Published on March 16th, 2026 by Bob Ciura

Oil prices have been on the rise since the U.S. and Israel attacked Iran 0n February 28th.

On March 16th, WTI crude briefly reached $100 per barrel in the United States.

Oil prices are rising due to the potential for supply constraints, since the Strait of Hormuz handles roughly one-fifth of the world’s oil.

Rising oil prices will be a major tailwind for the world’s oil producers.

With this in mind, we compiled a list of nearly 50 energy stocks (along with important investing metrics such as dividend yields), available for download below:

In times of heightened geopolitical risk, income investors should turn to the relative stability of dividend stocks.

This article will list the 10 top-ranked energy sector dividend stocks in the Sure Analysis Research Database.

Master Limited Partnerships, royalty trusts, and international securities were excluded from this analysis.

We also omitted securities of energy companies whose primary business involves natural gas, to better focus on companies that will benefit from rising oil prices.

Table of Contents

The table of contents below allows for easy navigation. The list is sorted by annual expected return over the next five years, from lowest to highest.

- Top Energy Stock #10: Phillips 66 (PSX)

- Top Energy Stock #9: Baker Hughes Co. (BKR)

- Top Energy Stock #8: Diamondback Energy (FANG)

- Top Energy Stock #7: HF Sinclair (DINO)

- Top Energy Stock #6: Coterra Energy (CTRA)

- Top Energy Stock #5: Matador Resources (MTDR)

- Top Energy Stock #4: Devon Energy (DVN)

- Top Energy Stock #3: Cactus, Inc. (WHD)

- Top Energy Stock #2: EOG Resources (EOG)

- Top Energy Stock #1: World Kinect Corporation (WKC)

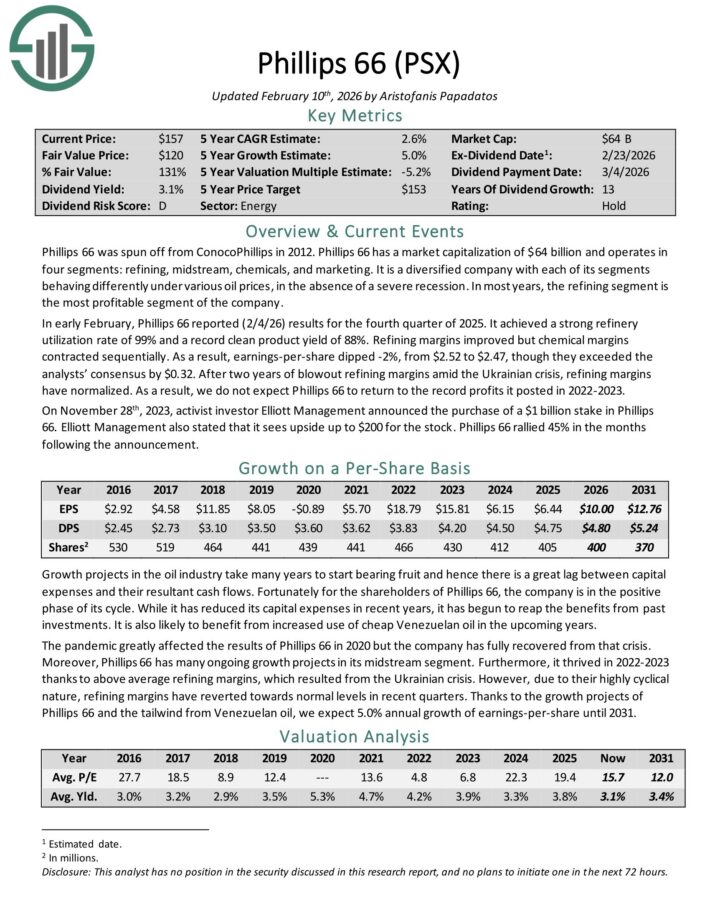

Top Energy Stock #10: Phillips 66 (PSX)

- Annual Expected Returns: 0.4%

Phillips 66 was spun off from ConocoPhillips in 2012. Phillips 66 operates in four segments: refining, midstream, chemicals, and marketing.

It is a diversified company with each of its segments behaving differently under various oil prices, in the absence of a severe recession. In most years, the refining segment is the most profitable segment of the company.

In early February, Phillips 66 reported (2/4/26) results for the fourth quarter of 2025. It achieved a strong refinery utilization rate of 99% and a record clean product yield of 88%.

Refining margins improved but chemical margins contracted sequentially. As a result, earnings-per-share dipped -2%, from $2.52 to $2.47, though they exceeded the analysts’ consensus by $0.32.

After two years of blowout refining margins amid the Ukrainian crisis, refining margins have normalized.

