Published on August 29th, 2025 by Bob Ciura

Investors looking for the best stocks for the long run should consider dividend growth stocks.

More specifically, we believe stocks that can raise their dividends each year, regardless of the broader economic climate, are the best dividend stocks to buy and hold.

The Dividend Kings are the best-of-the-best in dividend longevity.

What is a Dividend King? A stock with 50 or more consecutive years of dividend increases.

You can see the full downloadable spreadsheet of all 56 Dividend Kings (along with important financial metrics such as dividend yields, payout ratios, and price-to-earnings ratios) by clicking on the link below:

The list includes 10 Dividend Kings with our highest Dividend Risk Score of ‘A’ in the Sure Analysis Research Database, that also have the highest dividend growth rates.

The stocks are sorted by dividend growth rate, in ascending order.

Table of Contents

- Dividend King For The Long Run: RPM International (RPM)

- Dividend King For The Long Run: Abbott Laboratories (ABT)

- Dividend King For The Long Run: Illinois Tool Works (ITW)

- Dividend King For The Long Run: S&P Global (SPGI)

- Dividend King For The Long Run: Middlesex Water Co. (MSEX)

- Dividend King For The Long Run: Automatic Data Processing (ADP)

- Dividend King For The Long Run: Lowe’s Companies (LOW)

- Dividend King For The Long Run: Nordson Corp. (NDSN)

- Dividend King For The Long Run: Parker-Hannifin Corp. (PH)

- Dividend King For The Long Run: Nucor Corp. (NUE)

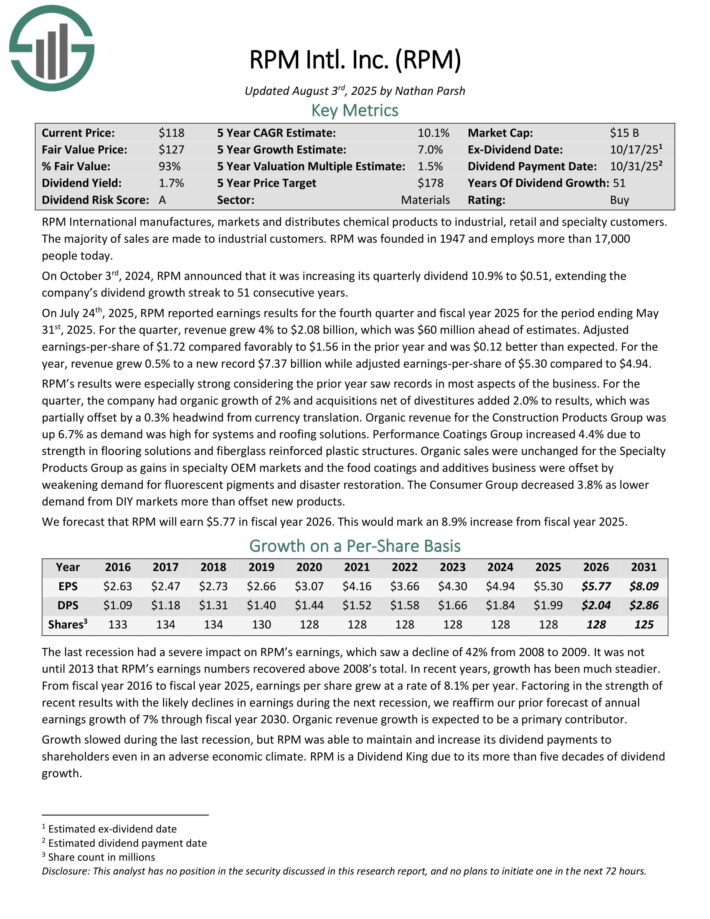

Dividend King For The Long Run: RPM International (RPM)

- Dividend Growth Rate: 7.0%

RPM International manufactures, markets and distributes chemical products to industrial, retail and specialty customers. The majority of sales are made to industrial customers.

On July 24th, 2025, RPM reported earnings results for the fourth quarter and fiscal year 2025 for the period ending May 31st, 2025. For the quarter, revenue grew 4% to $2.08 billion, which was $60 million ahead of estimates. Adjusted earnings-per-share of $1.72 compared favorably to $1.56 in the prior year and was $0.12 better than expected.

For the year, revenue grew 0.5% to a new record $7.37 billion while adjusted earnings-per-share of $5.30 compared to $4.94. RPM’s results were especially strong considering the prior year saw records in most aspects of the business.

For the quarter, the company had organic growth of 2% and acquisitions net of divestitures added 2.0% to results, which was partially offset by a 0.3% headwind from currency translation.

