Spreadsheet data updated daily

Updated on May 29th, 2026 by Bob Ciura

Individual products, businesses, and even entire industries (newspapers, typewriters, horse and buggy) go out of style and become obsolete.

Perhaps more than any other industry, agriculture is here to stay. Agriculture started around 14,000 years ago. It’s a safe bet we will be practicing agriculture far into the future.

And, the growth of the global population is tied to increasing agricultural efficiency. The agricultural revolution allowed greater population growth (and led to the industrial revolution).

As the global population grows, so does the need for improved agricultural production. This creates a long-term demand driver for agriculture stocks.

You can download the complete list of all 40+ agriculture stocks (along with important financial metrics such as price-to-earnings ratios, dividend yields, and dividend payout ratios) by clicking on the link below:

The agriculture stocks list was derived from two major exchange-traded funds. These are the AgTech & Food Innovation ETF (KROP) and the iShares Global Agriculture Index ETF (COW).

Investing in farm and agriculture stocks means investing in an industry that:

- Has stable long-term demand

- Has withstood the test of time, and is extremely likely to be around far into the future

- Benefits from advancing technology

This article analyzes 7 of the best agriculture stocks in detail. You can quickly navigate the article using the table of contents below.

Table of Contents

- Agriculture Stock #7: Corteva, Inc. (CTVA)

- Agriculture Stock #6: Mosaic Company (MOS)

- Agriculture Stock #5: Federal Agriculture Mortgage Association (AGM)

- Agriculture Stock #4: Ingredion Inc. (INGR)

- Agriculture Stock #3: Alamo Group (ALG)

- Agriculture Stock #2: Tractor Supply Company (TSCO)

- Agriculture Stock #1: The Andersons Inc. (ANDE)

- Final Thoughts

We have ranked our 7 favorite agriculture stocks below. The stocks are ranked according to expected returns over the next five years, in order of lowest to highest.

Even better, all 7 agriculture stocks pay dividends to shareholders, making them attractive for income investors. Interested investors should view this as a starting off point to more research.

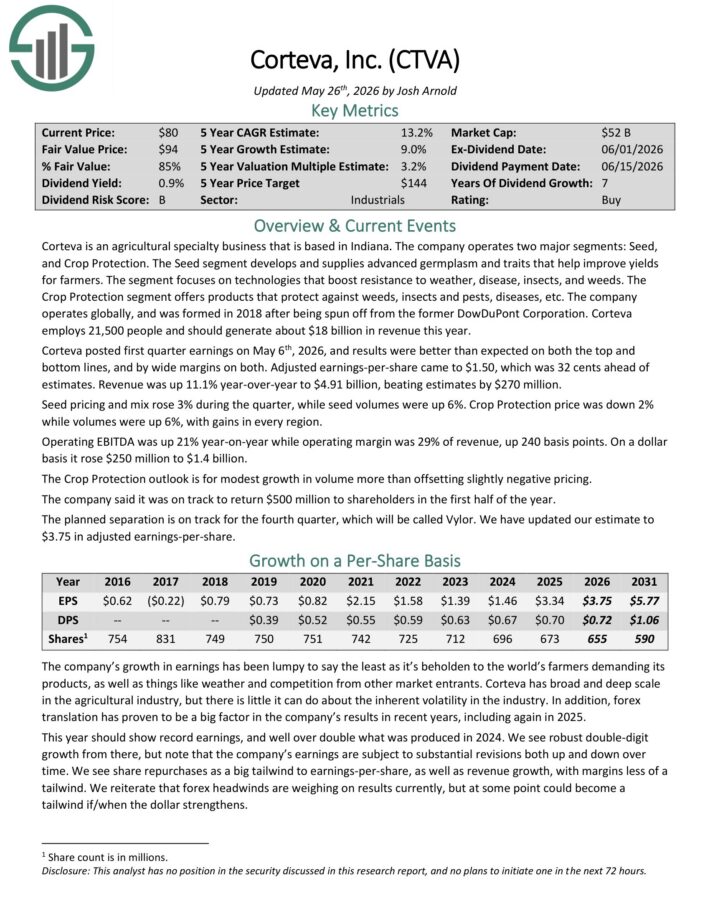

Agriculture Stock #7: Corteva, Inc. (CTVA)

- 5-year expected annual returns: 12.9%

Corteva is an agricultural specialty business that operates two major segments: Seed and Crop Protection.

