an 8% increase from the prior year.

Other planned registrational studies include Alzheimer’s, Autism, and bipolar disorder, with data due in 2026 and beyond.

Bristol-Myers reaffirmed prior guidance for 2026 as well with the company still expecting adjusted earnings-per-share in a range of $6.05 to $6.35 for the year.

Click here to download our most recent Sure Analysis report on BMY (preview of page 1 of 3 shown below):

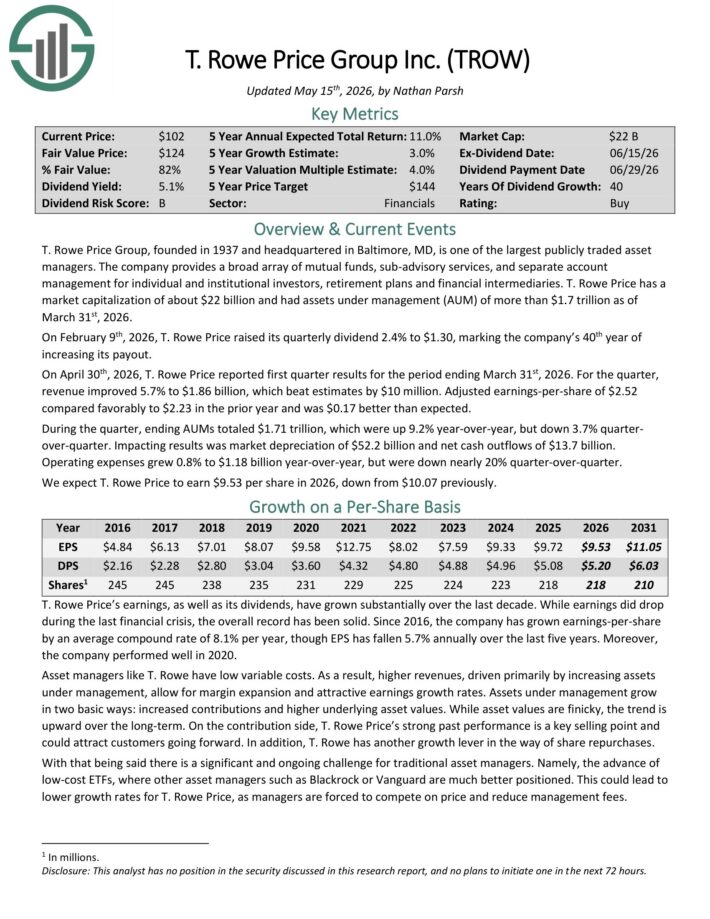

High Dividend Stock For The Long Run #8: T. Rowe Price Group (TROW)

- Dividend Yield: 4.8%

T. Rowe Price Group is one of the largest publicly traded asset managers. The company provides a broad array of mutual funds, sub-advisory services, and separate account management for individual and institutional investors, retirement plans and financial intermediaries.

T. Rowe Price had assets under management (AUM) of nearly $1.8 trillion as of December 31st, 2025.

On February 11th, 2025, T. Rowe Price raised its quarterly dividend 2.4% to $1.27, marking the company’s 39th year of increasing its payout.

On April 30th, 2026, T. Rowe Price reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue improved 5.7% to $1.86 billion, which beat estimates by $10 million.

Adjusted earnings-per-share of $2.52 compared favorably to $2.23 in the prior year and was $0.17 better than expected.

During the quarter, ending AUMs totaled $1.71 trillion, which were up 9.2% year-over-year, but down 3.7% quarter-over-quarter.

Impacting results was market depreciation of $52.2 billion and net cash outflows of $13.7 billion. Operating expenses grew 0.8% to $1.18 billion year-over-year, but were down nearly 20% quarter-over-quarter.