Organic revenue for the Construction Products Group was up 6.7% as demand was high for systems and roofing solutions.

Click here to download our most recent Sure Analysis report on RPM (preview of page 1 of 3 shown below):

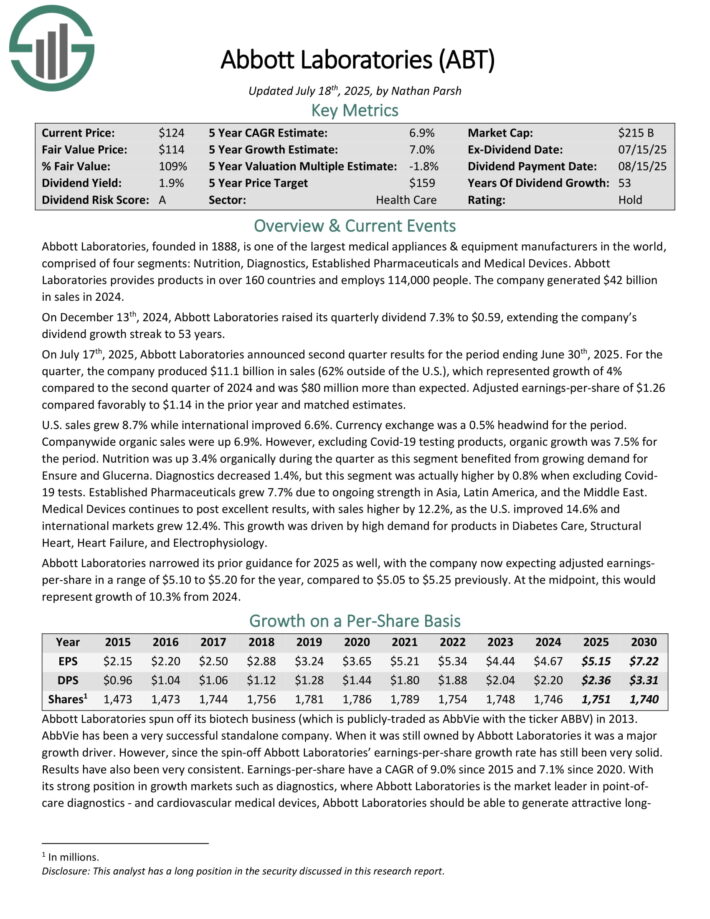

Dividend King For The Long Run: Abbott Laboratories (ABT)

- Dividend Growth Rate: 7.0%

Abbott Laboratories, founded in 1888, is one of the largest medical appliances & equipment manufacturers in the world, comprised of four segments: Nutrition, Diagnostics, Established Pharmaceuticals and Medical Devices.

Abbott Laboratories provides products in over 160 countries and employs 114,000 people. The company generated $42 billion in sales in 2024.

On July 17th, 2025, Abbott Laboratories announced second quarter results for the period ending June 30th, 2025. For the quarter, the company produced $11.1 billion in sales (62% outside of the U.S.), which represented growth of 4% compared to the second quarter of 2024 and was $80 million more than expected. Adjusted earnings-per-share of $1.26 compared favorably to $1.14 in the prior year and matched estimates.

U.S. sales grew 8.7% while international improved 6.6%. Currency exchange was a 0.5% headwind for the period. Companywide organic sales were up 6.9%. However, excluding Covid-19 testing products, organic growth was 7.5% for the period. Nutrition was up 3.4% organically during the quarter as this segment benefited from growing demand for Ensure and Glucerna. Diagnostics decreased 1.4%, but this segment was actually higher by 0.8% when excluding Covid19 tests.

Established Pharmaceuticals grew 7.7% due to ongoing strength in Asia, Latin America, and the Middle East. Medical Devices continues to post excellent results, with sales higher by 12.2%, as the U.S. improved 14.6% and international markets grew 12.4%. This growth was driven by high demand for products in Diabetes Care, Structural Heart, Heart Failure, and Electrophysiology.

