Updated on July 28th, 2026 by Nikolaos Sismanis

With contributions from Ben Reynolds

Business Development Companies (BDCs) make debt and/or equity investments in smaller businesses.

The appeal of BDCs is:

- Exposure to smaller businesses otherwise not available on the stock market

- Required to distribute income to investors

- Typically very high yields

With this in mind, we created a full downloadable spreadsheet list of over 50 BDCs.

You can download the Excel spreadsheet (along with relevant financial metrics like dividend yield and payout ratios) by clicking on the link below:

This research report will provide an overview of BDCs, along with our top 5 BDCs right now as ranked by expected total returns from the Sure Analysis Research Database.

Table Of Contents

The table of contents below provides for easy navigation of the article:

- Overview of BDCs

- Why Invest In BDCs?

- Tax Considerations Of BDCs

- The Top 5 BDCs Today

- #5: Stellus Capital Investment Corporation (SCM)

- #4: Horizon Technology Finance Corporation (HRZN)

- #3: PennantPark Floating Rate Capital Ltd. (PFLT)

- #2: Saratoga Investment Corp. (SAR)

- #1: PennantPark Investment Corporation (PNNT)

- Final Thoughts

Overview of BDCs

Business Development Companies are closed-end investment firms. Their business model involves making debt and/or equity investments in other companies, typically small or mid-size businesses.

These target companies may not have access to traditional means of raising capital, which makes them suitable partners for a BDC. BDCs invest in a variety of companies, including turnarounds, developing, or distressed companies.

BDCs are registered under the Investment Company Act of 1940. As they are publicly-traded, BDCs must also be registered with the Securities and Exchange Commission.

To qualify as a BDC, the firm must invest at least 70% of its assets in private or publicly-held companies with market capitalizations of $250 million or below.

BDCs make money by investing with the goal of generating income, as well as capital gains on their investments if and when they are sold.

In this way, BDCs operate similar business models as a private equity firm or venture capital firm.

The major difference is that private equity and venture capital investment is typically restricted to accredited investors, while anyone can invest in publicly-traded BDCs.

Why Invest In BDCs?

The obvious appeal for BDCs is their high dividend yields. It is not uncommon to find BDCs with dividend yields above 5%. In some cases, certain BDCs provide 10%+ yields.

Of course, investors should conduct a thorough amount of due diligence, to make sure the underlying fundamentals support the dividend.

Indeed, there are multiple risk factors that investors should know before they invest in BDCs.

First and foremost, BDCs are often heavily indebted.

This is commonplace across BDCs, as their business model involves borrowing to make investments in other companies. The end result is that BDCs are often significantly leveraged companies.

When the economy is strong and markets are rising, leverage can help amplify positive returns.

However, the flip side is that leverage can accelerate losses as well, which can happen in bear markets or recessions.

Another risk to be aware of is interest rates. Since the BDC business model heavily utilizes debt, investors should understand the interest rate environment before investing.

Rising interest rates can negatively affect BDCs if it causes a spike in borrowing costs.

Lastly, credit risk is an additional consideration for investors. As previously mentioned, BDCs make investments in small to mid-size businesses.

Therefore, the quality of the BDC’s portfolio must be assessed, to make sure the BDC will not experience a high level of defaults within its investment portfolio.

This would cause adverse results for the BDC itself, which could negatively impact its ability to maintain distributions to shareholders.

Another unique characteristic of BDCs that investors should know before buying is taxation.

Tax Considerations Of BDCs

BDC dividends are typically not fully (or even mostly) “qualified dividends” for tax purposes, which is generally a more favorable tax rate.

Instead, BDC distributions are taxable at the investor’s ordinary income rates, while the BDC’s capital gains and qualified dividend income is taxed at capital gains rates.

Business Development Companies must pay out 90%+ of their income as distributions. In this way, BDCs are very similar to Real Estate Investment Trusts.

Another factor to keep in mind is that approximately 70% to 80% of BDC dividend income is typically derived from ordinary income.

As a result, BDCs are widely considered to be good candidates for a tax-advantaged retirement account such as an IRA or 401k.

BDCs pay their distributions as a mix of ordinary income and non-qualified dividends, qualified dividends, return of capital, and capital gains.

