Updated on August 2nd, 2026 by Nikolaos Sismanis

With contributions from Ben Reynolds

Oil and gas royalty trusts are now offering exceptionally high distributions to their investors, resulting in much higher yields than the ~1.2% average dividend yield of the S&P 500.

We have created a spreadsheet of high dividend stocks with dividend yields of 4% or more…

You can download your free full list of all securities with 4%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

In this article, we will discuss the prospects of the highest-yielding royalty trusts in the Sure Analysis Research Database.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

- High-Yield Royalty Trust No. 7: Permian Basin Royalty Trust (PBT)

- High-Yield Royalty Trust No. 6: San Juan Basin Royalty Trust (SJT)

- High-Yield Royalty Trust No. 5: Cross Timbers Royalty Trust (CRT)

- High-Yield Royalty Trust No. 4: Sabine Royalty Trust (SBR)

- High-Yield Royalty Trust No. 3: Permianville Royalty Trust (PVL)

- High-Yield Royalty Trust No. 2: PermRock Royalty Trust (PRT)

- High-Yield Royalty Trust No. 1: Mesa Royalty Trust (MTR)

High-Yield Royalty Trust No. 7: Permian Basin Royalty Trust (PBT)

- Dividend Yield: 1.0%

Permian Basin Royalty Trust was created in 1980 and owns a 75% net overriding royalty interest in the Waddell Ranch properties and a 95% interest in the Texas Royalty properties.

The trust is a passive vehicle: it cannot acquire new assets or control drilling, production, or operating costs.

This makes its distributions highly dependent on commodity prices, production volumes, and expenses reported by the operators.

For the first quarter of 2026, royalty income increased to $3.6 million from $3.1 million a year earlier.

Distributable income was $3.0 million, or approximately $0.06 per unit, compared with $2.6 million and roughly the same per-unit amount in the prior-year period.

The quarter included a $1.1 million partial settlement payment from Blackbeard Operating, which helped offset lower realized oil and natural gas prices.

PBT declared a July distribution of $0.043566 per unit. That payment also benefited from another $1.1 million settlement installment and therefore should not be treated as a normalized run rate.

More importantly, the Waddell Ranch properties made no contribution because production costs exceeded gross proceeds, leaving the properties in an excess-cost position.

The 1.0% listed yield reflects the Sure Analysis estimate, but actual cash income can vary sharply from month to month.

High-Yield Royalty Trust No. 6: San Juan Basin Royalty Trust (SJT)

- Dividend Yield: 3.7%

San Juan Basin Royalty Trust was established in 1980 and owns a 75% net overriding royalty interest in properties located in northwestern New Mexico.

The assets are operated by Hilcorp San Juan, while the trust itself has no employees, cannot add properties, and has no control over capital spending.

SJT is overwhelmingly exposed to natural gas, making its cash flow sensitive to regional gas prices and operator expenses.

In the first quarter of 2026, the trust recorded no royalty income and a distributable loss of $363,000, or $0.0078 per unit.

Gross proceeds fell 36% to $15.1 million, while production costs totaled $12.8 million.

The resulting net proceeds were applied against accumulated excess production costs instead of being distributed.

Those excess costs declined to $6.2 million gross at quarter-end from $8.4 million at the end of 2025, but they remain a hurdle.

Hilcorp’s 2026 capital plan calls for $14 million of spending across 32 drilling, recompletion, workover, and facilities projects.

This activity could support future production, but it can also delay the return of cash distributions.

SJT has not generated royalty income since April 2024 and declared no July 2026 distribution.

Accordingly, the 3.7% figure is our modeled yield; the cash yield is zero until excess costs and other obligations are cleared.

High-Yield Royalty Trust No. 5: Cross Timbers Royalty Trust (CRT)

- Dividend Yield: 4.2%

Cross Timbers Royalty Trust was created in 1991 by XTO Energy. It holds 90% net profits interests in royalty and overriding-royalty properties in Texas, Oklahoma, and New Mexico, as well as 75% net profits interests in working-interest properties in Texas and Oklahoma.

XTO, a subsidiary of Exxon Mobil, operates all of the underlying properties, while the trust functions as a passive conduit for monthly cash distributions.

First-quarter 2026 results were weak. Net profit income fell 62% to $774,000, and distributable income declined to $503,000, or $0.083901 per unit, from $1.8 million, or $0.297323 per unit, a year earlier.

