Updated on September 19th, 2025 by Bob Ciura

Blue-chip stocks are established, financially strong, and consistently profitable publicly traded companies.

Their strength makes them appealing investments for comparatively safe, reliable dividends and capital appreciation versus less established stocks.

This research report has the following resources to help you invest in blue chip stocks:

Resource #1: The Blue Chip Stocks Spreadsheet List

There are currently more than 500 securities in our blue chip stocks list.

We categorize blue chip stocks as companies that are members of 1 or more of the following 3 lists:

- Dividend Achievers (10+ years of rising dividends, in the NASDAQ)

- Dividend Aristocrats (25+ years of rising dividends, in the S&P 500)

- Dividend Kings (50+ years of rising dividends)

Simply put, blue chip stocks have at least 10 consecutive years of dividend increases.

At the same time, we often recommend income investors consider high dividend stocks, for their elevated dividend yields.

High dividend stocks means more income for every dollar invested. All other things equal, the higher the dividend yield, the better.

The combination of dividend yield and growth, can result in outstanding long-term returns.

In this research report, we analyze the 10 highest-yielding blue chip stocks right now.

The list is sorted by dividend yield, in ascending order.

Table of Contents

The table of contents below allows for easy navigation.

- High Yield Blue Chip #10: Enterprise Products Partners LP (EPD)

- High Yield Blue Chip #9: Universal Health Realty Income Trust (UHT)

- High Yield Blue Chip #8: Pfizer Inc. (PFE)

- High Yield Blue Chip #7: Flowers Foods (FLO)

- High Yield Blue Chip #6: MPLX LP (MPLX)

- High Yield Blue Chip #5: Telus Corp. (TU)

- High Yield Blue Chip #4: United Parcel Service (UPS)

- High Yield Blue Chip #3: Delek Logistics Partners LP (DKL)

- High-Yield Blue Chip #2: LyondellBasell Industries (LYB)

- High Yield Blue Chip #1: Cogent Communications Holdings (CCOI)

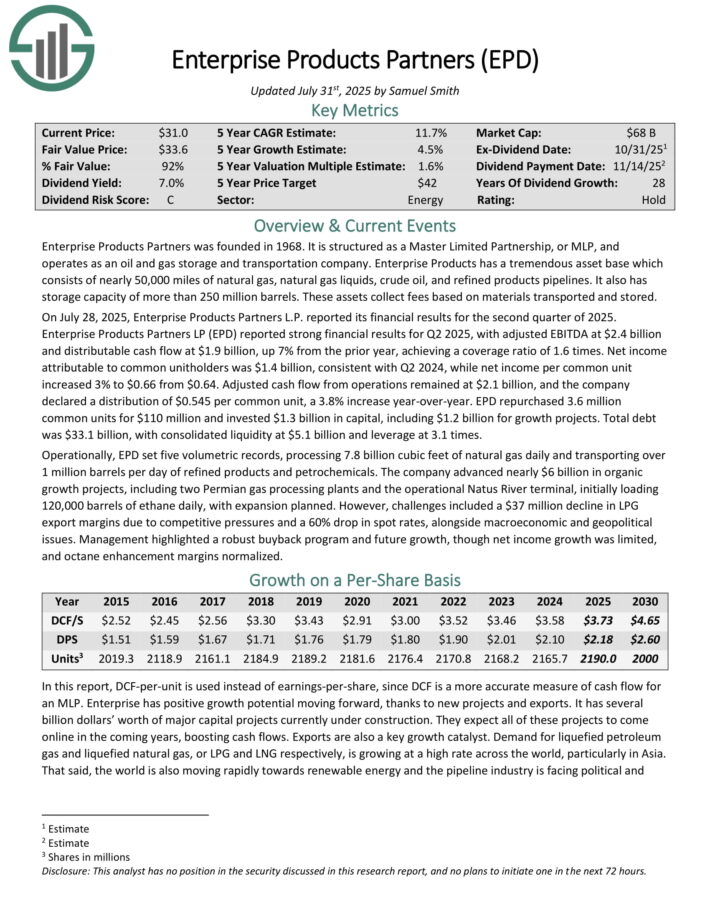

High Yield Blue Chip #10: Enterprise Products Partners LP (EPD)

- Dividend History: 28 years of consecutive increases

- Dividend Yield: 6.8%

Enterprise Products Partners was founded in 1968. It is structured as a Master Limited Partnership, or MLP, and operates as an oil and gas storage and transportation company. Enterprise Products has a large asset base which consists of nearly 50,000 miles of natural gas, natural gas liquids, crude oil, and refined products pipelines.