Click here to download our most recent Sure Analysis report on TROW (preview of page 1 of 3 shown below):

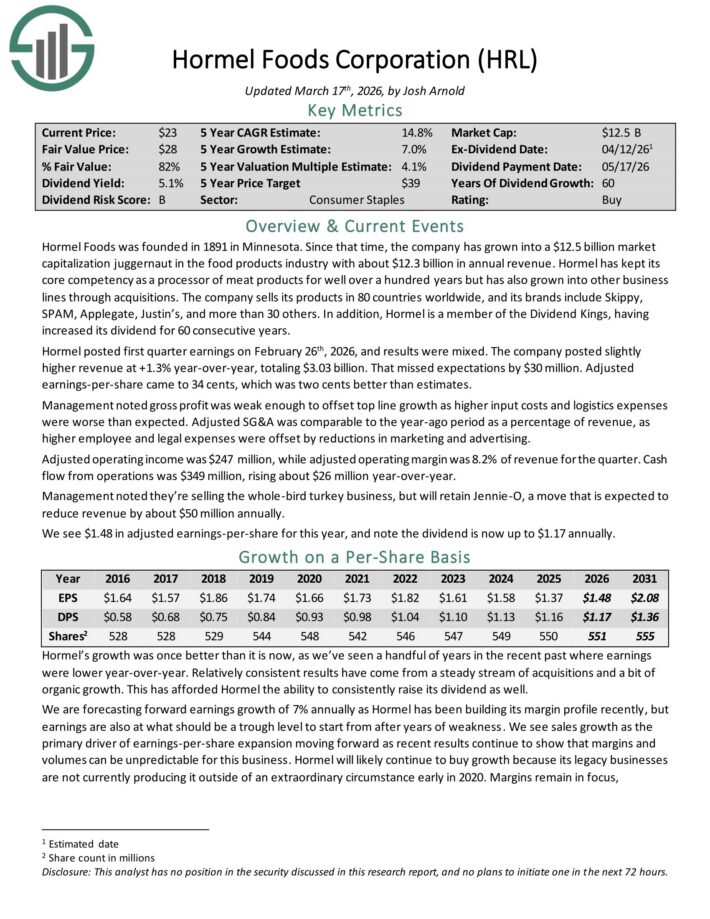

High Dividend Stock For The Long Run #7: Hormel Foods (HRL)

- Dividend Yield: 4.8%

Hormel Foods was founded in 1891 in Minnesota. Since that time, the company has grown into a juggernaut in the food products industry with about $12.3 billion in annual revenue.

The company sells its products in 80 countries worldwide, and its brands include Skippy, SPAM, Applegate, Justin’s, and more than 30 others.

Hormel posted first quarter earnings on February 26th, 2026, and results were mixed. The company posted slightly higher revenue at +1.3% year-over-year, totaling $3.03 billion. That missed expectations by $30 million.

Adjusted earnings-per-share came to 34 cents, which was two cents better than estimates.

Management noted gross profit was weak enough to offset top line growth as higher input costs and logistics expenses were worse than expected.

Adjusted SG&A was comparable to the year-ago period as a percentage of revenue, as higher employee and legal expenses were offset by reductions in marketing and advertising.

Adjusted operating income was $247 million, while adjusted operating margin was 8.2% of revenue for the quarter. Cash flow from operations was $349 million, rising about $26 million year-over-year.

Click here to download our most recent Sure Analysis report on HRL (preview of page 1 of 3 shown below):

