Updated on June 3rd, 2026 by Bob Ciura

Investors looking to generate higher income levels from their investment portfolios should look at Real Estate Investment Trusts or REITs.

These are companies that own real estate properties and lease them to tenants, or invest in real estate backed loans, both of which generate a steady stream of income.

The bulk of their income is then passed on to shareholders through dividends.

You can see all 200+ REITs here.

You can download our full list of REITs, along with important metrics such as dividend yields and market capitalizations, by clicking on the link below:

The beauty of REITs for income investors is that they are required to distribute 90% of their taxable income to shareholders annually in the form of dividends. In return, REITs typically do not pay corporate taxes.

As a result, many of the 200+ REITs we track offer high dividend yields of 5%+.

But not all high-yielding stocks are automatic buys. Investors should carefully assess the fundamentals to ensure that high yields are sustainable.

Note that while the securities in this article have very high yields, a high yield alone does not make for a solid investment. Dividend safety, valuation, management, balance sheet health, and growth are also very important factors.

We urge investors to use the analysis below as informative but to do significant due diligence before buying into any security – especially high-yield securities.

Many (but not all) high-yield securities have a significant risk of a dividend reduction and/or deteriorating business results.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

- High-Yield REIT No. 10: Nexus Industrial REIT (EFRTF)

- High-Yield REIT No. 9: Gladstone Commercial Corp. (GOOD)

- High-Yield REIT No. 8: Bridgemarq Real Estate Services (BREUF)

- High-Yield REIT No. 7: Community Healthcare Trust (CHCT)

- High-Yield REIT No. 6: Innovative Industrial Properties (IIPR)

- High-Yield REIT No. 5: AGNC Investment Corp. (AGNC)

- High-Yield REIT No. 4: Dynex Capital (DX)

- High-Yield REIT No. 3: ARMOUR Residential REIT (ARR)

- High-Yield REIT No. 2: Orchid Island Capital (ORC)

- High-Yield REIT No. 1: Ellington Credit Co. (EARN)

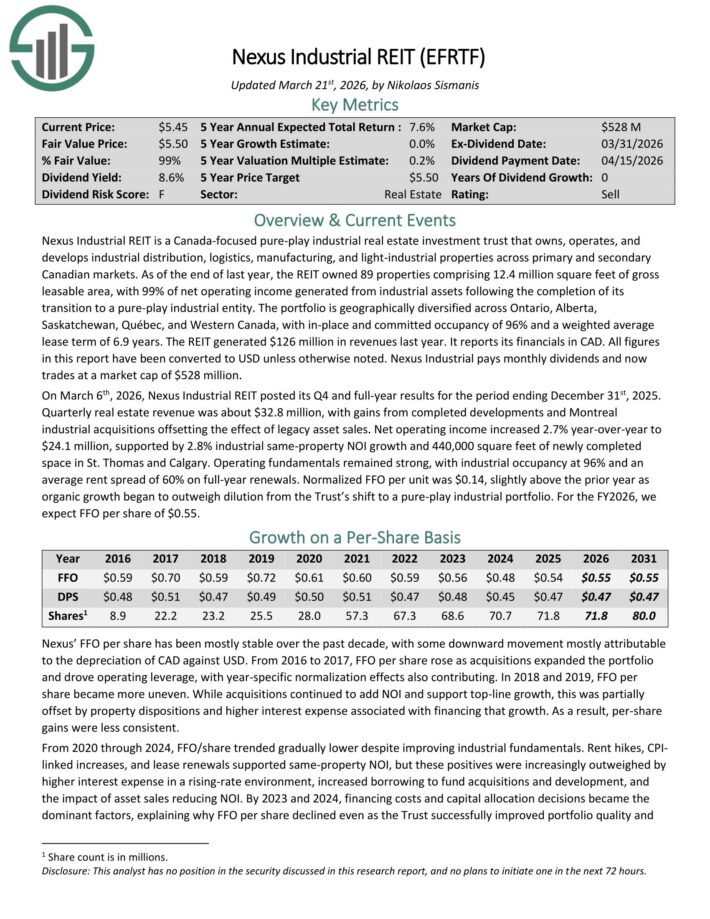

High-Yield REIT No. 10: Nexus Industrial REIT (EFRTF)

- Dividend Yield: 8.2%

Nexus Industrial REIT is a Canada-focused industrial real estate investment trust that owns, operates, and develops industrial distribution, logistics, manufacturing, and light-industrial properties across primary and secondary Canadian markets.

As of the end of last year, the REIT owned 89 properties comprising 12.4 million square feet of gross leasable area, with 99% of net operating income generated from industrial assets following the completion of its transition to a pure-play industrial entity.