Click here to download our most recent Sure Analysis report on ABT (preview of page 1 of 3 shown below):

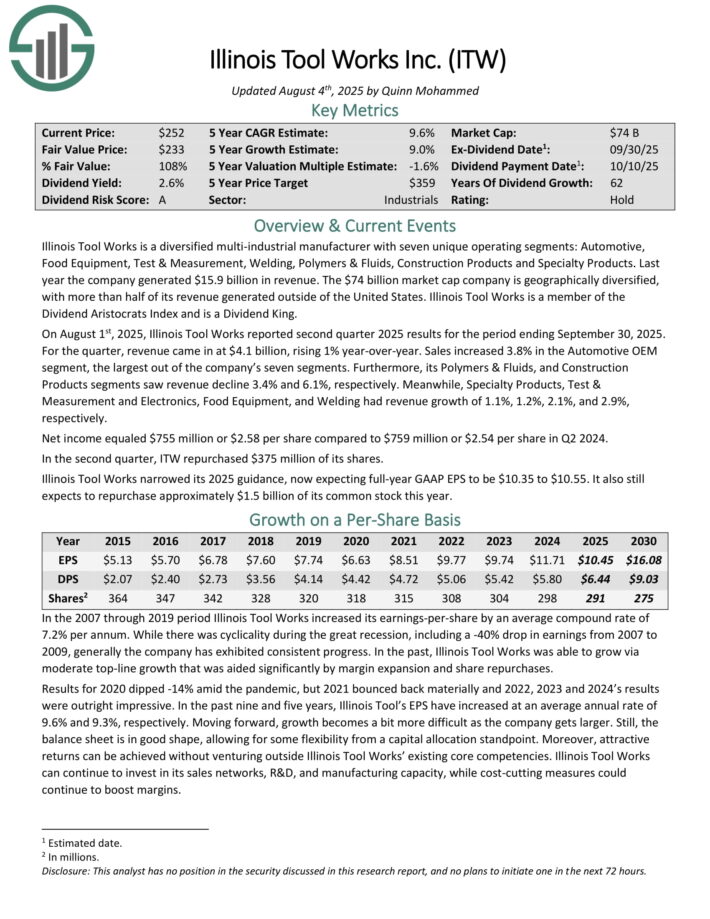

Dividend King For The Long Run: Illinois Tool Works (ITW)

- Dividend Growth Rate: 7.0%

Illinois Tool Works is a diversified multi-industrial manufacturer with seven unique operating segments: Automotive, Food Equipment, Test & Measurement, Welding, Polymers & Fluids, Construction Products and Specialty Products.

Last year the company generated $15.9 billion in revenue. The company is geographically diversified, with more than half of its revenue generated outside of the United States.

On August 1st, 2025, Illinois Tool Works reported second quarter 2025 results. For the quarter, revenue came in at $4.1 billion, rising 1% year-over-year. Sales increased 3.8% in the Automotive OEM segment, the largest out of the company’s seven segments.

Furthermore, its Polymers & Fluids, and Construction Products segments saw revenue decline 3.4% and 6.1%, respectively.

Meanwhile, Specialty Products, Test & Measurement and Electronics, Food Equipment, and Welding had revenue growth of 1.1%, 1.2%, 2.1%, and 2.9%, respectively. Net income equaled $755 million or $2.58 per share compared to $759 million or $2.54 per share in Q2 2024.

Click here to download our most recent Sure Analysis report on ITW (preview of page 1 of 3 shown below):

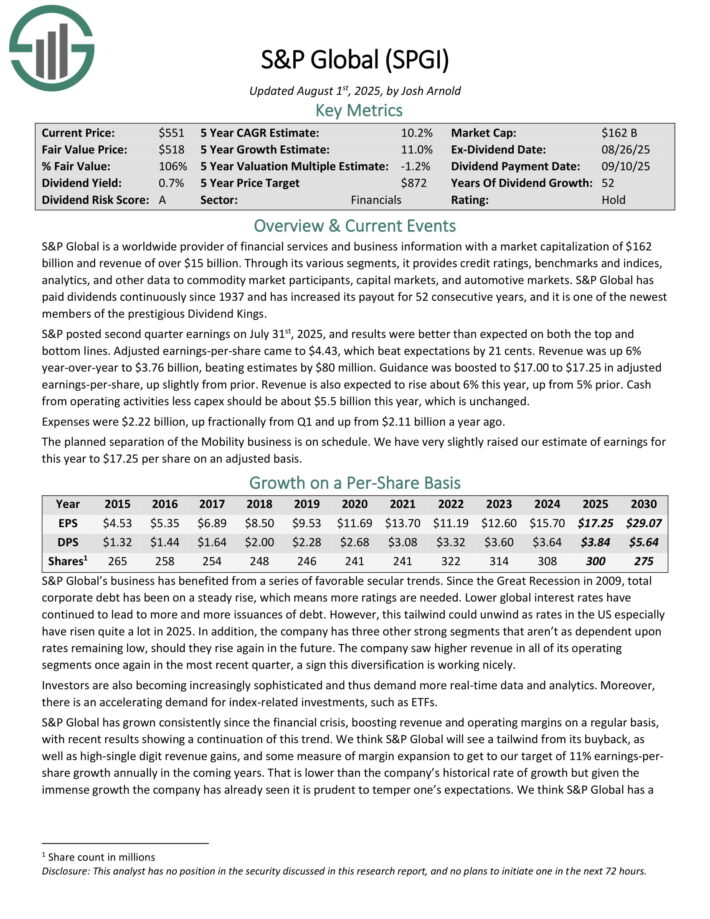

Dividend King For The Long Run: S&P Global (SPGI)