It also has storage capacity of more than 250 million barrels. These assets collect fees based on volumes of materials transported and stored.

On July 28, 2025, Enterprise Products Partners L.P. reported its financial results for the second quarter of 2025. Distributable cash flow was $1.9 billion, up 7% from the prior year, with a coverage ratio of 1.6 times. Net income per common unit increased 3% to $0.66 from $0.64.

Adjusted cash flow from operations remained at $2.1 billion, and the company declared a distribution of $0.545 per common unit, a 3.8% increase year-over-year. EPD repurchased 3.6 million common units for $110 million and invested $1.3 billion in capital, including $1.2 billion for growth projects.

Click here to download our most recent Sure Analysis report on EPD (preview of page 1 of 3 shown below):

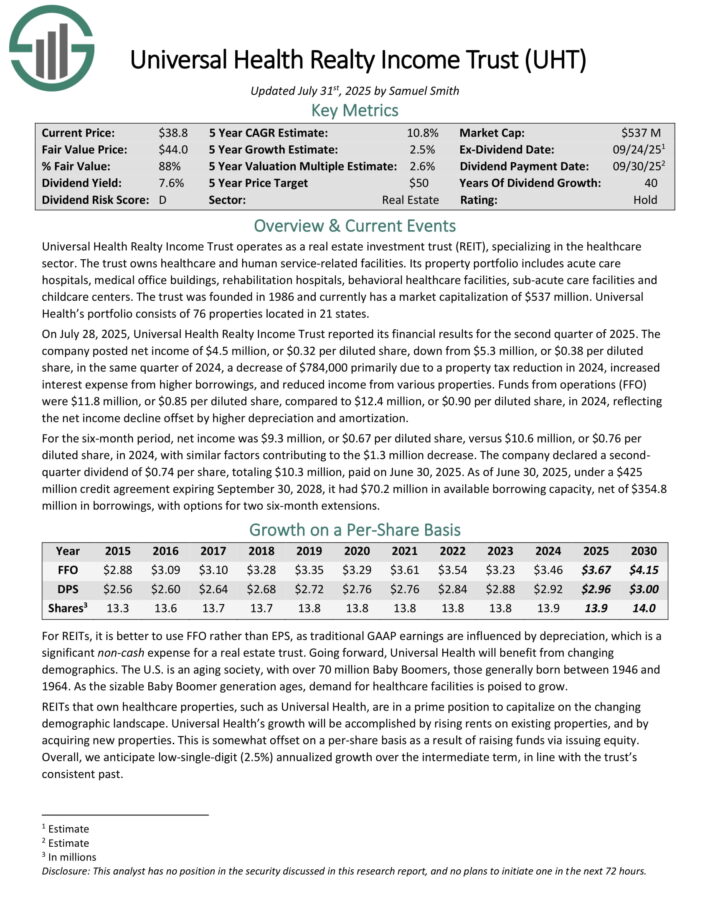

High Yield Blue Chip #9: Universal Health Realty Income Trust (UHT)

- Dividend History: 38 years of consecutive increases

- Dividend Yield: 7.0%

Universal Health Realty Income Trust operates as a real estate investment trust (REIT), specializing in the healthcare sector. The trust owns healthcare and human service-related facilities.

Its property portfolio includes acute care hospitals, medical office buildings, rehabilitation hospitals, behavioral healthcare facilities, sub-acute care facilities and childcare centers.

Universal Health’s portfolio consists of 76 properties located in 21 states.

On July 28, 2025, Universal Health Realty Income Trust reported its financial results for the second quarter of 2025. The company posted net income of $4.5 million, or $0.32 per diluted share, down from $5.3 million, or $0.38 per diluted share, in the same quarter of 2024, a decrease of $784,000 primarily due to a property tax reduction in 2024, increased interest expense from higher borrowings, and reduced income from various properties.

Funds from operations (FFO) were $11.8 million, or $0.85 per diluted share, compared to $12.4 million, or $0.90 per diluted share, in 2024, reflecting the net income decline offset by higher depreciation and amortization.

For the six-month period, net income was $9.3 million, or $0.67 per diluted share, versus $10.6 million, or $0.76 per diluted share, in 2024, with similar factors contributing to the $1.3 million decrease. The company declared a second-quarter dividend of $0.74 per share.