The Seed segment develops and supplies advanced germplasm and traits that help improve yields for farmers. The segment focuses on technologies that boost resistance to weather, disease, insects, and weeds.

The Crop Protection segment offers products that protect against weeds, insects and pests, diseases, and more. The company operates globally, and was formed in 2018 after being spun off from the former DowDuPont Corporation.

Corteva posted first quarter earnings on May 6th, 2026, and results were better than expected on both the top and bottom lines, and by wide margins on both. Adjusted earnings-per-share came to $1.50, which was 32 cents ahead of estimates.

Revenue was up 11.1% year-over-year to $4.91 billion, beating estimates by $270 million. Seed pricing and mix rose 3% during the quarter, while seed volumes were up 6%. Crop Protection price was down 2% while volumes were up 6%, with gains in every region.

Operating EBITDA was up 21% year-on-year while operating margin was 29% of revenue, up 240 basis points. On a dollar basis it rose $250 million to $1.4 billion.

Click here to download our most recent Sure Analysis report on CTVA (preview of page 1 of 3 shown below):

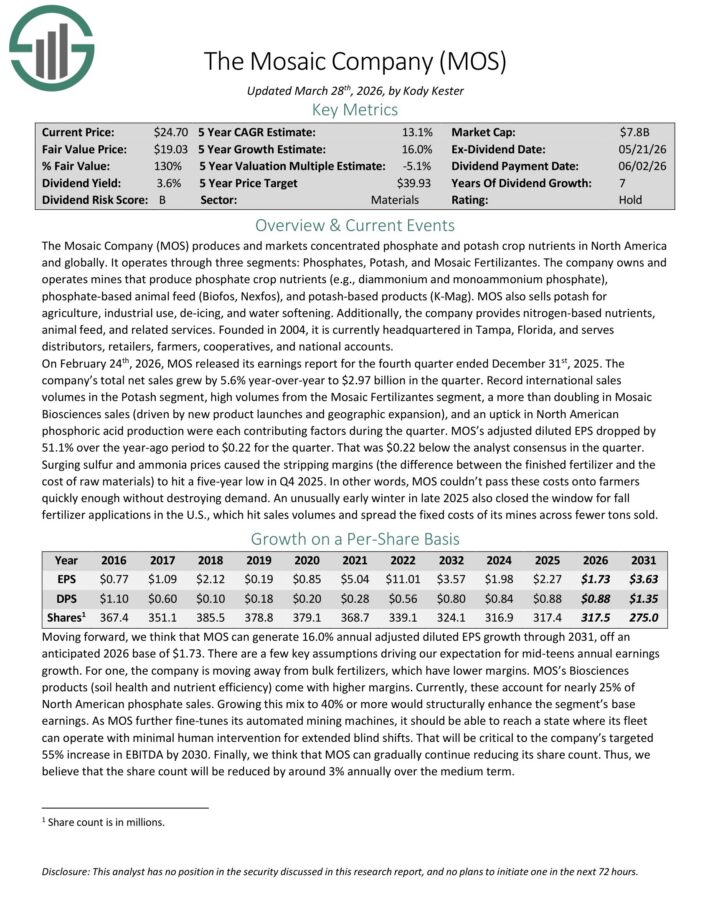

Agriculture Stock #6: Mosaic Company (MOS)

- 5-year expected annual returns: 13.7%

The Mosaic Company (MOS) produces and markets concentrated phosphate and potash crop nutrients in North America and globally.