- Dividend Growth Rate: 8.0%

S&P Global is a worldwide provider of financial services and business information and revenue of over $13 billion.

Through its various segments, it provides credit ratings, benchmarks and indices, analytics, and other data to commodity market participants, capital markets, and automotive markets.

S&P Global has paid dividends continuously since 1937 and has increased its payout for 51 consecutive years.

S&P posted second quarter earnings on July 31st, 2025, and results were better than expected on both the top and bottom lines. Adjusted earnings-per-share came to $4.43, which beat expectations by 21 cents. Revenue was up 6% year-over-year to $3.76 billion, beating estimates by $80 million.

Guidance was boosted to $17.00 to $17.25 in adjusted earnings-per-share, up slightly from prior. Revenue is also expected to rise about 6% this year, up from 5% prior.

Cash from operating activities less capex should be about $5.5 billion this year, which is unchanged. Expenses were $2.22 billion, up fractionally from Q1 and up from $2.11 billion a year ago.

Click here to download our most recent Sure Analysis report on SPGI (preview of page 1 of 3 shown below):

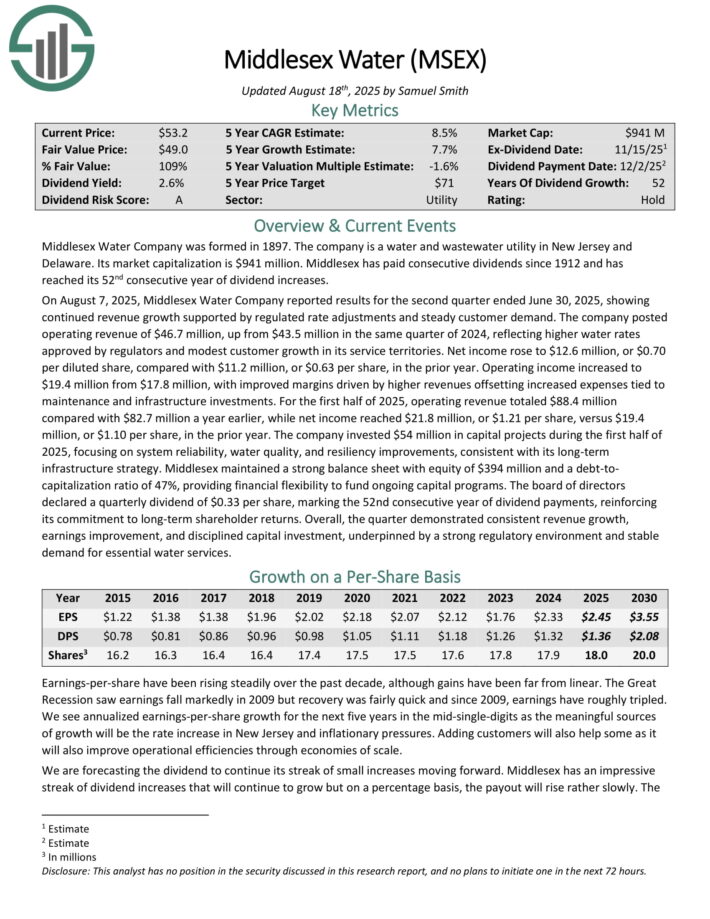

Dividend King For The Long Run: Middlesex Water Co. (MSEX)

- Dividend Growth Rate: 8.9%

Middlesex Water Company was formed in 1897. The company is a water and wastewater utility in New Jersey and Delaware. Middlesex has paid consecutive dividends since 1912.

On August 7, 2025, Middlesex Water Company reported results for the second quarter ended June 30, 2025, showing continued revenue growth supported by regulated rate adjustments and steady customer demand. The company posted operating revenue of $46.7 million, up from $43.5 million in the same quarter of 2024, reflecting higher water rates approved by regulators and modest customer growth in its service territories.