Click here to download our most recent Sure Analysis report on UHT (preview of page 1 of 3 shown below):

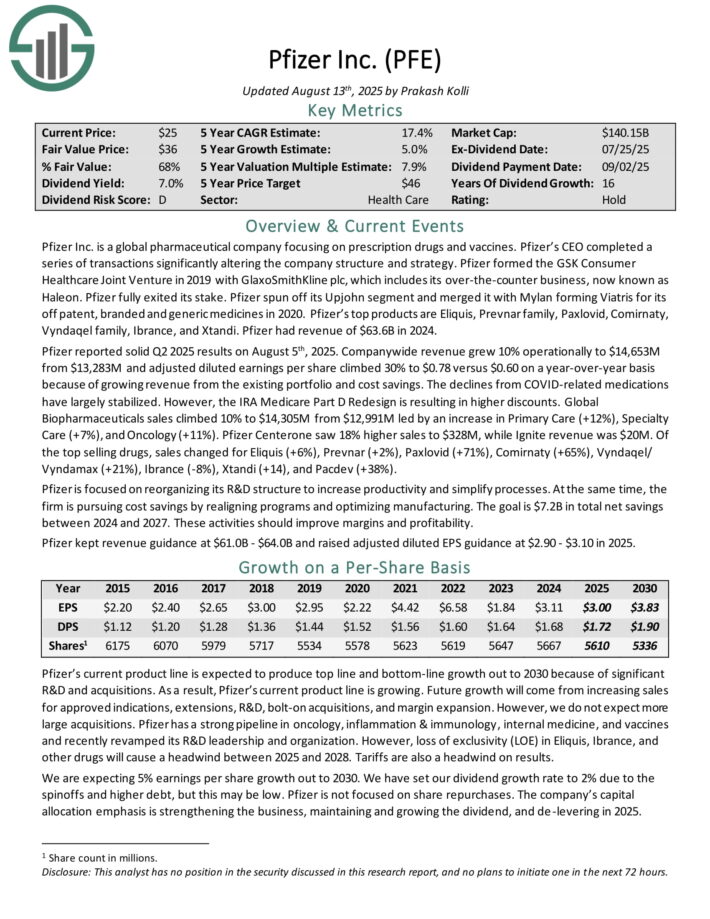

High Yield Blue Chip #8: Pfizer Inc. (PFE)

- Dividend History: 16 years of consecutive increases

- Dividend Yield: 7.1%

Pfizer Inc. is a global pharmaceutical company focusing on prescription drugs and vaccines. Pfizer’s top products are Eliquis, Prevnar family, Paxlovid, Comirnaty, Vyndaqel family, Ibrance, and Xtandi. Pfizer had revenue of $63.6B in 2024.

Pfizer reported solid Q2 2025 results on August 5th, 2025. Companywide revenue grew 10% operationally and adjusted diluted earnings per share climbed 30% to $0.78 versus $0.60 on a year-over-year basis because of growing revenue from the existing portfolio and cost savings.

The declines from COVID-related medications have largely stabilized. However, the IRA Medicare Part D Redesign is resulting in higher discounts. Global Biopharmaceuticals sales climbed 10% led by an increase in Primary Care (+12%), SpecialtyCare (+7%), and Oncology (+11%). Pfizer Centerone saw 18% higher sales.

Of the top selling drugs, sales changed for Eliquis (+6%), Prevnar (+2%), Paxlovid (+71%), Comirnaty (+65%), Vyndaqel/ Vyndamax (+21%), Ibrance (-8%), Xtandi (+14), and Pacdev (+38%).

Pfizer is focused on reorganizing its R&D structure to increase productivity and simplify processes. At the same time, the firm is pursuing cost savings by realigning programs and optimizing manufacturing. The goal is $7.2B in total net savings between 2024 and 2027. These activities should improve margins and profitability.

Pfizer kept revenue guidance at $61.0B – $64.0B and raised adjusted diluted EPS guidance at $2.90 – $3.10 in 2025..

Click here to download our most recent Sure Analysis report on PFE (preview of page 1 of 3 shown below):

High Yield Blue Chip #7: Flowers Foods (FLO)

- Dividend History: 23 years of consecutive increases

- Dividend Yield: 7.4%

Flowers Foods opened its first bakery in 1919 and has since become one of the largest producers of packaged bakery foods in the United States, operating 46 bakeries in 18 states.

Well-known brands include Wonder Bread, Home Pride, Nature’s Own, Dave’s Killer Bread, Tastykake and Canyon Bakehouse.

The company operates in two segments: Direct-Store-Delivery (DSD) and Warehouse Delivery, with ~85% of the company’s product being delivered directly to stores.

