Published on May 27th, 2026 by Bob Ciura

Dividend growth investing provides both long-term compounding and current income. This is an ideal mix for both retirement preparation and actual retirement.

But not just any stock that may be able to temporarily increase its dividends will do. Think of each individual dividend growth stock in which you invest as a “guardian” of your wealth.

“Good guardians” will compound over time. Poor investments do the opposite. That’s why the quality of the businesses in which you invest is of critical importance.

That’s where the Dividend Champions come in.

The Dividend Champions have increased their dividends for over 25 consecutive years. With this in mind, we created a downloadable list of over 130 Dividend Champions.

You can download your free copy of the Dividend Champions list, along with relevant financial metrics like price-to-earnings ratios, dividend yields, and payout ratios, by clicking on the link below:

We recommend high-quality dividend growth stocks meant to be bought and held for the long run.

This article will rank 10 Dividend Champions with Dividend Risk Scores of ‘A’, our highest rating, that currently have buy ratings from Sure Dividend.

Table of Contents

You can instantly jump to any specific section of the article by clicking on the links below:

- Wealth Guardian #10: Abbott Laboratories (ABT)

- Wealth Guardian #9: The Marzetti Company (MZTI)

- Wealth Guardian #8: Becton Dickinson & Co. (BDX)

- Wealth Guardian #7: H2O America (HTO)

- Wealth Guardian #6: Automatic Data Processing (ADP)

- Wealth Guardian #5: Stepan Co. (SCL)

- Wealth Guardian #4: Brown & Brown (BRO)

- Wealth Guardian #3: Badger Meter Inc. (BMI)

- Wealth Guardian #2: Thomson-Reuters Corp. (TRI)

- Wealth Guardian #1: Factset Research Systems (FDS)

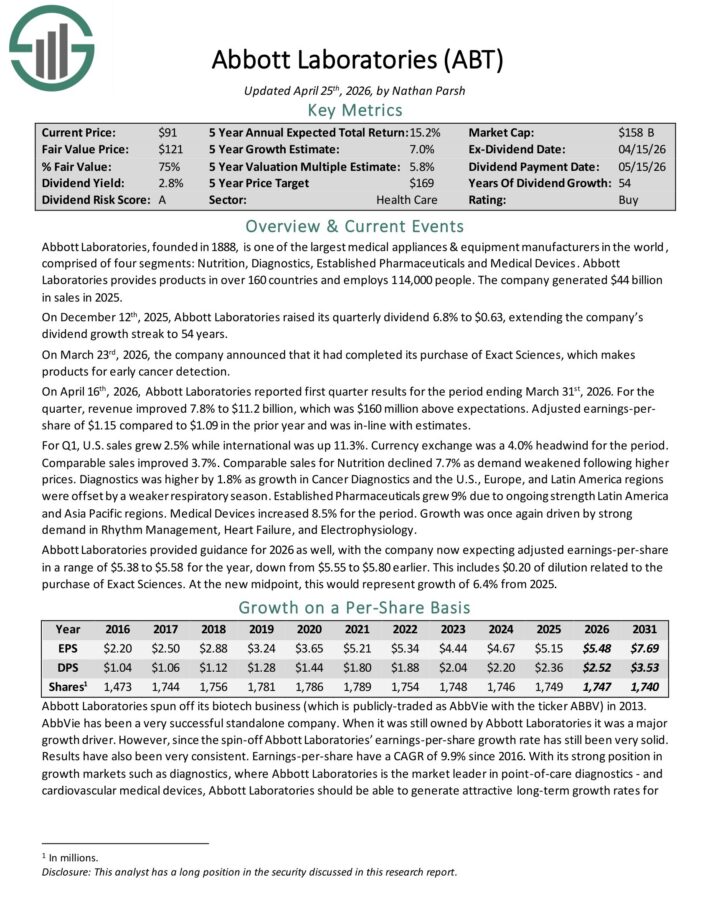

Wealth Guardian #10: Abbott Laboratories (ABT)

- Expected Annual Returns: 16.4%

Abbott Laboratories, founded in 1888, is one of the largest medical appliances & equipment manufacturers in the world, comprised of four segments: Nutrition, Diagnostics, Established Pharmaceuticals and Medical Devices.

Abbott Laboratories provides products in over 160 countries and employs 114,000 people. The company generated $44 billion in sales in 2025.

On December 12th, 2025, Abbott Laboratories raised its quarterly dividend 6.8% to $0.63, extending the company’s dividend growth streak to 54 years.