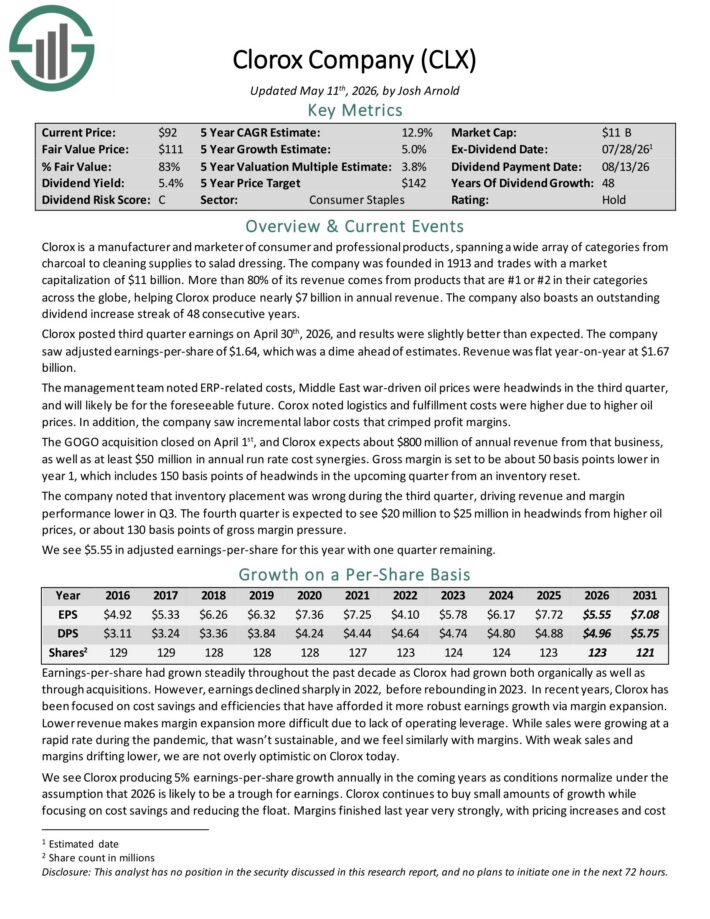

High Dividend Stock For The Long Run #6: Clorox Co. (CLX)

- Dividend Yield: 5.1%

Clorox is a manufacturer and marketer of consumer and professional products, spanning a wide array of categories from charcoal to cleaning supplies to salad dressing.

More than 80% of its revenue comes from products that are #1 or #2 in their categories across the globe, helping Clorox produce more than $7 billion in annual revenue.

The company also boasts an outstanding dividend increase streak of 48 consecutive years.

Clorox posted third quarter earnings on April 30th, 2026, and results were slightly better than expected. The company saw adjusted earnings-per-share of $1.64, which was a dime ahead of estimates.

Revenue was flat year-on-year at $1.67 billion. The management team noted ERP-related costs, Middle East war-driven oil prices were headwinds in the third quarter, and will likely be for the foreseeable future.

Corox noted logistics and fulfillment costs were higher due to higher oil prices. In addition, the company saw incremental labor costs that crimped profit margins.

The GOGO acquisition closed on April 1st, and Clorox expects about $800 million of annual revenue from that business, as well as at least $50 million in annual run rate cost synergies.

Click here to download our most recent Sure Analysis report on CLX (preview of page 1 of 3 shown below):

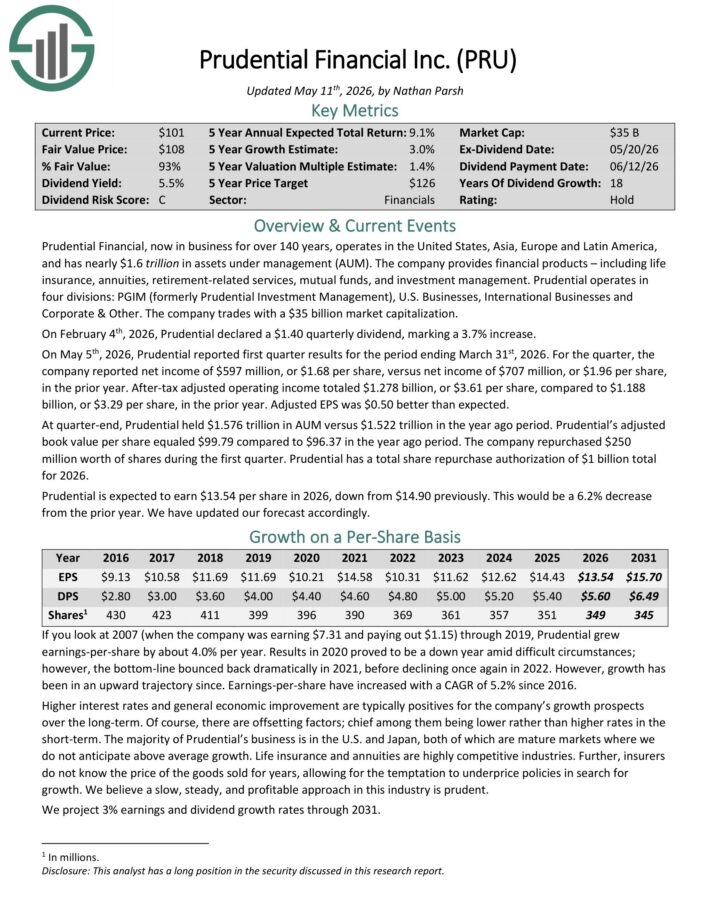

High Dividend Stock For The Long Run #5: Prudential Financial (PRU)