Fresh breads, buns, rolls, and tortillas make up about a three-fourths of the business, with sales channels for the company split between Supermarkets, Mass Merchandisers, Foodservice, and Convenience Store.

On May 22nd, 2025, Flower Foods increased its quarterly dividend 3.1% to $0.2475, extending the company’s dividend growth streak to 23 consecutive years.

On August 15th, 2025, Flowers Foods announced second quarter results for the period ending July 12th, 2025. For the quarter, revenue grew 0.8% to $1.24 billion, but missed estimates by $30 million. Adjusted earnings-per-share of $0.30 compared to $0.36 last year, but this was $0.01 more than expected.

For the quarter, Branded Retail sales improved 5% to $826.7 million as declines in pricing (-1.5%) and volumes (-1.3%) were offset by a strong contribution from Simple Mills (+7.8%).

Other sales decreased 4.8% to $416.1 million due to lower volumes and weaker pricing and mix. Materials, supplies, labor, and other production costs accounted for 51.2% of sales during the quarter, which was a 110 basis point increase from the prior year.

Flowers Foods provided an updated outlook for 2025 as well. Adjusted earnings-per-share are now expected to be in a range of $1.00 to $1.10 for the year.

Click here to download our most recent Sure Analysis report on FLO (preview of page 1 of 3 shown below):

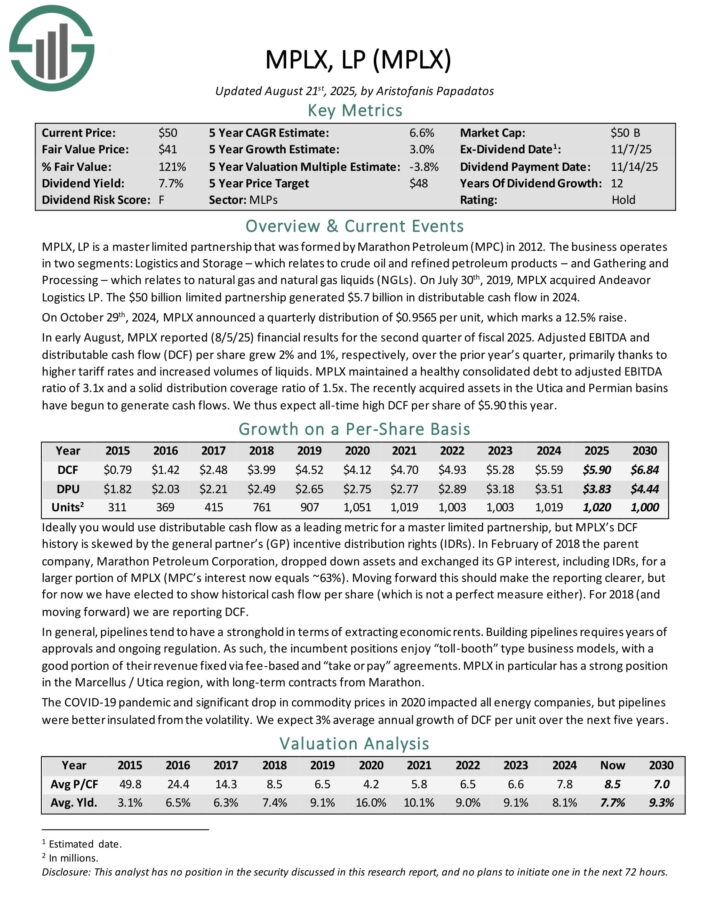

High Yield Blue Chip #6: MPLX LP (MPLX)

- Dividend History: 12 years of consecutive increases

- Dividend Yield: 7.5%

MPLX LP is a Master Limited Partnership that was formed by the Marathon Petroleum Corporation (MPC) in 2012. In 2019, MPLX acquired Andeavor Logistics LP.

The business operates in two segments:

- Logistics and Storage, which relates to crude oil and refined petroleum products

- Gathering and Processing, which relates to natural gas and natural gas liquids (NGLs)

In early August, MPLX reported (8/5/25) financial results for the second quarter of fiscal 2025. Adjusted EBITDA and distributable cash flow (DCF) per share grew 2% and 1%, respectively, over the prior year’s quarter, primarily thanks to higher tariff rates and increased volumes of liquids.

MPLX maintained a healthy consolidated debt to adjusted EBITDA ratio of 3.1x and a solid distribution coverage ratio of 1.5x. The recently acquired assets in the Utica and Permian basins have begun to generate cash flows.

Click here to download our most recent Sure Analysis report on MPLX (preview of page 1 of 3 shown below):

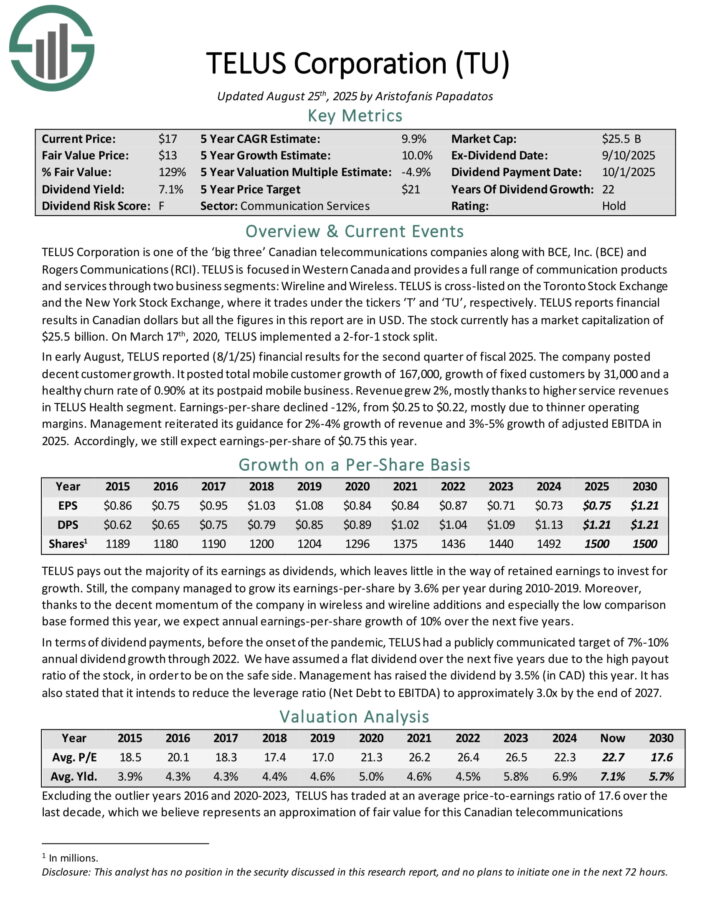

High Yield Blue Chip #5: Telus Corp. (TU)

- Dividend History: 22 years of consecutive increases

- Dividend Yield: 7.6%

TELUS Corporation is one of the ‘big three’ Canadian telecommunications companies. TELUS is focused in Western Canada and provides a full range of communication products and services through two business segments: Wireline and Wireless.

In early August, TELUS reported (8/1/25) financial results for the second quarter of fiscal 2025. The company posted decent customer growth.

It posted total mobile customer growth of 167,000, growth of fixed customers by 31,000 and a healthy churn rate of 0.90% at its postpaid mobile business.

Revenue grew 2%, mostly thanks to higher service revenues in TELUS Health segment. Earnings-per-share declined -12%, from $0.25 to $0.22, mostly due to thinner operating margins.

Management reiterated its guidance for 2%-4% growth of revenue and 3%-5% growth of adjusted EBITDA in 2025.

Click here to download our most recent Sure Analysis report on TU (preview of page 1 of 3 shown below):