The company is in the positive phase of its cycle. While it has reduced its capital expenses in recent years, it has begun to reap the benefits from past investments.

Click here to download our most recent Sure Analysis report on PSX (preview of page 1 of 3 shown below):

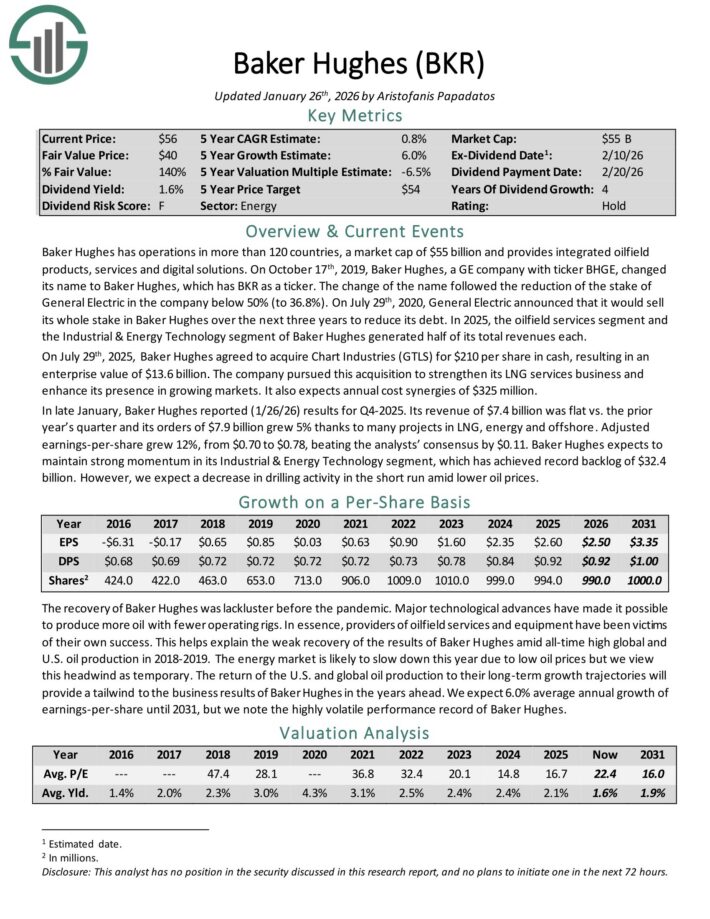

Top Energy Stock #9: Baker Hughes Co. (BKR)

- Annual Expected Returns: 1.4%

Baker Hughes has operations in more than 120 countries, and provides integrated oilfield products, services and digital solutions.

In late January, Baker Hughes reported (1/26/26) results for Q4-2025. Its revenue of $7.4 billion was flat vs. the prior year’s quarter and its orders of $7.9 billion grew 5% thanks to many projects in LNG, energy and offshore.

Adjusted earnings-per-share grew 12%, from $0.70 to $0.78, beating the analysts’ consensus by $0.11. Baker Hughes expects to maintain strong momentum in its Industrial & Energy Technology segment, which has achieved record backlog of $32.4 billion.

The return of the U.S. and global oil production to their long-term growth trajectories will provide a tailwind to the business results of Baker Hughes in the years ahead. We expect 6.0% average annual growth of earnings-per-share until 2031.

Click here to download our most recent Sure Analysis report on BKR (preview of page 1 of 3 shown below):

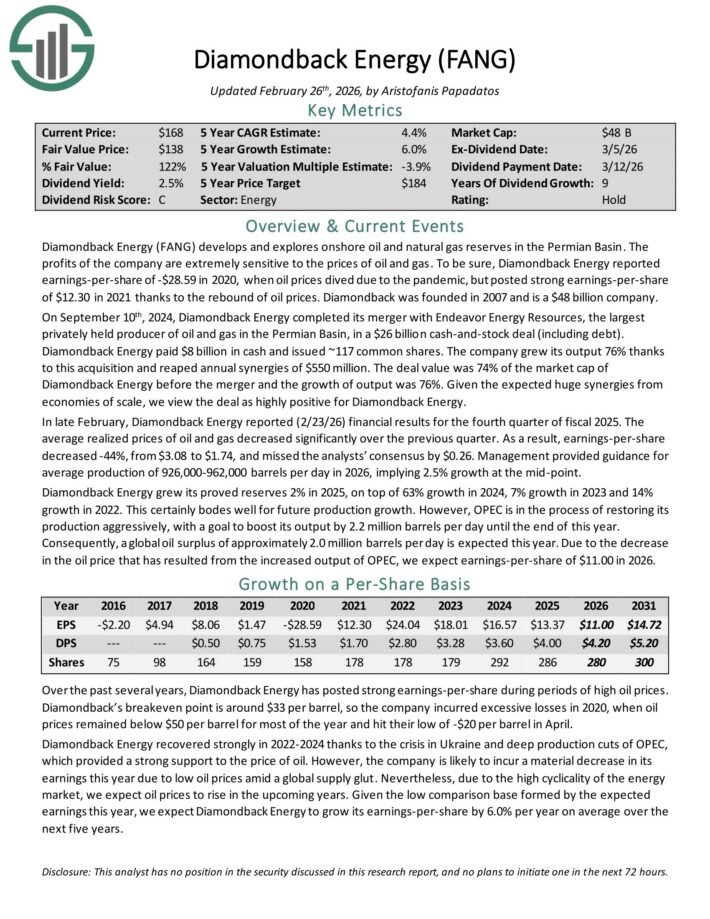

Top Energy Stock #8: Diamondback Energy (FANG)

- Annual Expected Returns: 2.7%

Diamondback Energy (FANG) develops and explores onshore oil and natural gas reserves in the Permian Basin. The profits of the company are extremely sensitive to the prices of oil and gas.

In late February, Diamondback Energy reported (2/23/26) financial results for the fourth quarter of fiscal 2025. The average realized prices of oil and gas decreased significantly over the previous quarter.

As a result, earnings-per-share decreased -44%, from $3.08 to $1.74, and missed the analysts’ consensus by $0.26.

Management provided guidance for average production of 926,000-962,000 barrels per day in 2026, implying 2.5% growth at the mid-point.

Diamondback Energy grew its proved reserves 2% in 2025, on top of 63% growth in 2024, 7% growth in 2023 and 14% growth in 2022. This certainly bodes well for future production growth.

Over the past several years, Diamondback Energy has posted strong earnings-per-share during periods of high oil prices. Diamondback’s breakeven point is around $33 per barrel.

The low dividend payout ratio of 38% is likely to provide a wide margin of safety for the dividend for the foreseeable future.

Click here to download our most recent Sure Analysis report on FANG (preview of page 1 of 3 shown below):

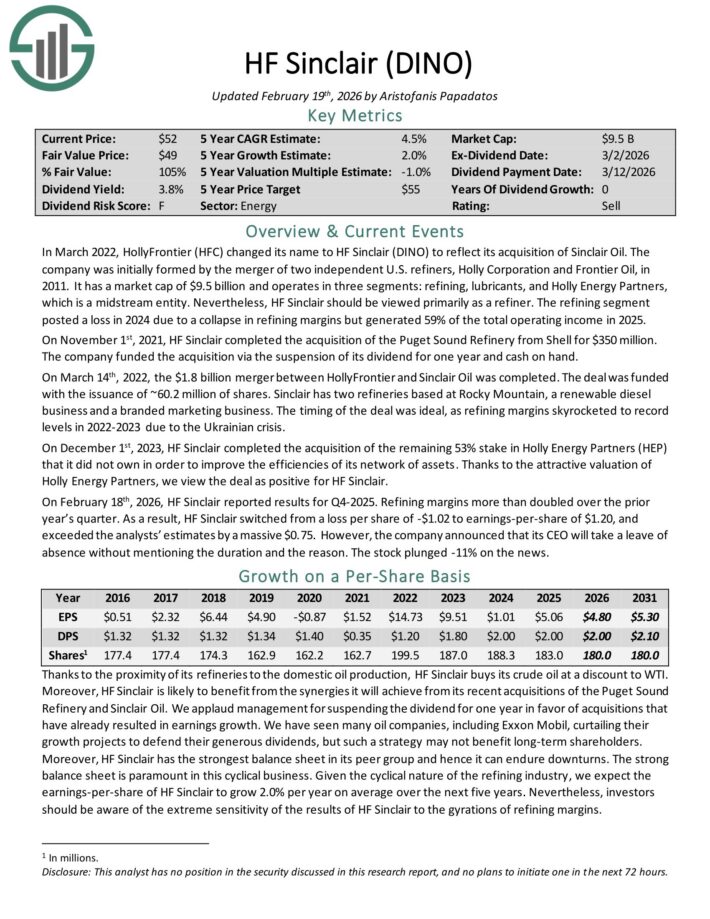

Top Energy Stock #7: H.F. Sinclair (DINO)

- Annual Expected Returns: 2.9%

HF Sinclair (DINO) operates in three segments: refining, lubricants, and Holly Energy Partners, which is a midstream entity.

The refining segment posted a loss in 2024 due to a collapse in refining margins but generated 59% of the total operating income in 2025.

On February 18th, 2026, HF Sinclair reported results for Q4-2025. Refining margins more than doubled over the prior year’s quarter. As a result, HF Sinclair switched from a loss per share of -$1.02 to earnings-per-share of $1.20, and exceeded the analysts’ estimates by a massive $0.75.