On April 16th, 2026, Abbott Laboratories reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue improved 7.8% to $11.2 billion, which was $160 million above expectations. Adjusted earnings-per-share of $1.15 compared to $1.09 in the prior year and was in-line with estimates.

For Q1, U.S. sales grew 2.5% while international was up 11.3%. Currency exchange was a 4.0% headwind for the period.

Comparable sales improved 3.7%. Comparable sales for Nutrition declined 7.7% as demand weakened following higher prices.

Abbott Laboratories provided guidance for 2026 as well, with the company now expecting adjusted earnings-per-share in a range of $5.38 to $5.58 for the year, down from $5.55 to $5.80 earlier.

At the new midpoint, this would represent growth of 6.4% from 2025.

Click here to download our most recent Sure Analysis report on ABT (preview of page 1 of 3 shown below):

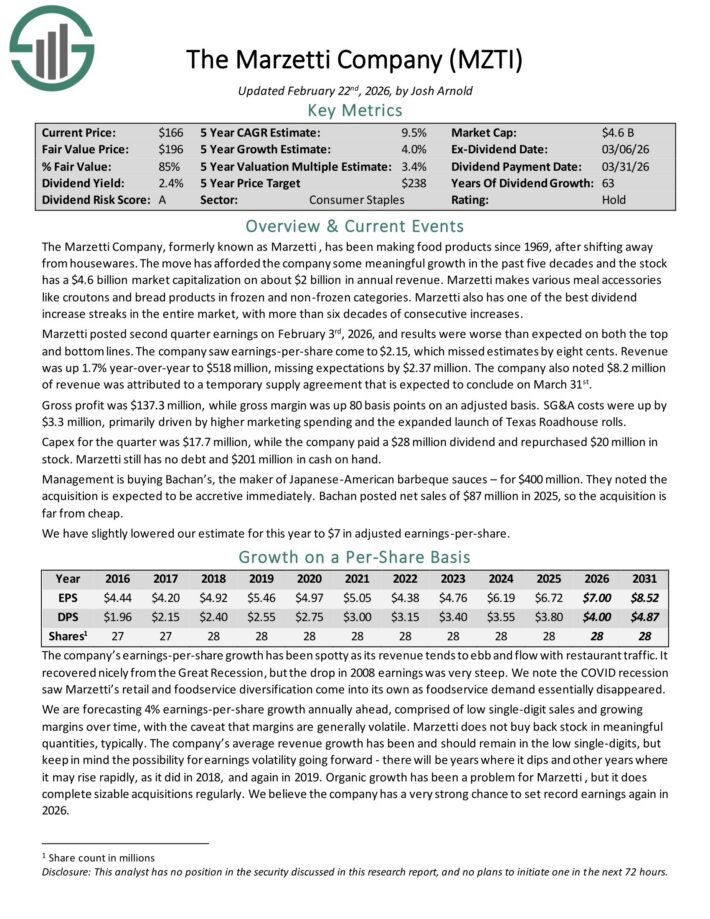

Wealth Guardian #9: The Marzetti Company (MZTI)

- Expected Annual Returns: 17.2%

The Marzetti Company has been making food products since 1969. Marzetti makes various meal accessories like croutons and bread products in frozen and non-frozen categories.

Marzetti also has one of the best dividend increase streaks in the entire market, with more than six decades of consecutive increases.

Marzetti posted second quarter earnings on February 3rd, 2026, and results were worse than expected on both the top and bottom lines. The company saw earnings-per-share come to $2.15, which missed estimates by eight cents.

Revenue was up 1.7% year-over-year to $518 million, missing expectations by $2.37 million. The company also noted $8.2 million of revenue was attributed to a temporary supply agreement that is expected to conclude on March 31st.

Gross profit was $137.3 million, while gross margin was up 80 basis points on an adjusted basis. SG&A costs were up by $3.3 million, primarily driven by higher marketing spending and the expanded launch of Texas Roadhouse rolls.

Capex for the quarter was $17.7 million, while the company paid a $28 million dividend and repurchased $20 million in stock. Marzetti still has no debt and $201 million in cash on hand.

Management is buying Bachan’s, the maker of Japanese-American barbeque sauces – for $400 million. They noted the acquisition is expected to be accretive immediately.

Click here to download our most recent Sure Analysis report on MZTI (preview of page 1 of 3 shown below):

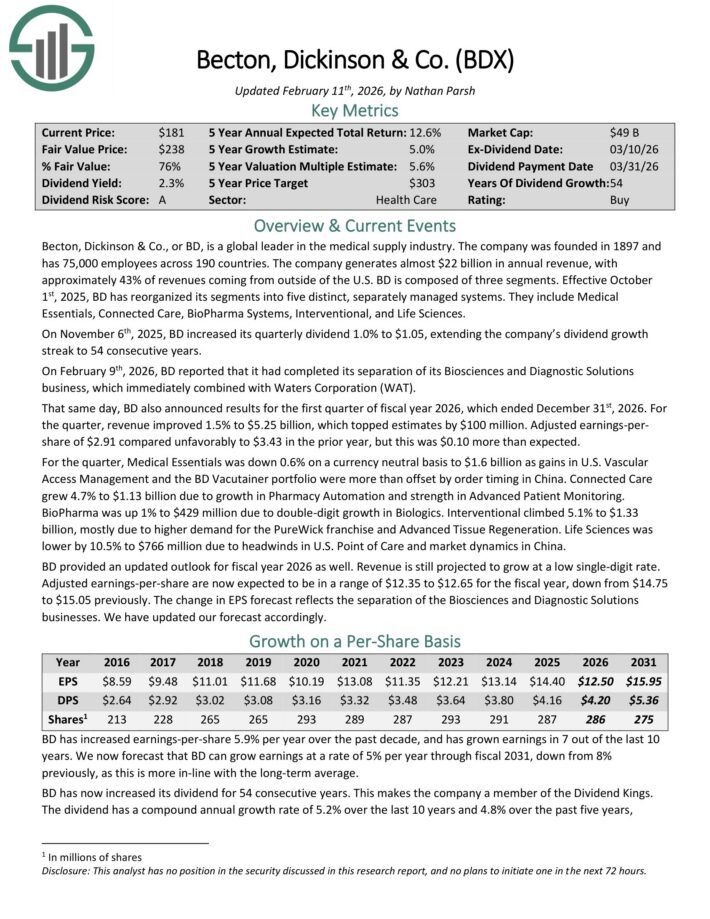

Wealth Guardian #8: Becton Dickinson & Co. (BDX)

- Expected Annual Returns: 17.3%

Becton, Dickinson & Co. is a global leader in the medical supply industry. The company was founded in 1897 and has 75,000 employees across 190 countries.

The company generates about $20 billion in annual revenue, with approximately 43% of revenues coming from outside of the U.S.

On November 6th, 2025, BD increased its quarterly dividend 1.0% to $1.05, extending the company’s dividend growth streak to 54 consecutive years.

BD also announced results for the first quarter of fiscal year 2026, which ended December 31st, 2026. For the quarter, revenue improved 1.5% to $5.25 billion, which topped estimates by $100 million.

Adjusted earnings-per-share of $2.91 compared unfavorably to $3.43 in the prior year, but this was $0.10 more than expected.

For the quarter, Medical Essentials was down 0.6% on a currency neutral basis to $1.6 billion as gains in U.S. Vascular Access Management and the BD Vacutainer portfolio were more than offset by order timing in China.

Connected Care grew 4.7% to $1.13 billion due to growth in Pharmacy Automation and strength in Advanced Patient Monitoring.

BioPharma was up 1% to $429 million due to double-digit growth in Biologics. Interventional climbed 5.1% to $1.33 billion, mostly due to higher demand for the PureWick franchise and Advanced Tissue Regeneration.

Click here to download our most recent Sure Analysis report on BDX (preview of page 1 of 3 shown below):

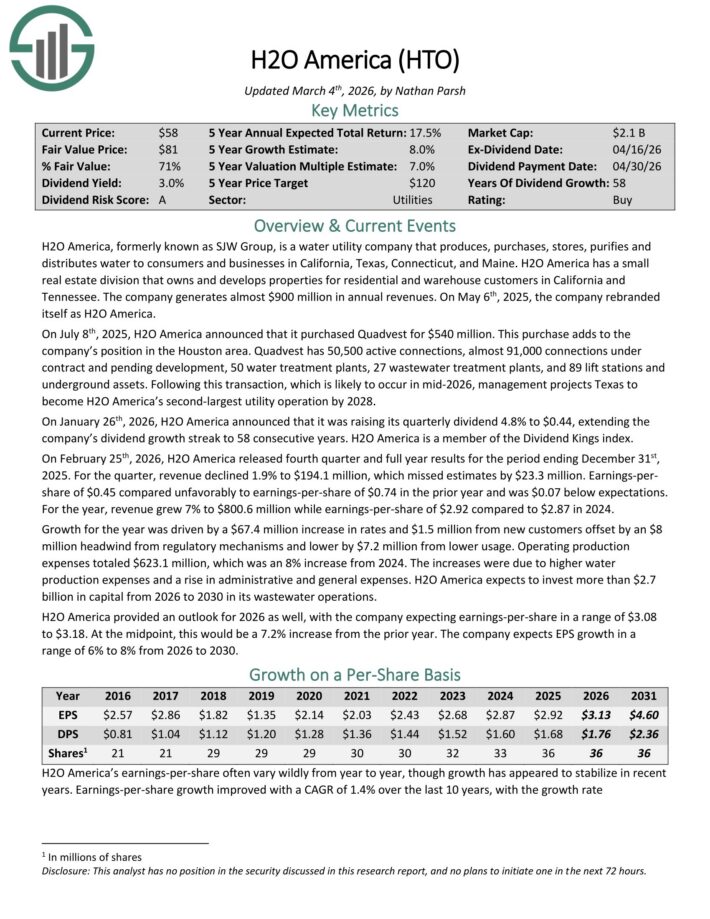

Wealth Guardian #7: H2O America (HTO)

- Expected Annual Returns: 17.6%

H2O America, formerly known as SJW Group, is a water utility company that distributes water to consumers and businesses in California, Texas, Connecticut, and Maine.

It also has a small real estate division that owns and develops properties for residential and warehouse customers in California and Tennessee. The company generates about $670 million in annual revenue.

On January 26th, 2026, H2O America raised its quarterly dividend 4.8% to $0.44, extending the company’s dividend growth streak to 58 consecutive years.

On February 25th, 2026, H2O America released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue declined 1.9% to $194.1 million, which missed estimates by $23.3 million.

Earnings-per-share of $0.45 compared unfavorably to earnings-per-share of $0.74 in the prior year and was $0.07 below expectations.

For the year, revenue grew 7% to $800.6 million while earnings-per-share of $2.92 compared to $2.87 in 2024.

Growth for the year was driven by a $67.4 million increase in rates and $1.5 million from new customers offset by an $8 million headwind from regulatory mechanisms and lower by $7.2 million from lower usage.

H2O America provided an outlook for 2026 as well, with the company expecting earnings-per-share in a range of $3.08 to $3.18. At the midpoint, this would be a 7.2% increase from the prior year.

Click here to download our most recent Sure Analysis report on HTO (preview of page 1 of 3 shown below):

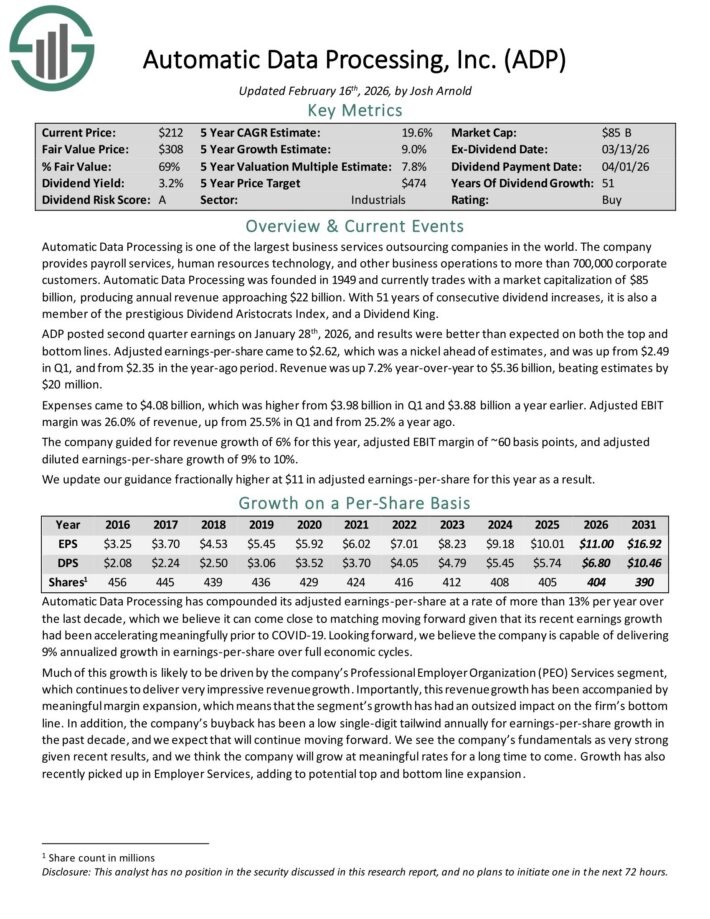

Wealth Guardian #6: Automatic Data Processing (ADP)

- Expected Annual Returns: 17.9%

Automatic Data Processing is one of the largest business services outsourcing companies in the world. The company provides payroll services, human resources technology, and other business operations to more than 700,000 corporate customers.

