Updated on June 16th, 2026 by Bob Ciura

The Dividend Kings are the best-of-the-best in dividend longevity.

What is a Dividend King? A stock with 50 or more consecutive years of dividend increases.

The downloadable Dividend Kings Spreadsheet List below contains the following for each stock in the index among other important investing metrics:

- Payout ratio

- Dividend yield

- Price-to-earnings ratio

You can see the full downloadable spreadsheet of all 58 Dividend Kings (along with important financial metrics such as dividend yields, payout ratios, and price-to-earnings ratios) by clicking on the link below:

We typically rank stocks based on their five-year expected annual returns, as stated in the Sure Analysis Research Database.

But for investors primarily interested in income, it is also useful to rank the Dividend Kings according to their dividend yields.

This article will rank the 20 highest-yielding Dividend Kings today.

Table of Contents

- High Yield Dividend King #20: H2O America (HTO)

- High Yield Dividend King #19: AbbVie Inc. (ABBV)

- High Yield Dividend King #18: Fortis Inc. (FTS)

- High-Yield Dividend King #17: Consolidated Edison (ED)

- High-Yield Dividend King #16: United Bankshares (UBSI)

- High-Yield Dividend King #15: Target Corporation (TGT)

- High-Yield Dividend King #14: Federal Realty Investment Trust (FRT)

- High-Yield Dividend King #13: Canadian Utilities (CDUAF)

- High-Yield Dividend King #12: The Marzetti Company (MZTI)

- High-Yield Dividend King #11: Black Hills Corp. (BKH)

- High-Yield Dividend King #10: Northwest Natural Holding Co. (NWN)

- High-Yield Dividend King #9: Stanley Black & Decker (SWK)

- High-Yield Dividend King #8: Genuine Parts Co. (GPC)

- High-Yield Dividend King #7: PepsiCo Inc. (PEP)

- High-Yield Dividend King #6: Sonoco Products (SON)

- High-Yield Dividend King #5: Kenvue Inc. (KVUE)

- High-Yield Dividend King #4: Hormel Foods (HRL)

- High-Yield Dividend King #3: Kimberly-Clark Corp. (KMB)

- High-Yield Dividend King #2: Altria Group (MO)

- High-Yield Dividend King #1: Universal Corp. (UVV)

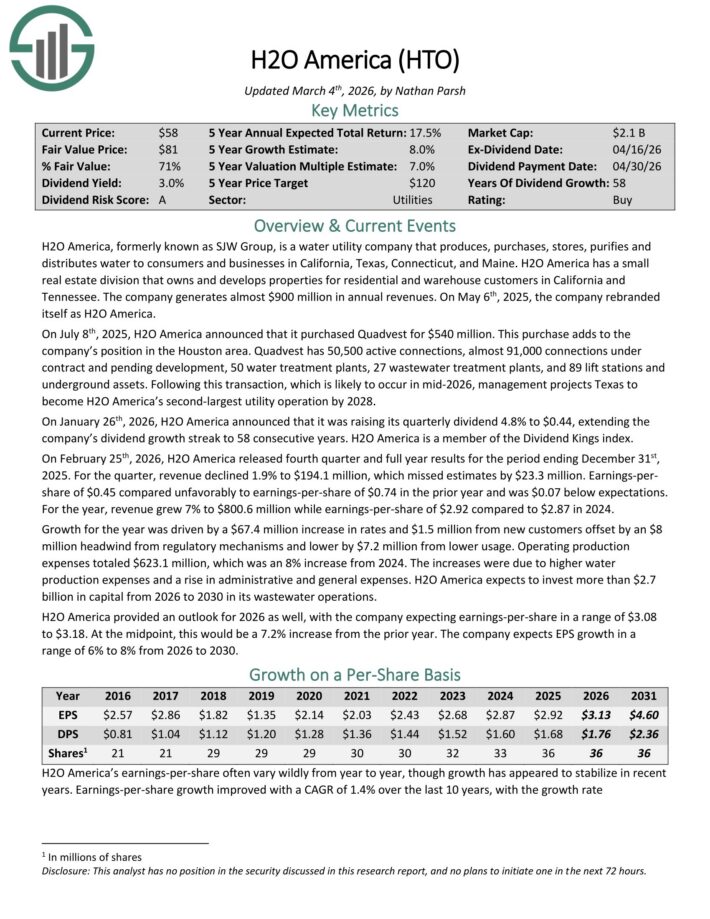

High Yield Dividend King #20: H2O America (HTO)

- Dividend Yield: 3.1%

H2O America, formerly known as SJW Group, is a water utility company that produces, purchases, stores, purifies and distributes water to consumers and businesses in the Silicon Valley area of California, the area north of San Antonio, Texas, Connecticut, and Maine.

It also has a small real estate division that owns and develops properties for residential and warehouse customers in California and Tennessee. The company generates about $670 million in annual revenues.

On January 26th, 2026, H2O America raised its quarterly dividend 4.8% to $0.44, extending the company’s dividend growth streak to 58 consecutive years.

On February 25th, 2026, H2O America released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue declined 1.9% to $194.1 million, which missed estimates by $23.3 million.

Earnings-per-share of $0.45 compared unfavorably to earnings-per-share of $0.74 in the prior year and was $0.07 below expectations.

For the year, revenue grew 7% to $800.6 million while earnings-per-share of $2.92 compared to $2.87 in 2024.

Growth for the year was driven by a $67.4 million increase in rates and $1.5 million from new customers offset by an $8 million headwind from regulatory mechanisms and lower by $7.2 million from lower usage.

H2O America provided an outlook for 2026 as well, with the company expecting earnings-per-share in a range of $3.08 to $3.18. At the midpoint, this would be a 7.2% increase from the prior year.

Click here to download our most recent Sure Analysis report on HTO (preview of page 1 of 3 shown below):

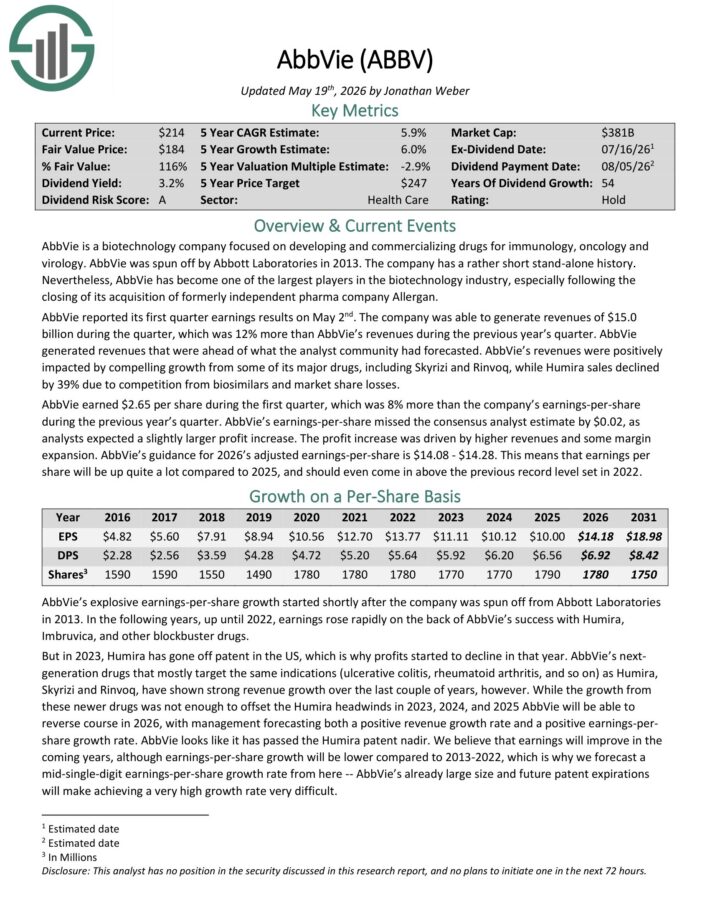

High Yield Dividend King #19: AbbVie Inc. (ABBV)

- Dividend Yield: 3.1%

AbbVie is a biotechnology company focused on developing and commercializing drugs for immunology, oncology and

virology. AbbVie was spun off by Abbott Laboratories in 2013.

AbbVie reported its first quarter earnings results on May 2nd. The company generated revenue of $15.0 billion during the quarter, which was 12% more than AbbVie’s revenues during the previous year’s quarter.

Revenue was positively impacted by compelling growth from some of its major drugs, including Skyrizi and Rinvoq, while Humira sales declined by 39% due to competition from biosimilars and market share losses.

AbbVie earned $2.65 per share during the first quarter, which was 8% more than the company’s earnings-per-share during the previous year’s quarter.

Earnings-per-share missed the consensus analyst estimate by $0.02, as analysts expected a slightly larger profit increase.

The profit increase was driven by higher revenues and some margin expansion. AbbVie’s guidance for 2026’s adjusted earnings-per-share is $14.08 – $14.28.