The portfolio is geographically diversified across Ontario, Alberta, Saskatchewan, Québec, and Western Canada, with in-place and committed occupancy of 96% and a weighted average lease term of 6.9 years.

The REIT generated $126 million in revenue last year.

On March 6th, 2026, Nexus Industrial REIT posted its Q4 and full-year results. Quarterly real estate revenue was about $32.8 million, with gains from completed developments and Montreal industrial acquisitions offsetting the effect of legacy asset sales.

Net operating income increased 2.7% year-over-year to $24.1 million, supported by 2.8% industrial same-property NOI growth and 440,000 square feet of newly completed space in St. Thomas and Calgary.

Operating fundamentals remained strong, with industrial occupancy at 96% and an average rent spread of 60% on full-year renewals.

Normalized FFO per unit was $0.14, slightly above the prior year as organic growth began to outweigh dilution from the Trust’s shift to a pure-play industrial portfolio.

Click here to download our most recent Sure Analysis report on EFRTF (preview of page 1 of 3 shown below):

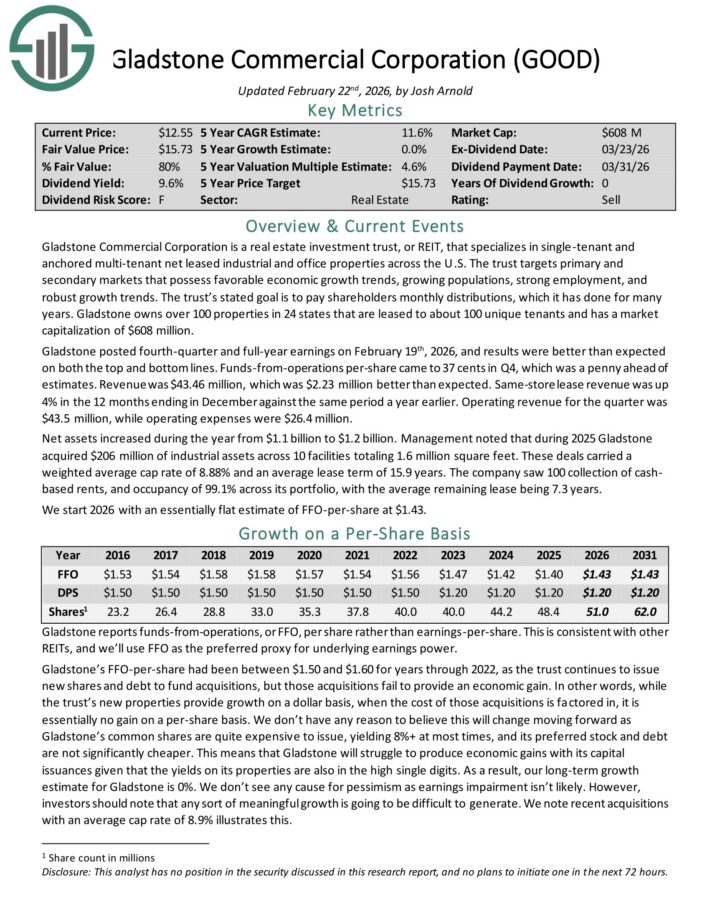

High-Yield REIT No. 9: Gladstone Commercial Corp. (GOOD)

- Dividend Yield: 9.5%

Gladstone Commercial Corporation is a real estate investment trust, or REIT, that specializes in single-tenant and anchored multi-tenant net leased industrial and office properties across the U.S.

The trust targets primary and secondary markets that possess favorable economic growth trends, growing populations, strong employment, and robust growth trends.

The trust’s stated goal is to pay shareholders monthly distributions, which it has done for more than 17 consecutive years. Gladstone owns over 100 properties in 24 states that are leased to about 100 unique tenants.

Gladstone posted fourth-quarter and full-year earnings on February 19th, 2026, and results were better than expected on both the top and bottom lines.

Funds-from-operations per-share came to 37 cents in Q4, which was a penny ahead of estimates. Revenue was $43.46 million, which was $2.23 million better than expected.

Same-store lease revenue was up 4% in the 12 months ending in December against the same period a year earlier. Operating revenue for the quarter was $43.5 million, while operating expenses were $26.4 million.

Net assets increased during the year from $1.1 billion to $1.2 billion. Management noted that during 2025 Gladstone acquired $206 million of industrial assets across 10 facilities totaling 1.6 million square feet.

These deals carried a weighted average cap rate of 8.88% and an average lease term of 15.9 years.