- Dividend Yield: 5.4%

Prudential Financial, now in business for over 140 years, operates in the United States, Asia, Europe and Latin America, with more than $1.6 trillion in assets under management (AUM).

The company provides financial products – including life insurance, annuities, retirement-related services, mutual funds, and investment management.

Prudential operates in four divisions: PGIM (formerly Prudential Investment Management), U.S. Businesses, International Businesses and Corporate & Other.

On May 5th, 2026, Prudential reported first quarter results. For the quarter, the company reported net income of $597 million, or $1.68 per share, versus net income of $707 million, or $1.96 per share, in the prior year.

After-tax adjusted operating income totaled $1.278 billion, or $3.61 per share, compared to $1.188 billion, or $3.29 per share, in the prior year. Adjusted EPS was $0.50 better than expected.

At quarter-end, Prudential held $1.576 trillion in AUM versus $1.522 trillion in the year ago period. Prudential’s adjusted book value per share equaled $99.79 compared to $96.37 in the year ago period.

The company repurchased $250 million worth of shares during the first quarter. Prudential has a total share repurchase authorization of $1 billion total for 2026.

Click here to download our most recent Sure Analysis report on PRU (preview of page 1 of 3 shown below):

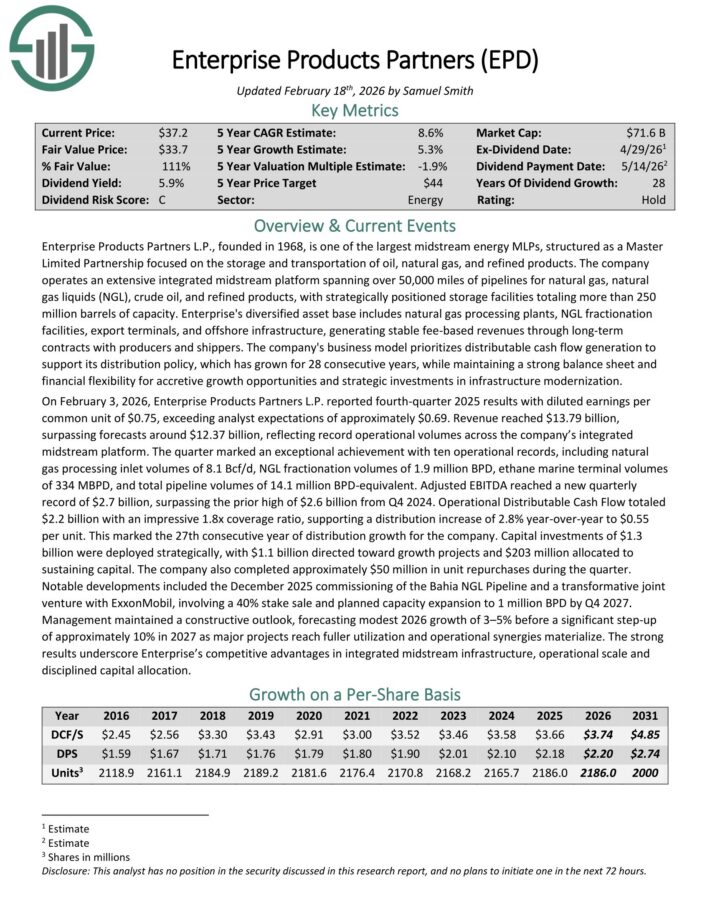

High Dividend Stock For The Long Run #5: Enterprise Products Partners LP (EPD)

- Dividend Yield: 5.8%

Enterprise Products Partners was founded in 1968. It is structured as a Master Limited Partnership, or MLP, and operates as an oil and gas storage and transportation company.

