Updated on July 24th, 2026 by Nikolaos Sismanis

With contributions from Ben Reynolds

The Dividend Champions are securities with 25+ years of consecutive dividend increases.

There are currently only 165 securities that meet this high bar.

The Dividend Champions are an excellent place to find high quality dividend growth stocks to buy and hold for the long run.

The free Dividend Champions spreadsheet below gives you the power to quickly sort all Dividend Champions by metrics that matter like:

- Dividend Risk Score

- Expected total return

- Buy/Hold/Sell rating

- Percent Fair Value

- And many, many more

Notes: Our Dividend Champions spreadsheet is updated daily. It is powered by data from the Sure Analysis Research Database. See here for a glossary of our metrics.

Note On Aristocrats Versus Champions: Dividend Aristocrats require 25+ years of rising dividends and to be in the S&P 500 and to meet certain size and liquidity requirements. All Aristocrats are Champions, but not all Champions are Aristocrats.

Keep reading to see our Top 10 Dividend Champions now analyzed in detail. Our Top 10 Rankings have the following criteria:

- 25+ Years of rising dividends (a Dividend Champion)

- US. Stocks only (no REITs/MLPs/BDCs, or international stocks)

- Dividend Risk Score of A or B (high level of dividend safety)

- Rank by expected total return (#1 has highest expected total return)

Table of Contents

You can instantly jump to any specific section of the article by clicking on the links below:

- Top Dividend Champion #10: Becton, Dickinson & Co. (BDX)

- Top Dividend Champion #9: Stryker Corporation (SYK)

- Top Dividend Champion #8: The Andersons, Inc. (ANDE)

- Top Dividend Champion #7: Stepan Company (SCL)

- Top Dividend Champion #6: The Marzetti Company (MZTI)

- Top Dividend Champion #5: Brown & Brown, Inc. (BRO)

- Top Dividend Champion #4: S&P Global Inc. (SPGI)

- Top Dividend Champion #3: Albemarle Corporation (ALB)

- Top Dividend Champion #2: Badger Meter, Inc. (BMI)

- Top Dividend Champion #1: FactSet Research Systems Inc. (FDS)

Top Dividend Champion #10: Becton, Dickinson & Co. (BDX)

- Expected total return: 16.7%

- Dividend Risk Score: A

Becton, Dickinson & Co., commonly known as BD, is a global medical technology company. Its continuing operations focus on medication delivery, medication management, connected care, and interventional products.

Many of these products are used daily in hospitals and clinics, giving BD a large recurring-revenue base and relatively defensive demand.

BD has increased its dividend for 54 consecutive years.

On May 7th, 2026, BD reported fiscal second-quarter results for the period ending March 31st, 2026. Revenue from continuing operations grew 5.2% to $4.7 billion, or 2.6% excluding currency movements. Adjusted earnings-per-share increased 3.9% to $2.90.

Interventional was the fastest-growing portfolio, with revenue rising 7.3% as reported and 5.3% excluding currency movements. Management raised its full-year adjusted earnings-per-share guidance to $12.52 to $12.72 while reaffirming its revenue growth outlook.

One major recent development was the February separation of BD’s former Biosciences and Diagnostic Solutions businesses and their combination with Waters Corporation. The transaction leaves BD as a more focused medical technology company.

During the quarter, BD also executed a $2.0 billion accelerated share repurchase and retired $2.1 billion of debt.

Its essential products, modest payout ratio, and long dividend record support its A Dividend Risk Score.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on BDX.

Top Dividend Champion #9: Stryker Corporation (SYK)