It operates through three segments: Phosphates, Potash, and Mosaic Fertilizantes. The company owns and operates mines that produce phosphate crop nutrients (e.g., diammonium and monoammonium phosphate), phosphate-based animal feed (Biofos, Nexfos), and potash-based products (K-Mag).

MOS also sells potash for agriculture, industrial use, de-icing, and water softening.

Additionally, the company provides nitrogen-based nutrients, animal feed, and related services. It serves distributors, retailers, farmers, cooperatives, and national accounts.

On February 24th, 2026, MOS released its earnings report for the fourth quarter ended December 31st, 2025. The company’s total net sales grew by 5.6% year-over-year to $2.97 billion in the quarter.

Record international sales volumes in the Potash segment, high volumes from the Mosaic Fertilizantes segment, a more than doubling in Mosaic Biosciences sales (driven by new product launches and geographic expansion), and an uptick in North American phosphoric acid production were each contributing factors during the quarter.

MOS’s adjusted diluted EPS dropped by 51.1% over the year-ago period to $0.22 for the quarter. That was $0.22 below the analyst consensus in the quarter.

Surging sulfur and ammonia prices caused the stripping margins (the difference between the finished fertilizer and the cost of raw materials) to hit a five-year low in Q4 2025.

Click here to download our most recent Sure Analysis report on MOS (preview of page 1 of 3 shown below):

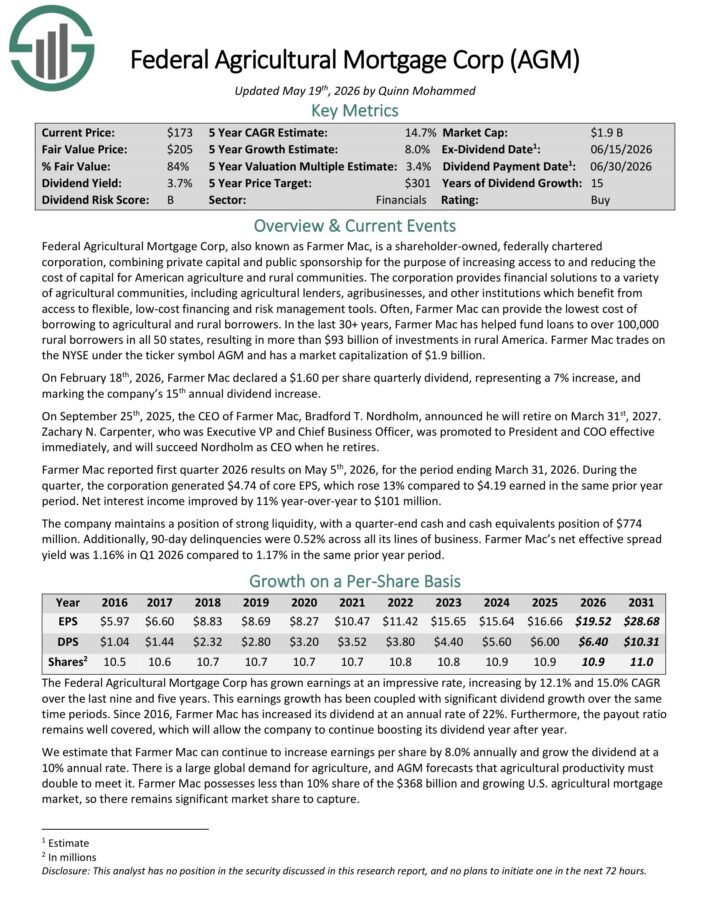

Agriculture Stock #5: Federal Agriculture Mortgage Association (AGM)

- 5-year expected annual returns: 13.9%

Federal Agricultural Mortgage Corp, also known as Farmer Mac, is a shareholder-owned, federally chartered corporation, combining private capital and public sponsorship for the purpose of increasing access to and reducing the cost of capital for American agriculture and rural communities.

The corporation provides financial solutions to a variety of agricultural communities, including agricultural lenders, agribusinesses, and other institutions which benefit from access to flexible, low-cost financing and risk management tools.