Click here to download our most recent Sure Analysis report on GOOD (preview of page 1 of 3 shown below):

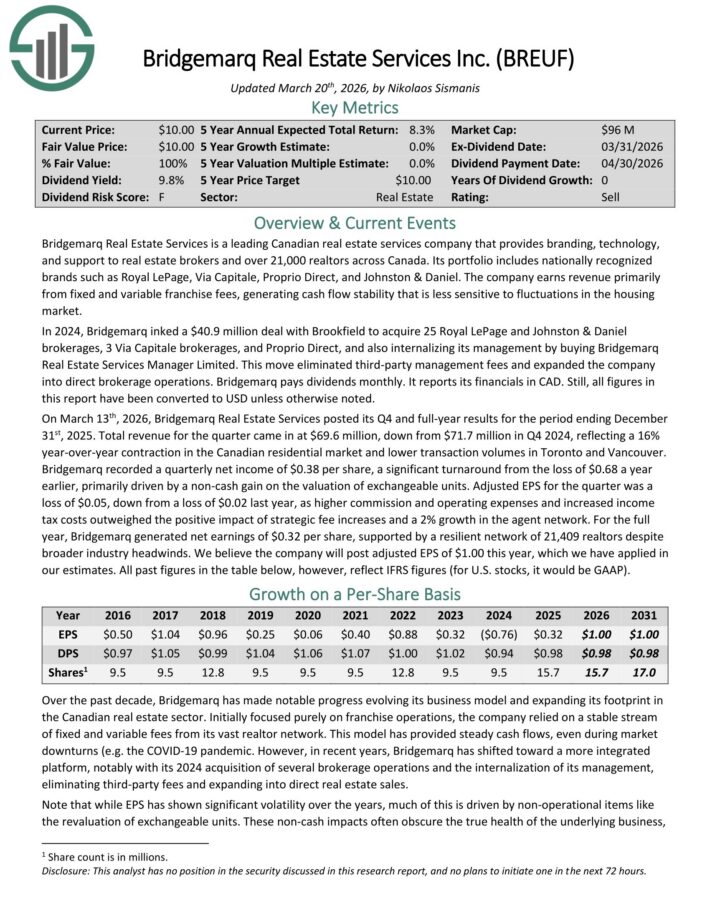

High-Yield REIT No. 8: Bridgemarq Real Estate Services (BREUF)

- Dividend Yield: 10.4%

Bridgemarq Real Estate Services is a leading Canadian real estate services company that provides branding, technology, and support to real estate brokers and over 21,000 realtors across Canada.

Its portfolio includes nationally recognized brands such as Royal LePage, Via Capitale, Proprio Direct, and Johnston & Daniel.

The company earns revenue primarily from fixed and variable franchise fees, generating cash flow stability that is less sensitive to fluctuations in the housing market.

On March 13th, 2026, Bridgemarq Real Estate Services posted its Q4 and full-year results. Total revenue for the quarter came in at $69.6 million, down from $71.7 million in Q4 2024, reflecting a 16% year-over-year contraction in the Canadian residential market and lower transaction volumes in Toronto and Vancouver.

Bridgemarq recorded a quarterly net income of $0.38 per share, a significant turnaround from the loss of $0.68 a year earlier, primarily driven by a non-cash gain on the valuation of exchangeable units.

Adjusted EPS for the quarter was a loss of $0.05, down from a loss of $0.02 last year, as higher commission and operating expenses and increased income tax costs outweighed the positive impact of strategic fee increases and a 2% growth in the agent network.

For the full year, Bridgemarq generated net earnings of $0.32 per share, supported by a resilient network of 21,409 realtors.

Click here to download our most recent Sure Analysis report on BREUF (preview of page 1 of 3 shown below):