- Expected total return: 17.2%

- Dividend Risk Score: A

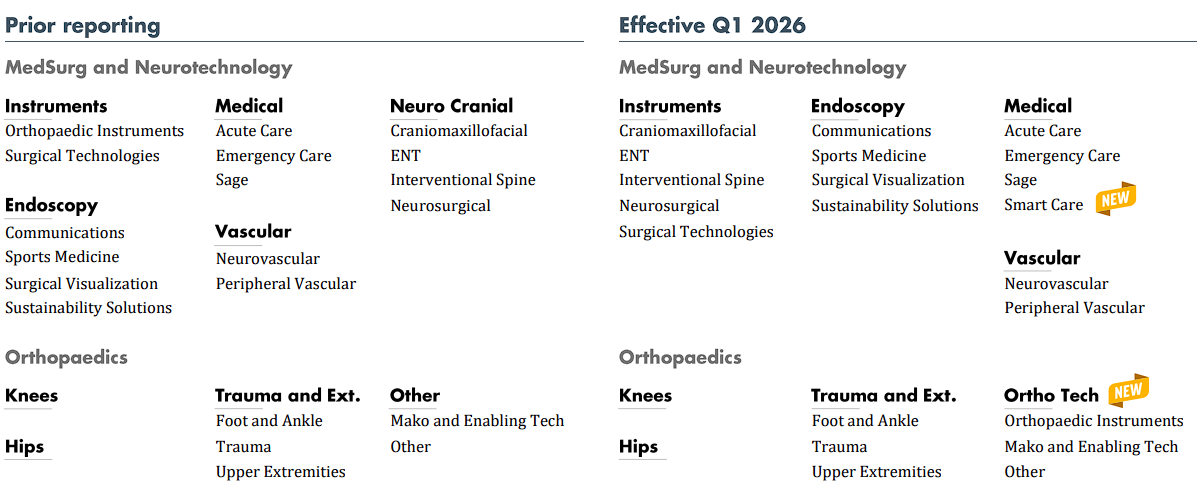

Stryker is a leading medical technology company with products across MedSurg, Neurotechnology, and Orthopaedics.

Its portfolio includes surgical equipment, endoscopy systems, joint replacements, trauma products, and robotic-assisted surgery technology.

The business benefits from rising procedure volumes, an aging population, and recurring demand for implants, instruments, and services.

Stryker has raised its dividend for 32 consecutive years.

On April 30th, 2026, Stryker reported first-quarter revenue of $6.0 billion, up 2.6% year-over-year. Organic sales increased 2.4%, including 4.1% growth in Orthopaedics. Adjusted earnings-per-share declined 8.5% to $2.60, while the adjusted operating margin contracted 180 basis points to 21.1%.

The company’s response to a cyber incident weighed on sales and expenses, making the quarter weaker than Stryker’s underlying procedure-demand trends would normally suggest.

Still, Stryker maintained its full-year outlook for organic sales growth of 8.0% to 9.5% and adjusted earnings per share of $14.90 to $15.10.

The company also reorganized its orthopaedic instruments, Mako, and enabling technologies businesses into a new Ortho Tech unit. Bringing these operations together should improve coordination across its robotics and implant platforms.

Stryker’s broad installed base and steady procedural demand provide a durable foundation for future growth.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on SYK.

Top Dividend Champion #8: The Andersons, Inc. (ANDE)