Enterprise Products has a large asset base which consists of nearly 50,000 miles of natural gas, natural gas liquids, crude oil, and refined products pipelines.

It also has storage capacity of more than 250 million barrels. These assets collect fees based on volumes of materials transported and stored.

On February 3, 2026, Enterprise Products Partners L.P. reported fourth-quarter 2025 results with diluted earnings per common unit of $0.75, exceeding analyst expectations of approximately $0.69.

Revenue reached $13.79 billion, surpassing forecasts around $12.37 billion, reflecting record operational volumes across the company’s integrated midstream platform.

The quarter marked an exceptional achievement with ten operational records, including natural gas processing inlet volumes of 8.1 Bcf/d, NGL fractionation volumes of 1.9 million BPD, ethane marine terminal volumes of 334 MBPD, and total pipeline volumes of 14.1 million BPD-equivalent.

Adjusted EBITDA reached a new quarterly record of $2.7 billion, surpassing the prior high of $2.6 billion from Q4 2024. Operational Distributable Cash Flow totaled $2.2 billion with an impressive 1.8x coverage ratio, supporting a distribution increase of 2.8% year-over-year to $0.55 per unit.

This marked the 27th consecutive year of distribution growth for the company.

Click here to download our most recent Sure Analysis report on EPD (preview of page 1 of 3 shown below):

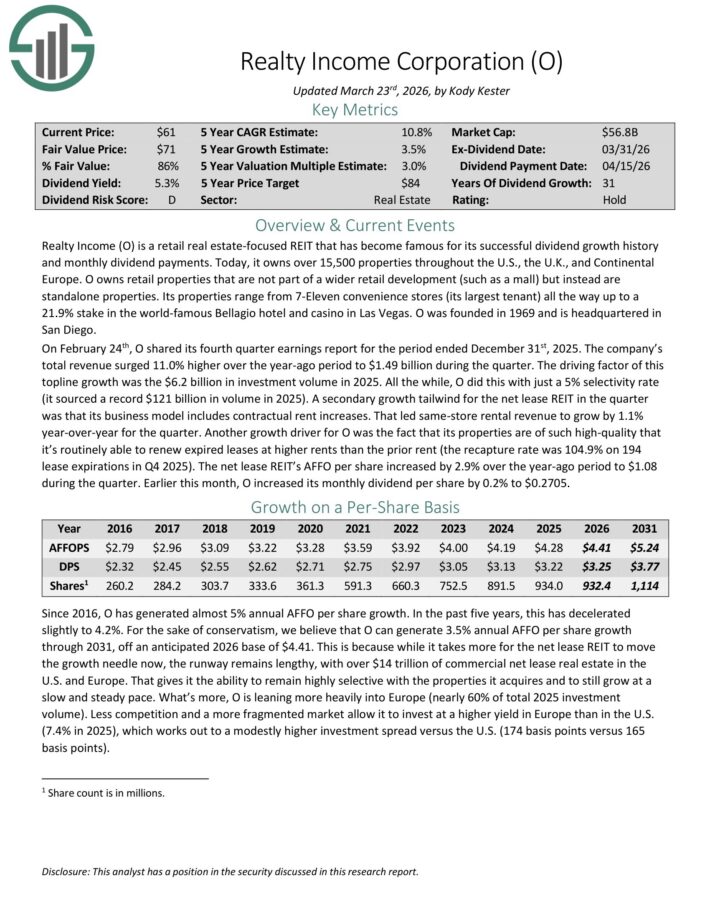

High Dividend Stock For The Long Run #4: Realty Income (O)

- Dividend Yield: 5.4%

Realty Income is a retail real estate-focused REIT that has become famous for its successful dividend growth history and monthly dividend payments.

Today, it owns over 15,500 properties throughout the U.S., the U.K., and Continental Europe. It owns retail properties that are not part of a wider retail development (such as a mall) but instead are standalone properties.

Its properties range from 7-Eleven convenience stores (its largest tenant) all the way up to a 21.9% stake in the Bellagio hotel and casino in Las Vegas.