Click here to download our most recent Sure Analysis report on ABBV (preview of page 1 of 3 shown below):

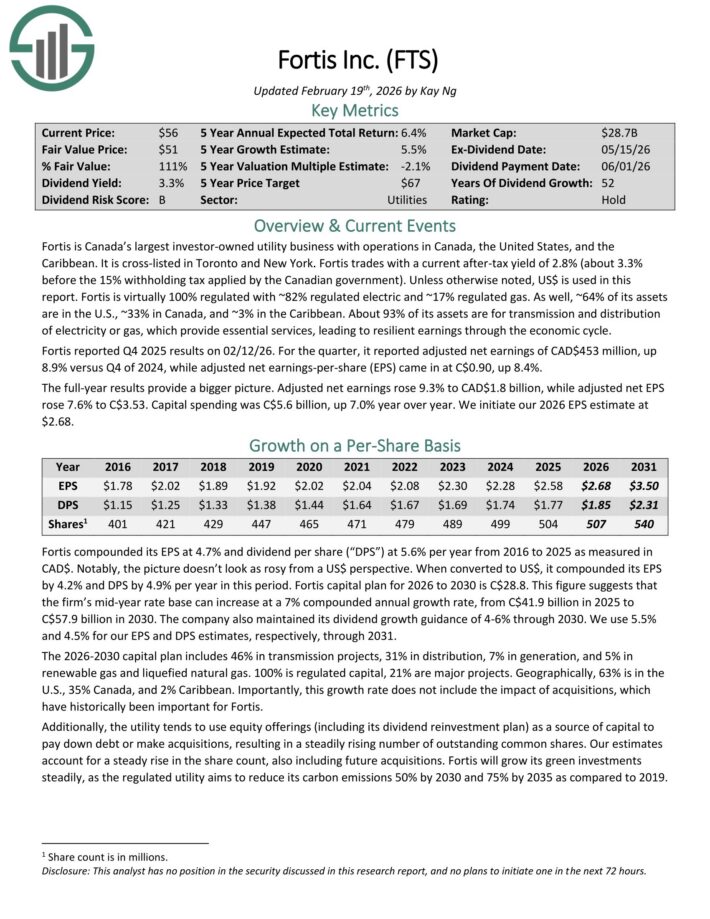

High Yield Dividend King #18: Fortis (FTS)

- Dividend Yield: 3.2%

Fortis is Canada’s largest investor-owned utility business with operations in Canada, the United States, and the Caribbean. It is cross-listed in Toronto and New York.

Fortis trades with a current after-tax yield of 3.0% (about 3.5% before the 15% withholding tax applied by the Canadian government).

Fortis is virtually 100% regulated with ~82% regulated electric and ~17% regulated gas. As well, ~64% of its assets are in the U.S., ~33% in Canada, and ~3% in the Caribbean.

About 93% of its assets are for transmission and distribution of electricity or gas, which provide essential services, leading to resilient earnings through the economic cycle.

Fortis reported Q3 2025 results on 11/04/25. For the quarter, its reported adjusted net earnings of CAD$441 million, up 5.0% versus Q3 2024, while adjusted net earnings-per-share (EPS) came in at C$0.87, up 2.4%.

The utility raised its quarterly dividend by 4.1% to C$0.64 per share, equating to an annualized payout of C$2.56 per share. It has a new capital investment plan of $28.8 billion for 2026 to 2030.

The year-to-date results provide a bigger picture. Adjusted net earnings rose 9.4% to CAD$1.3 billion, while adjusted net EPS rose 7.3% to C$2.63. Capital spending year to date was C$4.2 billion, while the total capital investment for the year is now expected to be C$5.6 billion.

Click here to download our most recent Sure Analysis report on FTS (preview of page 1 of 3 shown below):

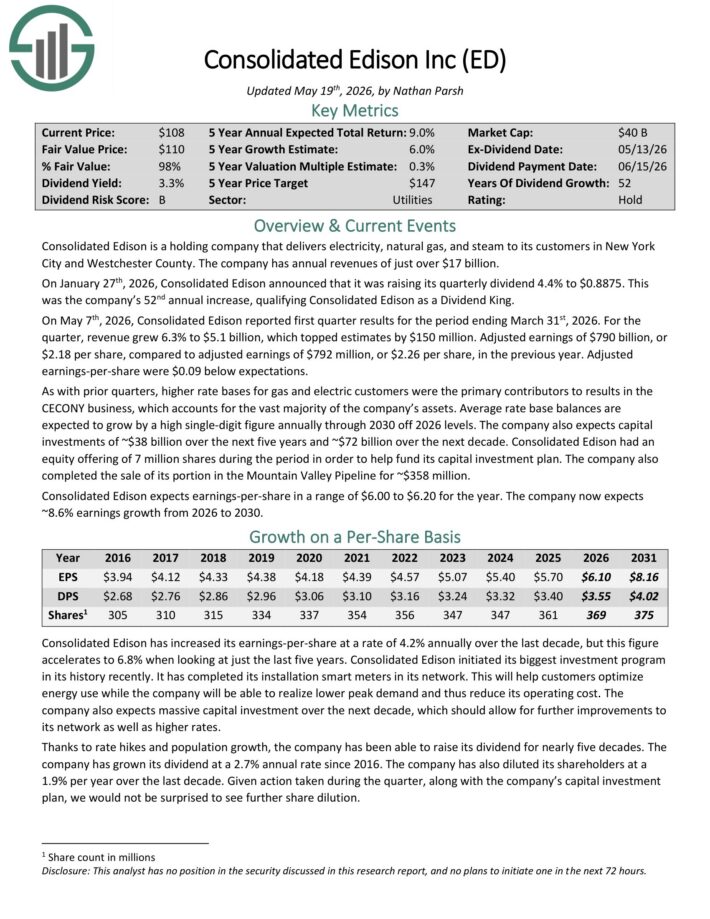

High Yield Dividend King #17: Consolidated Edison (ED)

- Dividend Yield: 3.3%

Consolidated Edison is a holding company that delivers electricity, natural gas, and steam to its customers in New York City and Westchester County. The company has annual revenue of just over $17 billion.

On January 27th, 2026, Consolidated Edison raised its quarterly dividend 4.4% to $0.8875. This was the company’s 52nd annual increase, qualifying Consolidated Edison as a Dividend King.

On May 7th, 2026, Consolidated Edison reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue grew 6.3% to $5.1 billion, which topped estimates by $150 million.

Adjusted earnings of $790 billion, or $2.18 per share, compared to adjusted earnings of $792 million, or $2.26 per share, in the previous year. Adjusted earnings-per-share were $0.09 below expectations.

As with prior quarters, higher rate bases for gas and electric customers were the primary contributors to results in the CECONY business, which accounts for the vast majority of the company’s assets.

Average rate base balances are expected to grow by a high single-digit figure annually through 2030 off 2026 levels. The company also expects capital investments of ~$38 billion over the next five years and ~$72 billion over the next decade.

Consolidated Edison expects earnings-per-share in a range of $6.00 to $6.20 for the year. The company now expects ~8.6% earnings growth from 2026 to 2030.

Click here to download our most recent Sure Analysis report on ED (preview of page 1 of 3 shown below):

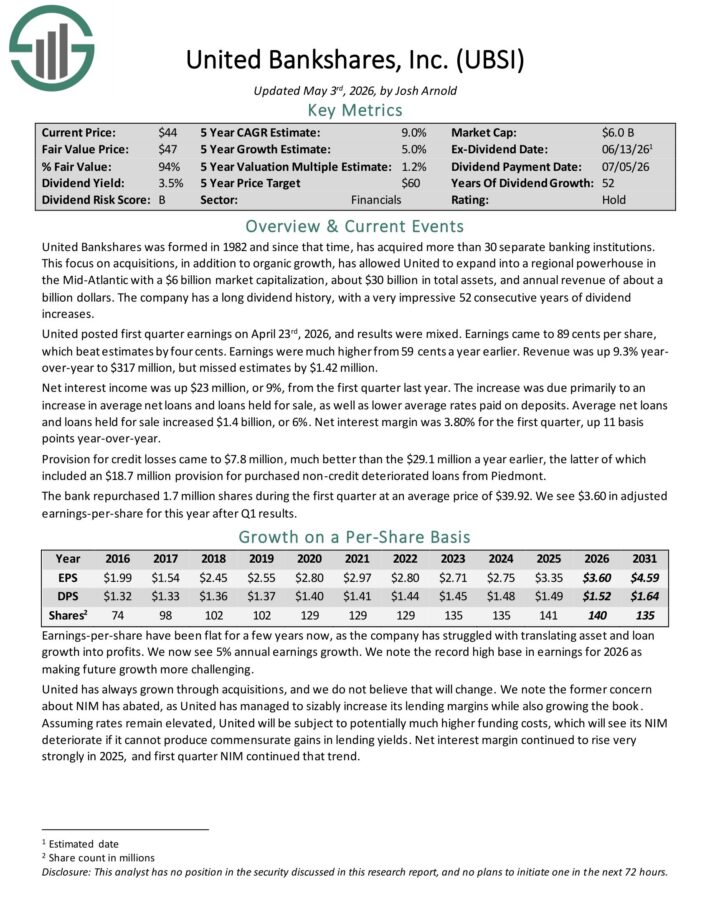

High Yield Dividend King #16: United Bankshares (UBSI)

- Dividend Yield: 3.4%

United Bankshares was formed in 1982 and since that time, has acquired more than 30 separate banking institutions.