- Expected total return: 17.9%

- Dividend Risk Score: B

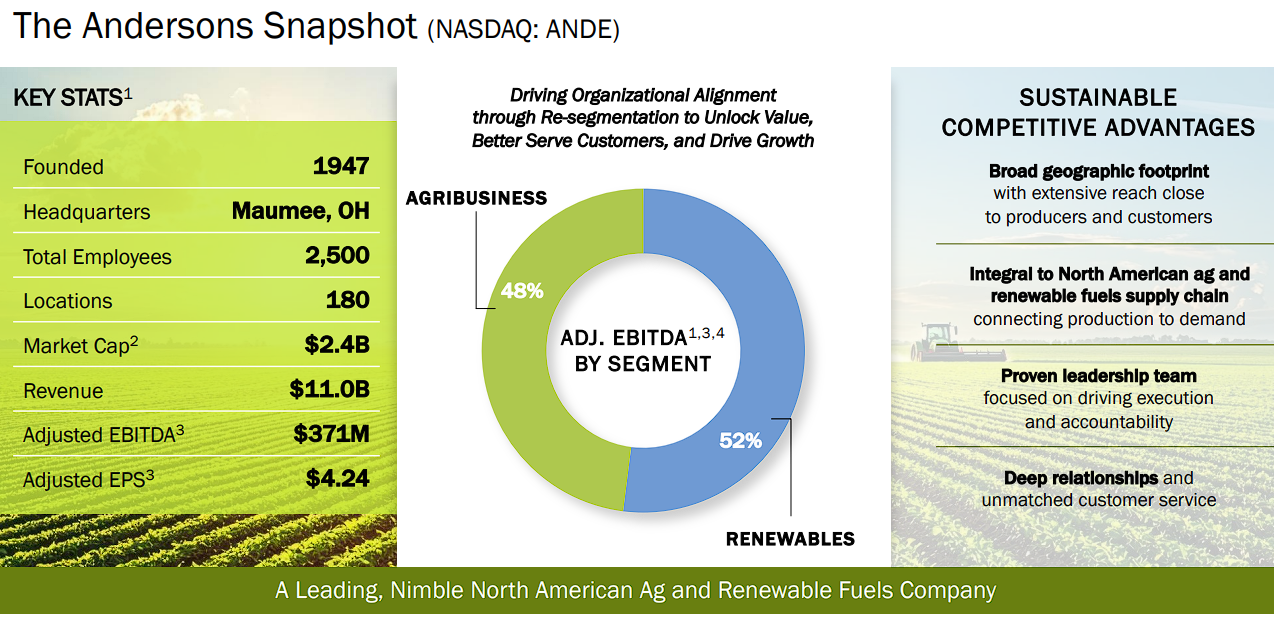

The Andersons is a diversified agribusiness company operating through its Agribusiness and Renewables segments.

Its activities include grain merchandising, specialty ingredients, fertilizer, ethanol production, and renewable feedstocks. Results can fluctuate with grain basis levels, fertilizer margins, ethanol spreads, and government biofuel policy.

The company has increased its dividend for 30 consecutive years.

On May 5th, 2026, The Andersons reported record first-quarter net income of $33.2 million, or $0.97 per share, compared with $0.3 million, or $0.01 per share, in the prior-year period.

Adjusted earnings per share rose to $1.12 from $0.12, while adjusted EBITDA increased to $91.5 million from $57.3 million.

Agribusiness benefited from stronger merchandising and fertilizer results, while Renewables generated $54 million of EBITDA.

The largest recent swing factor is the federal Section 45Z clean-fuel production credit. Renewables recorded a $26 million benefit during the quarter, meaning not all of the earnings improvement was operational and making the treatment of future credits important to the near-term outlook.

Still, ethanol demand, record plant production, and internal growth projects provide a constructive backdrop.

The company is also emphasizing productivity and higher-margin specialty businesses to make earnings less dependent on commodity conditions.

Management continues to target a $7.00 earnings-per-share run rate by the end of 2028.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on ANDE.

Top Dividend Champion #7: Stepan Company (SCL)

- Expected total return: 18.8%

- Dividend Risk Score: A

Stepan manufactures specialty and intermediate chemicals used in consumer, industrial, agricultural, and construction markets.

The company operates through its Surfactants, Polymers, and Specialty Products segments.

Its formulations are often small components of customers’ finished products but perform important functions, supporting sticky commercial relationships.

Stepan has increased its dividend for 59 consecutive years.

On April 28th, 2026, Stepan reported first-quarter net sales of $604.5 million, up 2% from the prior year. Organic net sales increased 4%, while organic volume was flat.

Strong demand in crop productivity, oilfield, and industrial cleaning applications was offset by weak European Polymers demand.

Adjusted earnings-per-share declined to $0.45 from $0.84, and adjusted EBITDA fell 14% to $49.6 million.