Thanks to the proximity of its refineries to the domestic oil production, HF Sinclair buys its crude oil at a discount to WTI.

Moreover, HF Sinclair is likely to benefit from the synergies it will achieve from its recent acquisitions of the Puget Sound Refinery and Sinclair Oil.

HF Sinclair has the strongest balance sheet in its peer group and hence it can endure downturns. The strong balance sheet is paramount in this cyclical business.

Given the cyclical nature of the refining industry, we expect the earnings-per-share of HF Sinclair to grow 2.0% per year on average over the next five years.

Click here to download our most recent Sure Analysis report on DINO (preview of page 1 of 3 shown below):

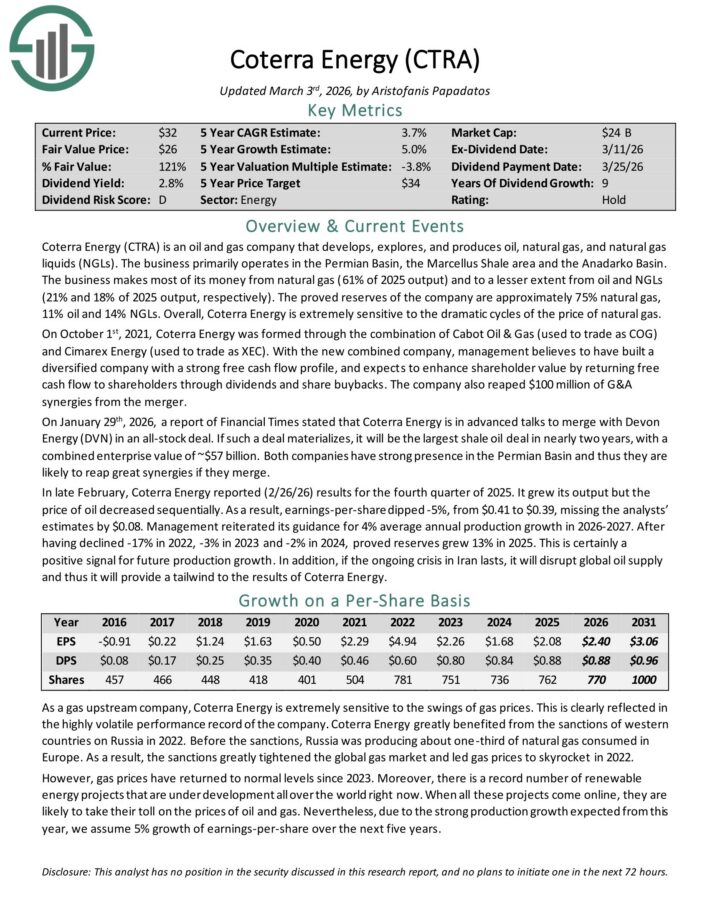

Top Energy Stock #6: Coterra Energy (CTRA)

- Annual Expected Returns: 3.3%

Coterra Energy (CTRA) is an oil and gas company that develops, explores, and produces oil, natural gas, and natural gas liquids (NGLs).

The business primarily operates in the Permian Basin, the Marcellus Shale area and the Anadarko Basin. The business makes most of its money from natural gas (61% of 2025 output) and to a lesser extent from oil and NGLs (21% and 18% of 2025 output, respectively).

The proved reserves of the company are approximately 75% natural gas, 11% oil and 14% NGLs.

On October 1st, 2021, Coterra Energy was formed through the combination of Cabot Oil & Gas (used to trade as COG) and Cimarex Energy (used to trade as XEC).

With the new combined company, management believes to have built a diversified company with a strong free cash flow profile, and expects to enhance shareholder value by returning free cash flow to shareholders through dividends and share buybacks. The company also reaped $100 million of G&A synergies from the merger.

On January 29th, 2026, a report of Financial Times stated that Coterra Energy is in advanced talks to merge with Devon Energy (DVN) in an all-stock deal.

If such a deal materializes, it will be the largest shale oil deal in nearly two years, with a combined enterprise value of ~$57 billion. Both companies have strong presence in the Permian Basin and thus they are likely to reap great synergies if they merge.

In late February, Coterra Energy reported (2/26/26) results for the fourth quarter of 2025. It grew its output but the price of oil decreased sequentially.

As a result, earnings-per-share dipped -5%, from $0.41 to $0.39, missing the analysts’ estimates by $0.08. Management reiterated its guidance for 4% average annual production growth in 2026-2027.

After having declined -17% in 2022, -3% in 2023 and -2% in 2024, proved reserves grew 13% in 2025. This is certainly a positive signal for future production growth.

