Updated on March 18th, 2026 by Felix Martinez

As the saying goes, slow-and-steady wins the race.

This comes to mind when discussing the Dividend Aristocrats, a select group of just 69 companies in the S&P 500 Index, each with at least 25 consecutive years of dividend increases.

The Dividend Aristocrats are among the best stocks for investors looking to generate long-term wealth that can last for generations.

With this in mind, we compiled a complete list of Dividend Aristocrats, along with relevant financial metrics, such as price-to-earnings ratios.

You can download your full Dividend Aristocrats list by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Hormel Foods (HRL) is the very definition of a slow-and-steady stock.

While it will not make investors rich overnight, it has steadily built wealth for its shareholders over many years.

Hormel operates in a stable industry and has many strong brands. It has also rewarded shareholders with 60 consecutive years of rising dividends over the past 90 years.

Not only is Hormel a Dividend Aristocrat, but it is also a Dividend King, thanks to its outstanding track record of returning cash to shareholders.

The Dividend Kings have increased their dividends for 50+ consecutive years. You can see all the Dividend Kings here.

This article will discuss why Hormel is a high-quality dividend growth stock and provide some perspective on the company’s growth and valuation outlook.

Business Overview

Hormel was founded in 1891, when George A. Hormel established Geo. A. Hormel & Company in Austin, Minnesota. Consumers took a liking to Hormel’s fresh pork products, which were a novelty at the time. In 1926, the company produced the world’s first canned ham.

Hormel has continued to grow in the decades since, and now generates ~$12.1 billion in annual revenue. It has a diverse product portfolio today, spanning several categories. Some of its major brands include Skippy, Jennie-O, Spam, Hormel, and Dinty Moore.

In recent years, it has added more natural products to complement its processed offerings, such as Justin’s and Applegate.

Hormel reported Q1 fiscal 2026 revenue of $3.03 billion, up 1.3% year over year, though slightly below expectations. GAAP EPS was $0.33 and adjusted EPS was $0.34, beating estimates.

Operating income totaled $244 million with an 8.0% operating margin, while adjusted operating income was $247 million (8.2% margin). The company generated $349 million in operating cash flow, reflecting solid underlying execution.

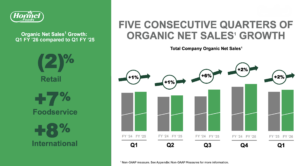

Segment performance was mixed. Foodservice revenue increased 7% with profit up 13%, and International sales rose 8% with profit up 10%, driven by strong demand and pricing.

In contrast, Retail sales declined 2%, and segment profit fell 19%, pressured by lower volumes, higher input costs, and portfolio adjustments. Overall, organic net sales grew 2%, marking the fifth consecutive quarter of growth.

Looking ahead, management reaffirmed fiscal 2026 revenue guidance of $12.2–$12.5 billion (1%–4% organic growth) and expects adjusted EPS of $1.43–$1.51 (4%–10% growth). GAAP EPS guidance was raised to $1.37–$1.46, reflecting portfolio changes, including the sale of the Justin’s business.

The company continues to shift toward higher-margin, value-added protein products while reducing exposure to more volatile commodity segments.

Source: Investor Presentation

Growth Prospects

Hormel has an extremely impressive history of generating consistent year-over-year growth, regardless of the broader economic climate. This speaks to the company’s strong brands and staying power during the recession.

Hormel’s growth prospects depend upon a few different levers it can pull in the coming years. Organic growth is likely due to the company’s strong brands. In addition, Hormel has habitually bought its growth over the years through acquisitions.

The most recent example is Hormel’s $3.35 billion acquisition of the Planters snack-nut portfolio from Kraft Heinz (KHC). The acquisition fits perfectly into Hormel’s long-held acquisition strategy.

The deal is expected to provide Hormel with a $560 million tax benefit, for a net price of $2.79 billion. The portfolio generated $1 billion in sales in 2020 and is expected to meet Hormel’s long–term organic growth target.

Moving forward, we expect 7% annualized earnings per share growth over the next half-decade.

Source: Investor Presentation

Competitive Advantages & Recession Performance

Hormel has several operational advantages. First, it operates in a wide variety of very stable food businesses. Everyone has to eat, which gives the company a certain level of demand, even during recessions.

In addition, Hormel’s products are affordable for everyone, so stability should shine through during tough economic times.

In addition, Hormel has many strong brands, which give the company pricing power. Hormel has the #1 or #2 position in over 40 of its brands.

Hormel’s popular products make it difficult for competing food companies to take market share. In fact, Hormel has held that enviable leadership position for years, so it is certainly a lasting advantage.

Hormel’s competitive advantages provide the company with a recession-resistant business model. Hormel’s earnings per share during the Great Recession are below:

- 2007 earnings-per-share of $0.54

- 2008 earnings-per-share of $0.52 (3.7% decline)

- 2009 earnings-per-share of $0.63 (21% increase)

- 2010 earnings-per-share of $0.76 (21% increase)

As you can see, Hormel experienced a mild earnings decline in 2008, then racked up two consecutive years of 20%+ earnings growth. We expect Hormel to perform very well whenever the next recession strikes.

Valuation & Expected Returns

We expect Hormel to generate an adjusted EPS of $1.48 for fiscal 2026. Based on this, the stock trades for a price-to-earnings ratio of 15.5x. This is below Hormel’s 10-year average price-to-earnings ratio. We view Hormel’s fair value at a P/E of 19x.

As a result, Hormel appears to be undervalued right now. If the P/E expands to 19 over the next five years, it would increase annual returns by 4.1%.

With expected EPS growth of 7% and a dividend yield of 3.7%, total returns are estimated at 14.8% per year.

The company’s dividend is very safe and will almost certainly continue to grow for many years. Given that the total return profile is over 10% annualized, we rate Hormel stock a buy.

Final Thoughts

Hormel has paid consecutive quarterly dividends without interruption since it became a public company in 1928. It has established one of the longest dividend-increase streaks in the market and is a Dividend King.

Consumer staples stocks enjoy steady demand and pricing power, particularly food companies with strong brands. Hormel has a strong business with a high-quality brand portfolio.

We rate HRL stock a Buy.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: