Article updated on August 7th, 2026 by Nick Sismanis

Spreadsheet data updated daily

High dividend stocks are stocks with a dividend yield well in excess of the S&P 500’s average dividend yield of ~1.0%.

The resources in this report focus on truly high yielding securities (4.0%+ yields), with dividend yields multiples higher than the market average.

Resource #1: The High Dividend Stocks List Spreadsheet

The free high dividend stocks list spreadsheet has our complete list of ~200 individual securities (stocks, REITs, MLPs, etc.) with 4%+ dividend yields that we cover in the Sure Analysis Research Database.

This spreadsheet contains important metrics, including: years of dividend growth, dividend yields, payout ratios, buy/hold/sell ratings, fair value prices, expected total returns, and much more.

Resource #2: The 10 Best High Yield Stocks Now

This resource analyzes the 10 best high-yield stocks in detail. The criteria we use to rank high dividend securities in this resource are:

- Is in the 900+ income security Sure Analysis Research Database

- Rank based on dividend yield, from highest to lowest

- Dividend Risk Scores of C or better

- Based in the U.S.

Click below to jump to analysis on any of the Top 10:

- High Dividend Stock #10: United Bancorp, Inc. (UBCP)

- High Dividend Stock #9: Edison International (EIX)

- High Dividend Stock #8: Realty Income (O)

- High Dividend Stock #7: Comcast Corporation (CMCSA)

- High Dividend Stock #6: NNN REIT, Inc. (NNN)

- High Dividend Stock #5: Solvay Bank Corp. (SOBS)

- High Dividend Stock #4: Albertsons Companies, Inc. (ACI)

- High Dividend Stock #3: Enterprise Products Partners L.P. (EPD)

- High Dividend Stock #2: Altria Group, Inc. (MO)

- High Dividend Stock #1: Universal Corporation (UVV)

Resource #3: The High Dividend 50 Series

This series provides our most recent 3-Page PDF report for the 50 highest-yielding securities in the Sure Analysis Research Database now. Nearly all securities in Sure Analysis are updated quarterly.

Click here to jump to this resource now.

High Dividend Stock #10: United Bancorp, Inc. (UBCP)

- Dividend Risk Score: C

- Dividend Yield: 4.9%

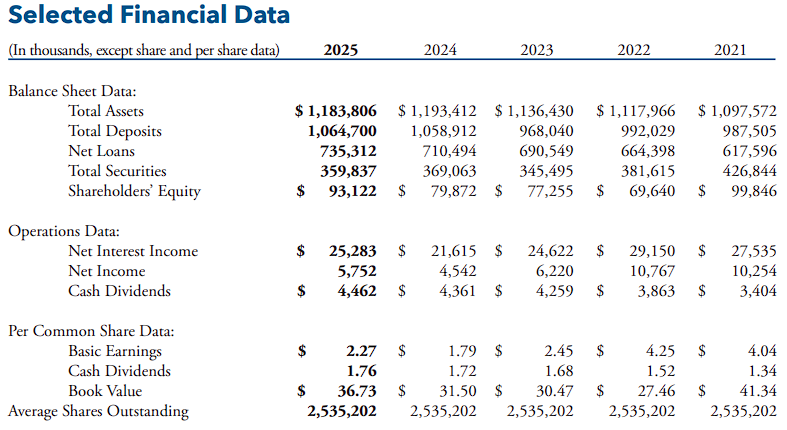

United Bancorp, Inc. is the holding company for Unified Bank, a community bank with 19 banking centers across eastern and southeastern Ohio and parts of West Virginia.

Its small scale and concentrated operating footprint create more company-specific risk than a large regional bank, but they also support close customer relationships and a stable deposit franchise.

For the second quarter of 2026, United Bancorp reported net income of $2.1 million, or $0.36 per diluted share, up 9.4% and 9.1%, respectively, from the prior-year period.

Net interest income increased 6.2% to $7.0 million, while the net interest margin expanded to 3.82% from 3.65%.

Deposits reached $686.9 million, increasing $44.0 million during the first half, with lower-cost demand and savings balances accounting for about 70% of the total.

Management continues to invest in banking centers, mortgage lending, treasury management, and technology.

Those initiatives carry upfront expenses, but they can broaden the bank’s earnings base over time.

United Bancorp also raised its regular second-quarter dividend 5.4% to $0.195 per share and paid a $0.175 special dividend earlier in the year.

The regular payout remains the more useful measure of recurring income, and the company has increased its dividend for 13 consecutive years.

High Dividend Stock #9: Edison International (EIX)

- Dividend Risk Score: C

- Dividend Yield: 5.2%

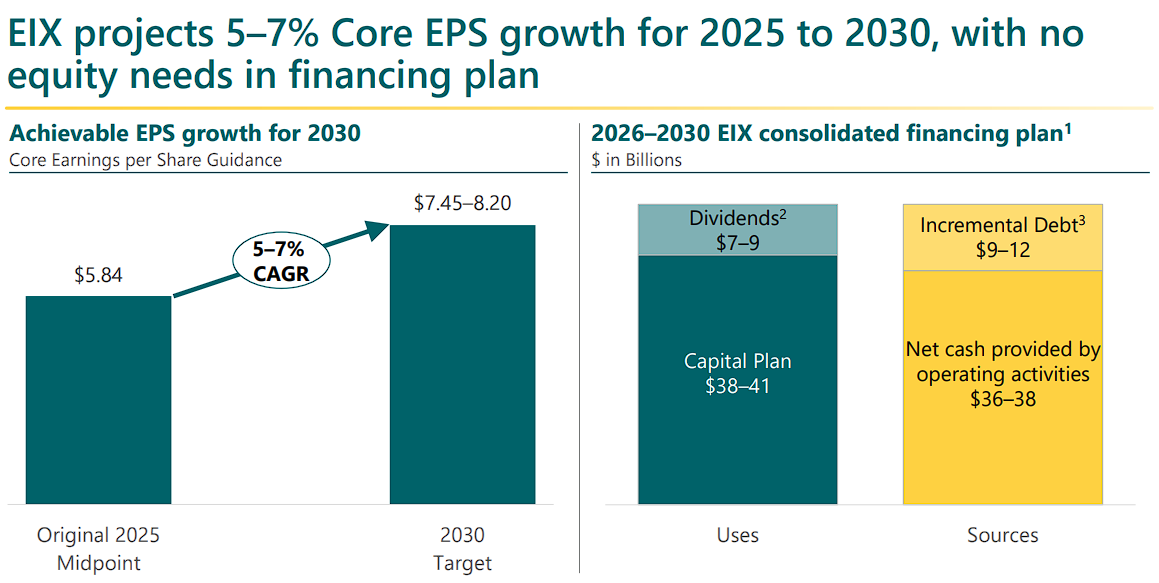

Edison International is the parent of Southern California Edison, which supplies electricity to roughly 15 million people across Southern, Central, and Coastal California.

The company also owns Trio, a smaller collection of nonregulated energy and sustainability advisory businesses.

Edison reported second-quarter 2026 net income of $534 million, or $1.39 per share, compared with $343 million, or $0.89 per share, a year earlier.

Core earnings increased to $592 million, or $1.54 per share, from $374 million, or $0.97 per share.

The improvement primarily reflected the adoption of Southern California Edison’s 2025 general rate case decision.

Management reaffirmed its 2026 core EPS guidance of $5.90 to $6.20 and its longer-term target of 5% to 7% annual core EPS growth through 2030.

The central risk remains wildfire exposure. Southern California Edison continues to harden its system while operating a compensation program for those affected by the Eaton Fire, making the pace and ultimate cost of claims important variables.

Even with that uncertainty, Edison raised its dividend 6% for 2026, marking 22 consecutive years of growth.

The $0.8775 quarterly dividend appears supported by regulated earnings, but the C Dividend Risk Score appropriately recognizes the unusually significant liability and regulatory risks.

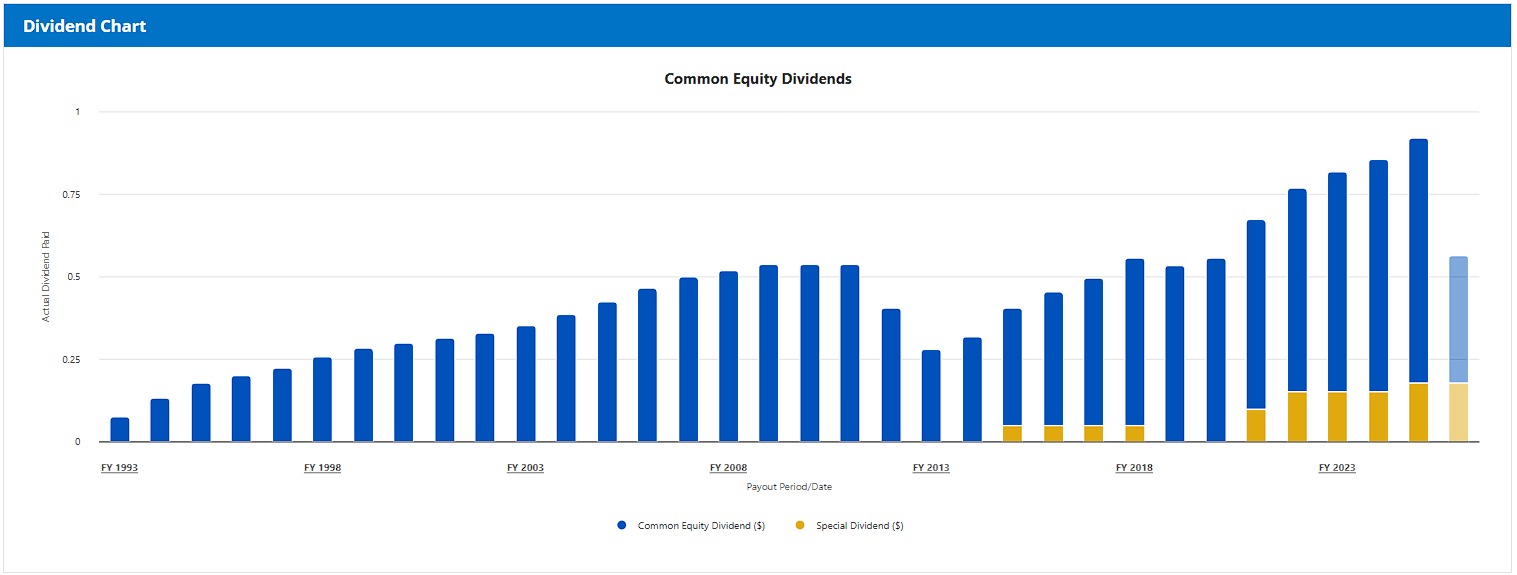

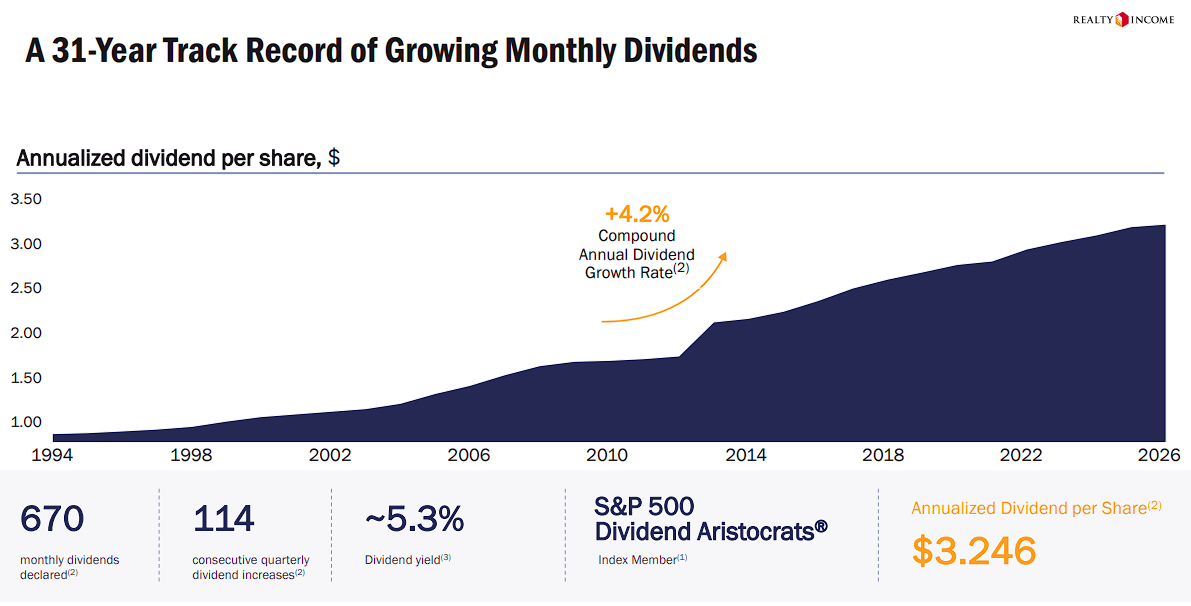

High Dividend Stock #8: Realty Income (O)