Net income rose to $12.6 million, or $0.70 per diluted share, compared with $11.2 million, or $0.63 per share, in the prior year. Operating income increased to $19.4 million from $17.8 million, with improved margins driven by higher revenues offsetting increased expenses tied to maintenance and infrastructure investments.

For the first half of 2025, operating revenue totaled $88.4 million compared with $82.7 million a year earlier, while net income reached $21.8 million, or $1.21 per share, versus $19.4 million, or $1.10 per share, in the prior year.

The company invested $54 million in capital projects during the first half of 2025, focusing on system reliability, water quality, and resiliency improvements, consistent with its long-term infrastructure strategy. Middlesex maintained a strong balance sheet with equity of $394 million and a debt-to-capitalization ratio of 47%, providing financial flexibility to fund ongoing capital programs.

Click here to download our most recent Sure Analysis report on MSEX (preview of page 1 of 3 shown below):

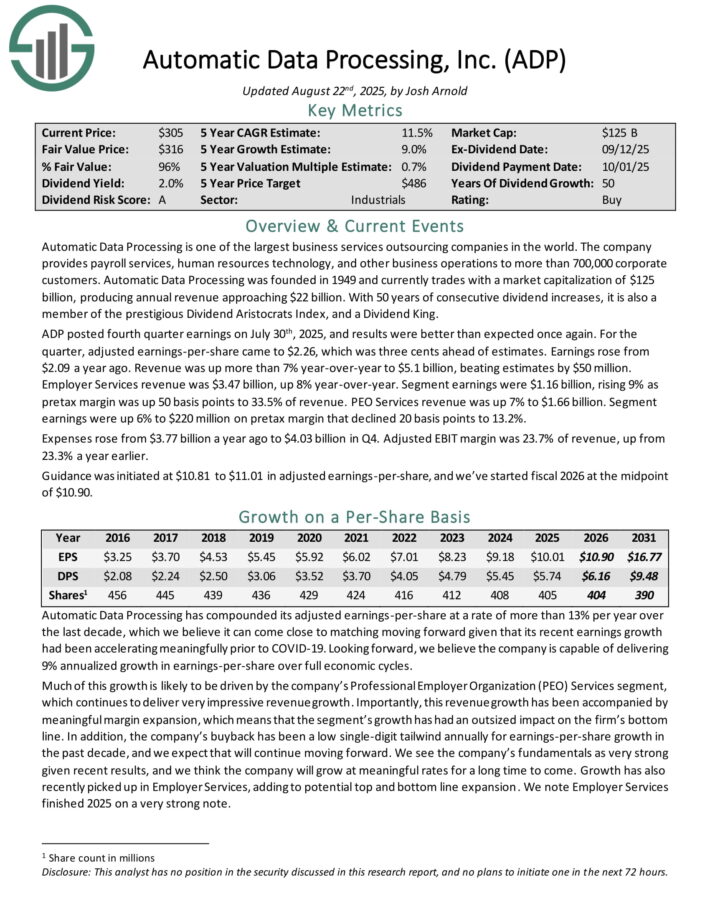

Dividend King For The Long Run: Automatic Data Processing (ADP)

- Dividend Growth Rate: 9.0%

Automatic Data Processing is one of the largest business services outsourcing companies in the world. The company provides payroll services, human resources technology, and other business operations to more than 700,000 corporate customers. Automatic Data Processing produces annual revenue of about $20 billion.

ADP posted fourth quarter earnings on July 30th, 2025, and results were better than expected once again. For the quarter, adjusted earnings-per-share came to $2.26, which was three cents ahead of estimates. Earnings rose from $2.09 a year ago. Revenue was up more than 7% year-over-year to $5.1 billion, beating estimates by $50 million.

Employer Services revenue was $3.47 billion, up 8% year-over-year. Segment earnings were $1.16 billion, rising 9% as pretax margin was up 50 basis points to 33.5% of revenue. PEO Services revenue was up 7% to $1.66 billion. Segment earnings were up 6% to $220 million on pretax margin that declined 20 basis points to 13.2%.

Expenses rose from $3.77 billion a year ago to $4.03 billion in Q4. Adjusted EBIT margin was 23.7% of revenue, up from 23.3% a year earlier. Guidance was initiated at $10.81 to $11.01 in adjusted earnings-per-share.