Click here to download our most recent Sure Analysis report on CTRA (preview of page 1 of 3 shown below):

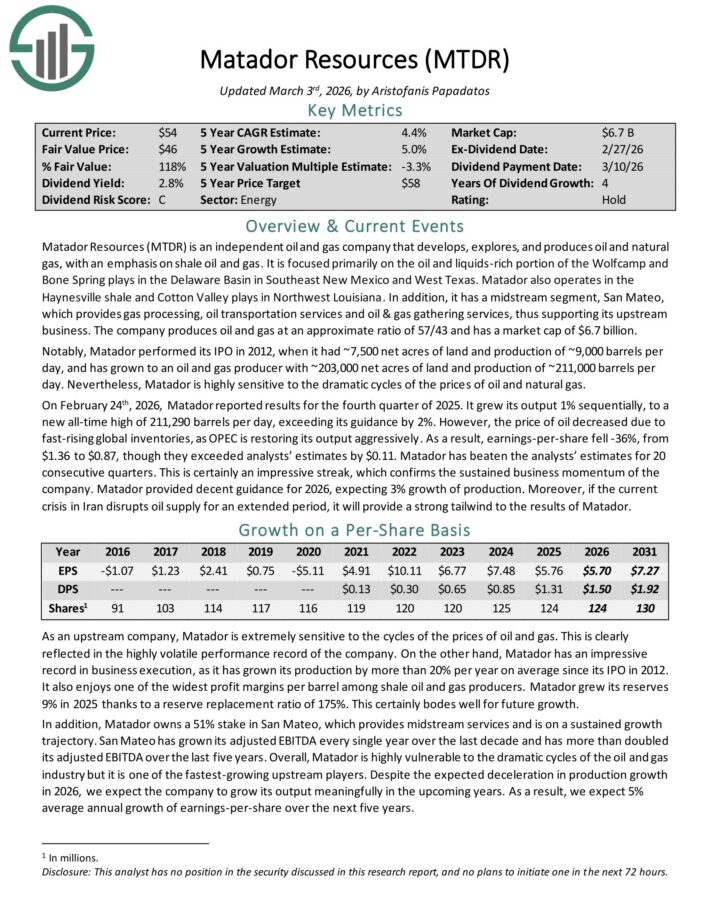

Top Energy Stock #5: Matador Resources (MTDR)

- Annual Expected Returns: 3.4%

Matador Resources (MTDR) is an independent oil and gas company that develops, explores, and produces oil and natural gas, with an emphasis on shale oil and gas.

It is focused primarily on the oil and liquids-rich portion of the Wolfcamp and Bone Spring plays in the Delaware Basin in Southeast New Mexico and West Texas.

Matador also operates in the Haynesville shale and Cotton Valley plays in Northwest Louisiana. The company produces oil and gas at an approximate ratio of 57/43.

Matador is an oil and gas producer with ~203,000 net acres of land and production of ~211,000 barrels per day. It is highly sensitive to the dramatic cycles of the prices of oil and natural gas.

On February 24th, 2026, Matador reported results for the fourth quarter of 2025. It grew its output 1% sequentially, to a new all-time high of 211,290 barrels per day, exceeding its guidance by 2%.

However, the price of oil decreased due to fast-rising global inventories, as OPEC is restoring its output aggressively. As a result, earnings-per-share fell -36%, from $1.36 to $0.87, though they exceeded analysts’ estimates by $0.11.

Matador has beaten the analysts’ estimates for 20 consecutive quarters. This is certainly an impressive streak, which confirms the sustained business momentum of the company.

Matador provided decent guidance for 2026, expecting 3% growth of production.

Click here to download our most recent Sure Analysis report on MTDR (preview of page 1 of 3 shown below):