ADP posted second quarter earnings on January 28th, 2026, and results were better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to $2.62, which was a nickel ahead of estimates, and was up from $2.49 in Q1, and from $2.35 in the year-ago period. Revenue was up 7.2% year-over-year to $5.36 billion, beating estimates by $20 million.

Expenses came to $4.08 billion, which was higher from $3.98 billion in Q1 and $3.88 billion a year earlier. Adjusted EBIT margin was 26.0% of revenue, up from 25.5% in Q1 and from 25.2% a year ago.

For 2026, ADP guided for revenue growth of 6%, adjusted EBIT margin of ~60 basis points, and adjusted diluted earnings-per-share growth of 9% to 10%.

Click here to download our most recent Sure Analysis report on ADP (preview of page 1 of 3 shown below):

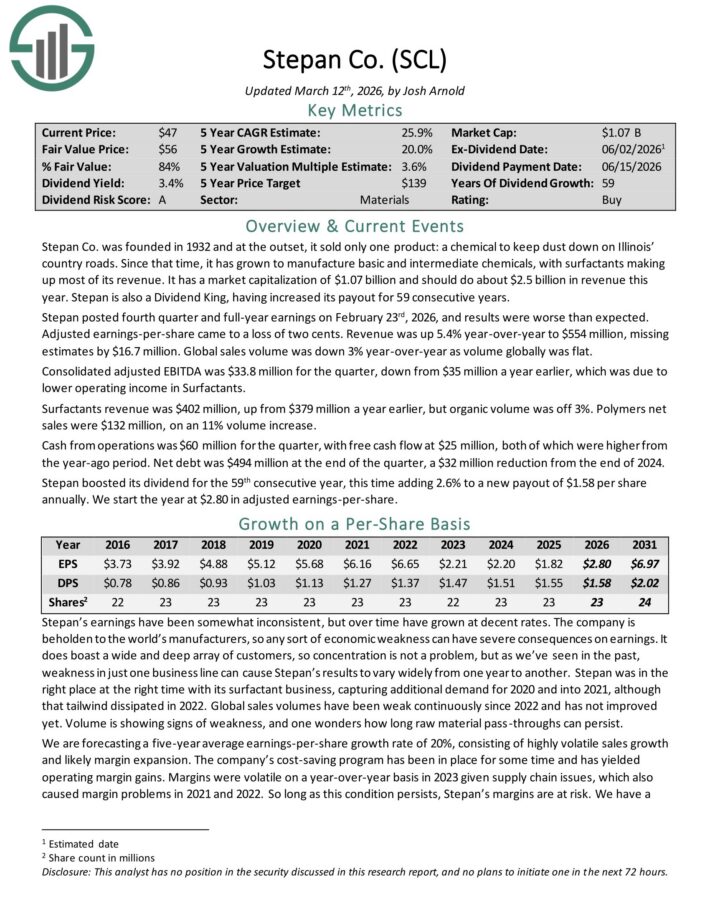

Wealth Guardian #5: Stepan Co. (SCL)

- Expected Annual Returns: 22.8%

Stepan manufactures basic and intermediate chemicals, including surfactants, specialty products, and much more for the food, supplement, and pharmaceutical markets.

It is organized into three distinct business lines: surfactants, polymers, and specialty products. The surfactants business is Stepan’s largest by revenue, accounting for ~68% of total sales in the most recent quarter.

Stepan posted fourth quarter and full-year earnings on February 23rd, 2026. Adjusted earnings-per-share came to a loss of two cents.

Revenue was up 5.4% year-over-year to $554 million, missing estimates by $16.7 million. Global sales volume was down 3% year-over-year as volume globally was flat.

Consolidated adjusted EBITDA was $33.8 million for the quarter, down from $35 million a year earlier, which was due to lower operating income in Surfactants.

Stepan boosted its dividend for the 59th consecutive year.