- Dividend Risk Score: C

- Dividend Yield: 5.2%

Realty Income is a diversified net-lease REIT known as “The Monthly Dividend Company.”

At the end of the second quarter, it owned or held interests in 15,588 properties leased to 1,798 clients across 92 industries.

Occupancy was 98.8%, and the portfolio’s weighted-average remaining lease term was 8.6 years.

Second-quarter 2026 adjusted funds from operations increased 3.8% to $1.09 per share.

Realty Income invested $2.6 billion during the quarter, or $2.1 billion at its proportionate share, at an initial weighted-average cash yield of 7.3%.

It also achieved 102.7% rent recapture on re-leased properties.

Management raised full-year AFFO guidance to $4.44 to $4.45 per share and increased its investment-volume outlook to $10.0 billion.

The REIT is increasingly using joint ventures and private capital to extend its scale without funding every investment alone.

A newly announced hyperscale data-center joint venture began with more than $6 billion of seed assets, while Fitch assigned Realty Income an A credit rating.

The annualized dividend was $3.252 per share at quarter-end and consumed 74.5% of quarterly AFFO.

Realty Income has declared 673 consecutive monthly dividends and increased its payout for more than 31 consecutive years, making its 5.2% yield notable for its consistency.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on Realty Income (O).

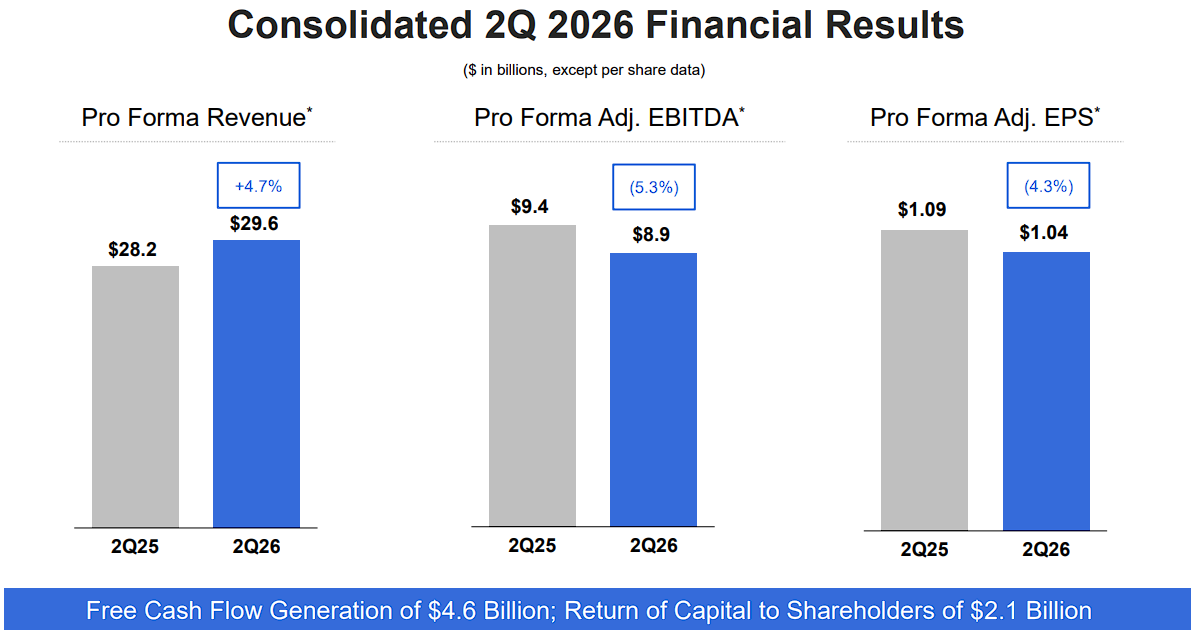

High Dividend Stock #7: Comcast Corporation (CMCSA)

- Dividend Risk Score: B

- Dividend Yield: 5.3%

Comcast Corporation combines broadband, wireless, business connectivity, media, studios, and theme parks.