This focus on acquisitions, in addition to organic growth, has allowed United to expand into a regional powerhouse in the Mid-Atlantic with about $30 billion in total assets, and annual revenue of about a billion dollars.

The company has a long dividend history, with a very impressive 52 consecutive years of dividend increases.

United posted first quarter earnings on April 23rd, 2026, and results were mixed. Earnings came to 89 cents per share, which beat estimates by four cents.

Earnings were much higher from 59 cents a year earlier. Revenue was up 9.3% year-over-year to $317 million, but missed estimates by $1.42 million.

Net interest income was up $23 million, or 9%, from the first quarter last year. The increase was due primarily to an increase in average net loans and loans held for sale, as well as lower average rates paid on deposits.

Average net loans and loans held for sale increased $1.4 billion, or 6%. Net interest margin was 3.80% for the first quarter, up 11 basis points year-over-year.

Provision for credit losses came to $7.8 million, much better than the $29.1 million a year earlier, the latter of which included an $18.7 million provision for purchased non-credit deteriorated loans from Piedmont.

The bank repurchased 1.7 million shares during the first quarter at an average price of $39.92.

Click here to download our most recent Sure Analysis report on UBSI (preview of page 1 of 3 shown below):

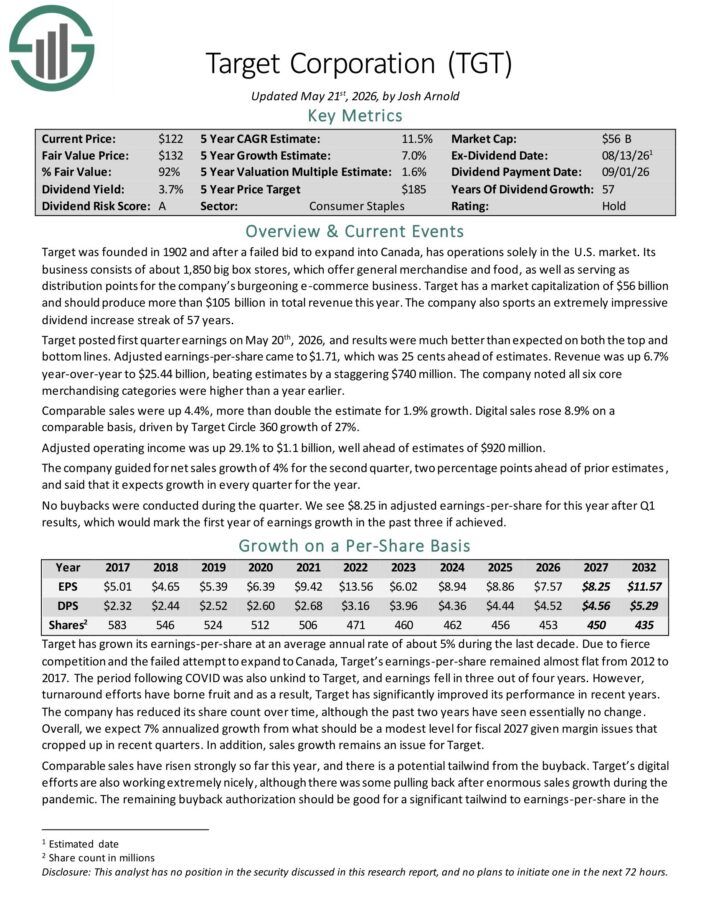

High Yield Dividend King #15: Target Corporation (TGT)

- Dividend Yield: 3.5%

Target was founded in 1902 and has operations solely in the U.S. market.

Its business consists of about 1,850 big box stores, which offer general merchandise and food, as well as serving as distribution points for the company’s burgeoning e-commerce business.

Target should produce more than $105 billion in total revenue this year. The company also sports an extremely impressive dividend increase streak of 57 years.

Target posted first quarter earnings on May 20th, 2026, and results were much better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to $1.71, which was 25 cents ahead of estimates. Revenue was up 6.7% year-over-year to $25.44 billion, beating estimates by a staggering $740 million.

The company noted all six core merchandising categories were higher than a year earlier. Comparable sales were up 4.4%, more than double the estimate for 1.9% growth.

Digital sales rose 8.9% on a comparable basis, driven by Target Circle 360 growth of 27%.

Click here to download our most recent Sure Analysis report on TGT (preview of page 1 of 3 shown below):

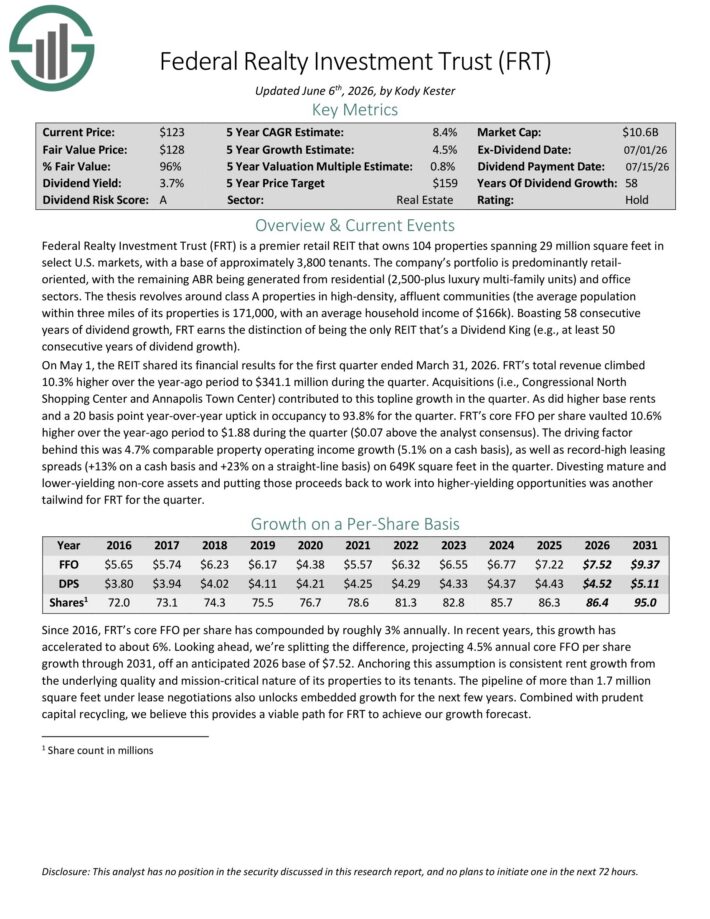

High Yield Dividend King #14: Federal Realty Investment Trust (FRT)

- Dividend Yield: 3.6%

Federal Realty is one of the larger real estate investment trusts (REITs) in the United States. The trust was founded in 1962 and concentrates on high-income, densely populated coastal markets in the US, allowing it to charge more per square foot than its competition.

On May 1, the REIT shared its financial results for the first quarter ended March 31, 2026. FRT’s total revenue climbed 10.3% higher over the year-ago period to $341.1 million during the quarter.

Acquisitions (i.e., Congressional North Shopping Center and Annapolis Town Center) contributed to this top-line growth in the quarter. As did higher base rents and a 20 basis point year-over-year uptick in occupancy to 93.8% for the quarter.

FRT’s core FFO per share vaulted 10.6% higher over the year-ago period to $1.88 during the quarter ($0.07 above the analyst consensus).

The driving factor behind this was 4.7% comparable property operating income growth (5.1% on a cash basis), as well as record-high leasing spreads (+13% on a cash basis and +23% on a straight-line basis) on 649K square feet in the quarter.