On February 24th, O shared its fourth quarter earnings report for the period ended December 31st, 2025. The company’s total revenue surged 11.0% higher over the year-ago period to $1.49 billion during the quarter.

The driving factor of this top-line growth was the $6.2 billion in investment volume in 2025. All the while, the company did this with just a 5% selectivity rate (it sourced a record $121 billion in volume in 2025).

A secondary growth tailwind for the net lease REIT in the quarter was that its business model includes contractual rent increases. That led same-store rental revenue to grow by 1.1% year-over-year for the quarter.

The net lease REIT’s AFFO per share increased by 2.9% over the year-ago period to $1.08 during the quarter.

Click here to download our most recent Sure Analysis report on O (preview of page 1 of 3 shown below):

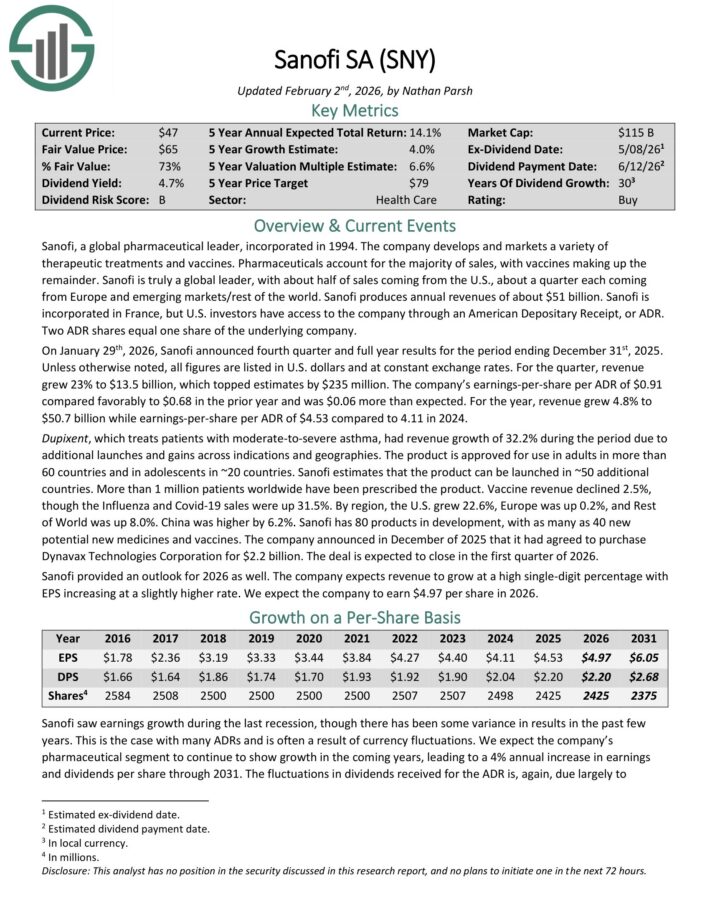

High Dividend Stock For The Long Run #3: Sanofi (SNY)

- Dividend Yield: 5.7%

Sanofi is a global pharmaceutical leader that develops a variety of therapeutic treatments and vaccines.

Pharmaceuticals account for the majority of sales, with vaccines making up the remainder. Sanofi produces annual revenues of about $51 billion.

Sanofi is incorporated in France, but U.S. investors have access to the company through an American Depositary Receipt, or ADR. Two ADR shares equal one share of the underlying company.

On January 29th, 2026, Sanofi announced fourth quarter and full year results. Unless otherwise noted, all figures are listed in U.S. dollars and at constant exchange rates.

For the quarter, revenue grew 23% to $13.5 billion, which topped estimates by $235 million. The company’s earnings-per-share per ADR of $0.91 compared favorably to $0.68 in the prior year and was $0.06 more than expected.

For the year, revenue grew 4.8% to $50.7 billion while earnings-per-share per ADR of $4.53 compared to 4.11 in 2024.

Dupixent, which treats patients with moderate-to-severe asthma, had revenue growth of 32.2% during the period due to additional launches and gains across indications and geographies.