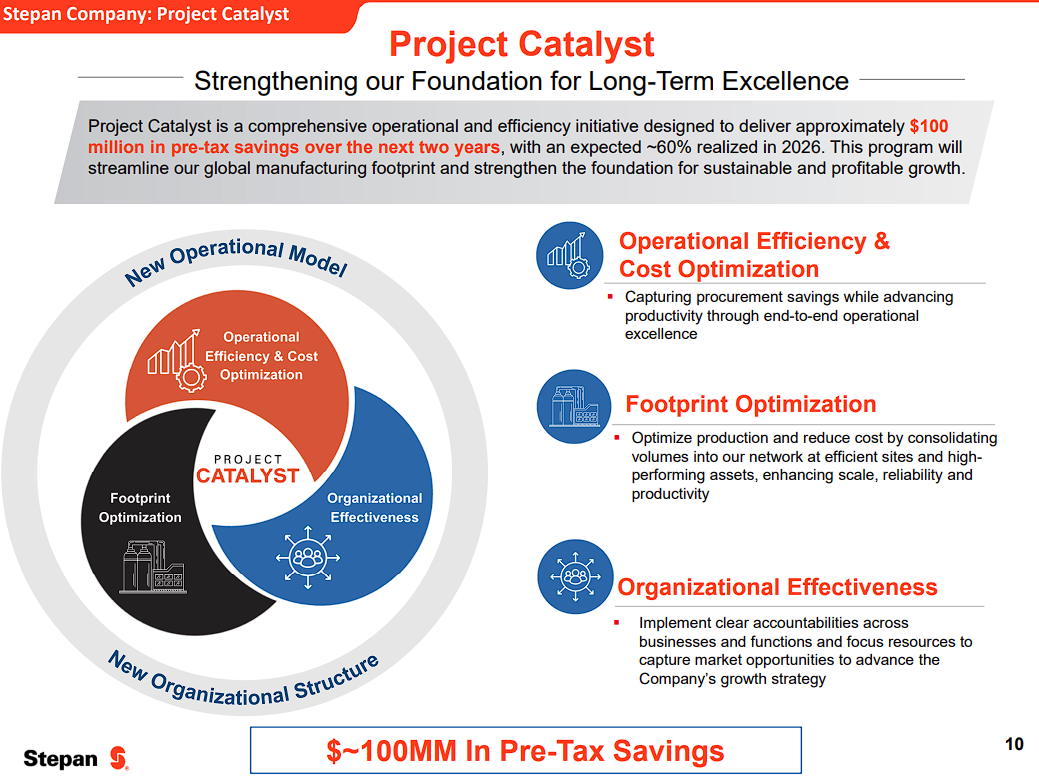

Stepan’s is now undergoing a restructuring program called Project Catalyst. GAAP results included a $65.4 million pre-tax charge tied to facility closures and asset optimization, producing a reported net loss of $41.4 million.

The changes are intended to create a leaner manufacturing footprint and improve asset utilization, but restructuring costs and soft demand could keep results uneven in the near term.

The long-term case rests on management converting those actions into better margins as volumes recover.

Stepan’s broad end-market exposure, manageable payout, and conservative dividend policy continue to support its A Dividend Risk Score.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on SCL.

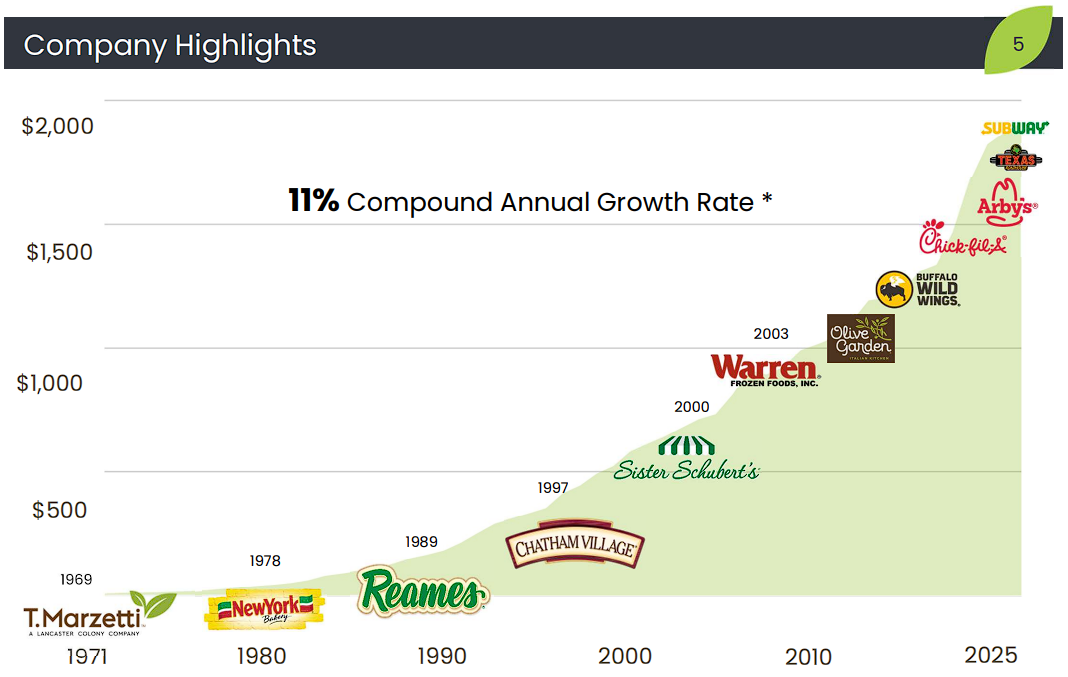

Top Dividend Champion #6: The Marzetti Company (MZTI)

- Expected total return: 18.8%

- Dividend Risk Score: A

The Marzetti Company, formerly Lancaster Colony, manufactures specialty food products for retail and foodservice customers.