Click here to download our most recent Sure Analysis report on FRT (preview of page 1 of 3 shown below):

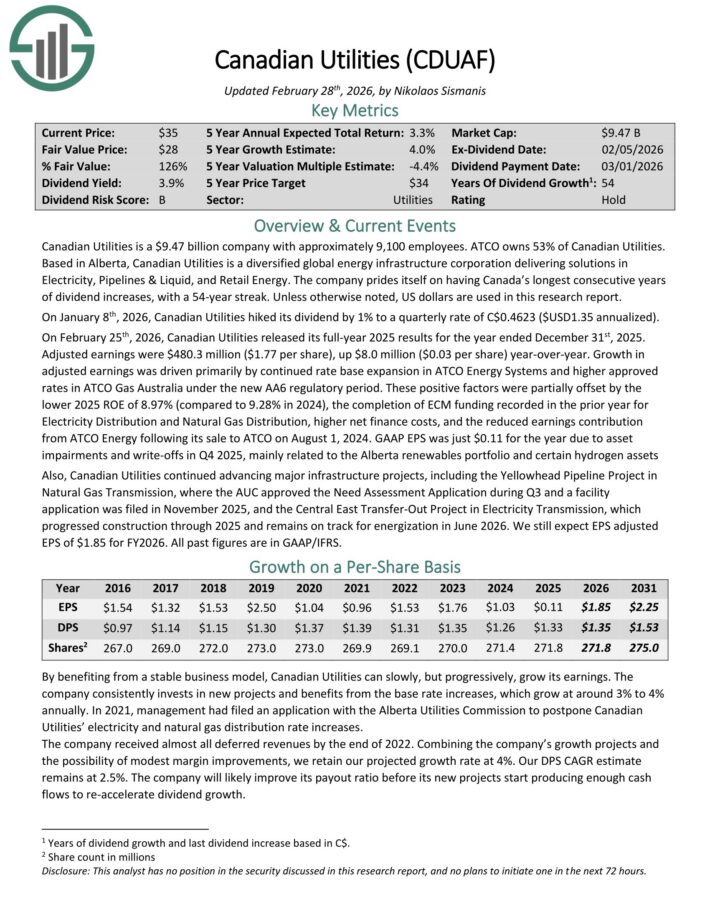

High Yield Dividend King #13: Canadian Utilities (CDUAF)

- Dividend Yield: 3.7%

Canadian Utilities is a $8.14 billion company with approximately 5,000 employees. ATCO owns 53% of Canadian Utilities.

Based in Alberta, Canadian Utilities is a diversified global energy infrastructure corporation delivering solutions in Electricity, Pipelines & Liquid, and Retail Energy.

The company prides itself on having Canada’s longest consecutive years of dividend increases, with a 54-year streak. Unless otherwise noted, US dollars are used in this research report.

On January 8th, 2026, Canadian Utilities hiked its dividend by 1% to a quarterly rate of C$0.4623 ($USD1.35 annualized).

On February 25th, 2026, Canadian Utilities released its full-year 2025 results for the year ended December 31st, 2025. Adjusted earnings were $480.3 million ($1.77 per share), up $8.0 million ($0.03 per share) year-over-year.

Growth in adjusted earnings was driven primarily by continued rate base expansion in ATCO Energy Systems and higher approved rates in ATCO Gas Australia under the new AA6 regulatory period.

These positive factors were partially offset by the lower 2025 ROE of 8.97% (compared to 9.28% in 2024), the completion of ECM funding recorded in the prior year for Electricity Distribution and Natural Gas Distribution, higher net finance costs, and the reduced earnings contribution from ATCO Energy following its sale to ATCO on August 1, 2024.

GAAP EPS was just $0.11 for the year due to asset impairments and write-offs in Q4 2025, mainly related to the Alberta renewables portfolio and certain hydrogen assets.

Click here to download our most recent Sure Analysis report on CDUAF (preview of page 1 of 3 shown below):

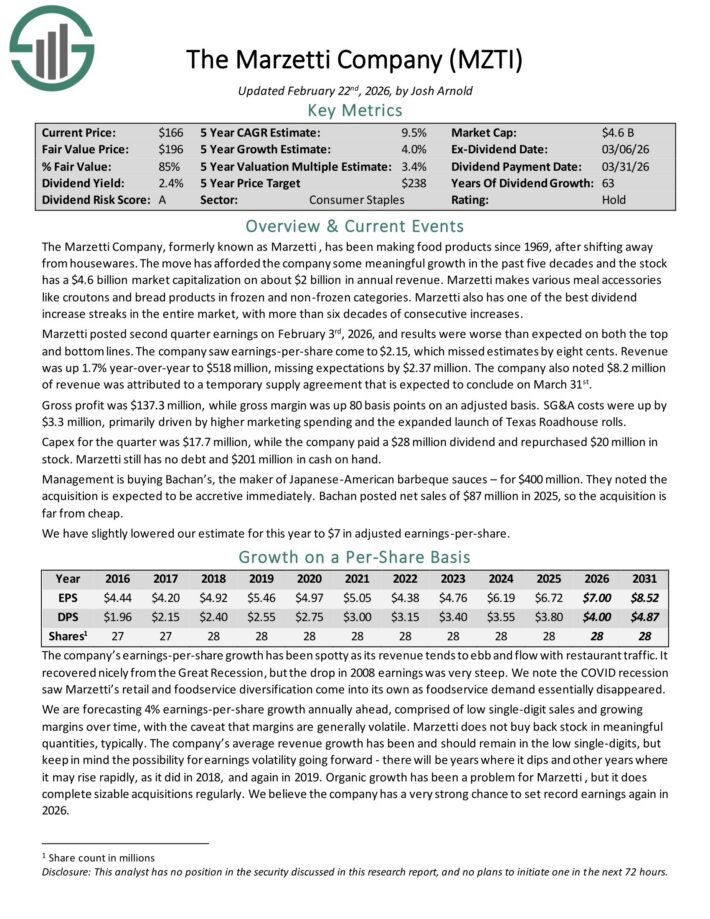

High Yield Dividend King #12: The Marzetti Company (MZTI)

- Dividend Yield: 3.7%

The Marzetti Company has been making food products since 1969. Marzetti makes various meal accessories like croutons and bread products in frozen and non-frozen categories.

Marzetti also has one of the best dividend increase streaks in the entire market, with more than six decades of consecutive increases.

Marzetti posted second quarter earnings on February 3rd, 2026, and results were worse than expected on both the top and bottom lines. The company saw earnings-per-share come to $2.15, which missed estimates by eight cents.

Revenue was up 1.7% year-over-year to $518 million, missing expectations by $2.37 million. The company also noted $8.2 million of revenue was attributed to a temporary supply agreement that is expected to conclude on March 31st.

Gross profit was $137.3 million, while gross margin was up 80 basis points on an adjusted basis. SG&A costs were up by $3.3 million, primarily driven by higher marketing spending and the expanded launch of Texas Roadhouse rolls.

Capex for the quarter was $17.7 million, while the company paid a $28 million dividend and repurchased $20 million in stock. Marzetti still has no debt and $201 million in cash on hand.

Management is buying Bachan’s, the maker of Japanese-American barbeque sauces – for $400 million. They noted the acquisition is expected to be accretive immediately.

Click here to download our most recent Sure Analysis report on MZTI (preview of page 1 of 3 shown below):

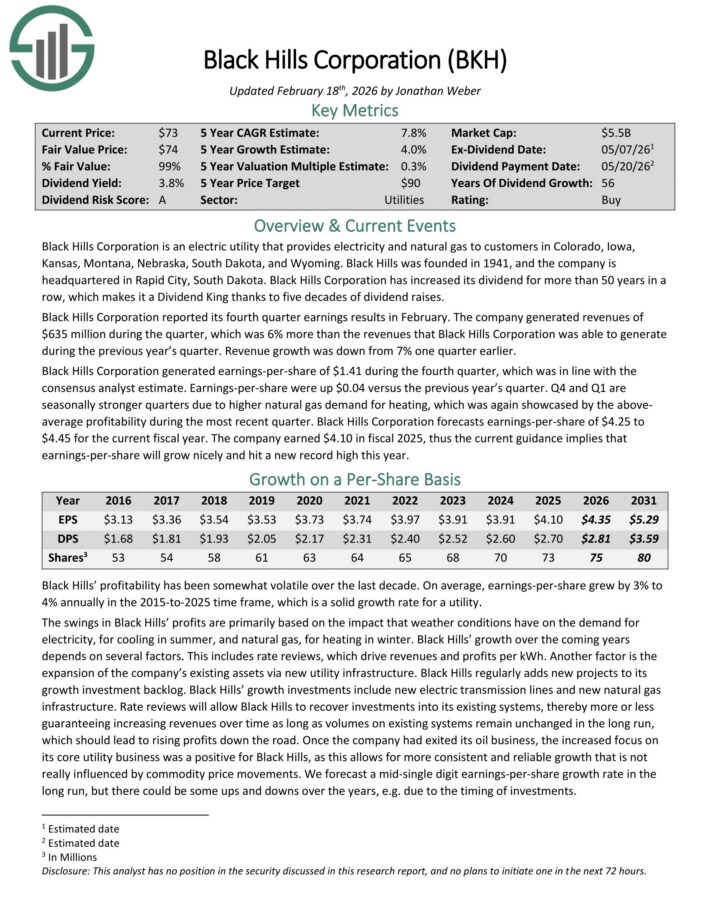

High Yield Dividend King #11: Black Hills Corporation (BKH)

- Dividend Yield: 3.8%

Black Hills Corporation is an electric utility that provides electricity and natural gas to customers in Colorado, Iowa, Kansas, Montana, Nebraska, South Dakota, and Wyoming.

The company has 1.35 million utility customers in eight states. Its natural gas assets include 49,200 miles of natural gas lines. Separately, it has ~9,200 miles of electric lines and 1.4 gigawatts of electric generation capacity.

Black Hills Corporation reported its fourth quarter earnings results in February. The company generated revenue of $635 million during the quarter, which was 6% more than the previous year’s fourth quarter.

Black Hills Corporation generated earnings-per-share of $1.41 during the fourth quarter, which was in line with the consensus analyst estimate. Earnings-per-share were up $0.04 versus the previous year’s quarter.