Click here to download our most recent Sure Analysis report on ADP (preview of page 1 of 3 shown below):

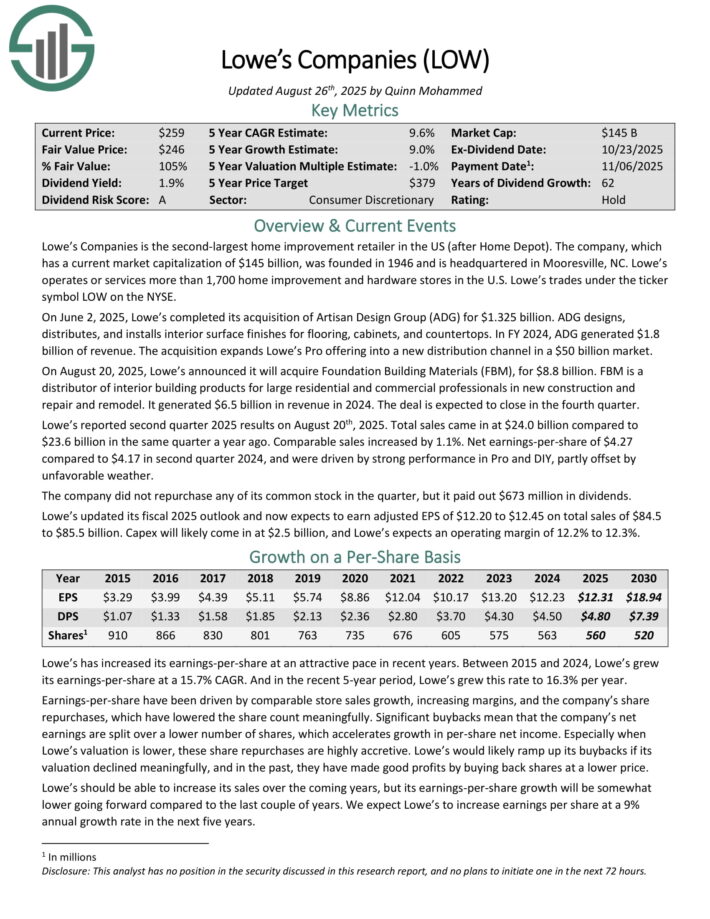

Dividend King For The Long Run: Lowe’s Companies (LOW)

- Dividend Growth Rate: 9.0%

Lowe’s Companies is the second-largest home improvement retailer in the US (after Home Depot). The company was founded in 1946 and is headquartered in Mooresville, NC. Lowe’s operates or services more than 1,700 home improvement and hardware stores in the U.S.

On August 20, 2025, Lowe’s announced it will acquire Foundation Building Materials (FBM), for $8.8 billion. FBM is a distributor of interior building products for large residential and commercial professionals in new construction and repair and remodel. It generated $6.5 billion in revenue in 2024. The deal is expected to close in the fourth quarter.

Lowe’s reported second quarter 2025 results on August 20th, 2025. Total sales came in at $24.0 billion compared to $23.6 billion in the same quarter a year ago. Comparable sales increased by 1.1%. Net earnings-per-share of $4.27 compared to $4.17 in second quarter 2024, and were driven by strong performance in Pro and DIY, partly offset by

unfavorable weather.

The company did not repurchase any of its common stock in the quarter, but it paid out $673 million in dividends. Lowe’s updated its fiscal 2025 outlook and now expects to earn adjusted EPS of $12.20 to $12.45 on total sales of $84.5 to $85.5 billion.

Click here to download our most recent Sure Analysis report on LOW (preview of page 1 of 3 shown below):