The company’s brands include Marzetti, New York Bakery, and Sister Schubert’s, while licensed products include Olive Garden dressings and Chick-fil-A sauces.

Its mix of retail brands and restaurant partnerships provides exposure to both at-home and away-from-home food spending.

Marzetti has increased its regular cash dividend for 63 consecutive years.

On May 4th, 2026, Marzetti reported fiscal third-quarter sales of $453.4 million, down 1.0% year-over-year. Retail sales declined 3.2%, while reported Foodservice sales increased 1.5%.

Gross profit nevertheless rose 1.2% to a third-quarter record of $107.2 million, and gross margin expanded about 50 basis points to 23.6%.

The margin improvement shows that productivity and cost control partly offset the softer top line. Earnings per share declined to $1.35 from $1.49.

Marzetti completed its $400 million acquisition of Bachan’s Japanese Barbecue Sauce on May 1st. Bachan’s generated about $87 million of sales in 2025 and gives Marzetti another fast-growing brand to expand through its distribution network.

The purchase was funded with cash and a $200 million term loan, making integration and debt reduction important items to watch.

Regardless, we’ve reduced our earnings-per-share estimate for Fiscal 2026 by 25 cents to $6.75 following a very weak quarter.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on MZTI.

Top Dividend Champion #5: Brown & Brown, Inc. (BRO)

- Expected total return: 19.9%

- Dividend Risk Score: A

Brown & Brown is a leading insurance brokerage firm that provides property and casualty insurance, employee benefits, risk management, and specialty distribution services.

Its brokerage model produces recurring commission revenue without assuming most of the underwriting risk carried by insurers.

The company now operates from more than 700 locations and employs roughly 23,000 professionals.

Brown & Brown has increased its dividend for 32 consecutive years.

On April 27th, 2026, Brown & Brown reported first-quarter revenue of $1.9 billion, up 35.4% year-over-year. Acquisitions contributed $435 million, while organic revenue was flat.

Organic revenue including contingent commissions increased 2.2%. Adjusted EBITDAC rose 36.6% to $731 million, and the adjusted EBITDAC margin improved 40 basis points to 38.5%. Adjusted earnings-per-share increased 7.8% to $1.39.

Brown & Brown is still dealing with the integration of Accession Risk Management, which substantially expanded its retail brokerage and specialty distribution operations.

Acquisitions drove most of the reported growth in the quarter, so converting that added scale into stronger organic growth will be central to the investment case.

Organic trends were subdued, but margins remained firm despite the integration work.

Brown & Brown’s recurring revenue, low capital requirements, decentralized operating model, and long acquisition record continue to support its dividend and long-term growth outlook.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on BRO.