Farmer Mac reported first quarter 2026 results on May 5th, 2026, for the period ending March 31, 2026. During the quarter, the corporation generated $4.74 of core EPS, which rose 13% compared to $4.19 earned in the same prior year period.

Net interest income improved by 11% year-over-year to $101 million. The company maintains a position of strong liquidity, with a quarter-end cash and cash equivalents position of $774 million.

Additionally, 90-day delinquencies were 0.52% across all its lines of business. Farmer Mac’s net effective spread yield was 1.16% in Q1 2026 compared to 1.17% in the same prior year period..

Click here to download our most recent Sure Analysis report on AGM (preview of page 1 of 3 shown below):

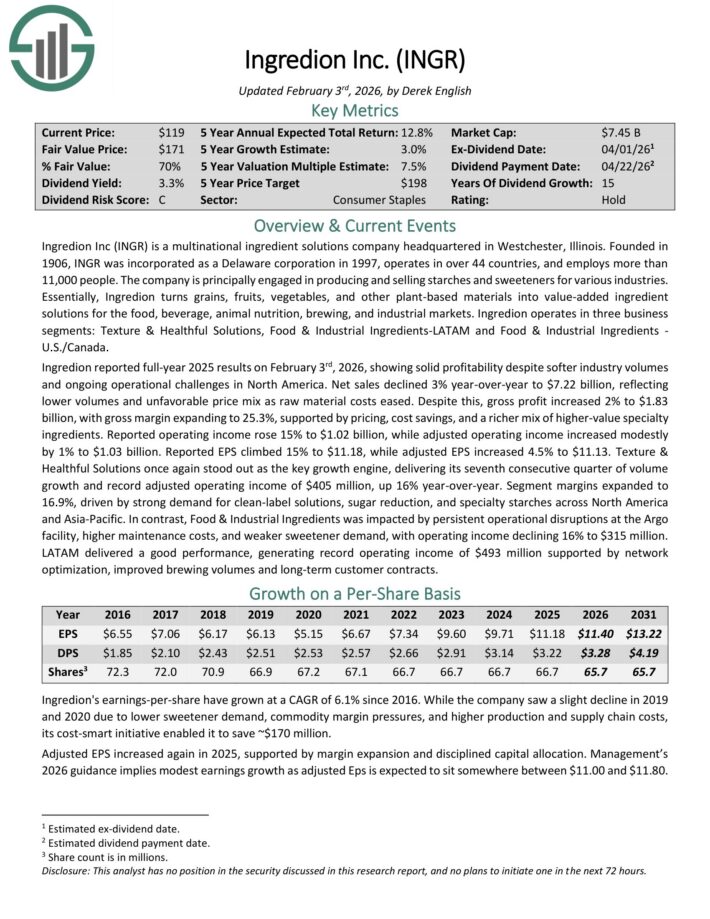

Agriculture Stock #4: Ingredion Inc. (INGR)

- 5-year expected annual returns: 16.1%

Ingredion Inc. is a multinational ingredient solutions company headquartered in Westchester, Illinois. The company is principally engaged in producing and selling starches and sweeteners for various industries.

Ingredion turns grains, fruits, vegetables, and other plant-based materials into value-added ingredient solutions for the food, beverage, animal nutrition, brewing, and industrial markets.

Ingredion operates in three business segments: Texture & Healthful Solutions, Food & Industrial Ingredients-LATAM and Food & Industrial Ingredients–U.S./Canada.

Ingredion reported full-year 2025 results on February 3rd, 2026, showing solid profitability despite softer industry volumes and ongoing operational challenges in North America.

Net sales declined 3% year-over-year to $7.22 billion, reflecting lower volumes and unfavorable price mix as raw material costs eased.

Despite this, gross profit increased 2% to $1.83 billion, with gross margin expanding to 25.3%, supported by pricing, cost savings, and a richer mix of higher-value specialty ingredients.