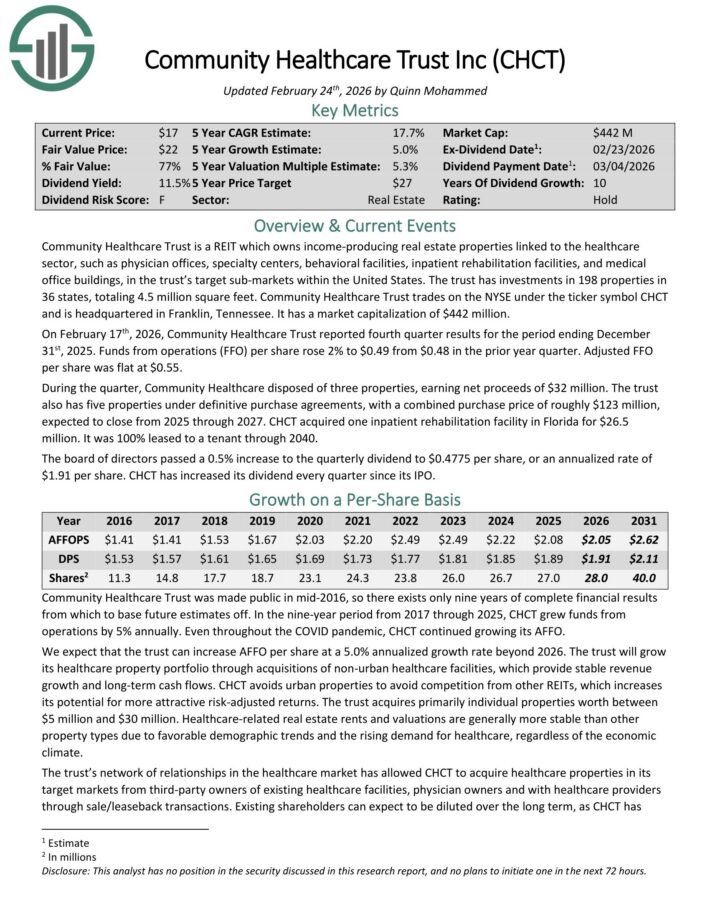

High-Yield REIT No. 7: Community Healthcare Trust (CHCT)

- Dividend Yield: 11.0%

Community Healthcare Trust is a REIT which owns income-producing real estate properties linked to the healthcare sector, such as physician offices, specialty centers, behavioral facilities, inpatient rehabilitation facilities, and medical office buildings, in the trust’s target sub-markets within the United States.

The trust has investments in 200 properties in 36 states, totaling 4.6 million square feet.

On February 17th, 2026, Community Healthcare Trust reported fourth quarter results for the period ending December 31st, 2025. Funds from operations (FFO) per share rose 2% to $0.49 from $0.48 in the prior year quarter. Adjusted FFO per share was flat at $0.55.

During the quarter, Community Healthcare disposed of three properties, earning net proceeds of $32 million. The trust also has five properties under definitive purchase agreements, with a combined purchase price of roughly $123 million, expected to close from 2025 through 2027.

CHCT acquired one inpatient rehabilitation facility in Florida for $26.5 million. It was 100% leased to a tenant through 2040.

The board of directors passed a 0.5% increase to the quarterly dividend to $0.4775 per share, or an annualized rate of $1.91 per share. CHCT has increased its dividend every quarter since its IPO.

Click here to download our most recent Sure Analysis report on CHCT (preview of page 1 of 3 shown below):

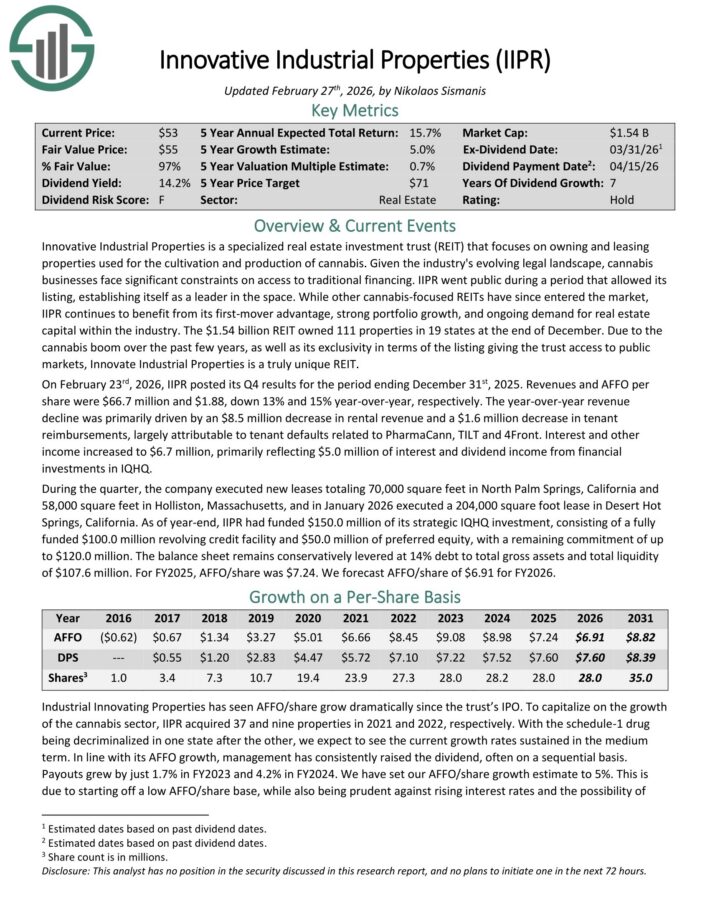

High-Yield REIT No. 6: Innovative Industrial Properties (IIPR)

- Dividend Yield: 13.3%

Innovative Industrial Properties, Inc. is a single-use “specialty REIT” that exclusively focuses on owning properties used for the cultivation and production of cannabis.