Q4 and Q1 are seasonally stronger quarters due to higher natural gas demand for heating, which was again showcased by the above-average profitability during the most recent quarter. Black Hills Corporation forecasts earnings-per-share of $4.25 to $4.45 for the current fiscal year.

Click here to download our most recent Sure Analysis report on BKH (preview of page 1 of 3 shown below):

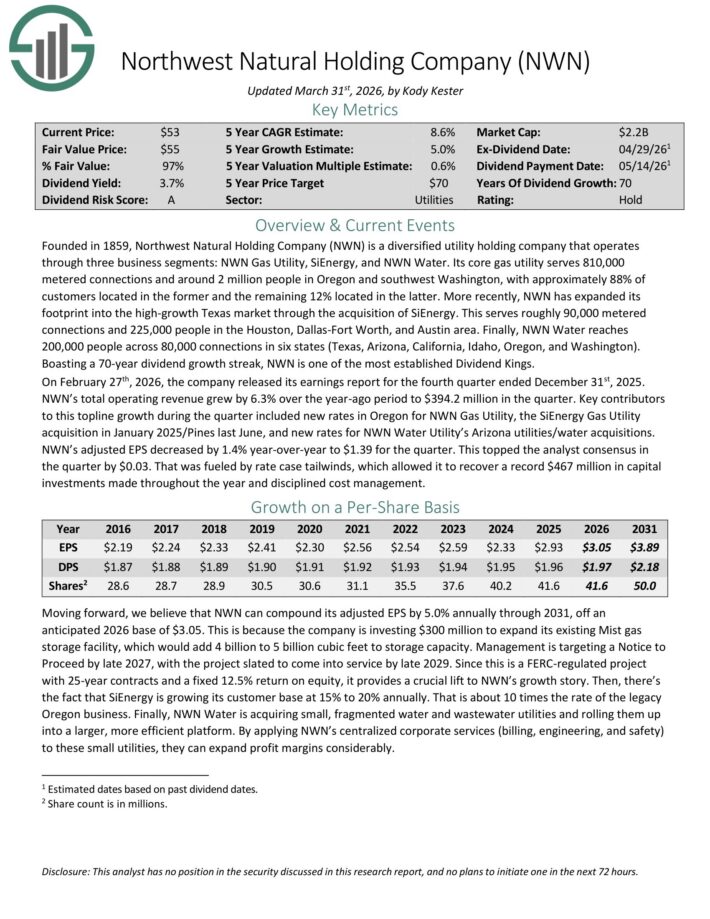

High Yield Dividend King #10: Northwest Natural Holding Co. (NWN)

- Dividend Yield: 4.0%

Northwest Natural Holding Company is a diversified utility holding company that operates through three business segments: NWN Gas Utility, SiEnergy, and NWN Water.

Its core gas utility serves 810,000 metered connections and around 2 million people in Oregon and southwest Washington, with approximately 88% of customers located in the former and the remaining 12% located in the latter.

More recently, NWN has expanded its footprint into the high-growth Texas market through the acquisition of SiEnergy. This serves roughly 90,000 metered connections and 225,000 people in the Houston, Dallas-Fort Worth, and Austin area.

Finally, NWN Water reaches 200,000 people across 80,000 connections in six states (Texas, Arizona, California, Idaho, Oregon, and Washington).

Boasting a 70-year dividend growth streak, NWN is one of the most established Dividend Kings.

On February 27th, 2026, the company released its earnings report for the fourth quarter ended December 31st, 2025. NWN’s total operating revenue grew by 6.3% over the year-ago period to $394.2 million in the quarter.

Key contributors to this topline growth during the quarter included new rates in Oregon for NWN Gas Utility, the SiEnergy Gas Utility acquisition in January 2025/Pines last June, and new rates for NWN Water Utility’s Arizona utilities/water acquisitions.

NWN’s adjusted EPS decreased by 1.4% year-over-year to $1.39 for the quarter.

Click here to download our most recent Sure Analysis report on NWN (preview of page 1 of 3 shown below):

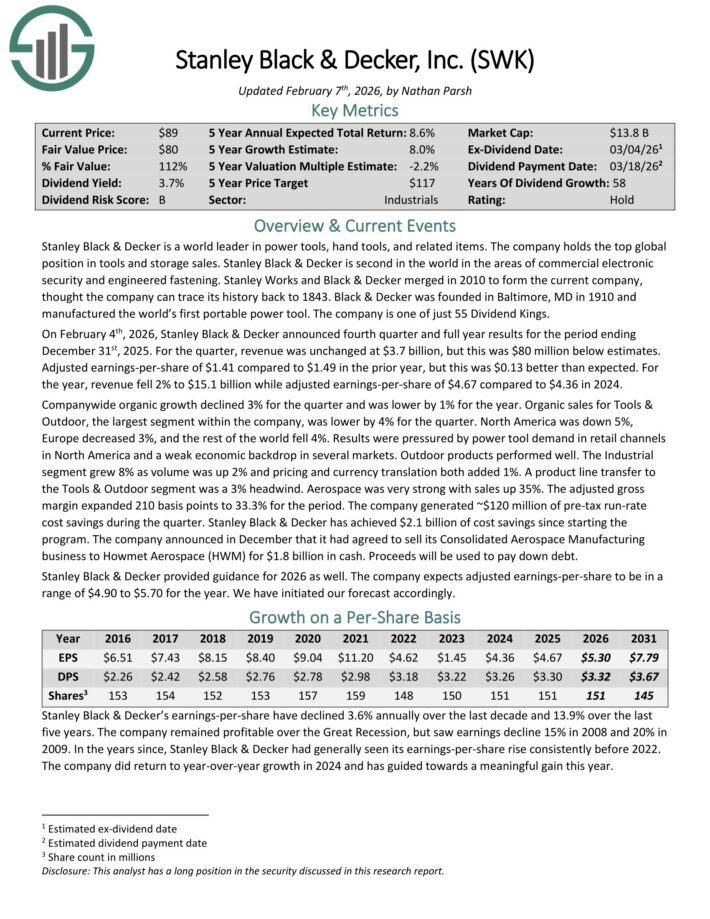

High Yield Dividend King #9: Stanley Black & Decker (SWK)

- Dividend Yield: 4.0%

Stanley Black & Decker is a world leader in power tools, hand tools, and related items. The company holds the top global position in tools and storage sales.

Stanley Black & Decker is second in the world in the areas of commercial electronic security and engineered fastening. The company is composed of three segments: tools & outdoor, and industrial.

On February 4th, 2026, Stanley Black & Decker announced fourth quarter and full year results. For the quarter, revenue was unchanged at $3.7 billion, but this was $80 million below estimates.

Adjusted earnings-per-share of $1.41 compared to $1.49 in the prior year, but this was $0.13 better than expected. For the year, revenue fell 2% to $15.1 billion while adjusted earnings-per-share of $4.67 compared to $4.36 in 2024.

Company-wide organic growth declined 3% for the quarter and was lower by 1% for the year. Organic sales for Tools & Outdoor, the largest segment within the company, was lower by 4% for the quarter.

North America was down 5%, Europe decreased 3%, and the rest of the world fell 4%. Results were pressured by power tool demand in retail channels in North America and a weak economic backdrop in several markets.

Click here to download our most recent Sure Analysis report on SWK (preview of page 1 of 3 shown below):

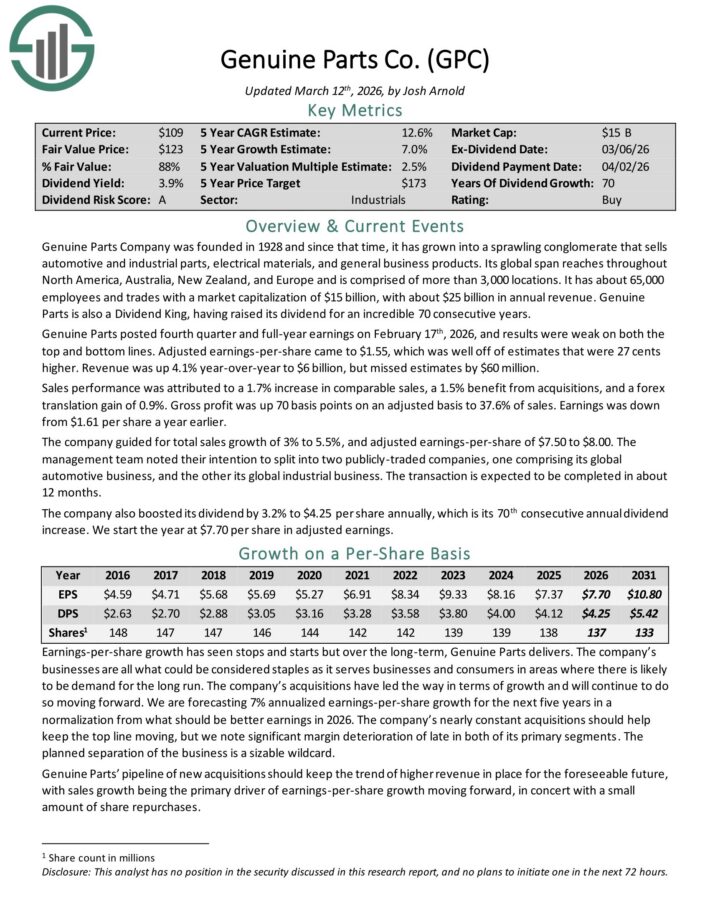

High Yield Dividend King #8: Genuine Parts Co. (GPC)

- Dividend Yield: 4.1%

Genuine Parts Company was founded in 1928 and since that time, it has grown into a sprawling conglomerate that sells automotive and industrial parts, electrical materials, and general business products.