Click here to download our most recent Sure Analysis report on SCL (preview of page 1 of 3 shown below):

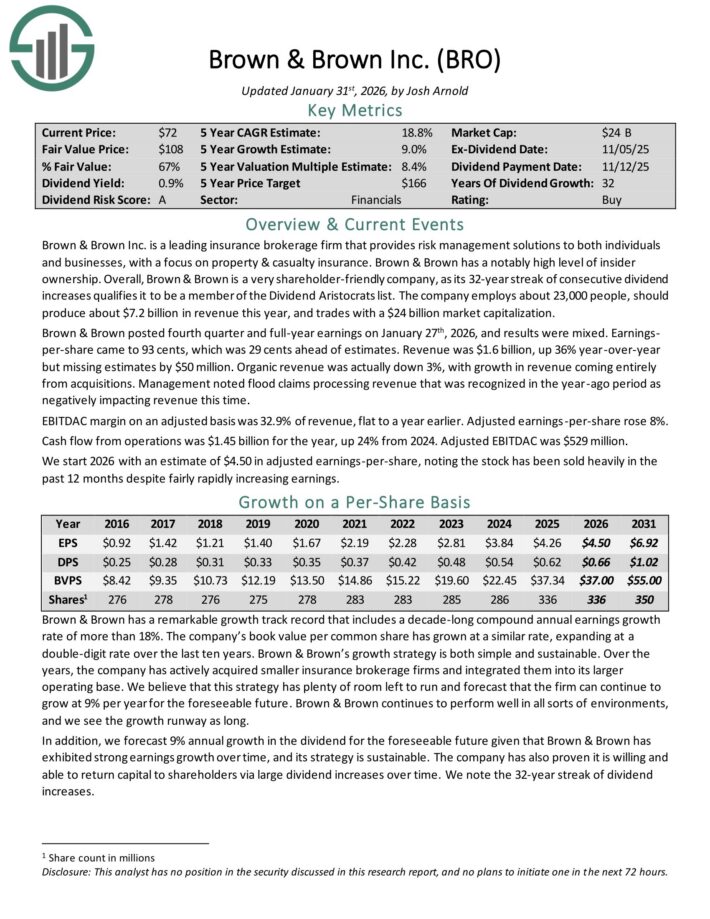

Wealth Guardian #4: Brown & Brown (BRO)

- Expected Annual Returns: 23.4%

Brown & Brown Inc. is a leading insurance brokerage firm that provides risk management solutions to both individuals and businesses, with a focus on property & casualty insurance.

Brown & Brown posted fourth quarter and full-year earnings on January 27th, 2026, and results were mixed. Earnings-per-share came to 93 cents, which was 29 cents ahead of estimates.

Revenue was $1.6 billion, up 36% year-over-year but missing estimates by $50 million. Organic revenue was actually down 3%, with growth in revenue coming entirely from acquisitions.

Management noted flood claims processing revenue that was recognized in the year-ago period as negatively impacting revenue this time.

EBITDAC margin on an adjusted basis was 32.9% of revenue, flat to a year earlier. Adjusted earnings-per-share rose 8%.

Cash flow from operations was $1.45 billion for the year, up 24% from 2024. Adjusted EBITDAC was $529 million.

For 2026, we anticipate EPS of $4.50.

Click here to download our most recent Sure Analysis report on BRO (preview of page 1 of 3 shown below):

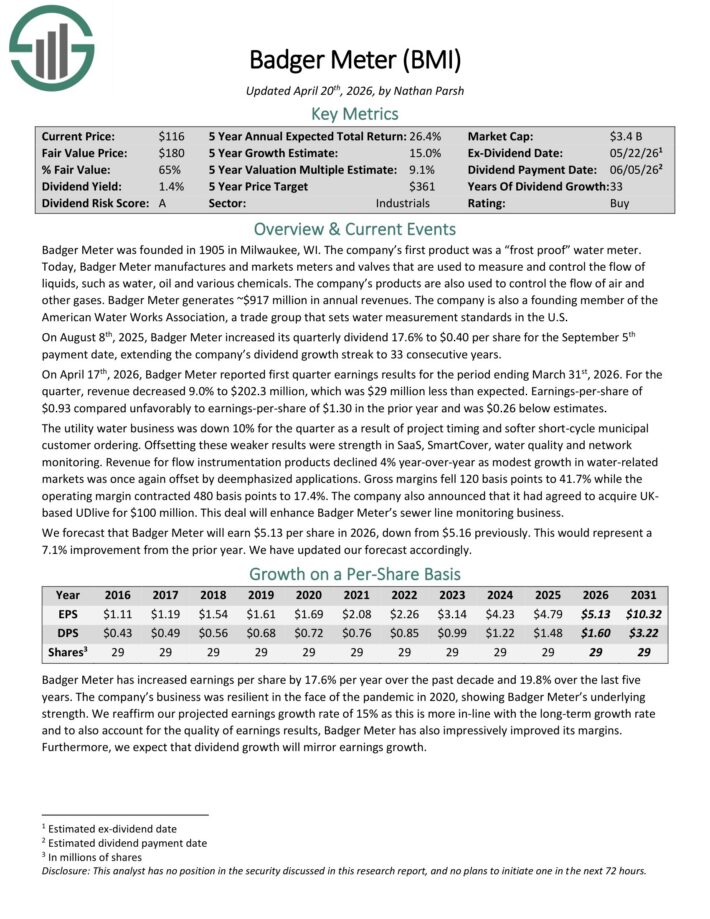

Wealth Guardian #3: Badger Meter Inc. (BMI)

- Expected Annual Returns: 24.1%

Badger Meter manufactures and markets meters and valves that are used to measure and control the flow of liquids, such as water, oil and various chemicals.

The company’s products are also used to control the flow of air and other gases. Badger Meter generates ~$917 million in annual revenues.

On April 17th, 2026, Badger Meter reported first quarter earnings results for the period ending March 31st, 2026. For the quarter, revenue decreased 9.0% to $202.3 million, which was $29 million less than expected.

Earnings-per-share of $0.93 compared unfavorably to earnings-per-share of $1.30 in the prior year and was $0.26 below estimates.

The utility water business was down 10% for the quarter as a result of project timing and softer short-cycle municipal customer ordering.

Offsetting these weaker results were strength in SaaS, SmartCover, water quality and network monitoring.

Click here to download our most recent Sure Analysis report on BMI (preview of page 1 of 3 shown below):

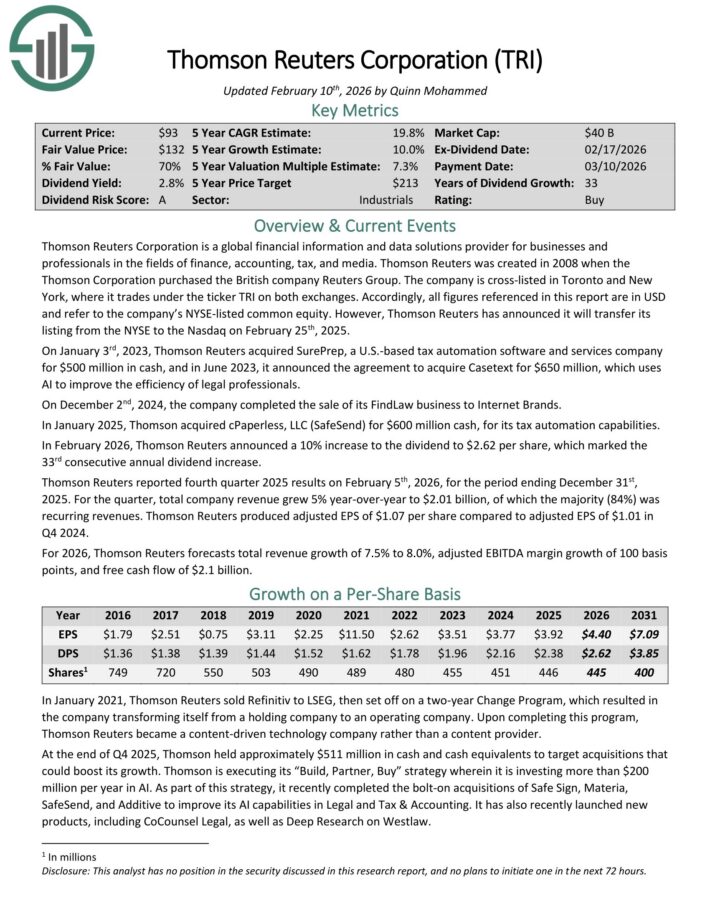

Wealth Guardian #2: Thomson-Reuters (TRI)

- Expected Annual Returns: 24.5%

Thomson Reuters Corporation is a global financial information and data solutions provider for businesses and professionals in the fields of finance, accounting, tax, and media.

In January 2025, Thomson acquired cPaperless, LLC (SafeSend) for $600 million cash, for its tax automation capabilities.

In February 2026, Thomson Reuters announced a 10% increase to the dividend to $2.62 per share, which marked the 33rd consecutive annual dividend increase.