The REIT owned 112 properties in 19 states at the end of June. Due to the cannabis boom over the past few years, as well as its exclusivity in terms of the listing giving the trust access to public markets, Innovate Industrial Properties is a truly unique REIT.

On February 23rd, 2026, IIPR posted its Q4 results for the period ending December 31st, 2025. Revenues and AFFO per share were $66.7 million and $1.88, down 13% and 15% year-over-year, respectively.

The year-over-year revenue decline was primarily driven by an $8.5 million decrease in rental revenue and a $1.6 million decrease in tenant reimbursements, largely attributable to tenant defaults related to PharmaCann, TILT and 4Front.

Interest and other income increased to $6.7 million, primarily reflecting $5.0 million of interest and dividend income from financial investments in IQHQ.

During the quarter, the company executed new leases totaling 70,000 square feet in North Palm Springs, California and 58,000 square feet in Holliston, Massachusetts, and in January 2026 executed a 204,000 square foot lease in Desert Hot Springs, California.

Click here to download our most recent Sure Analysis report on IIPR (preview of page 1 of 3 shown below):

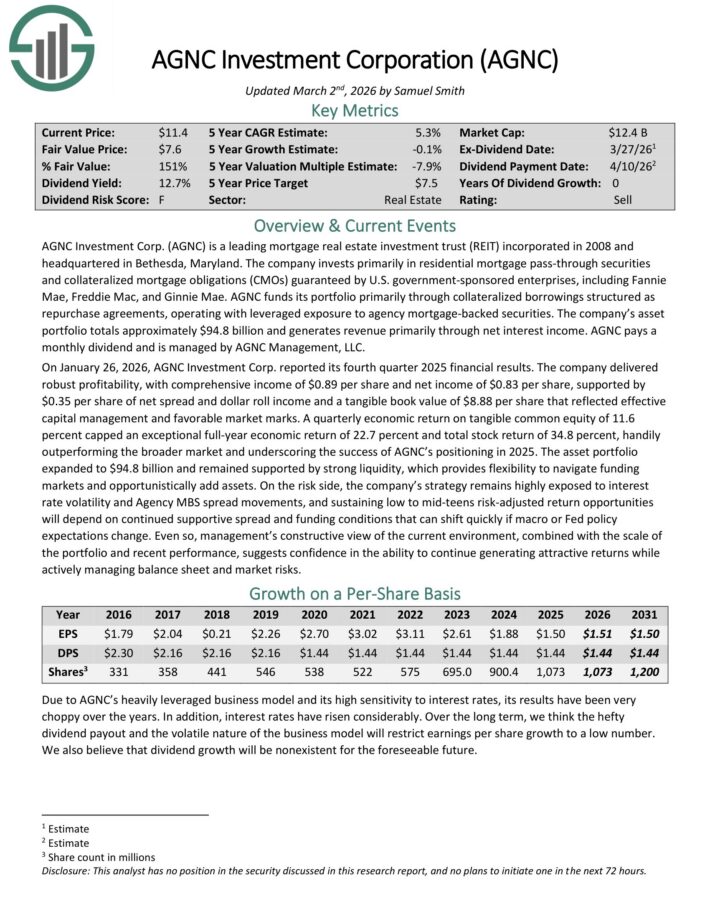

High-Yield REIT No. 5: AGNC Investment Corp. (AGNC)

- Dividend Yield: 14.1%

American Capital Agency Corp is a mortgage real estate investment trust that invests primarily in agency mortgage–backed securities (or MBS) on a leveraged basis.

The firm’s asset portfolio is comprised of residential mortgage pass–through securities, collateralized mortgage obligations (or CMO), and non–agency MBS. Many of these are guaranteed by government–sponsored enterprises.

On January 26, 2026, AGNC Investment Corp. reported its fourth quarter 2025 financial results. The company delivered robust profitability, with comprehensive income of $0.89 per share and net income of $0.83 per share, supported by $0.35 per share of net spread and dollar roll income and a tangible book value of $8.88 per share that reflected effective capital management and favorable market marks.

A quarterly economic return on tangible common equity of 11.6% capped an exceptional full-year economic return of 22.7% and total stock return of 34.8%, handily outperforming the broader market and underscoring the success of AGNC’s positioning in 2025.

Click here to download our most recent Sure Analysis report on AGNC Investment Corp (AGNC) (preview of page 1 of 3 shown below):

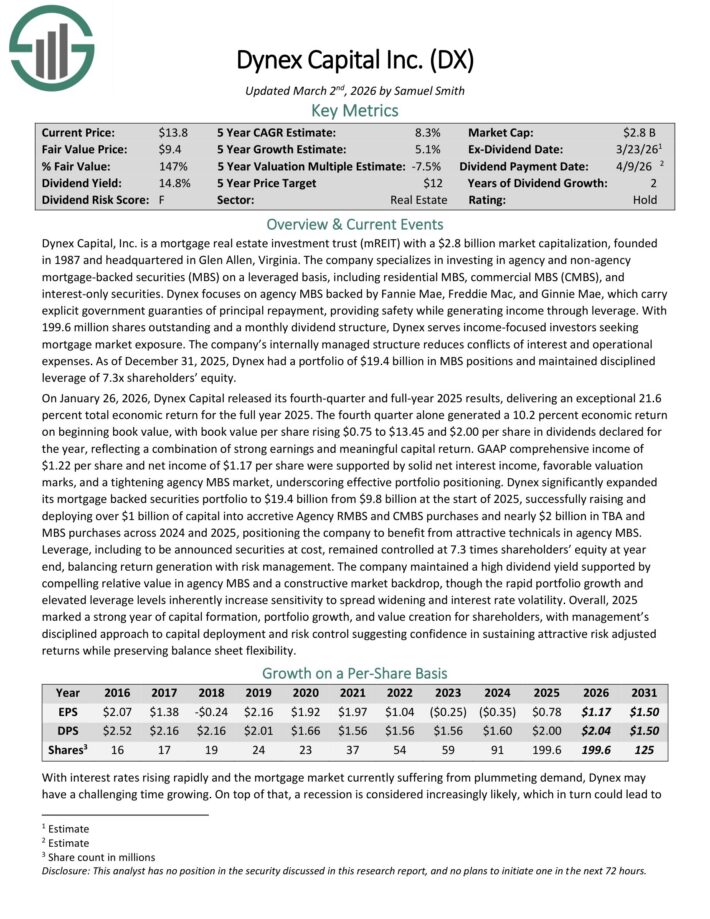

High-Yield REIT No. 4: Dynex Capital (DX)

- Dividend Yield: 15.9%

Dynex Capital invests in mortgage–backed securities (MBS) on a leveraged basis in the United States. It invests in agency and non–agency MBS consisting of residential MBS, commercial MBS (CMBS), and CMBS interest–only securities.

On January 26, 2026, Dynex Capital released its fourth-quarter and full-year 2025 results, delivering an exceptional 21.6% total economic return for the full year 2025.

The fourth quarter alone generated a 10.2% economic return on beginning book value, with book value per share rising $0.75 to $13.45 and $2.00 per share in dividends declared for the year, reflecting a combination of strong earnings and meaningful capital return.

GAAP comprehensive income of $1.22 per share and net income of $1.17 per share were supported by solid net interest income, favorable valuation marks, and a tightening agency MBS market, underscoring effective portfolio positioning.

Click here to download our most recent Sure Analysis report on DX (preview of page 1 of 3 shown below):

