Updated on March 11th, 2025 by Nathan Parsh

Investors looking for high-quality dividend growth stocks should first consider the Dividend Aristocrats. These are an exclusive list of 69 stocks in the S&P 500 Index with 25+ years of consecutive dividend increases.

The Dividend Aristocrats are an elite group of dividend growth stocks. For this reason, we created a full list of all 69 Dividend Aristocrats.

You can download your free copy of the Dividend Aristocrats list, along with important metrics like dividend yields and price-to-earnings ratios, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

T. Rowe Price Group (TROW) has increased its dividend for 39 years in a row, thanks to its strong brand, a highly profitable business, and future growth potential.

The stock’s dividend yield is 5.2%, which is above the ~1.3% average dividend yield of the broader S&P 500 Index. Taken together, T. Rowe Price stock possesses many of the qualities dividend growth investors typically look for.

Business Overview

T. Rowe Price, Jr., founded it in 1937. In the eight decades since, it has grown into one of the largest financial services providers in the United States. Today, the company has a market cap of ~$22 billion and impressive assets under management.

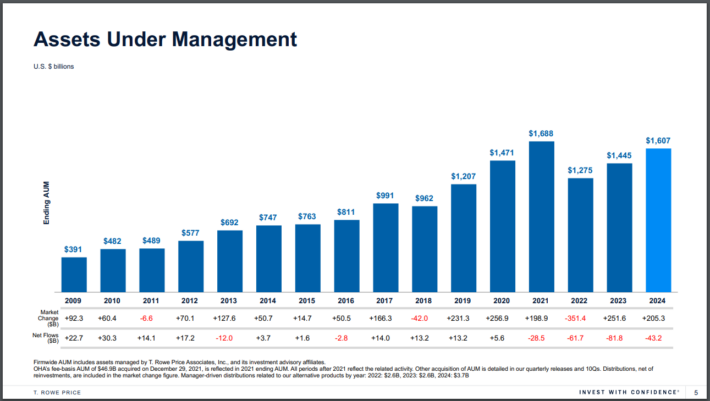

Source: Investor Presentation

T. Rowe Price ended 2024 with more than $1.6 trillion in assets under management.

The company provides mutual funds, advisory services, and separately managed accounts for individuals, institutional investors, retirement plans, and financial intermediaries. T. Rowe Price has a diverse client base in terms of assets and client type.

This is a challenging climate for asset managers. Some investors have grown weary of higher trading costs and annual fees. The onset of low-cost exchange-traded funds, or ETFs, has successfully lured client assets away from traditional mutual funds that have higher fees. This has caused brokers to lower commissions and fees to retain client assets.

However, company has strong growth potential in the years ahead.

Growth Prospects

T. Rowe Price has several catalysts for future growth. On February 5th, 2025, T. Rowe Price announced its fourth quarter and full-year results for the period ending December 31st, 2024. For the quarter, revenue increased 11% to $1.82 billion, which was $50 million below estimates. Adjusted earnings-per-share were $2.12 compared to $1.72 in the prior year, but this was $0.09 less than expected.

For the year, revenue grew 9.8% to $7.1 billion, and adjusted earnings-per-share were $9.33, compared to $7.59in 2023.

During the quarter, assets under management (AUM) of $1.639 trillion were up 19.2% year-over-year and higher by 3.1% sequentially. Market appreciation of $205.3 billion was partially offset by $43.2 billion of net client outflows. Operating expenses of $1.26 billion increased 0.1% year-over-year and grew 6.4% sequentially.

Since 2015, the company has grown earnings-per-share by an average compound rate of 8.1% annually. Moreover, the company performed well in 2020. Asset managers like T. Rowe have low variable costs. As a result, higher revenues, driven primarily by increasing assets under management, allow for margin expansion and attractive earnings growth rates.

Assets under management grow in two basic ways: increased contributions and higher underlying asset values. While asset values are finicky, the trend is upward over the long term. In addition, T. Rowe has another growth lever in the form of share repurchases. The company has shrunk its share count by an annual rate of 1.3% over the last decade.

Competitive Advantages & Recession Performance

T. Rowe Price’s competitive advantage comes from its brand recognition and expertise. The company enjoys a good reputation in the financial services industry. This helps generate fees, a significant driver of revenue. It has built this reputation through strong mutual fund performance.

T. Rowe Price considers its employees to be its most valuable assets. There is a good reason for this, It is critical for an asset management company to have qualified experts and retain top talent. This focus on building a strong brand gives the company competitive advantages, primarily the ability to keep existing clients and bring in new ones.

T. Rowe Price did not perform well during the Great Recession:

- 2007 earnings-per-share of $2.40

- 2008 earnings-per-share of $1.82 (24% decline)

- 2009 earnings-per-share of $1.65 (9% decline)

- 2010 earnings-per-share of $2.53 (53% increase)

As could be expected, T. Rowe Price experienced a sharp decline in earnings-per-share in 2008 and 2009. When stock markets decline, equity investors typically withdraw funds to raise cash.

Fortunately, the company remained profitable throughout the recession, allowing it to raise its dividend each year. T. Rowe Price quickly recovered in the aftermath of the Great Recession. Earnings increased significantly in 2010 and reached a new high by 2011.

Valuation & Expected Returns

We expect T. Rowe Price to produce adjusted earnings-per-share of $9.23 for 2025. Using the recent share price of ~$97, the stock has a price-to-earnings ratio of 10.5. We have a target price-to-earnings ratio of 14. If the stock valuation returns to the fair value estimate, then multiple expansion would add 5.9% to annual returns over the next five years.

The company does have a strong brand, with fairly consistent profitability and earnings growth. Even better, the stock appears undervalued today. We see earnings-per-share increasing at a rate of 3% annually through 2030 due to a combination of the sheer number of AUM and share repurchases.

Therefore, total returns would consist of the following:

- 3% earnings growth

- 5.2% dividend yield

- 5.9% multiple expansion

T. Rowe Price is expected to return 12.9% annually through 2030. T. Rowe Price is a particularly attractive stock for dividend growth. The company has raised its dividend for 39 years in a row. And the dividend is reasonably secure, with an expected payout ratio below 55% for this year.

Final Thoughts

Investors scanning the financial sector for dividend stocks may naturally land on the big banks.

In fact, most Dividend Aristocrats in the financial sector come from the insurance and investment management industries. This speaks volumes about the stability of their business models.

T. Rowe Price is an industry leader and should continue increasing its dividend yearly. The focus on lower fees will continue to be a headwind for the industry. That said, shares of T. Rowe Price earn a buy rating due to expected annual returns.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.