Lower oil and natural gas volumes, weaker oil pricing, and higher overhead and production expenses outweighed lower taxes and development costs. Monthly distributions during the quarter totaled only $0.083901 per unit.

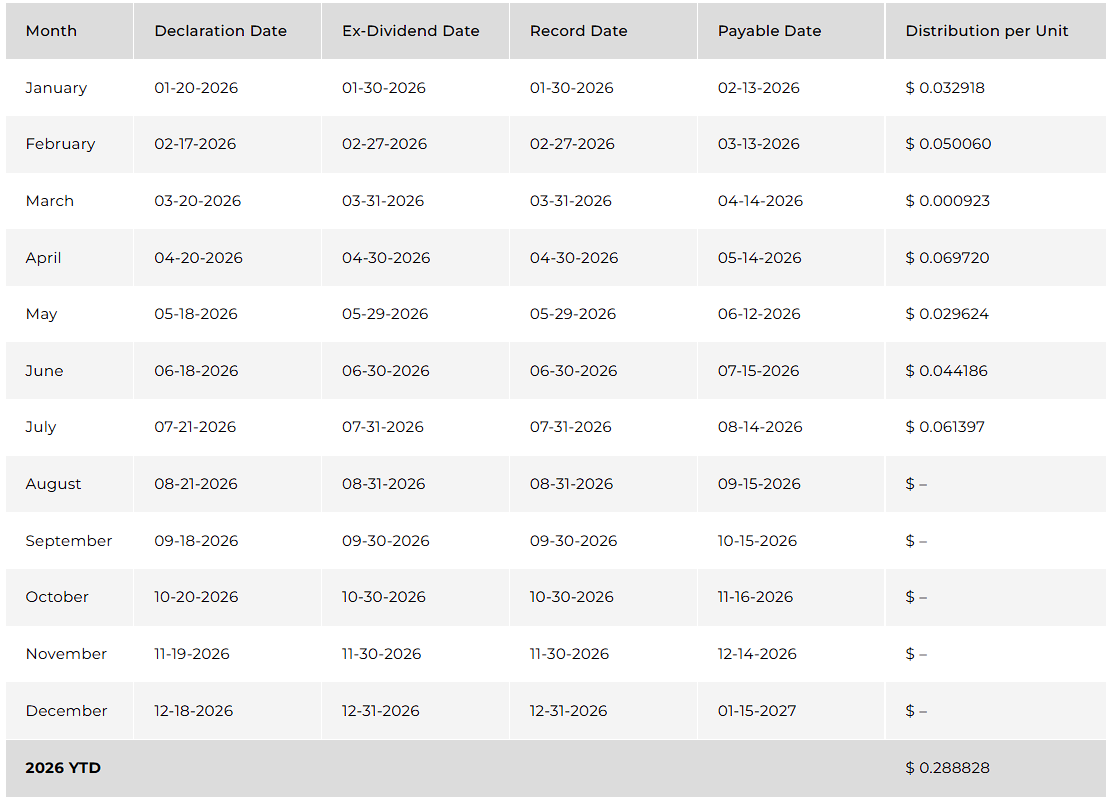

Results improved in July, when CRT declared a distribution of $0.061397 per unit. The underlying calculation benefited from higher realized prices of $109.21 per barrel of oil and $4.84 per Mcf of natural gas.

However, excess costs remained sizable on both the Texas and Oklahoma working-interest properties.

Investors should therefore view the 4.2% yield as variable rather than bond-like, as monthly payments can rise when prices improve, but production declines, development spending, and excess-cost balances can just as quickly pressure cash flow.

High-Yield Royalty Trust No. 4: Sabine Royalty Trust (SBR)

- Dividend Yield: 5.7%

Sabine Royalty Trust was formed in 1982 and began trading in 1983.

It owns royalty and mineral interests in producing oil and natural gas properties across Florida, Louisiana, Mississippi, New Mexico, Oklahoma, and Texas.

Its assets have remained productive for more than 40 years. Like other royalty trusts, SBR cannot acquire new properties and depends on third-party operators.

In the first quarter of 2026, distributable income was $13.0 million, or about $0.89 per unit. Royalty income fell 27% to $14.2 million as lower oil and natural gas production and weaker oil prices more than offset improved gas pricing and lower operating expenses and taxes.

Oil production dropped to 139,120 barrels from 211,707 barrels, while natural gas production declined to 2.8 million Mcf from 3.9 million Mcf.