Returns of capital reduce your tax basis. Qualified dividends and long-term capital gains are taxed at lower rates, while ordinary income and non-qualified dividends are taxed at your personal income tax bracket rate.

The Top 5 BDCs Today

With all this in mind, here are our top 5 BDCs today, ranked according to their expected annual returns over the next five years.

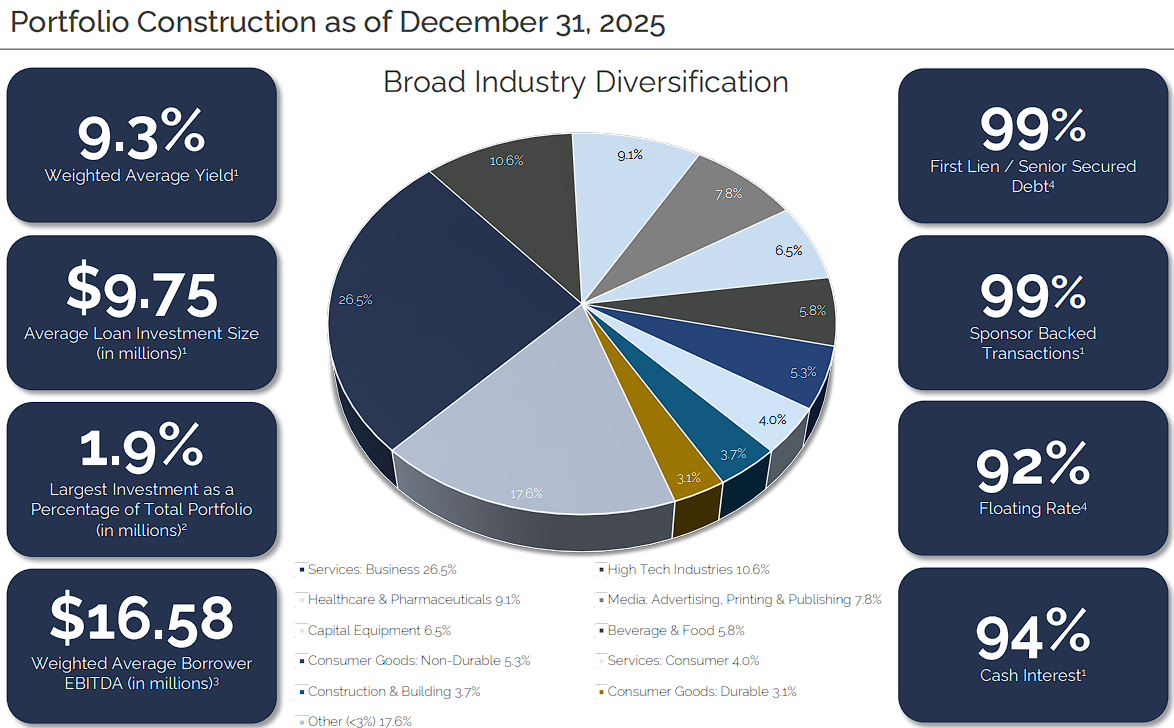

BDC #5: Stellus Capital Investment Corporation (SCM)

- 5-year expected annual return: 13.9%

Stellus Capital Investment Corporation is an externally managed BDC focused mainly on first-lien, unitranche, second-lien, and mezzanine loans to private middle-market companies.

Its borrowers generally produce between $5 million and $50 million of EBITDA, while selective equity co-investments provide some upside beyond interest income.

On May 11th, 2026, Stellus reported first-quarter net investment income of $0.26 per share and core NII of $0.27, down from $0.35 and $0.37, respectively, a year earlier.

The portfolio ended the quarter at $990 million at fair value, compared with $1.008 billion at year-end, as $42 million of repayments exceeded $28 million of new investments.

NAV also eased from $12.82 to $12.54 per share. The portfolio’s effective yield remained attractive at 9.0%, although it declined from 9.3% at the end of 2025.

The dividend deserves close attention. Stellus declared $0.34 per share for the quarter, paid in monthly installments of $0.1133, but core NII covered only about 79% of that amount.

Management noted that the distribution is not expected to include a return of capital, and shareholders have received $18.49 per share since inception.

Still, coverage will need to recover if the present monthly rate is to remain dependable over time.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on SCM.

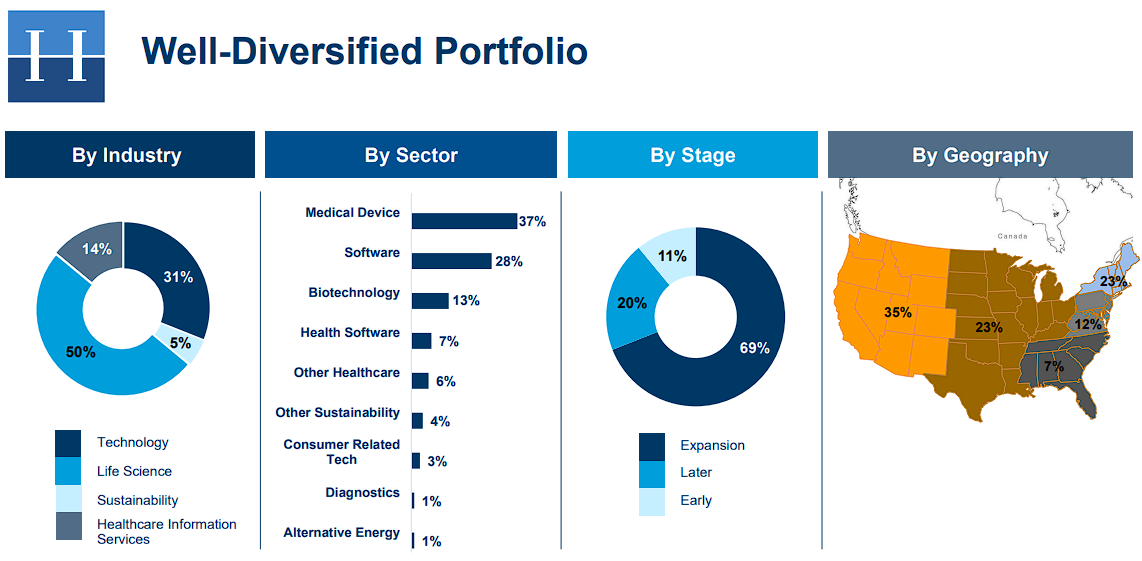

BDC #4: Horizon Technology Finance Corporation (HRZN)

- 5-year expected annual return: 14.6%

Horizon Technology Finance Corporation provides venture debt to development-stage companies in technology, life sciences, healthcare information and services, and sustainability.

Its senior secured loans produce high current yields, while warrants and equity positions can add capital gains when portfolio companies are sold or complete public offerings.

On May 5th, 2026, Horizon reported first-quarter total investment income of $24.1 million, little changed from $24.5 million a year earlier.

NII declined to $9.0 million, or $0.19 per share, from $0.27 per share, while NAV finished the quarter at $6.98 per share.

Horizon’s debt portfolio still produced a strong 15.2% annualized yield, and the company ended March with $180 million of committed backlog.

Credit and valuation risk remain meaningful, however, as venture-backed borrowers can be particularly sensitive to weak fundraising markets.

The biggest change was the April merger with Monroe Capital Corporation. Horizon received $141.1 million of cash and issued about 20.4 million shares to former Monroe shareholders, creating a larger and more diversified platform.

The regular monthly dividend was reduced from $0.11 to $0.06, although $0.03 monthly special distributions are being paid for July through September from spillover income.

You should therefore value the shares using the lower regular rate, since the temporary supplement is not a permanent substitute for stronger NII coverage.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on HRZN.

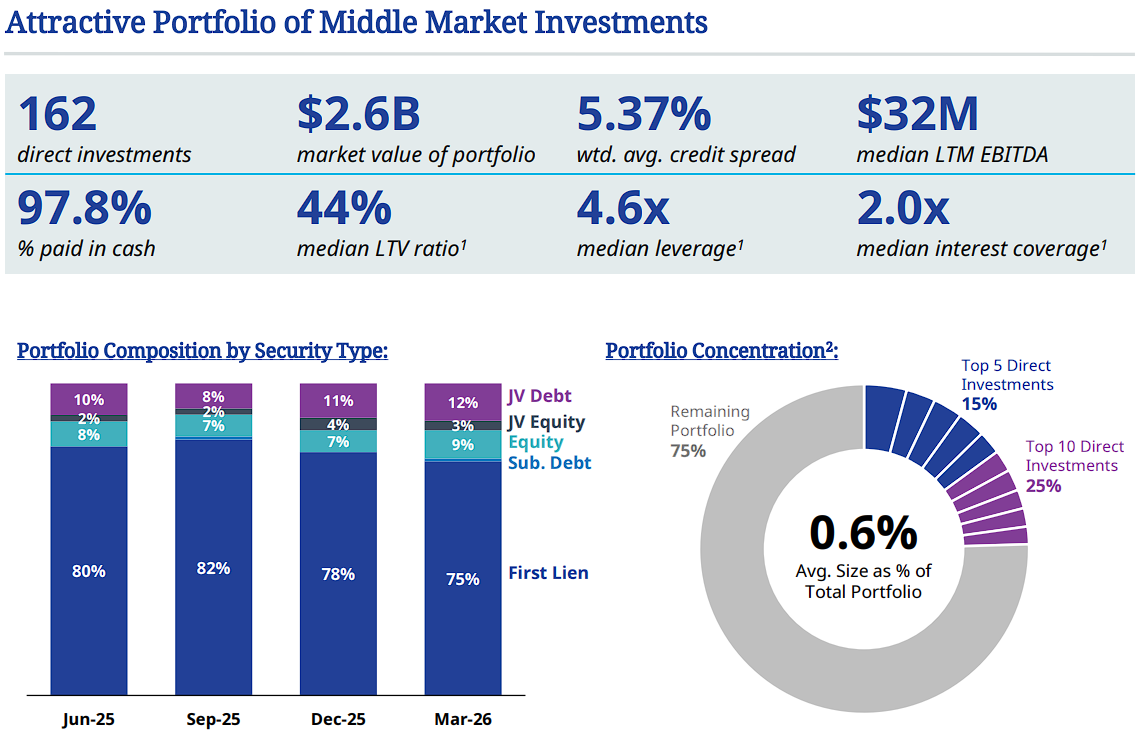

BDC #3: PennantPark Floating Rate Capital Ltd. (PFLT)

- 5-year expected annual return: 16.8%

PennantPark Floating Rate Capital Ltd. lends primarily to U.S. middle-market businesses through first-lien, floating-rate debt.

This structure limits direct duration risk and allows asset yields to adjust with short-term rates, but falling benchmark rates can also reduce portfolio income faster than funding costs reset.

On May 7th, 2026, PFLT reported results for its fiscal second quarter ended March 31st. Investment income increased to $66.0 million from $61.9 million a year earlier.

NII was $25.7 million, or $0.26 per share, compared with $0.28 per share in the prior-year period.

The investment portfolio stood at $2.58 billion, NAV was $10.47 per share, and the weighted average yield on debt investments was 9.8%.

PFLT’s two senior-loan joint ventures had combined portfolios of roughly $1.55 billion, giving the company another avenue for deploying capital.

The dividend policy was reset as lower rates and competitive lending spreads pressured earnings.

Beginning with the July payment, the monthly base distribution fell to $0.08 from $0.1025, supplemented by $0.0033 per month for July through September.

Management intends to calculate future supplements based on excess NII, which should more closely align distributions with recurring earnings.

That is a healthier framework, but it also means you should not assume the former payout will return soon.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on PFLT.

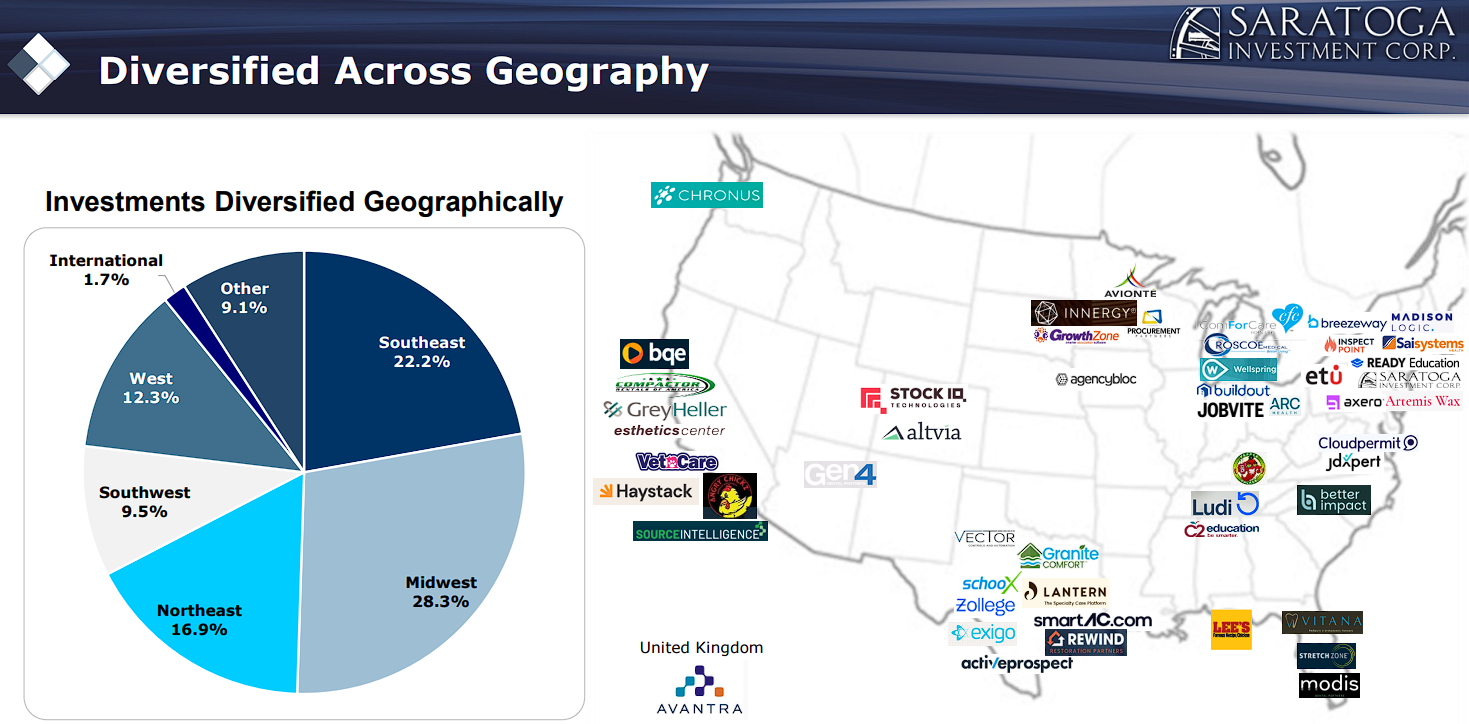

BDC #2: Saratoga Investment Corp. (SAR)

- 5-year expected annual return: 19.1%

Saratoga Investment Corp. provides debt and equity capital to U.S. middle-market companies.

Alongside its core lending portfolio, Saratoga manages a collateralized loan obligation, a joint venture, and a growing portfolio of BB- and BBB-rated CLO debt, giving it a broader mix of income sources than many smaller BDCs.

On July 7th, 2026, Saratoga reported results for its fiscal first quarter ended May 31st. Assets under management increased 1.6% sequentially to $1.126 billion as originations of $79.2 million exceeded repayments of $48.4 million.

Adjusted NII came to $0.47 per share, down from $0.53 in the previous quarter and $0.66 a year earlier.

NAV declined 4.9% sequentially to $23.23 per share after $15.2 million of net portfolio depreciation.

Credit statistics were mixed: non-accruals improved to zero at fair value, but several investments remained on the red watchlist.

Saratoga continues to pay $0.25 per month, or $0.75 each quarter.

Its annual base dividend rose from $2.44 in fiscal 2023 to $3.00 in fiscal 2026, with special dividends lifting the latter year’s total to $3.25.

Still, the latest quarterly dividend exceeded adjusted NII by $0.28 per share and contributed to the NAV decline.

The income is appealing, but we need better coverage before we can consider the payout secure.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on SAR.