Reported operating income rose 15% to $1.02 billion, while adjusted operating income increased modestly by 1% to $1.03 billion.

Reported EPS climbed 15% to $11.18, while adjusted EPS increased 4.5% to $11.13. Texture & Healthful Solutions once again stood out as the key growth engine, delivering its seventh consecutive quarter of volume growth and record adjusted operating income of $405 million, up 16% year-over-year.

Click here to download our most recent Sure Analysis report on INGR (preview of page 1 of 3 shown below):

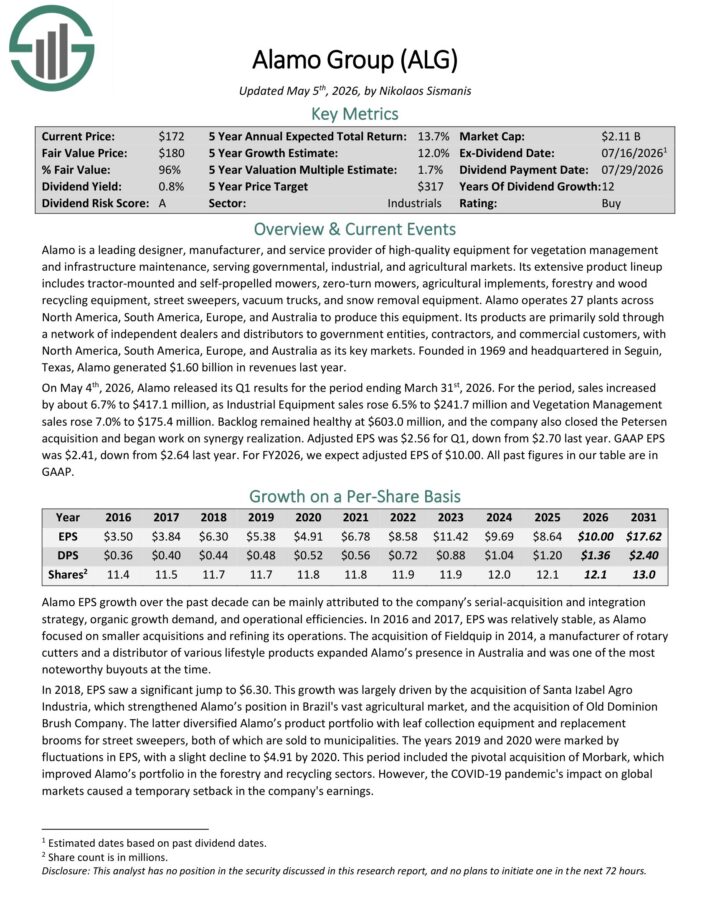

Agriculture Stock #3: Alamo Group (ALG)

- 5-year expected annual returns: 16.5%

Alamo is a leading designer, manufacturer, and service provider of high-quality equipment for vegetation management and infrastructure maintenance, serving governmental, industrial, and agricultural markets.

Its extensive product lineup includes tractor-mounted and self-propelled mowers, zero-turn mowers, agricultural implements, forestry and wood recycling equipment, street sweepers, vacuum trucks, and snow removal equipment. Alamo operates 27 plants across North America, South America, Europe, and Australia to produce this equipment.

Its products are primarily sold through a network of independent dealers and distributors to government entities, contractors, and commercial customers, with North America, South America, Europe, and Australia as its key markets.

Founded in 1969 and headquartered in Seguin, Texas, Alamo generated $1.60 billion in revenues last year.

On May 4th, 2026, Alamo released its Q1 results for the period ending March 31st, 2026. For the period, sales increased by about 6.7% to $417.1 million, as Industrial Equipment sales rose 6.5% to $241.7 million and Vegetation Management sales rose 7.0% to $175.4 million.

Backlog remained healthy at $603.0 million, and the company also closed the Petersen acquisition and began work on synergy realization.

Adjusted EPS was $2.56 for Q1, down from $2.70 last year. GAAP EPS was $2.41, down from $2.64 last year. For FY2026, we expect adjusted EPS of $10.00.