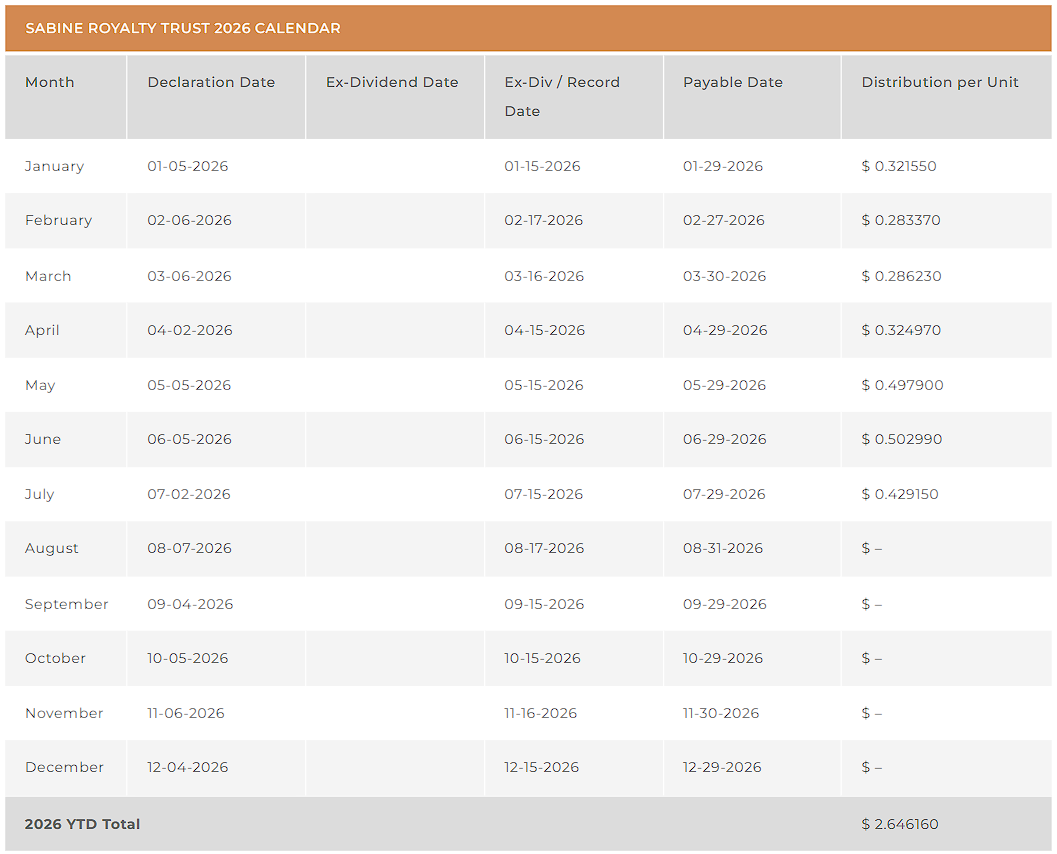

SBR nevertheless continues to produce meaningful monthly income. The trust declared a July distribution of $0.429150 per unit, bringing total distributions through the first seven months of 2026 to $2.646160 per unit.

Its broad property base is a relative strength within the royalty-trust group, but the declining first-quarter volumes remain important.

The 5.7% yield can fluctuate materially with production timing, commodity prices, and operator expenses, so investors should not assume the July payment will persist every month.

High-Yield Royalty Trust No. 3: Permianville Royalty Trust (PVL)

- Dividend Yield: 7.7%

Permianville Royalty Trust was formed in 2011 and owns an 80% net profits interest in oil and natural gas properties located in Texas, Louisiana, and New Mexico.

The trust is passive and cannot purchase additional assets or direct operating activity.

Its distributions are therefore determined by production volumes, commodity prices, operating and development expenses, and any amounts withheld to build cash reserves.

PVL’s first-quarter 2026 results showed a meaningful recovery. Income from the net profits interest was $2.0 million, compared with no income in the prior-year quarter.

Distributable income reached $1.4 million, or $0.043 per unit, versus zero a year earlier.

Combined production increased 27% to 395,905 barrels of oil equivalent, driven by a 48% increase in natural gas volumes, although oil production declined 9%.