Thomson Reuters reported fourth quarter 2025 results on February 5th, 2026. For the quarter, total company revenue grew 5% year-over-year to $2.01 billion, of which the majority (84%) was recurring revenues.

Thomson Reuters produced adjusted EPS of $1.07 per share compared to adjusted EPS of $1.01 in Q4 2024.

For 2026, Thomson Reuters forecasts total revenue growth of 7.5% to 8.0%, adjusted EBITDA margin growth of 100 basis points, and free cash flow of $2.1 billion.

Click here to download our most recent Sure Analysis report on TRI (preview of page 1 of 3 shown below):

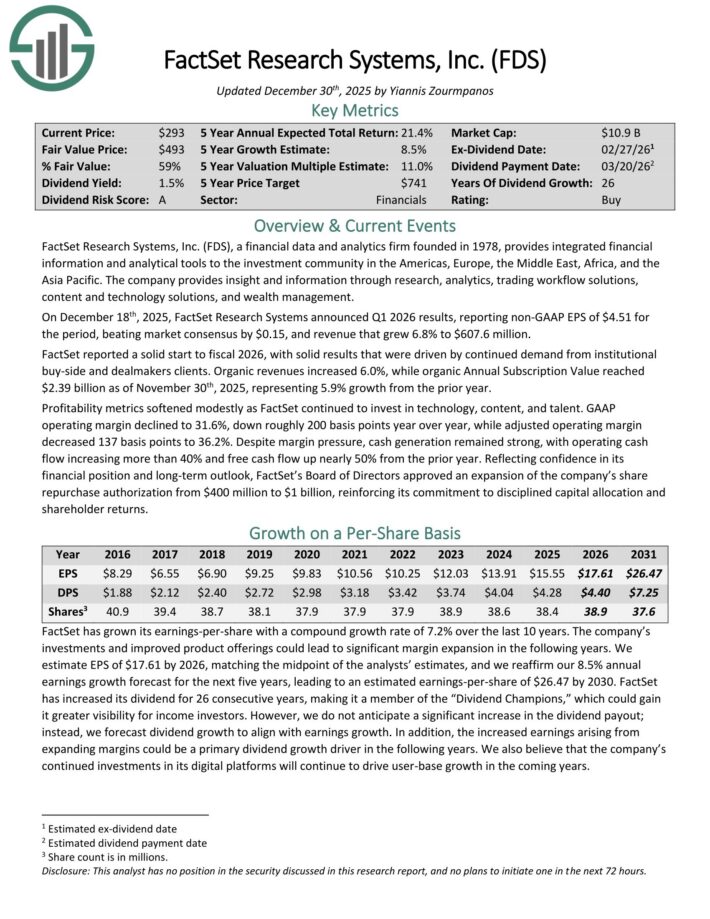

Wealth Guardian #1: Factset Research Systems (FDS)

- Expected Annual Returns: 27.4%

FactSet Research Systems, a financial data and analytics firm founded in 1978, provides integrated financial information and analytical tools to the investment community in the Americas, Europe, the Middle East, Africa, and Asia-Pacific.

The company provides insight and information through research, analytics, trading workflow solutions, content and technology solutions, and wealth management.

On December 18th, 2025, FactSet Research Systems announced Q1 2026 results, reporting non-GAAP EPS of $4.51 for the period, beating market consensus by $0.15, and revenue that grew 6.8% to $607.6 million.

FactSet reported a solid start to fiscal 2026, with solid results that were driven by continued demand from institutional buy-side and dealmakers clients.

Organic revenues increased 6.0%, while organic Annual Subscription Value reached $2.39 billion as of November 30th, 2025, representing 5.9% growth from the prior year.

Profitability metrics softened modestly as FactSet continued to invest in technology, content, and talent. GAAP operating margin declined to 31.6%, down roughly 200 basis points year over year, while adjusted operating margin decreased 137 basis points to 36.2%.

Despite margin pressure, cash generation remained strong, with operating cash flow increasing more than 40% and free cash flow up nearly 50% from the prior year.

Reflecting confidence in its financial position and long-term outlook, FactSet’s Board of Directors approved an expansion of the company’s share repurchase authorization from $400 million to $1 billion.

Click here to download our most recent Sure Analysis report on FDS (preview of page 1 of 3 shown below):

Additional Reading

The Dividend Champions list is not the only way to quickly screen for stocks that regularly pay rising dividends.

- Dividend Kings: 50+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Monthly Dividend Stocks: Individual securities that pay out every month

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more