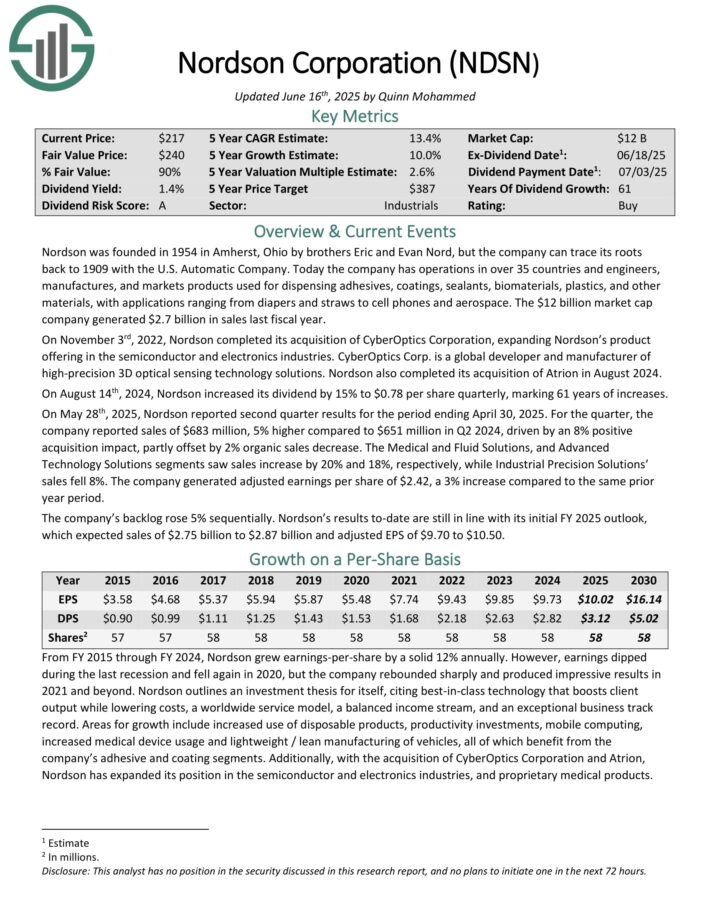

Dividend King For The Long Run: Nordson Corp. (NDSN)

- Dividend Growth Rate: 10.0%

Nordson was founded in 1954. Today the company has operations in over 35 countries and engineers, manufactures, and markets products used for dispensing adhesives, coatings, sealants, biomaterials, plastics, and other materials, with applications ranging from diapers and straws to cell phones and aerospace.

The company generated $2.7 billion in sales last fiscal year.

On May 28th, 2025, Nordson reported second quarter results for the period ending April 30, 2025. For the quarter, the company reported sales of $683 million, 5% higher compared to $651 million in Q2 2024, driven by an 8% positive acquisition impact, partly offset by 2% organic sales decrease.

The Medical and Fluid Solutions, and Advanced Technology Solutions segments saw sales increase by 20% and 18%, respectively, while Industrial Precision Solutions sales fell 8%. The company generated adjusted earnings per share of $2.42, a 3% increase compared to the same prior year period.

The company’s backlog rose 5% sequentially.

Click here to download our most recent Sure Analysis report on NDSN (preview of page 1 of 3 shown below):

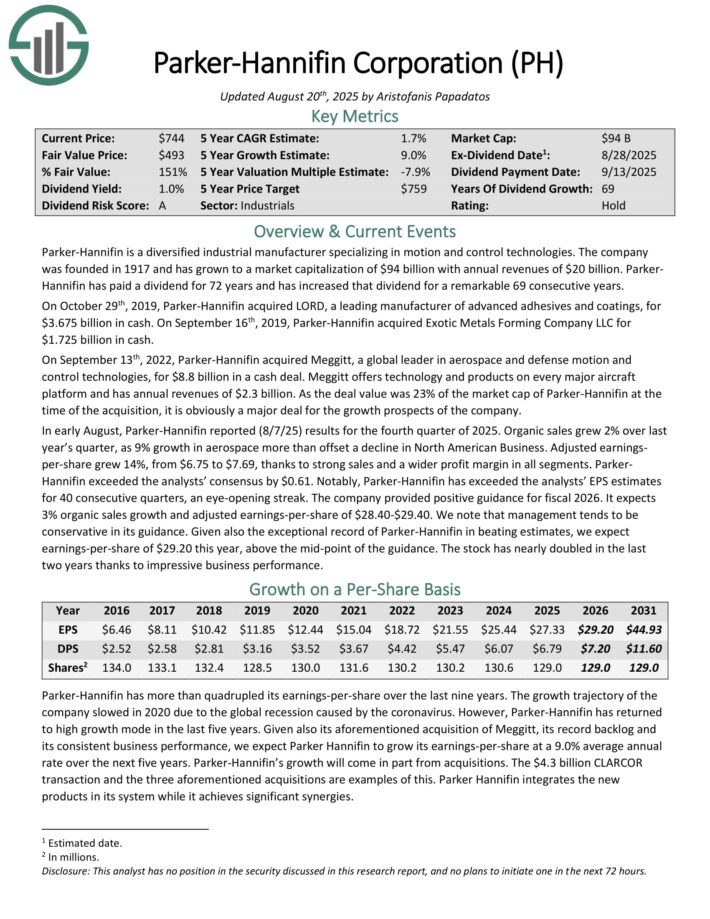

Dividend King For The Long Run: Parker-Hannifin Corp. (PH)

- Payout Ratio: 10.0%

Parker-Hannifin is a diversified industrial manufacturer specializing in motion and control technologies. The company generates annual revenues of $20 billion. Parker-Hannifin has increased the dividend for 69 consecutive years.