Its global span reaches throughout North America, Australia, New Zealand, and Europe and is comprised of more than 3,000 locations. It has about 63,000 employees with about $24 billion in annual revenue.

Genuine Parts is also a Dividend King, having raised its dividend for an incredible 69 consecutive years.

Genuine Parts posted fourth quarter and full-year earnings on February 17th, 2026, and results were weak on both the top and bottom lines. Adjusted earnings-per-share came to $1.55, which was well off of estimates that were 27 cents higher. Revenue was up 4.1% year-over-year to $6 billion, but missed estimates by $60 million.

Sales performance was attributed to a 1.7% increase in comparable sales, a 1.5% benefit from acquisitions, and a forex translation gain of 0.9%. Gross profit was up 70 basis points on an adjusted basis to 37.6% of sales. Earnings was down from $1.61 per share a year earlier.

The company guided for total sales growth of 3% to 5.5%, and adjusted earnings-per-share of $7.50 to $8.00.

Click here to download our most recent Sure Analysis report on GPC (preview of page 1 of 3 shown below):

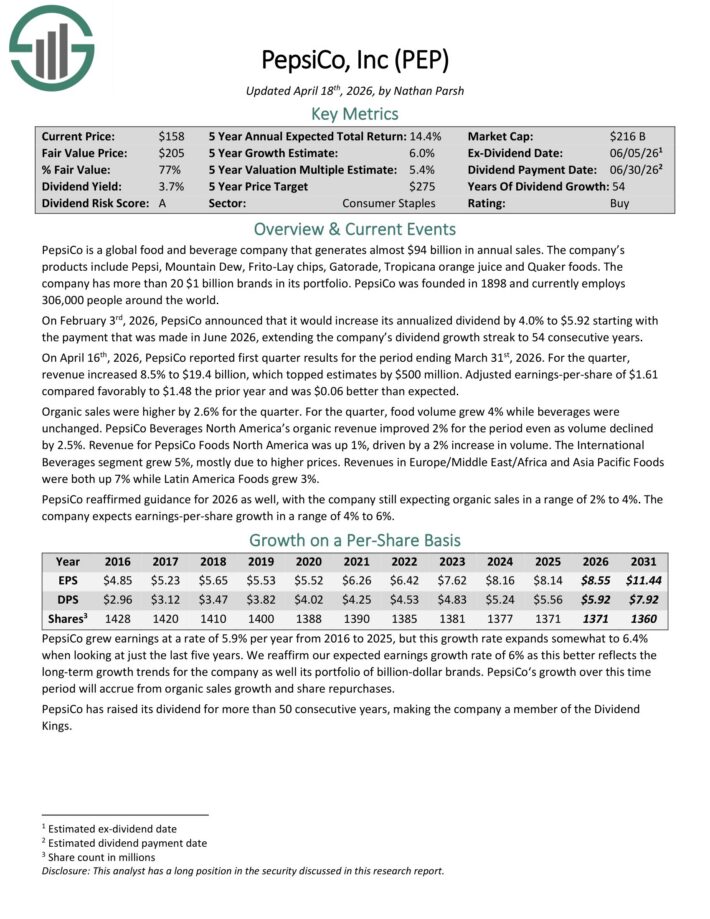

High Yield Dividend King #7: PepsiCo Inc. (PEP)

- Dividend Yield: 4.1%

PepsiCo is a global food and beverage company that generates almost $94 billion in annual sales. The company’s products include Pepsi, Mountain Dew, Frito-Lay chips, Gatorade, Tropicana orange juice and Quaker foods.

The company has more than 20 $1 billion brands in its portfolio. PepsiCo was founded in 1898 and currently employs

306,000 people around the world.

On February 3rd, 2026, PepsiCo increased its annualized dividend by 4.0% to $5.92 starting with the payment that was made in June 2026, extending the company’s dividend growth streak to 54 consecutive years.

On April 16th, 2026, PepsiCo reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue increased 8.5% to $19.4 billion, which topped estimates by $500 million.

Adjusted earnings-per-share of $1.61 compared favorably to $1.48 the prior year and was $0.06 better than expected.

Organic sales were higher by 2.6% for the quarter. For the quarter, food volume grew 4% while beverages were unchanged.

PepsiCo Beverages North America’s organic revenue improved 2% for the period even as volume declined by 2.5%. Revenue for PepsiCo Foods North America was up 1%, driven by a 2% increase in volume.

The International Beverages segment grew 5%, mostly due to higher prices. Revenue in Europe/Middle East/Africa and Asia Pacific Foods were both up 7% while Latin America Foods grew 3%.

PepsiCo reaffirmed guidance for 2026 as well, with the company still expecting organic sales in a range of 2% to 4%. The company expects earnings-per-share growth in a range of 4% to 6%.

Click here to download our most recent Sure Analysis report on PEP (preview of page 1 of 3 shown below):

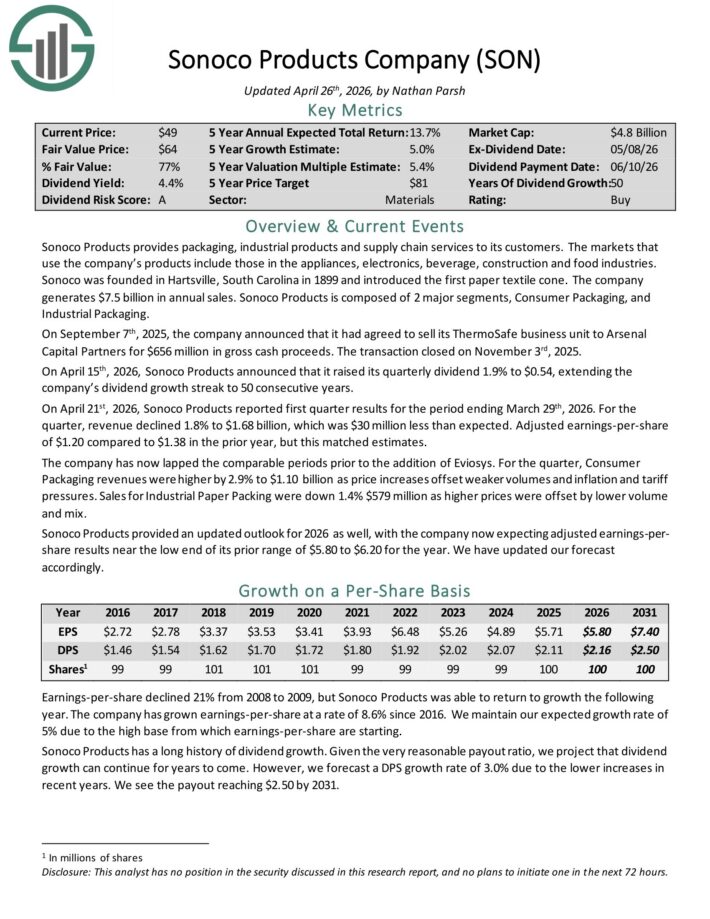

High Yield Dividend King #6: Sonoco Products (SON)

- Dividend Yield: 4.3%

Sonoco Products provides packaging, industrial products and supply chain services. The markets that use the company’s products include those in the appliances, electronics, beverage, construction and food industries.

The company generates $7.5 billion in annual sales.

On April 15th, 2026, Sonoco Products announced that it raised its quarterly dividend 1.9% to $0.54, extending the company’s dividend growth streak to 50 consecutive years.

On April 21st, 2026, Sonoco Products reported first quarter results for the period ending March 29th, 2026. For the quarter, revenue declined 1.8% to $1.68 billion, which was $30 million less than expected.

Adjusted earnings-per-share of $1.20 compared to $1.38 in the prior year, but this matched estimates.

The company has now lapped the comparable periods prior to the addition of Eviosys. For the quarter, Consumer Packaging revenue was higher by 2.9% to $1.10 billion as price increases offset weaker volumes and inflation and tariff pressures.

Sales for Industrial Paper Packing were down 1.4% $579 million as higher prices were offset by lower volume and mix.

Click here to download our most recent Sure Analysis report on SON (preview of page 1 of 3 shown below):

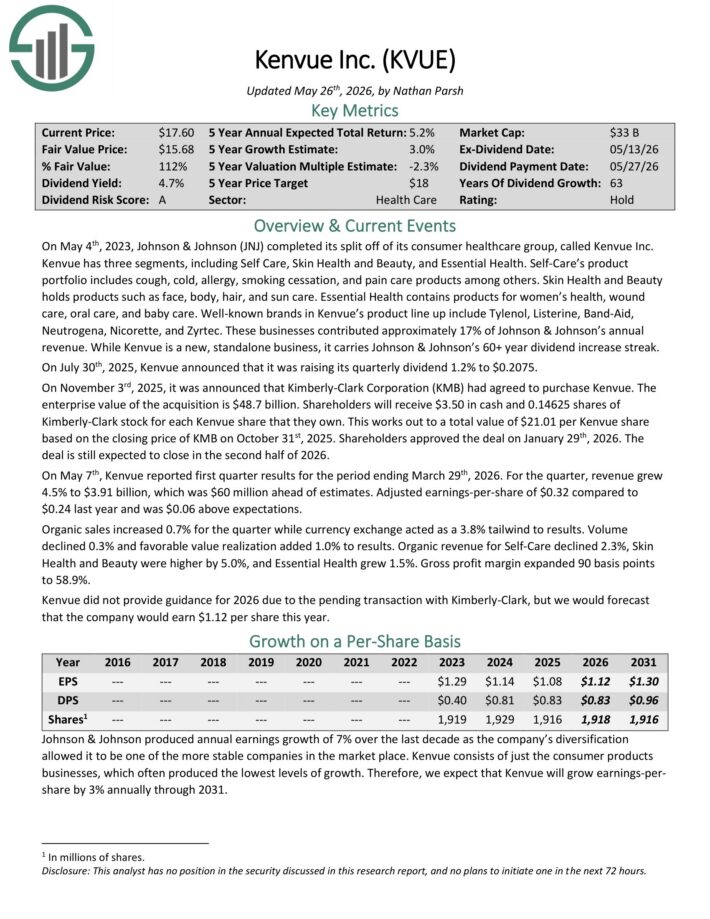

High Yield Dividend King #5: Kenvue Inc. (KVUE)

- Dividend Yield: 4.6%

Kenvue has three segments, including Self Care, Skin Health and Beauty, and Essential Health. Self-Care’s product portfolio includes cough, cold, allergy, smoking cessation, and pain care products among others.

Skin Health and Beauty holds products such as face, body, hair, and sun care. Essential Health contains products for women’s health, wound care, oral care, and baby care.

Well-known brands in Kenvue’s product line up include Tylenol, Listerine, Band-Aid, Neutrogena, Nicorette, and Zyrtec. These businesses contributed approximately 17% of Johnson & Johnson’s annual revenue.

While Kenvue is a new, standalone business, it carries Johnson & Johnson’s 60+ year dividend increase streak.

On November 3rd, 2025, it was announced that Kimberly-Clark Corporation (KMB) had agreed to purchase Kenvue. The enterprise value of the acquisition is $48.7 billion. Shareholders will receive $3.50 in cash and 0.14625 shares of Kimberly-Clark stock for each Kenvue share that they own.

This works out to a total value of $21.01 per Kenvue share based on the closing price of KMB on October 31st, 2025. The deal is expected to close in the second half of 2026.

On May 7th, Kenvue reported first quarter results for the period ending March 29th, 2026. For the quarter, revenue grew 4.5% to $3.91 billion, which was $60 million ahead of estimates.

Adjusted earnings-per-share of $0.32 compared to $0.24 last year and was $0.06 above expectations.

Organic sales increased 0.7% for the quarter while currency exchange acted as a 3.8% tailwind to results. Volume declined 0.3% and favorable value realization added 1.0% to results.

Click here to download our most recent Sure Analysis report on KVUE (preview of page 1 of 3 shown below):

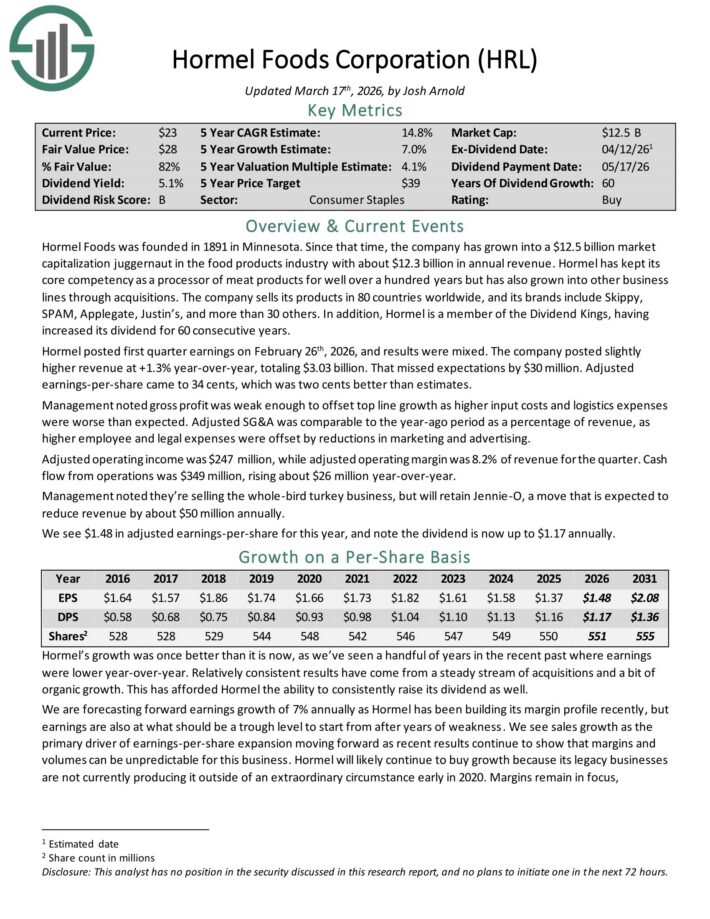

High Yield Dividend King #4: Hormel Foods (HRL)

- Dividend Yield: 4.8%

Hormel Foods was founded in 1891 in Minnesota. Since that time, the company has grown into a juggernaut in the food products industry with about $12.3 billion in annual revenue.

Hormel has kept its core competency as a processor of meat products for well over a hundred years but has also grown into other business lines through acquisitions.

The company sells its products in 80 countries worldwide, and its brands include Skippy, SPAM, Applegate, Justin’s, and more than 30 others.

Hormel posted first quarter earnings on February 26th, 2026, and results were mixed. The company posted slightly higher revenue at +1.3% year-over-year, totaling $3.03 billion. That missed expectations by $30 million.

Adjusted earnings-per-share came to 34 cents, which was two cents better than estimates.

Management noted gross profit was weak enough to offset top line growth as higher input costs and logistics expenses were worse than expected.

Adjusted SG&A was comparable to the year-ago period as a percentage of revenue, as higher employee and legal expenses were offset by reductions in marketing and advertising.

Adjusted operating income was $247 million, while adjusted operating margin was 8.2% of revenue for the quarter.

Cash flow from operations was $349 million, rising about $26 million year-over-year.

Click here to download our most recent Sure Analysis report on HRL (preview of page 1 of 3 shown below):

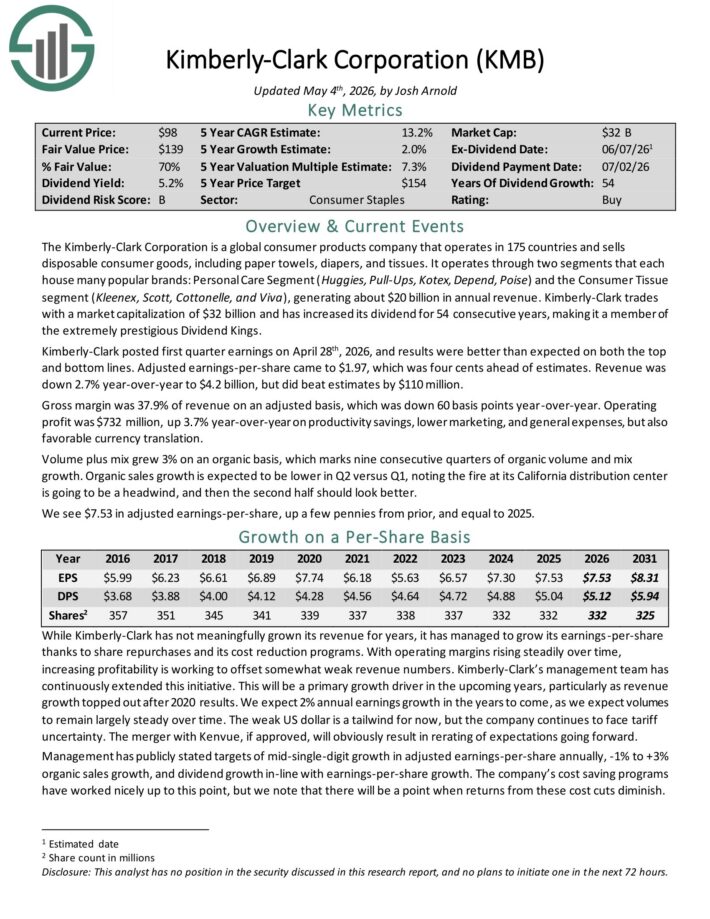

High Yield Dividend King #3: Kimberly-Clark (KMB)

- Dividend Yield: 5.0%

The Kimberly-Clark Corporation is a global consumer products company that operates in 175 countries and sells disposable consumer goods, including paper towels, diapers, and tissues.