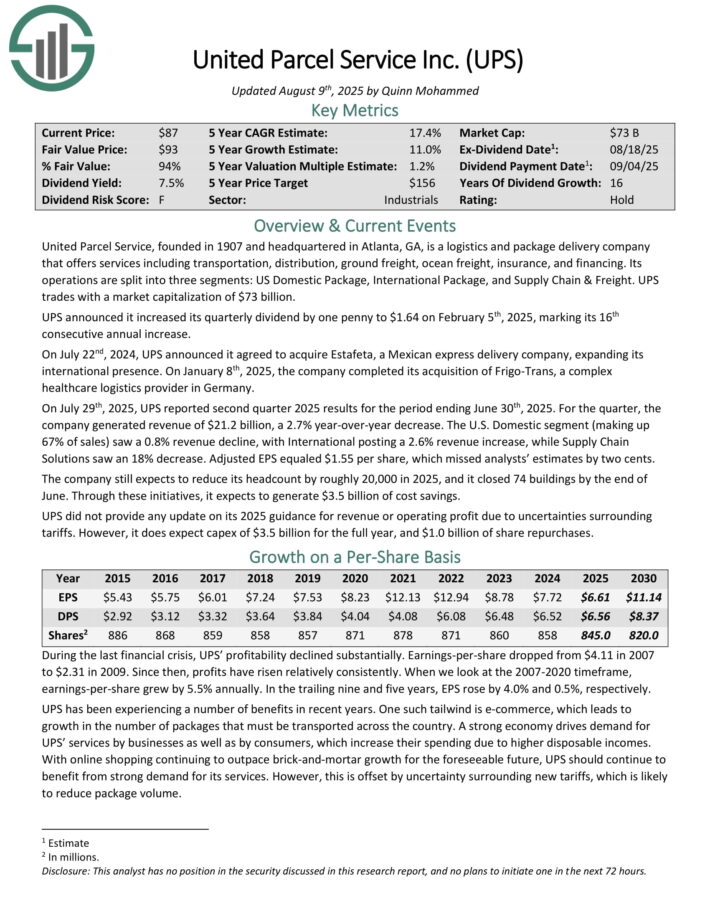

High Yield Blue Chip #4: United Parcel Service (UPS)

- Dividend History: 16 years of consecutive increases

- Dividend Yield: 7.6%

United Parcel Service, founded in 1907 and headquartered in Atlanta, GA, is a logistics and package delivery company that offers services including transportation, distribution, ground freight, ocean freight, insurance, and financing.

Its operations are split into three segments: US Domestic Package, International Package, and Supply Chain & Freight.

On July 22nd, 2024, UPS announced it agreed to acquire Estafeta, a Mexican express delivery company, expanding its international presence. On January 8th, 2025, the company completed its acquisition of Frigo-Trans, a complex healthcare logistics provider in Germany.

On July 29th, 2025, UPS reported second quarter 2025 results for the period ending June 30th, 2025. For the quarter, the company generated revenue of $21.2 billion, a 2.7% year-over-year decrease.

The U.S. Domestic segment (making up 67% of sales) saw a 0.8% revenue decline, with International posting a 2.6% revenue increase, while Supply Chain Solutions saw an 18% decrease. Adjusted EPS equaled $1.55 per share, which missed analysts’ estimates by two cents.

The company still expects to reduce its headcount by roughly 20,000 in 2025, and it closed 74 buildings by the end of June. Through these initiatives, it expects to generate $3.5 billion of cost savings.

Click here to download our most recent Sure Analysis report on UPS (preview of page 1 of 3 shown below):

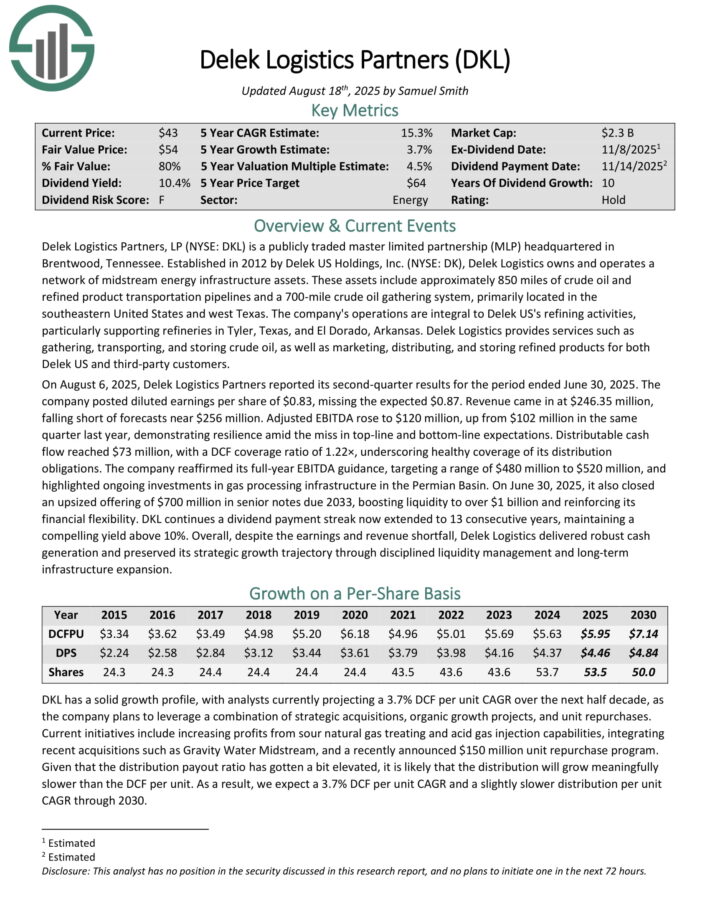

High Yield Blue Chip #3: Delek Logistics Partners LP (DKL)

- Dividend History: 10 years of consecutive increases

- Dividend Yield: 9.7%

Delek Logistics Partners, LP is a publicly traded master limited partnership (MLP) headquartered in Brentwood, Tennessee. Established in 2012 by Delek US Holdings, Inc. (NYSE: DK), Delek Logistics owns and operates a network of midstream energy infrastructure assets.

These assets include approximately 850 miles of crude oil and refined product transportation pipelines and a 700-mile crude oil gathering system, primarily located in the southeastern United States and west Texas.

The company’s operations are integral to Delek US’s refining activities, particularly supporting refineries in Tyler, Texas, and El Dorado, Arkansas.

Delek Logistics provides services such as gathering, transporting, and storing crude oil, as well as marketing, distributing, and storing refined products for both Delek US and third-party customers.

On August 6, 2025, Delek Logistics Partners reported its second-quarter results for the period ended June 30, 2025. The company posted diluted earnings per share of $0.83, missing the expected $0.87.

Revenue came in at $246.35 million, falling short of forecasts near $256 million. Adjusted EBITDA rose to $120 million, up from $102 million in the same quarter last year, demonstrating resilience amid the miss in top-line and bottom-line expectations.

Distributable cash flow reached $73 million, with a DCF coverage ratio of 1.22×, underscoring healthy coverage of its distribution obligations.

The company reaffirmed its full-year EBITDA guidance, targeting a range of $480 million to $520 million, and highlighted ongoing investments in gas processing infrastructure in the Permian Basin.

Click here to download our most recent Sure Analysis report on DKL (preview of page 1 of 3 shown below):

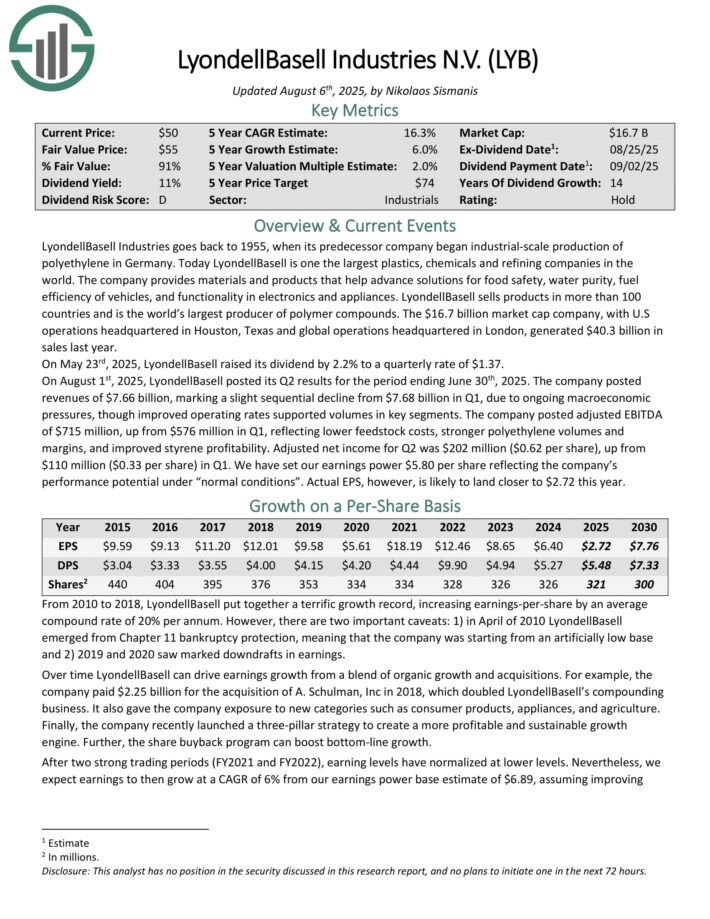

High Yield Blue Chip #2: LyondellBasell Industries (LYB)

- Dividend History: 14 years of consecutive increases

- Dividend Yield: 10.4%

LyondellBasell is one the largest plastics, chemicals and refining companies in the world. The company provides materials and products that help advance solutions for food safety, water purity, fuel efficiency of vehicles, and functionality in electronics and appliances.

LyondellBasell sells products in more than 100 countries and is the world’s largest producer of polymer compounds. The company, with U.S operations headquartered in Houston, Texas and global operations headquartered in London, generated $40.3 billion in sales last year.

On August 1st, 2025, LyondellBasell posted its Q2 results. The company posted revenues of $7.66 billion, marking a slight sequential decline from $7.68 billion in Q1, due to ongoing macroeconomic pressures, though improved operating rates supported volumes in key segments.