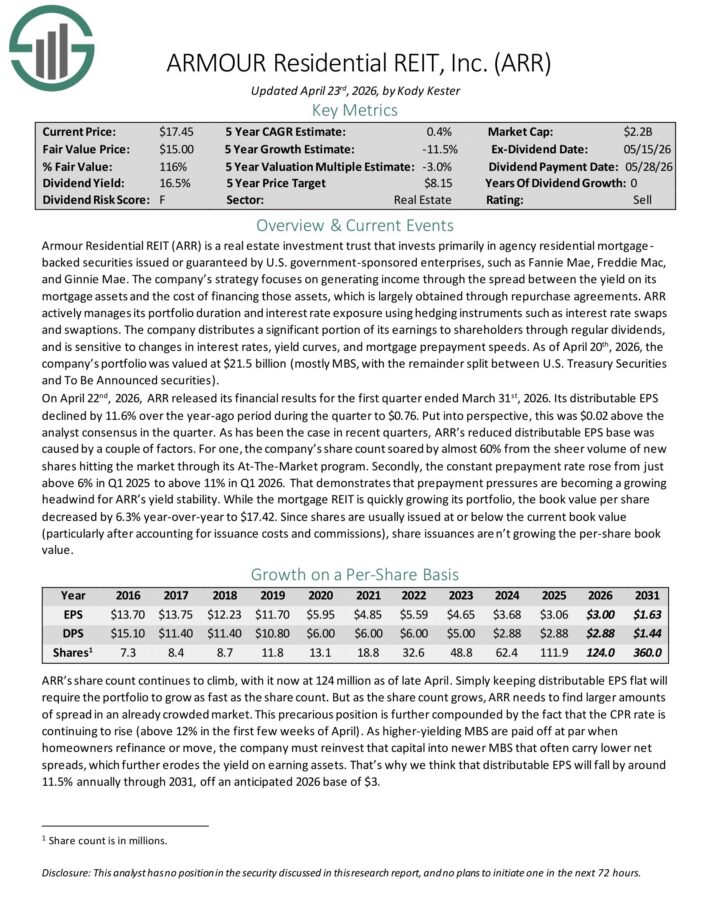

High-Yield REIT No. 3: ARMOUR Residential REIT (ARR)

- Dividend Yield: 16.7%

ARMOUR Residential invests in residential mortgage-backed securities that include U.S. Government-sponsored entities (GSE) such as Fannie Mae and Freddie Mac.

It also includes Ginnie Mae, the Government National Mortgage Administration’s issued or guaranteed securities backed by fixed-rate, hybrid adjustable-rate, and adjustable-rate home loans.

Unsecured notes and bonds issued by the GSE and the US Treasury, money market instruments, and non-GSE or government agency-backed securities are examples of other types of investments.

On April 22nd, 2026, ARR released its financial results for the first quarter ended March 31st, 2026. Its distributable EPS declined by 11.6% over the year-ago period during the quarter to $0.76. This was $0.02 above the analyst consensus in the quarter.

The reduced distributable EPS base was caused by a couple of factors. For one, the company’s share count soared by almost 60% from the sheer volume of new shares hitting the market through its At-The-Market program.

Secondly, the constant prepayment rate rose from just above 6% in Q1 2025 to above 11% in Q1 2026.

Book value per share decreased by 6.3% year-over-year to $17.42.

Click here to download our most recent Sure Analysis report on ARMOUR Residential REIT Inc (ARR) (preview of page 1 of 3 shown below):

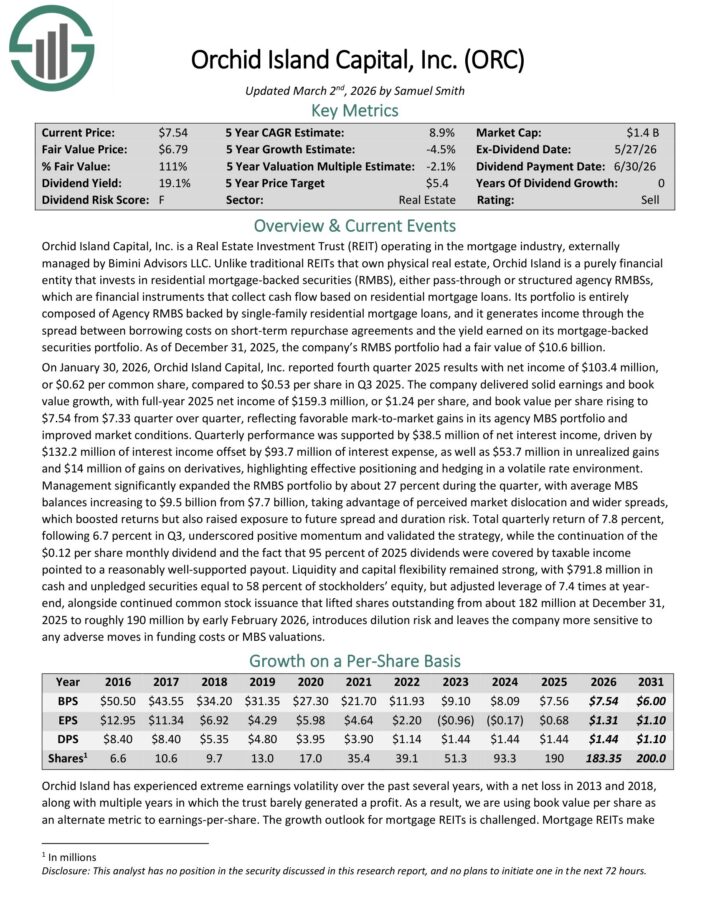

High-Yield REIT No. 2: Orchid Island Capital Inc (ORC)

- Dividend Yield: 17.9%

Orchid Island Capital, Inc. is a Real Estate Investment Trust (REIT) operating in the mortgage industry, externally managed by Bimini Advisors LLC.