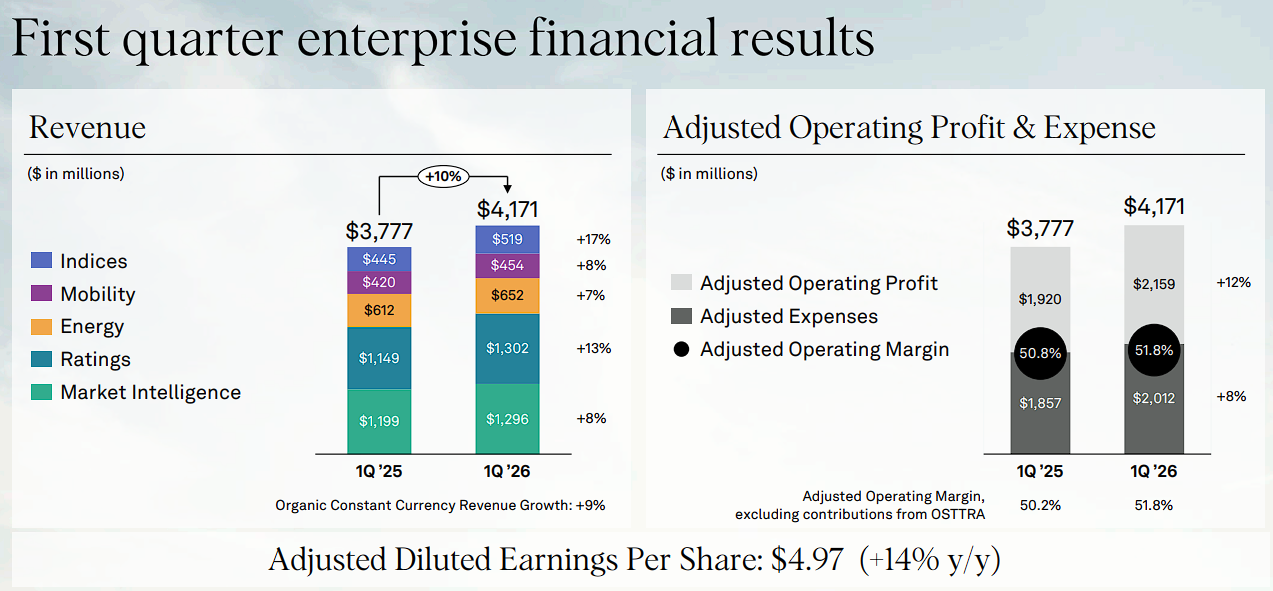

Top Dividend Champion #4: S&P Global Inc. (SPGI)

- Expected total return: 21.4%

- Dividend Risk Score: A

S&P Global provides credit ratings, financial data and analytics, commodity-market intelligence, and stock market indices.

Its revenue comes from recurring subscriptions, transaction-linked ratings fees, and asset-based index fees. These businesses benefit from valuable proprietary data, recognized brands, and high switching costs.

S&P Global has increased its dividend for 53 consecutive years.

On April 28th, 2026, S&P Global reported first-quarter revenue of $4.17 billion, up 10% year-over-year.

Adjusted earnings per share increased 14% to $4.97, while the adjusted operating margin expanded 100 basis points to 51.8%.

Ratings, Indices, and Market Intelligence were the primary growth drivers. The company also repurchased $1.0 billion of stock during the quarter.

On July 1st, the company completed the spin-off of its Mobility division as Mobility Global, now trading under the ticker MBGL. S&P Global shareholders received one Mobility Global share for each S&P Global share held on the record date.

The separation leaves S&P Global focused on its four core businesses and removes a more operationally distinct automotive-data platform from the group. It should also simplify the investment case and management’s capital-allocation decisions.

S&P Global expects to return more than 100% of adjusted free cash flow to shareholders in 2026.

Strong margins, recurring revenue, and substantial cash generation support its A Dividend Risk Score.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on SPGI.