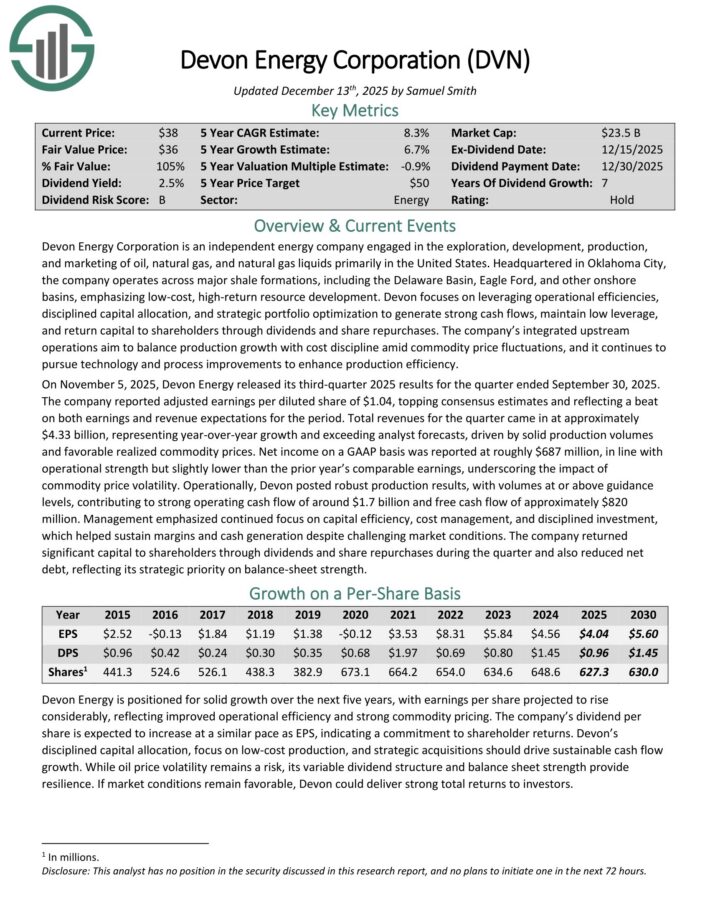

Top Energy Stock #4: Devon Energy (DVN)

- Annual Expected Returns: 3.6%

Devon Energy Corporation is an independent energy company engaged in the exploration, development, production, and marketing of oil, natural gas, and natural gas liquids primarily in the United States.

The company operates across major shale formations, including the Delaware Basin, Eagle Ford, and other onshore basins, emphasizing low-cost, high-return resource development.

On November 5, 2025, Devon Energy released its third-quarter 2025 results for the quarter ended September 30, 2025. The company reported adjusted earnings per diluted share of $1.04, topping consensus estimates and reflecting a beat on both earnings and revenue expectations for the period.

Total revenue for the quarter came in at approximately $4.33 billion, representing year-over-year growth and exceeding analyst forecasts, driven by solid production volumes and favorable realized commodity prices.

Net income on a GAAP basis was reported at roughly $687 million, in line with operational strength but slightly lower than the prior year’s comparable earnings, underscoring the impact of commodity price volatility.

Operationally, Devon posted robust production results, with volumes at or above guidance levels, contributing to strong operating cash flow of around $1.7 billion and free cash flow of approximately $820 million.

Management emphasized continued focus on capital efficiency, cost management, and disciplined investment, which helped sustain margins and cash generation despite challenging market conditions.

The company returned significant capital to shareholders through dividends and share repurchases during the quarter and also reduced net debt.

Click here to download our most recent Sure Analysis report on DVN (preview of page 1 of 3 shown below):

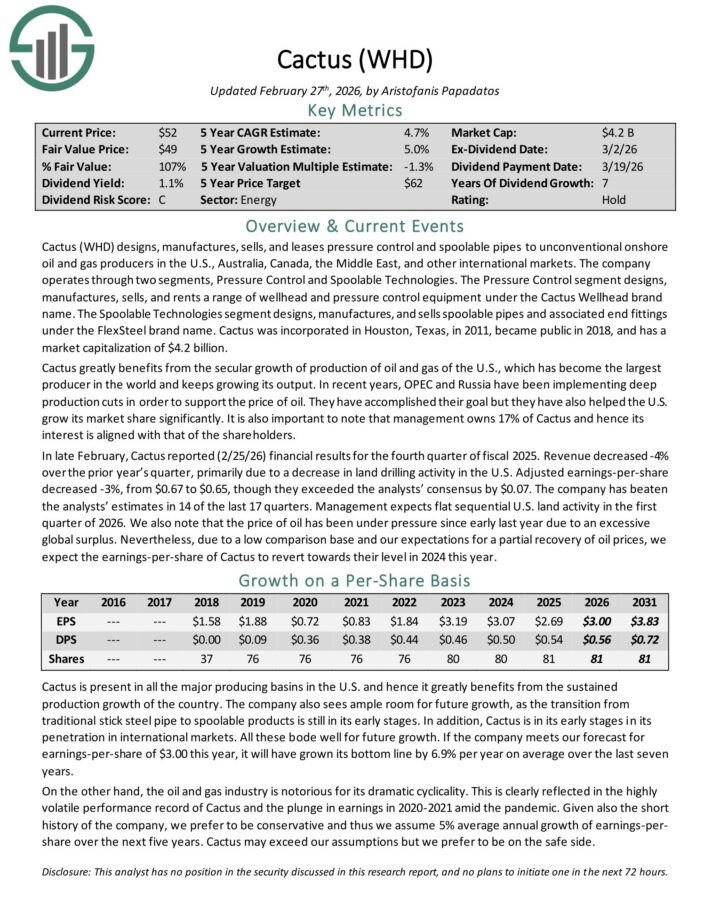

Top Energy Stock #3: Cactus, Inc. (WHD)

- Annual Expected Returns: 7.2%

Cactus (WHD) designs, manufactures, sells, and leases pressure control and spoolable pipes to unconventional onshore oil and gas producers in the U.S., Australia, Canada, the Middle East, and other international markets.