The company posted adjusted EBITDA of $715 million, up from $576 million in Q1, reflecting lower feedstock costs, stronger polyethylene volumes and margins, and improved styrene profitability.

Adjusted net income for Q2 was $202 million ($0.62 per share), up from $110 million ($0.33 per share) in Q1.

Click here to download our most recent Sure Analysis report on LYB (preview of page 1 of 3 shown below):

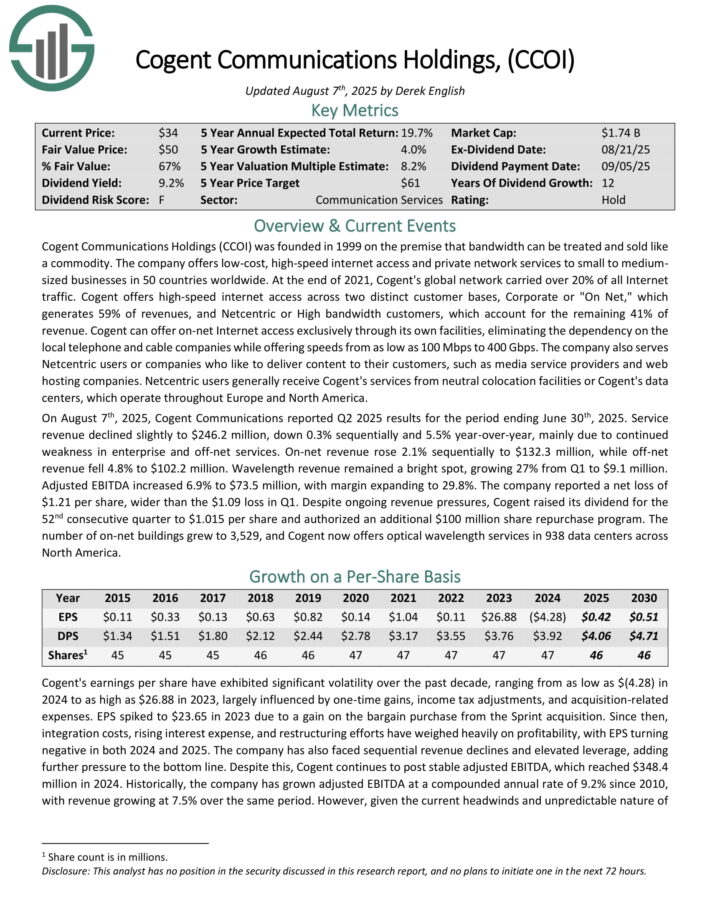

High Yield Blue Chip #1: Cogent Communications Holdings (CCOI)

- Dividend History: 12 years of consecutive increases

- Dividend Yield: 10.7%

Cogent Communications Holdings (CCOI) was founded in 1999 on the premise that bandwidth can be treated and sold like a commodity. The company offers low-cost, high-speed internet access and private network services to small to medium-sized businesses in 50 countries worldwide.

Cogent offers high-speed internet access across two distinct customer bases, Corporate or “On Net,” which generates 59% of revenues, and Netcentric or High bandwidth customers, which account for the remaining 41% of revenue.

Cogent can offer on-net Internet access exclusively through its own facilities, eliminating the dependency on the local telephone and cable companies while offering speeds from as low as 100 Mbps to 400 Gbps.

The company also serves Netcentric users or companies who like to deliver content to their customers, such as media service providers and web hosting companies.

On August 7th, 2025, Cogent Communications reported Q2 2025 results for the period ending June 30th, 2025. Service revenue declined slightly to $246.2 million, down 0.3% sequentially and 5.5% year-over-year, mainly due to continued weakness in enterprise and off-net services.

On-net revenue rose 2.1% sequentially to $132.3 million, while off-net revenue fell 4.8% to $102.2 million. Wavelength revenue remained a bright spot, growing 27% from Q1 to $9.1 million.

Adjusted EBITDA increased 6.9% to $73.5 million, with margin expanding to 29.8%. The company reported a net loss of $1.21 per share, wider than the $1.09 loss in Q1.

Click here to download our most recent Sure Analysis report on CCOI (preview of page 1 of 3 shown below):

Additional Reading

If you are interested in finding other high-yield securities, the following Sure Dividend resources may be useful:

High-Yield Individual Security Research

- 20 High-Dividend Stocks Under $10

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Super High Dividend REITs

- 4 Highest Yielding Royalty Trusts

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- Monthly Dividend Stocks: Individual securities that pay out every month