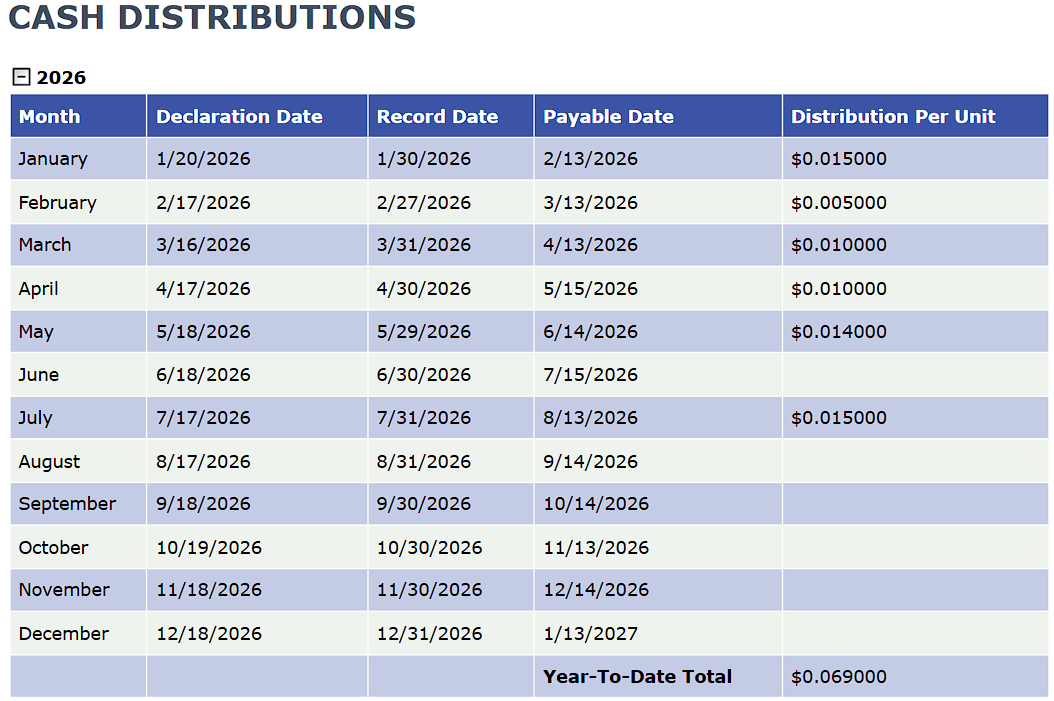

The trust declared a July distribution of $0.015 per unit, bringing year-to-date distributions through July to $0.069 per unit.

This continued the recovery that began when PVL reinstated distributions in August 2025 following a lengthy suspension.

However, the trustee withheld approximately $453,000 during the first quarter to strengthen its cash reserve.

The 7.7% yield is attractive, but PVL’s recent history demonstrates that payments can disappear when property-level costs exceed proceeds.

Investors should treat the improving production profile as encouraging while maintaining conservative expectations for monthly income.

High-Yield Royalty Trust No. 2: PermRock Royalty Trust (PRT)

- Dividend Yield: 9.9%

PermRock Royalty Trust was formed in 2017 and owns an 80% net profits interest in oil and natural gas properties spanning four operating areas in the Texas Permian Basin. The underlying portfolio covers 31,354 gross acres.

The trust is passive, while operator T2S manages production, workovers, and development decisions that determine the monthly cash available to unitholders.

For the first quarter of 2026, net profit income fell to $647,000 from $1.7 million a year earlier.

After interest and administrative expenses, distributable income was $404,000, or $0.033212 per unit, versus $1.5 million, or $0.120517 per unit.

Oil volumes declined 36%, natural gas volumes fell 22%, and realized prices decreased for both commodities. Severe winter weather caused temporary shut-ins, while weak Waha Hub pricing further pressured natural gas realizations.

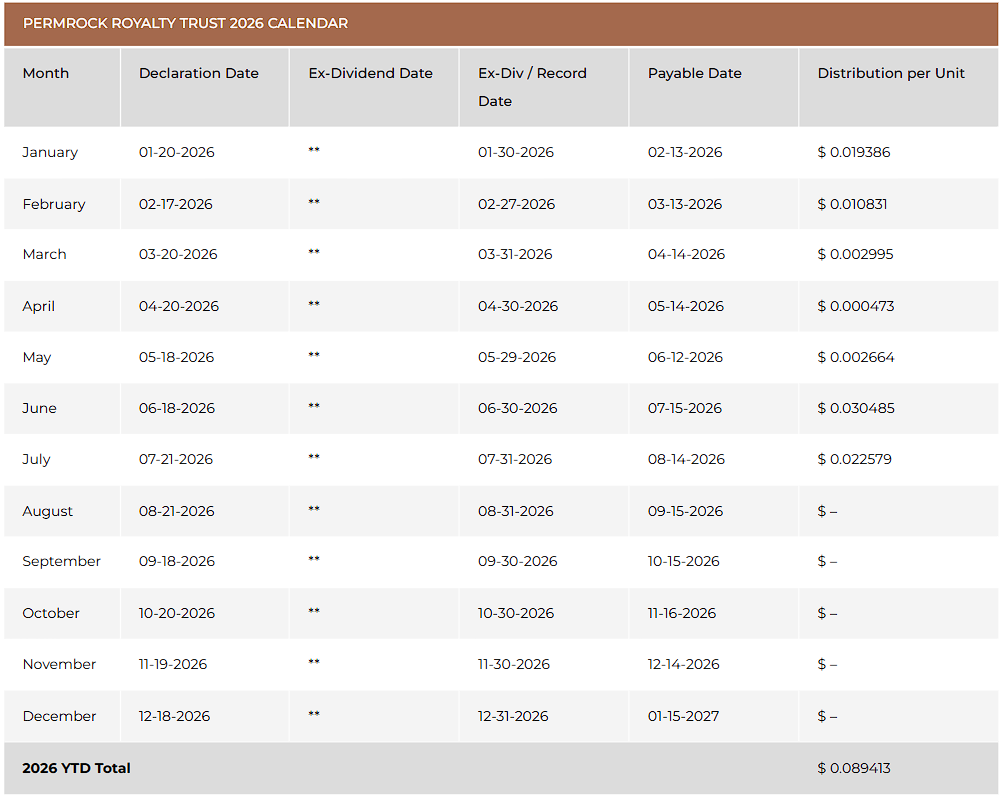

PRT declared a July distribution of $0.022579 per unit.

The payout was reduced by $385,000 of reserves retained by T2S for future ad valorem taxes and workovers, illustrating how operator decisions can create monthly volatility.

T2S has budgeted about $0.7 million for 2026 workovers on 22 shut-in wells, which could improve production but also requires near-term spending.

PRT’s 9.9% yield is compelling, yet the recent decline in distributable income and reserve withholding make it appropriate only for investors comfortable with variable payments.

High-Yield Royalty Trust No. 1: Mesa Royalty Trust (MTR)

- Dividend Yield: 10.3%

Mesa Royalty Trust was created in 1979 and owns overriding royalty interests in the Hugoton field of Kansas and the San Juan Basin of New Mexico and Colorado.

It is entitled to 11.44% of 90% of net proceeds from interests in the underlying properties.

The trust cannot acquire assets or control operations, leaving results in the hands of Hilcorp, Scout Energy, Simcoe, Red Willow, and working-interest owners.

First-quarter 2026 results were weak. Royalty income fell to $51,687 from $110,963 a year earlier, while higher administrative expenses left distributable income of $601, or $0.0003 per unit, compared with $80,999, or $0.0435 per unit.

All royalty income came from the Hilcorp-operated New Mexico properties. The Hugoton and Colorado properties generated none because costs and prior-period adjustments exceeded revenue.

The trustee announced that no July 2026 distribution would be paid because property-level costs, trust charges, and other expenses exceeded available revenue.

Future payments may also remain limited while the trustee works toward a $2.0 million contingent reserve.

Therefore, MTR’s top-ranked 10.3% yield is our forward estimate, not a dependable current income rate.

The units offer upside if commodity prices and net proceeds recover, but excess costs, reserve funding, and a recent zero distribution make MTR the most speculative income selection in this ranking.

Final Thoughts

On the surface, oil and gas royalty trusts are attractive as they widely offer higher yields than the S&P 500 average.

However, oil and gas prices are infamous for their dramatic swings. Investors should also be aware of the excessive risk of all these trusts near the peak of their cycle.

The ideal time to buy these trusts is during a severe downturn of the energy sector, when these stocks plunge and may become undervalued.

As mentioned above, all the oil and gas trusts are highly risky due to the natural decline of their production and their sensitivity to the prices of oil and gas.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Monthly Dividend Stocks: Individual securities that pay out every month