In early August, Parker-Hannifin reported (8/7/25) results for the fourth quarter of 2025. Organic sales grew 2% over last year’s quarter, as 9% growth in aerospace more than offset a decline in North American Business. Adjusted earningsper-share grew 14%, from $6.75 to $7.69, thanks to strong sales and a wider profit margin in all segments.

Parker-Hannifin exceeded the analysts’ consensus by $0.61. Notably, Parker-Hannifin has exceeded the analysts’ EPS estimates for 40 consecutive quarters, an eye-opening streak.

The company provided positive guidance for fiscal 2026. It expects 3% organic sales growth and adjusted earnings-per-share of $28.40-$29.40. We note that management tends to be conservative in its guidance.

Click here to download our most recent Sure Analysis report on Parker-Hannifin (preview of page 1 of 3 shown below):

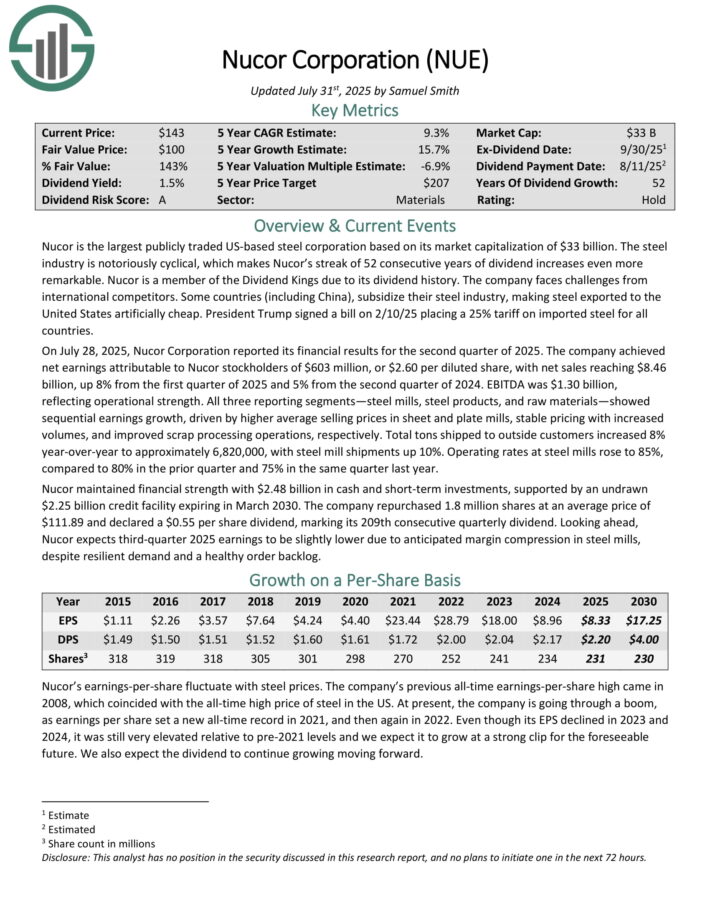

Dividend King For The Long Run: Nucor Corp. (NUE)

- Dividend Growth Rate: 12.7%

Nucor is the largest publicly traded US-based steel corporation based on its market capitalization. The steel industry is notoriously cyclical, which makes Nucor’s streak of 52 consecutive years of dividend increases even more remarkable.

On July 28, 2025, Nucor Corporation reported its financial results for the second quarter of 2025. The company achieved net earnings attributable to Nucor stockholders of $2.60 per diluted share, with net sales reaching $8.46 billion, up 8% from the second quarter of 2024. EBITDA was $1.30 billion, reflecting operational strength.

All three reporting segments—steel mills, steel products, and raw materials—showed sequential earnings growth, driven by higher average selling prices in sheet and plate mills, stable pricing with increased volumes, and improved scrap processing operations, respectively.

Total tons shipped to outside customers increased 8% year-over-year to approximately 6,820,000, with steel mill shipments up 10%. Operating rates at steel mills rose to 85%, compared to 80% in the prior quarter and 75% in the same quarter last year.

Click here to download our most recent Sure Analysis report on NUE (preview of page 1 of 3 shown below):

Final Thoughts & Additional Reading

Screening to find the best Dividend Kings is not the only way to find high-quality dividend growth stocks to hold forever.

Sure Dividend maintains similar databases on the following useful universes of stocks:

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Dividend Aristocrats: S&P 500 stocks with 25+ years of consecutive dividend increases.

- The Complete List of High Dividend Stocks: Stocks with 5%+ dividend yields.

- The Complete List of Monthly Dividend Stocks: our database currently contains roughly 80 stocks that pay dividends every month.