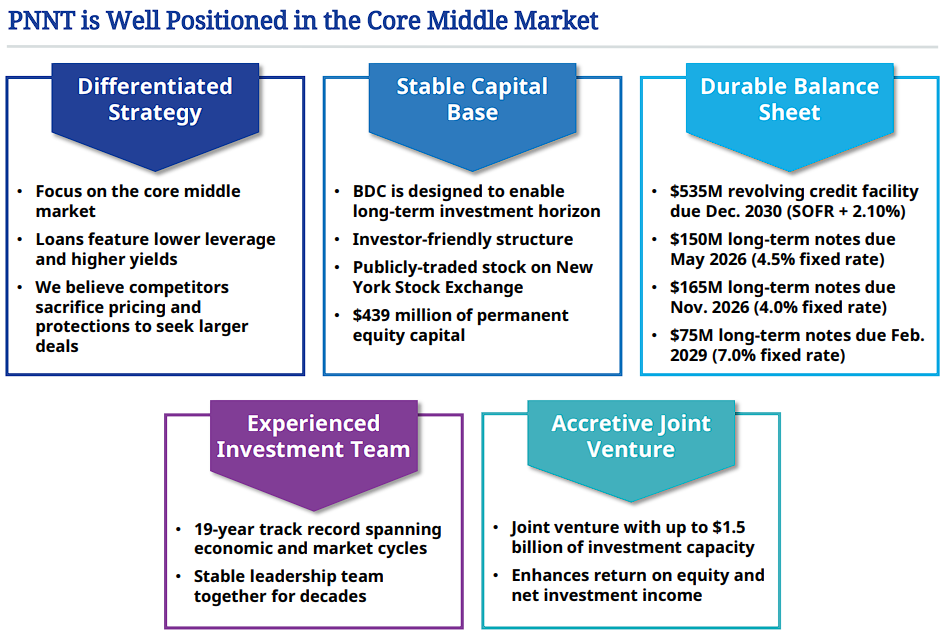

BDC #1: PennantPark Investment Corporation (PNNT)

- 5-year expected annual return: 21.2%

PennantPark Investment Corporation invests in first- and second-lien loans, subordinated debt, and equity issued by U.S. middle-market businesses.

Compared with a senior-loan-focused BDC, PNNT’s larger allocation to subordinated debt and equity can enhance returns, but it also makes NAV more sensitive to portfolio-company performance and market valuations.

On May 7th, 2026, PNNT reported results for its fiscal second quarter ended March 31st. Investment income declined to $24.9 million from $30.7 million a year earlier.

NII was $9.3 million, or $0.14 per share, while NAV fell 3.9% sequentially to $6.73. The $1.20 billion portfolio included 162 companies and carried a 10.9% weighted average yield on interest-bearing debt.

Non-accruals remained manageable at 1.3% of fair value, although net unrealized depreciation of $12.2 million weighed on book value during the quarter.

PNNT currently pays $0.08 per month, split evenly between a $0.04 base dividend and a $0.04 supplemental distribution.

That distinction matters because quarterly NII of $0.14 did not cover the $0.24 distributed during the period.

The lower base rate gives management more flexibility, but maintaining the supplement will require improved recurring income or support from realized gains.

PNNT offers the highest projected return in this ranking, yet its payout coverage and equity exposure also make it the most speculative income choice.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on PNNT.

Final Thoughts

BDCs can provide unusually high income, but we believe the headline yield should be the beginning of the analysis — not the conclusion.

Before buying, you should evaluate recurring NII with the regular dividend and review NAV trends and non-accruals.

It’s also important to determine how much of the payout depends on supplemental distributions or spillover income.

Treat our ranking as a research shortlist, not necessarily a buy list.

After all, PNNT and SAR offer the highest projected returns, but both currently distribute more than they earn from recurring investment income. This makes their dividends particularly unsafe.

PFLT has already reset its payout, while HRZN’s special distributions are temporary.

If you prioritize dividend stability over maximum yield, you may want to wait for clearer coverage before committing capital.

At Sure Dividend, we often advocate for investing in companies with a high probability of increasing their dividends each and every year.

If that strategy appeals to you, it may be useful to browse through the following databases of dividend growth stocks:

- The Dividend Aristocrats List: S&P 500 stocks with 25+ years of dividend increases.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of stocks with 50+ years of consecutive dividend increases.

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 4% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in the S&P 500.