The company operates through two segments, Pressure Control and Spoolable Technologies. The Pressure Control segment designs, manufactures, sells, and rents a range of wellhead and pressure control equipment under the Cactus Wellhead brand name.

The Spoolable Technologies segment designs, manufactures, and sells spoolable pipes and associated end fittings under the FlexSteel brand name.

Cactus greatly benefits from the secular growth of production of oil and gas of the U.S., which has become the largest producer in the world and keeps growing its output.

In late February, Cactus reported (2/25/26) financial results for the fourth quarter of fiscal 2025. Revenue decreased -4% over the prior year’s quarter, primarily due to a decrease in land drilling activity in the U.S.

Adjusted earnings-per-share decreased -3%, from $0.67 to $0.65, though they exceeded the analysts’ consensus by $0.07. The company has beaten the analysts’ estimates in 14 of the last 17 quarters.

Management expects flat sequential U.S. land activity in the first quarter of 2026. We also note that the price of oil has been under pressure since early last year due to an excessive global surplus.

Nevertheless, due to a low comparison base and our expectations for a partial recovery of oil prices, we expect the earnings-per-share of Cactus to revert towards their level in 2024 this year.

Click here to download our most recent Sure Analysis report on WHD (preview of page 1 of 3 shown below):

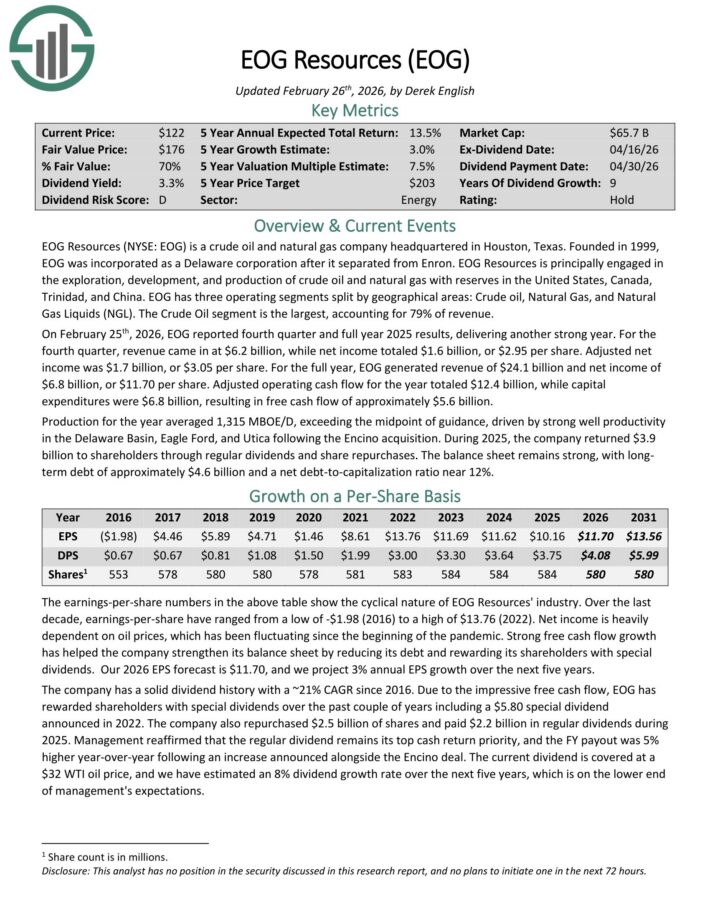

Top Energy Stock #2: EOG Resources (EOG)

- Annual Expected Returns: 11.6%

EOG Resources (NYSE: EOG) is a crude oil and natural gas company headquartered in Houston, Texas. It is principally engaged in the exploration, development, and production of crude oil and natural gas with reserves in the United States, Canada, Trinidad, and China.

EOG has three operating segments split by geographical areas: Crude oil, Natural Gas, and Natural Gas Liquids (NGL). The Crude Oil segment is the largest, accounting for 79% of revenue.

On February 25th, 2026, EOG reported fourth quarter and full year 2025 results, delivering another strong year. For the fourth quarter, revenue came in at $6.2 billion, while net income totaled $1.6 billion, or $2.95 per share. Adjusted net income was $1.7 billion, or $3.05 per share.