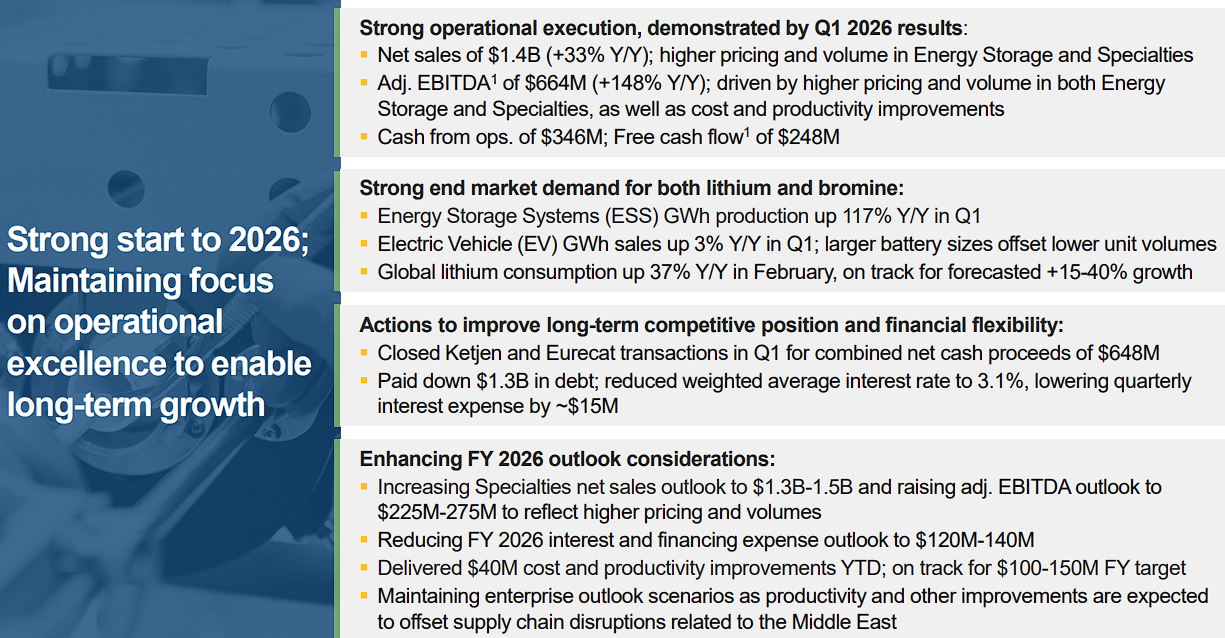

Top Dividend Champion #3: Albemarle Corporation (ALB)

- Expected total return: 21.5%

- Dividend Risk Score: A

Albemarle is a leading producer of lithium and specialty chemicals. Its Energy Storage segment supplies lithium products used in electric vehicles and grid storage, while Specialties serves markets including electronics, energy, pharmaceuticals, and industrial applications.

Its global resource and conversion footprint is a competitive advantage, although earnings remain highly sensitive to lithium prices.

On May 6th, 2026, Albemarle reported first-quarter sales of $1.4 billion, up 33% year-over-year. Adjusted earnings-per-share improved to $2.95 from a loss of $0.18, while adjusted EBITDA surged to $664 million from $267 million.

Energy Storage sales increased 70% to $891 million, with pricing up 51% and volumes up 14%. Specialties sales grew 12% to $358 million.

The sharp recovery in lithium prices is the most important recent development. It shows Albemarle’s earnings leverage when market conditions improve, but also highlights the stock’s cyclicality after the severe industry downturn.

Management expects 2026 capital spending of $550 million to $600 million and continues to prioritize productivity, disciplined investment, and cash preservation.

Those measures are important because commodity prices can reverse quickly even as long-term lithium demand grows.

On July 21st, Albemarle raised its quarterly dividend by 1.2% to $0.41 per share. Albemarle has now increased its dividend for 30 consecutive years.

The stock’s dividend yield remains modest, but its three-decade-long dividend growth record and the large gap between the share price and our fair value estimate produce a high expected total return.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on ALB.