Sanofi has 80 products in development, with as many as 40 new potential new medicines and vaccines.

Sanofi provided an outlook for 2026 as well. The company expects revenue to grow at a high single-digit percentage with EPS increasing at a slightly higher rate.

Click here to download our most recent Sure Analysis report on SNY (preview of page 1 of 3 shown below):

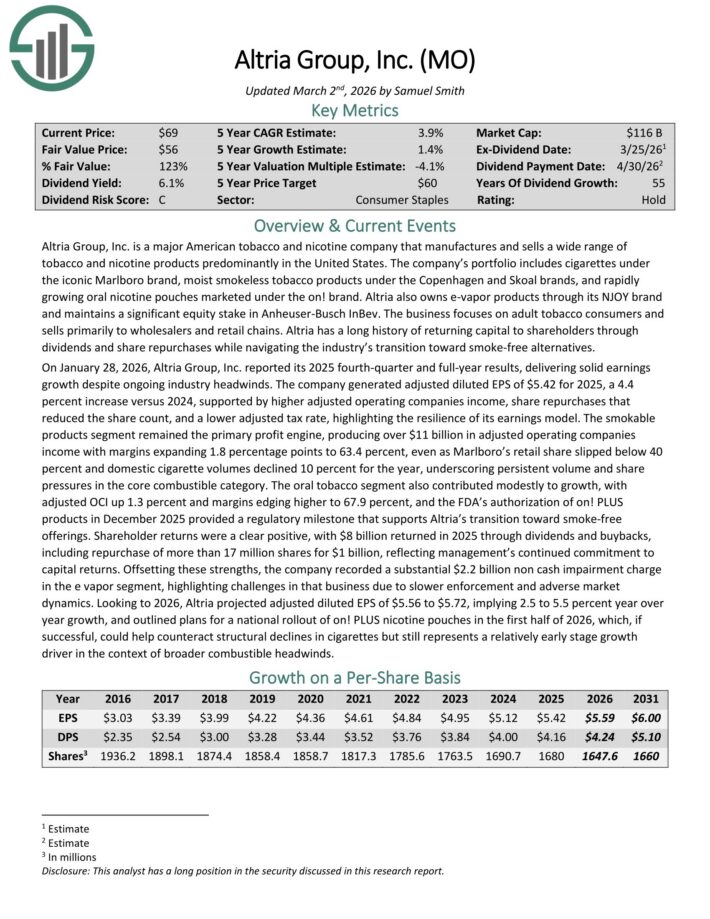

High Dividend Stock For The Long Run #1: Altria Group (MO)

- Dividend Yield: 6.1%

Altria is a tobacco stock that sells cigarettes, chewing tobacco, cigars, e-cigarettes, and more under a variety of brands, including Marlboro, Skoal, and Copenhagen, among others.

This is a period of transition for Altria. The decline in the U.S. smoking rate continues. In response, Altria has invested heavily in new products that appeal to changing consumer preferences, as the smoke-free category continues to grow.

The company also has a 35% investment stake in e-cigarette maker JUUL, and a 45% stake in the Canadian cannabis producer Cronos Group (CRON).

On January 28, 2026, Altria Group, Inc. reported its 2025 fourth-quarter and full-year results. The company generated adjusted diluted EPS of $5.42 for 2025, a 4.4% increase versus 2024.

EPS growth was supported by higher adjusted operating companies income, share repurchases that reduced the share count, and a lower adjusted tax rate.

The smokable products segment remained the primary profit engine, producing over $11 billion in adjusted operating companies income with margins expanding 1.8 percentage points to 63.4%.

Margin expansion occurred even as Marlboro’s retail share slipped below 40% and domestic cigarette volumes declined 10% for the year. The oral tobacco segment also contributed modestly to growth, with adjusted OCI up 1.3%.

Looking to 2026, Altria projected adjusted diluted EPS of $5.56 to $5.72, implying 2.5% to 5.5% year-over-year growth.

Click here to download our most recent Sure Analysis report on Altria (preview of page 1 of 3 shown below):

Additional Reading

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research