It operates through two segments that each house many popular brands: Personal Care Segment (Huggies, Pull-Ups, Kotex, Depend, Poise) and the Consumer Tissue segment (Kleenex, Scott, Cottonelle, and Viva), generating about $20 billion in annual revenue.

Kimberly-Clark has increased its dividend for 54 consecutive years, making it a member of the extremely prestigious Dividend Kings.

Kimberly-Clark posted first quarter earnings on April 28th, 2026, and results were better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to $1.97, which was four cents ahead of estimates. Revenue was down 2.7% year-over-year to $4.2 billion, but did beat estimates by $110 million.

Click here to download our most recent Sure Analysis report on KMB (preview of page 1 of 3 shown below):

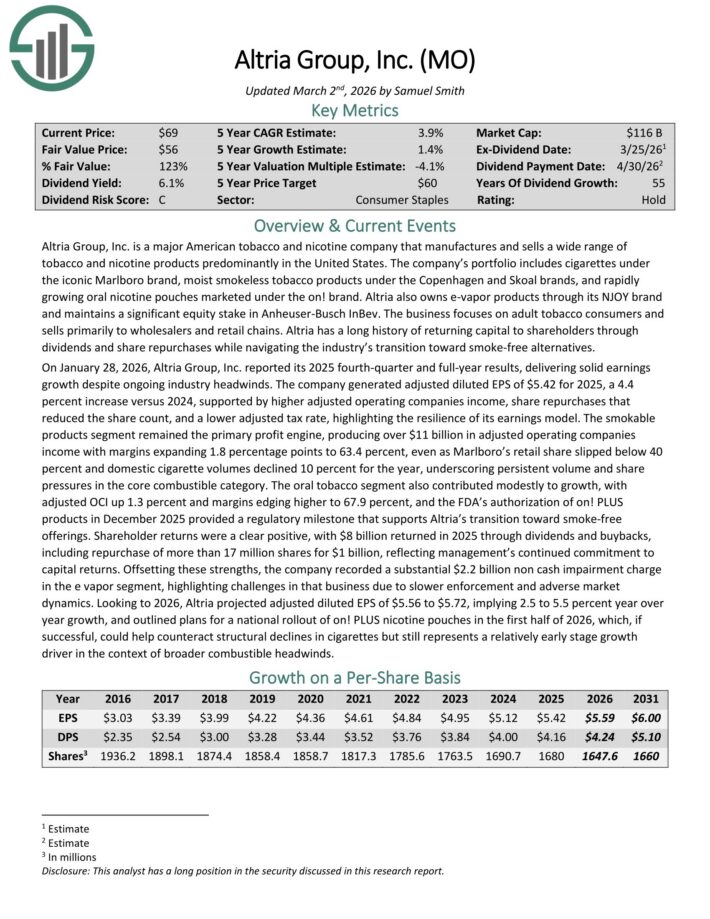

High Yield Dividend King #2: Altria Group (MO)

- Dividend Yield: 6.0%

Altria is a tobacco stock that sells cigarettes, chewing tobacco, cigars, e-cigarettes, and more under a variety of brands, including Marlboro, Skoal, and Copenhagen, among others.

This is a period of transition for Altria. The decline in the U.S. smoking rate continues. In response, Altria has invested heavily in new products that appeal to changing consumer preferences, as the smoke-free category continues to grow.

The company also has a 35% investment stake in e-cigarette maker JUUL, and a 45% stake in the Canadian cannabis producer Cronos Group (CRON).

On January 28, 2026, Altria Group, Inc. reported its 2025 fourth-quarter and full-year results. The company generated adjusted diluted EPS of $5.42 for 2025, a 4.4% increase versus 2024.

EPS growth was supported by higher adjusted operating companies income, share repurchases that reduced the share count, and a lower adjusted tax rate.

The smokable products segment remained the primary profit engine, producing over $11 billion in adjusted operating companies income with margins expanding 1.8 percentage points to 63.4%.

Margin expansion occurred even as Marlboro’s retail share slipped below 40% and domestic cigarette volumes declined 10% for the year. The oral tobacco segment also contributed modestly to growth, with adjusted OCI up 1.3%.

Looking to 2026, Altria projected adjusted diluted EPS of $5.56 to $5.72, implying 2.5% to 5.5% year-over-year growth.

Click here to download our most recent Sure Analysis report on Altria (preview of page 1 of 3 shown below):

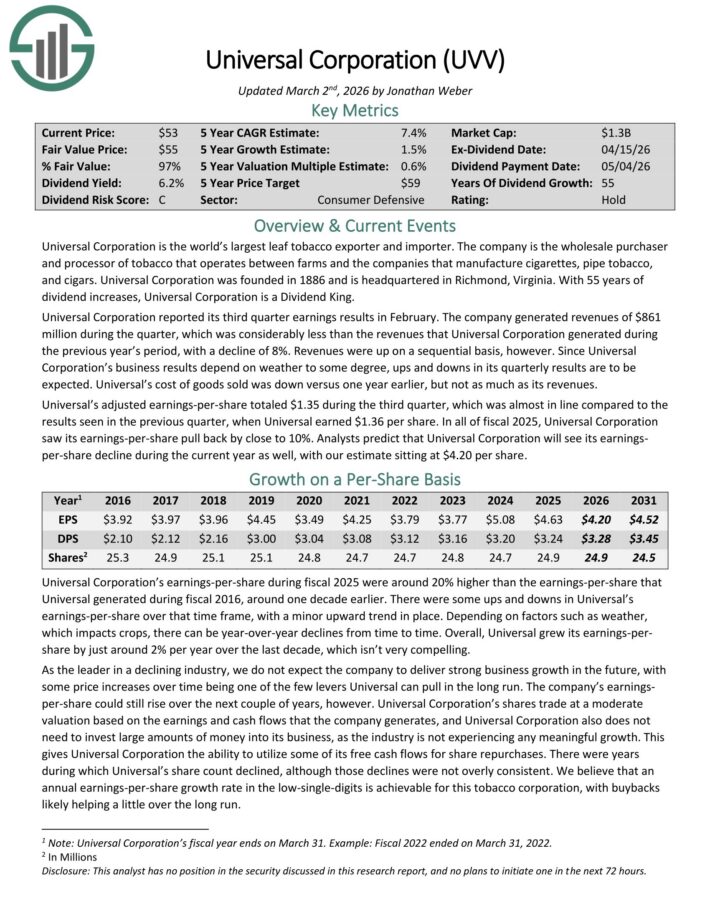

High Yield Dividend King #1: Universal Corporation (UVV)

- Dividend Yield: 6.2%

Universal Corporation is a market leader in supplying leaf tobacco and other plant-based inputs to consumer product manufacturers.

The Tobacco Operations segment buys and sells tobacco used to make cigarettes, cigars, pipe tobacco, and smokeless products. Universal buys tobacco from its suppliers, processes it, and sells it to large tobacco companies in the US and internationally.

The Ingredient Operations deal mainly with vegetables and fruits but is significantly smaller than the tobacco operations.

Universal Corporation reported its third quarter earnings results in February. The company generated revenues of $861 million during the quarter, a year-over-year decline of 8%. Revenues were up on a sequential basis, however.

Since Universal Corporation’s business results depend on weather to some degree, ups and downs in its quarterly results are to be expected. Cost of goods sold was down versus one year earlier, but not as much as its revenues.

Universal’s adjusted earnings-per-share totaled $1.35 during the third quarter, which was almost in line compared to the results seen in the previous quarter, when Universal earned $1.36 per share.

In all of fiscal 2025, Universal Corporation saw its earnings-per-share pull back by close to 10%..

Click here to download our most recent Sure Analysis report on UVV (preview of page 1 of 3 shown below):

Final Thoughts

High yield dividend stocks have obvious appeal to income investors. The S&P 500 Index yields just ~1.2% right now on average, making high yield stocks even more attractive by comparison.

Of course, investors should always do their research before buying individual stocks.

That said, the 20 stocks in this list have yields at least double the S&P 500 Index average. And, each of these stocks has increased their dividends for 50 consecutive years.

They are all part of the exclusive Dividend Kings list. As a result, income investors may find these 20 dividend stocks attractive.

Further Reading

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

- 20 Undervalued High-Dividend Stocks

- 20 Highest Yielding Monthly Dividend Stocks

- 20 Highest-Yielding Small Cap Dividend Stocks

- Long-Term High-Dividend Stocks To Buy And Hold For Decades

- 10 Super High Dividend REITs

- Highest Yielding Royalty Trusts

Other Sure Dividend Resources

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- High Dividend Stocks: 5%+ dividend yields

- Monthly Dividend Stocks: Individual securities that pay out every month

- Blue Chip Stocks: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more