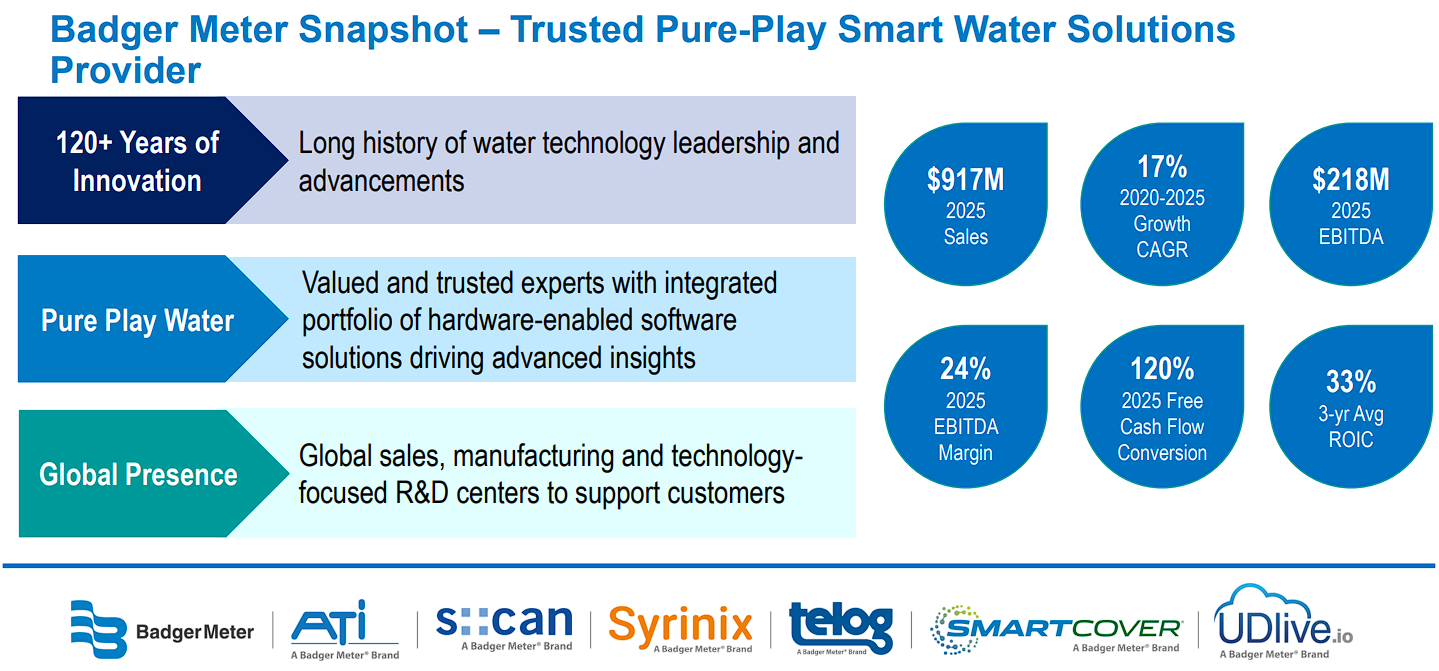

Top Dividend Champion #2: Badger Meter, Inc. (BMI)

- Expected total return: 24.8%

- Dividend Risk Score: A

Badger Meter provides smart water solutions through its BlueEdge portfolio. Its products combine meters, communications equipment, software, and analytics that help utilities and industrial customers monitor water use and detect leaks.

The portfolio includes connected endpoints and cloud-based applications, providing both equipment sales and growing recurring software and service revenue.

Badger Meter has increased its dividend for 33 consecutive years.

On July 22nd, 2026, Badger Meter reported second-quarter sales of $222.3 million. Sales increased 10% sequentially but declined 7% from a record prior-year quarter.

Operating earnings fell 12% to $39.4 million, and diluted earnings per share declined to $1.02 from $1.17. Utility water sales were down 8% year-over-year, reflecting uneven timing for advanced metering infrastructure projects, while flow instrumentation sales increased 6%.

Project timing can make quarterly comparisons uneven even when utilities’ long-term modernization needs remain intact.

Management expects awarded utility projects to support a stronger revenue run rate in the second half of 2026.

On May 1st, Badger Meter acquired sewer-monitoring specialist UDlive, expanding its capabilities beyond clean-water metering into sewer flow, level, and flood monitoring. This acquisition broadens the problems its technology can address for municipal customers.

The company reiterated its long-term framework for high-single-digit growth, supported by the multi-year digital transformation of water infrastructure and increasing adoption of data-driven utility management.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on BMI.

Top Dividend Champion #1: FactSet Research Systems Inc. (FDS)

- Expected total return: 26.0%

- Dividend Risk Score: A

FactSet provides financial data, analytics, and workflow solutions to investment managers, banks, wealth managers, private-market firms, and corporations.

Its subscription model creates recurring revenue and high customer switching costs. Deep integration into investment research, portfolio management, and trading workflows also supports strong retention and pricing power.

FactSet has raised its dividend for 27 consecutive years.

On July 1st, 2026, FactSet reported fiscal third-quarter revenue of $622.9 million, up 6.4% year-over-year. Organic revenue grew 7.0%, and adjusted earnings per share increased 6.1% to $4.53.

Organic annual subscription value reached $2.49 billion, up 7.1%, while annual retention remained above 95%. Free cash flow increased 11.1% to $254.0 million.

Adjusted operating margin declined to 34.0% from 36.8%, showing that current investment is weighing on profitability despite continued earnings growth.

FactSet is now pushing to embed artificial intelligence across its platform. More than 90% of its 50 largest clients now use at least four FactSet AI products, suggesting that AI can deepen customer relationships instead of simply disrupting the platform.

FactSet also returned $243.4 million to shareholders during the quarter through dividends and share repurchases and raised its quarterly dividend by $0.06 to $1.16.

A depressed valuation, combined with continued subscription growth and high retention, drives the highest expected return in this ranking.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on FDS.