Its cable network remains the principal cash generator, while Peacock, wireless, and the Universal entertainment businesses provide additional growth avenues.

Second-quarter 2026 revenue declined 1.2% to $29.9 billion, although pro forma revenue increased 4.7% after adjusting for portfolio changes.

Adjusted EPS fell 16.7% to $1.04, but free cash flow remained substantial at $4.6 billion.

Domestic wireless additions reached a record 448,000, taking total lines to 10.2 million.

Peacock also achieved its first quarterly profit, posting adjusted EBITDA of $189 million as paid subscribers increased by two million to 48 million.

Comcast’s next major step is its planned tax-free separation of NBCUniversal and Sky into a second public company.

Management paused share repurchases while preparing the transaction, which should produce two more focused businesses but also introduces execution risk and makes future capital allocation less predictable.

Comcast maintained its annualized dividend at $1.32 for 2026 after 17 consecutive years of increases.

The B Dividend Risk Score reflects the company’s strong free cash flow and moderate payout ratio, even as legacy broadband competition and the pending separation complicate the outlook.

High Dividend Stock #6: NNN REIT, Inc. (NNN)

- Dividend Risk Score: C

- Dividend Yield: 5.3%

NNN REIT, Inc. owns a large portfolio of single-tenant properties leased primarily under long-term triple-net agreements.

Tenants generally pay property taxes, insurance, and maintenance, which keeps NNN’s recurring capital requirements relatively low and supports predictable cash flow.

NNN generated second-quarter 2026 adjusted funds from operations of $0.90 per share, up 5.9% year-over-year.

Occupancy improved to 99.1%, and the REIT completed $291 million of investments at a 7.3% initial cash cap rate and a 17.9-year weighted-average lease term.

Following the quarter, management increased its 2026 AFFO guidance to $3.55 to $3.59 per share and raised its acquisition target to $700 million to $800 million.

The company also exercised a $200 million incremental term-loan option and negotiated lower pricing on both its term loan and revolving credit facility, improving financial flexibility as it expands the portfolio.

In July, NNN raised its quarterly dividend 3.3% to $0.62 per share. That marked its 37th consecutive annual dividend increase, a record matched by very few publicly traded REITs.

The combination of high occupancy, long leases, disciplined acquisition yields, and a long dividend record strengthens the income case, although interest rates and tenant credit remain important risks.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on NNN REIT, Inc. (NNN).

High Dividend Stock #5: Solvay Bank Corp. (SOBS)

- Dividend Risk Score: B

- Dividend Yield: 5.3%

Solvay Bank Corp. is the holding company for Solvay Bank, a state-chartered community bank serving Onondaga County and nearby markets in New York.

Its operations include consumer and commercial banking, trust and investment management, and insurance services, providing several sources of fee and interest income within a focused regional franchise.

In its latest quarterly disclosure, for the period ending March 31, 2026, total interest income was $12.2 million and net interest income was $7.0 million.

Net interest margin was 2.43%, while quarterly net income totaled $1.65 million.

The bank’s earnings remain sensitive to deposit costs, loan growth, and local credit conditions, but its established customer base and conservative operating history provide a measure of stability.

Solvay Bank increased its quarterly dividend to $0.45 per share in 2026 from $0.44 previously, with the latest payment made on July 31.

The increase extended the company’s dividend-growth streak to 34 consecutive years, an unusually long record for a small community bank.

Investors should nevertheless account for the stock’s limited trading liquidity and relatively sparse public disclosures.

Those characteristics can produce wider bid-ask spreads and require more careful monitoring, even though the B Dividend Risk Score and long dividend record compare favorably with many higher-yielding securities.