For the full year, EOG generated revenue of $24.1 billion and net income of $6.8 billion, or $11.70 per share. Adjusted operating cash flow for the year totaled $12.4 billion, while capital expenditures were $6.8 billion, resulting in free cash flow of approximately $5.6 billion.

Production for the year averaged 1,315 MBOE/D, exceeding the midpoint of guidance, driven by strong well productivity in the Delaware Basin, Eagle Ford, and Utica following the Encino acquisition.

During 2025, the company returned $3.9 billion to shareholders through regular dividends and share repurchases.

The balance sheet remains strong, with longterm debt of approximately $4.6 billion and a net debt-to-capitalization ratio near 12%.

Click here to download our most recent Sure Analysis report on EOG (preview of page 1 of 3 shown below):

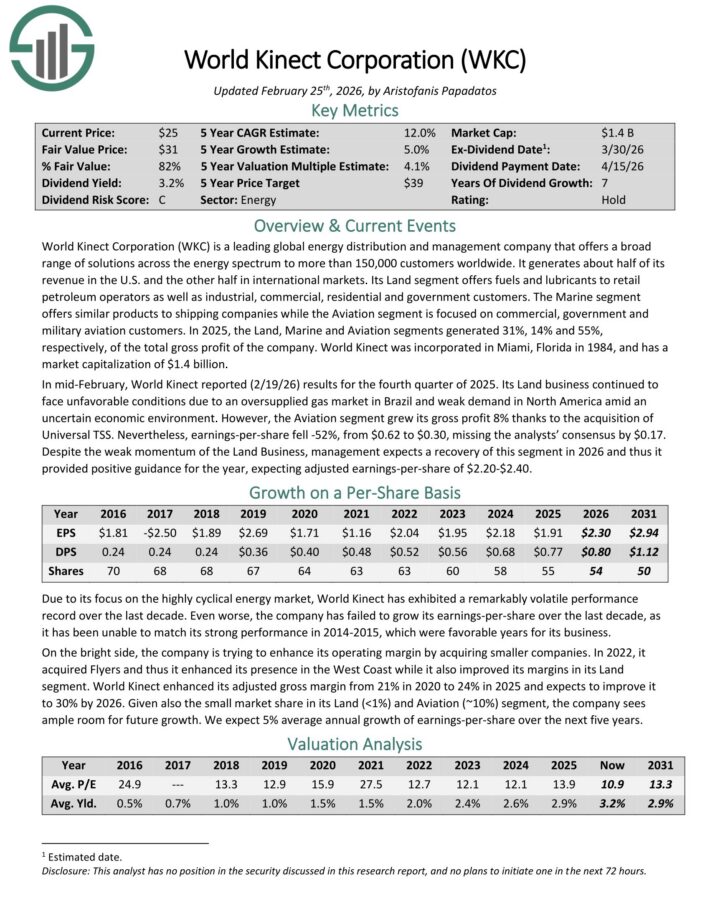

Top Energy Stock #1: World Kinect Corporation (WKC)

- Annual Expected Returns: 14.3%

World Kinect Corporation (WKC) is a leading global energy distribution and management company that offers a broad range of solutions across the energy spectrum to more than 150,000 customers worldwide.

It generates about half of its revenue in the U.S. and the other half in international markets. Its Land segment offers fuels and lubricants to retail petroleum operators as well as industrial, commercial, residential and government customers.

The Marine segment offers similar products to shipping companies while the Aviation segment is focused on commercial, government and military aviation customers.

In 2025, the Land, Marine and Aviation segments generated 31%, 14% and 55%, respectively, of the total gross profit of the company.

In mid-February, World Kinect reported (2/19/26) results for the fourth quarter of 2025. Its Land business continued to face unfavorable conditions due to an oversupplied gas market in Brazil and weak demand in North America amid an uncertain economic environment.

However, the Aviation segment grew its gross profit 8% thanks to the acquisition of Universal TSS. Nevertheless, earnings-per-share fell -52%, from $0.62 to $0.30, missing the analysts’ consensus by $0.17.

Click here to download our most recent Sure Analysis report on WKC (preview of page 1 of 3 shown below):

Final Thoughts

The energy sector has many quality dividend stocks, a select few of which have maintained long histories of increasing their dividends.

With that said, it’s not the only place where great investments can be found.

For investors that already have a full dose of energy exposure but are still looking for high-quality investment opportunities, the following Sure Dividend databases will be useful:

- The Dividend Aristocrats List: dividend stocks in the S&P 500 with 25+ years of consecutive dividend increases.

- The Dividend Kings List: containing the ‘best-of-the-best’ when it comes to dividend growth, the Dividend Kings List is composed of dividend stocks with 50+ years of consecutive dividend increases.

- The Blue Chip Stocks List: dividend stocks with 10+ years of dividend increases that represent quality long-term investments.