Click here to download our most recent Sure Analysis report on ALG (preview of page 1 of 3 shown below):

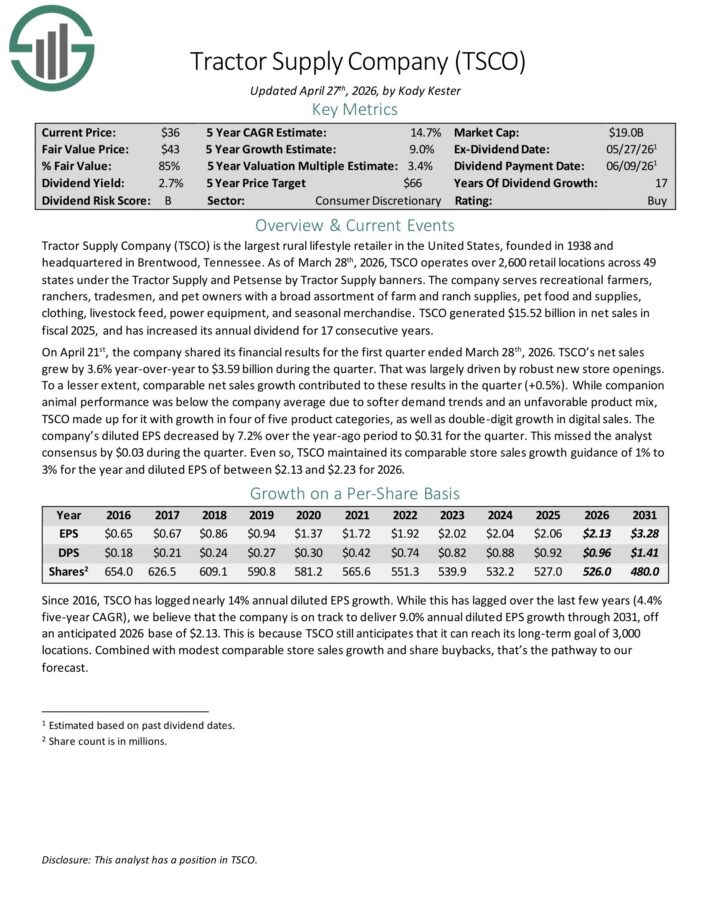

Agriculture Stock #2: Tractor Supply (TSCO)

- 5-year expected annual returns: 18.1%

Tractor Supply Company is the largest rural lifestyle retailer in the United States, founded in 1938 and headquartered in Brentwood, Tennessee.

As of March 28th, 2026, TSCO operates over 2,600 retail locations across 49 states under the Tractor Supply and Petsense by Tractor Supply banners.

The company serves recreational farmers, ranchers, tradesmen, and pet owners with a broad assortment of farm and ranch supplies, pet food and supplies, clothing, livestock feed, power equipment, and seasonal merchandise.

TSCO generated $15.52 billion in net sales in fiscal 2025, and has increased its annual dividend for 17 consecutive years.

On April 21st, the company shared its financial results for the first quarter ended March 28th, 2026. TSCO’s net sales grew by 3.6% year-over-year to $3.59 billion during the quarter. That was largely driven by robust new store openings.

To a lesser extent, comparable net sales growth contributed to these results in the quarter (+0.5%). While companion animal performance was below the company average due to softer demand trends and an unfavorable product mix, TSCO made up for it with growth in four of five product categories, as well as double-digit growth in digital sales.

The company’s diluted EPS decreased by 7.2% over the year-ago period to $0.31 for the quarter.