Orchid Island is a purely financial entity that invests in residential mortgage-backed securities (RMBS), either pass-through or structured agency RMBSs, which are financial instruments that collect cash flow based on residential mortgage loans.

Its portfolio is entirely composed of Agency RMBS backed by single-family residential mortgage loans.

On January 30, 2026, Orchid Island Capital, Inc. reported fourth quarter 2025 results with net income of $103.4 million, or $0.62 per common share, compared to $0.53 per share in Q3 2025.

The company delivered solid earnings and book value growth, with full-year 2025 net income of $159.3 million, or $1.24 per share, and book value per share rising to $7.54 from $7.33 quarter over quarter, reflecting favorable mark-to-market gains in its agency MBS portfolio and improved market conditions.

Quarterly performance was supported by $38.5 million of net interest income, driven by $132.2 million of interest income offset by $93.7 million of interest expense, as well as $53.7 million in unrealized gains and $14 million of gains on derivatives, highlighting effective positioning and hedging in a volatile rate environment.

Management significantly expanded the RMBS portfolio by about 27 percent during the quarter, with average MBS balances increasing to $9.5 billion from $7.7 billion, taking advantage of perceived market dislocation and wider spreads, which boosted returns but also raised exposure to future spread and duration risk.

Click here to download our most recent Sure Analysis report on ORC (preview of page 1 of 3 shown below):

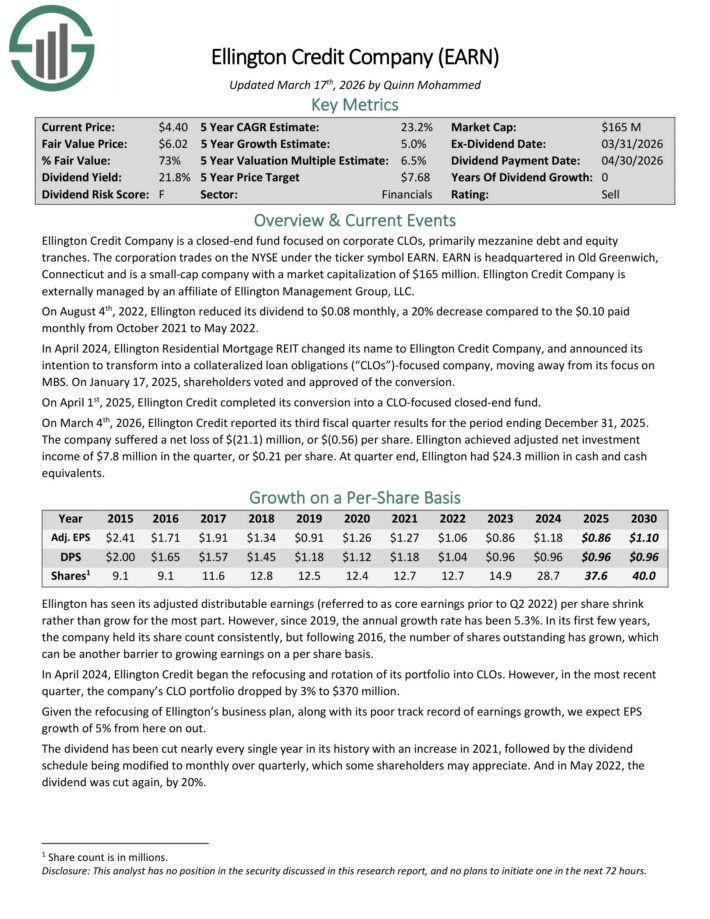

High-Yield REIT No. 1: Ellington Credit Co. (EARN)

- Dividend Yield: 20.9%

Ellington Credit Co. acquires, invests in, and manages residential mortgage and real estate related assets.

Ellington focuses primarily on residential mortgage-backed securities, specifically those backed by a U.S. Government agency or U.S. government–sponsored enterprise.

Agency MBS are created and backed by government agencies or enterprises, while non-agency MBS are not guaranteed by the government.

On March 4th, 2026, Ellington Credit reported its third fiscal quarter results for the period ending December 31, 2025. The company suffered a net loss of $(21.1) million, or $(0.56) per share.

Ellington achieved adjusted net investment income of $7.8 million in the quarter, or $0.21 per share. At quarter end, Ellington had $24.3 million in cash and cash equivalents.

Click here to download our most recent Sure Analysis report on EARN (preview of page 1 of 3 shown below):

Final Thoughts

REITs have significant appeal for income investors due to their high yields.

These 10 extremely high-yielding REITs are especially attractive on the surface, although investors should be aware that abnormally high yields are often accompanied by elevated risks.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Monthly Dividend Stocks: Individual securities that pay out every month