Updated on Febuaury 11th, 2026 by Felix Martinez

In the realm of dividend investing, the Dividend Aristocrats are the crème de la crème. The Dividend Aristocrats are stocks in the S&P 500 Index that have 25+ consecutive years of dividend increases.

Achieving Dividend Aristocrat status is rare; only 69 companies currently hold this distinction.

The Dividend Aristocrats list is highly selective. With that in mind, we’ve compiled a downloadable list of all 69 Dividend Aristocrats, including key metrics such as dividend yields and price-to-earnings ratios.

You can download a free copy of the Dividend Aristocrats list by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

While there are countless options for dividend stocks, the Dividend Aristocrats are in a league of their own. These companies have a track record of financial stability and consistent cash flow, and are positioned to grow their profits over time. This makes them resilient during economic downturns and able to consistently raise their dividends each year.

C.H. Robinson Worldwide, Inc. (CHRW) is a recent addition to the Index. The company recently announced its 27th consecutive annual dividend increase and currently offers a 1.3% yield.

Despite the transportation industry being cyclical, C.H. Robinson Worldwide’s mission-critical logistics solutions have enabled it to deliver resilient results over the years and support consistent dividend increases. Therefore, C.H. Robinson could be a fitting stock for income-oriented investors.

Business Overview

C.H. Robinson Worldwide is a transportation and logistics giant that has been around since the early 1900s. Founded by Charles Henry Robinson, the company has grown into a Fortune 500 provider of multimodal transportation and third-party logistics services.

CHRW offers a wide range of services to help its clients move their goods, including freight transportation, transportation management, brokerage, and warehousing. Whether by truckload, air freight, intermodal, or ocean transportation, the company has the expertise to do the job.

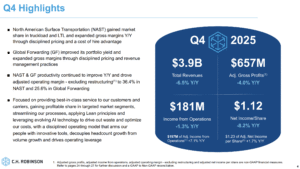

On January 28th, 2026, C.H. Robinson Worldwide reported Q4 2025 adjusted EPS of $1.23, beating expectations by $0.10, despite revenue declining 6.5% year over year to $3.9 billion. GAAP EPS fell to $1.12 (-8.2% YoY) as weak global freight demand, lower ocean rates, and higher spot trucking costs pressured results.

Even so, the company delivered market share gains, with NAST total volume up ~1% and truckload volume up ~3%, significantly outperforming the 7.6% decline in the Cass Freight Shipment Index. Adjusted operating income rose 7.1% to $197.4 million, and adjusted operating margin expanded 80 basis points to 27.6%, reflecting cost discipline and productivity gains.

Cash generation remained strong, with operating cash flow up $37.5 million to $305.4 million, enabling $207.7 million returned to shareholders during the quarter, up 151% year over year. For full-year 2025, adjusted EPS increased 12.9% to $5.09, operating income rose 18.8% to $795 million, and adjusted operating margin expanded 490 basis points to 29.1%, driven by lower costs and Lean AI-led productivity improvements.

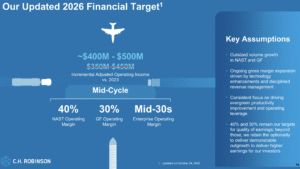

Management expects continued margin strength in 2026, supported by automation, disciplined revenue management, and capital spending of $75–$85 million, positioning CHRW to outperform when freight markets recover.

Source: Investor Presentation

Growth Prospects

C.H. Robinson has grown revenue by 3.1% annually over the past 10 years. Earnings per share have increased by 2.3% over the past five years. We expect annual earnings growth of 5% over the next five years, supported by the newly acquired Prime Distribution Services.

C.H. Robinson adds significant value to its customers through its efficient Freight & Logistics brokerage services, which are gradually capturing a larger share of the U.S. freight market. In fact, as the industry has been shifting from asset-based trucking to brokers such as C.H. Robinson, brokerage penetration over the past two decades has nearly quadrupled.

Another growth driver for the company is its digital transformation, which should further scale its operations. This includes C.H. Robinson providing meaningful products, features, and insights to both sides of the two-sided freight marketplace, resulting in unique information advantages for its customers.

Finally, C.H. Robinson should continue leveraging its scale to capitalize on the growing freight market and expand its unique global footprint. For fiscal 2026, we expect earnings per share of about $6.10, up 20% from 2025.

Source: Investor Presentation

Competitive Advantages & Recession Performance

The integrated Freight & Logistics sector can be cyclical, leading to fluctuating results for companies in the space, as transportation demand varies with underlying economic conditions. That said, as the industry’s preferred partner, C.H. Robinson has delivered resilient results over the decades.

When it comes to competition, C.H. Robinson is in a league of its own. The company has built a network that is second to none, thanks to its efficiency and effectiveness. But what really sets it apart is the massive barrier to entry that new or small competitors would face.

Building a network that can rival C.H. Robinson’s would require significant capital, which not many companies have. In other words, C.H. Robinson has a wide economic moat that makes it difficult for competitors to compete. This is why they are considered one of the best in the industry.

C.H. Robinson’s ability to continue growing its earnings even under adverse economic conditions was greatly illustrated during the Great Financial Crisis:

- 2007 earnings-per-share of $1.90

- 2008 earnings-per-share of $2.12 (11.8% decline)

- 2009 earnings-per-share of $2.15 (2.4% decline)

- 2010 earnings-per-share of $2.35 (9.4% increase)

In fact, it has an unbroken streak of profitability dating back to 1996 and has never posted a loss in any quarter since. This is a remarkable achievement and a testament to the robustness of its business model.

Valuation & Expected Returns

We expect that C.H. Robinson is expected to earn $6.10 per share in the fiscal year 2026. The stock has a price-to-earnings ratio of 32.1. This is significantly above our fair value P/E estimate of 15.0. A declining price-to-earnings ratio could reduce annual returns by 8.0% over the next five years.

In addition, C.H. Robinson has a 2.6% dividend yield, and the dividend payout appears well covered by earnings. A breakdown of potential returns is as follows:

- 5.0% earnings-per-share growth

- 1.3% dividend yield

- -8.0% valuation headwind

In total, we believe C.H. Robinson could produce negative annual returns of 1.7% over the next five years.

Final Thoughts

C.H. Robinson has delivered an excellent track record of growth, consistent profitability, and rising dividends for many years, but the company is seeing declines following record results during the pandemic.

The stock has a dividend yield above 1.3% and a long history of annual dividend increases. That said, dividend growth is likely to increase, given the company expected earnings grwoth.

In addition, shares appear significantly overvalued given the company’s reduced earnings power. We forecast that C.H. Robinson stock will deliver negative annual returns, making it a sell in our view.

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

- The High Yield Dividend Aristocrats List is comprised of the 20 Dividend Aristocrats with the highest current yields.

- The Dividend Achievers List is comprised of ~350 stocks with 10+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500.