Click here to download our most recent Sure Analysis report on TSCO (preview of page 1 of 3 shown below):

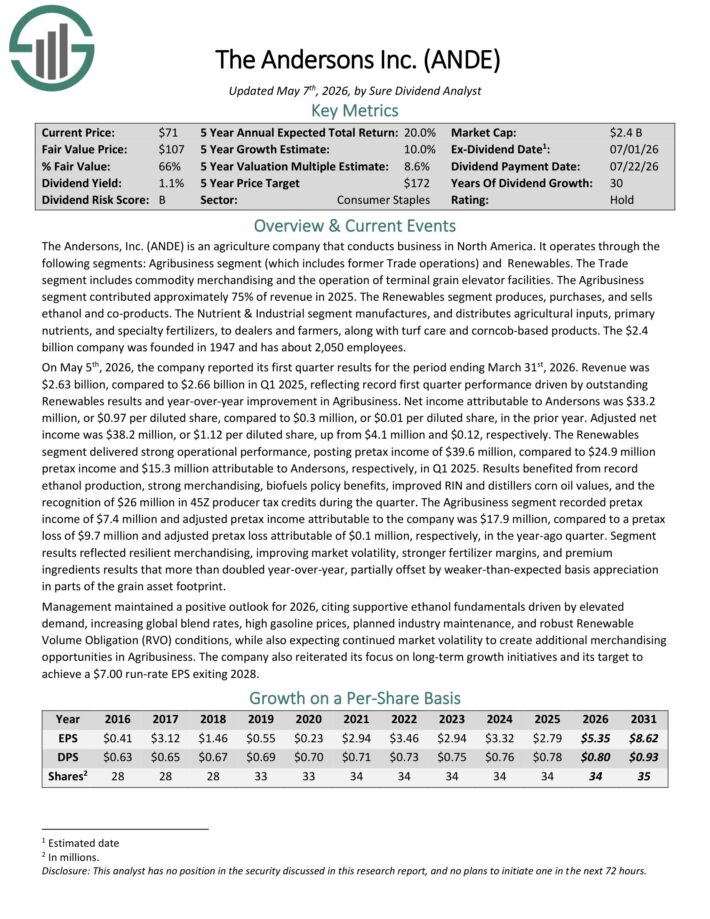

Agriculture Stock #1: The Andersons Inc. (ANDE)

- 5-year expected annual returns: 19.8%

The Andersons is an agriculture company that conducts business in North America. It operates through the following segments: Agribusiness segment (which includes former Trade operations) and Renewables.

The Trade segment includes commodity merchandising and the operation of terminal grain elevator facilities. The Agribusiness segment contributed approximately 75% of revenue in 2025.

The Renewables segment produces, purchases, and sells ethanol and co-products. The Nutrient & Industrial segment manufactures, and distributes agricultural inputs, primary nutrients, and specialty fertilizers, to dealers and farmers, along with turf care and corncob-based products.

On May 5th, 2026, the company reported its first quarter results for the period ending March 31st, 2026. Revenue was $2.63 billion, compared to $2.66 billion in Q1 2025, reflecting record first quarter performance driven by outstanding Renewables results and year-over-year improvement in Agribusiness.

Net income attributable to Andersons was $33.2 million, or $0.97 per diluted share, compared to $0.3 million, or $0.01 per diluted share, in the prior year.

Adjusted net income was $38.2 million, or $1.12 per diluted share, up from $4.1 million and $0.12, respectively. The Renewables segment delivered strong operational performance, posting pretax income of $39.6 million, compared to $24.9 million pretax income and $15.3 million attributable to Andersons, respectively, in Q1 2025.

Click here to download our most recent Sure Analysis report on ANDE (preview of page 1 of 3 shown below):

Final Thoughts

Agriculture stocks are a compelling place to look for long-term stock investments. That’s because the demand drivers of the industry make it extremely likely to be around far into the future.

We believe the 7 agriculture stocks examined in this article are the best within the industry.

At Sure Dividend, we often advocate for investing in companies with a high probability of increasing their dividends each and every year.

If that strategy appeals to you, it may be useful to browse through the following databases of dividend growth stocks:

- The Dividend Aristocrats List: S&P 500 stocks with 25+ years of dividend increases.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 58 stocks with 50+ years of consecutive dividend increases.

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.