High Dividend Stock #4: Albertsons Companies, Inc. (ACI)

- Dividend Risk Score: C

- Dividend Yield: 5.6%

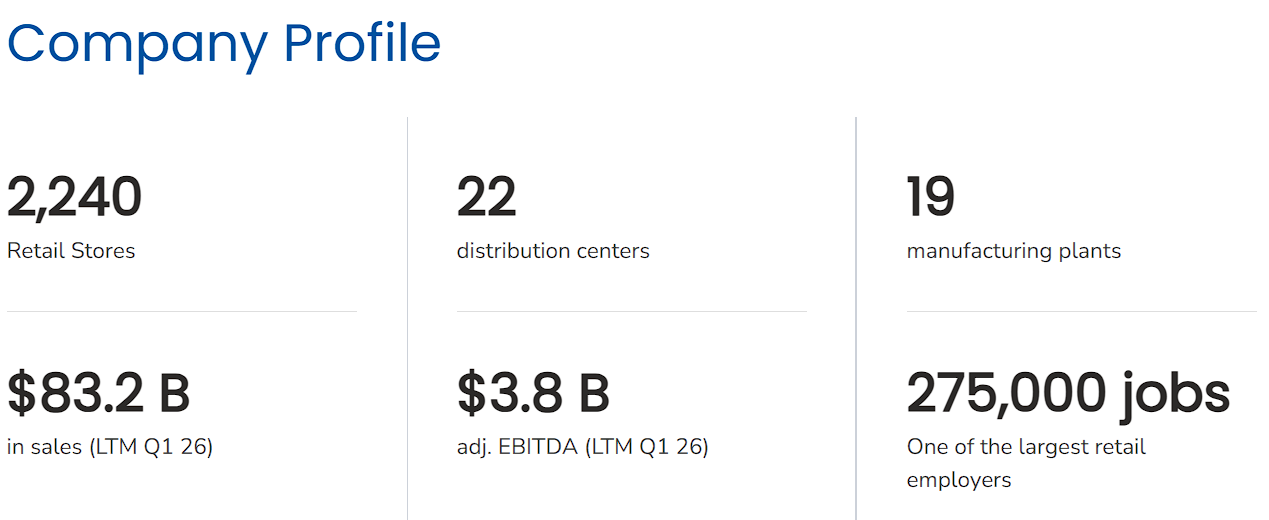

Albertsons Companies, Inc. is one of the largest U.S. food and drug retailers.

At the end of its latest quarter, it operated 2,240 stores in 35 states and the District of Columbia under banners including Albertsons, Safeway, Vons, Jewel-Osco, and ACME, supported by 1,708 in-store pharmacies.

For the first quarter of fiscal 2026, revenue increased 0.2% to $24.9 billion, while identical sales declined 0.8%.

Digital sales rose 13%, and pharmacy remained a source of growth, but adjusted EBITDA fell to $1.01 billion and adjusted EPS declined to $0.42.

Management reduced its full-year outlook, now expecting identical sales to decline 0.5% to 1.5%, adjusted EBITDA of $3.55 billion to $3.63 billion, and adjusted EPS of $1.75 to $1.85.

Albertsons responded by launching ACI Edge, which will consolidate 11 operating divisions into four regions and centralize center-store merchandising.

The plan is intended to simplify decision-making, improve value, and better leverage the company’s scale, but savings will take time while customer investments pressure near-term results.

The board raised the quarterly dividend 13% to $0.17 in April and expanded the share-repurchase authorization to $2.0 billion.

The high yield therefore comes with real operating risk following the guidance reduction, consistent with the C Dividend Risk Score.

High Dividend Stock #3: Enterprise Products Partners L.P. (EPD)

- Dividend Risk Score: C

- Dividend Yield: 5.8%

Enterprise Products Partners L.P. is one of the largest publicly traded midstream partnerships.

Its integrated system of pipelines, processing plants, fractionators, storage facilities, and export terminals earns primarily fee-based cash flows by transporting and handling natural gas, natural gas liquids, crude oil, refined products, and petrochemicals.

Enterprise produced record second-quarter 2026 results. Net income attributable to common unitholders increased 28% to $1.8 billion, or $0.84 per unit.

Adjusted EBITDA rose 17% to $2.8 billion, while operational distributable cash flow increased 21% to $2.3 billion and covered the quarterly distribution 1.9 times.

Equivalent pipeline volumes reached a record 14.7 million barrels per day, and marine-terminal volumes increased 33% to a record 2.8 million barrels per day.

The partnership raised its quarterly distribution 2.8% to $0.56 per unit and repurchased $159 million of units during the quarter.

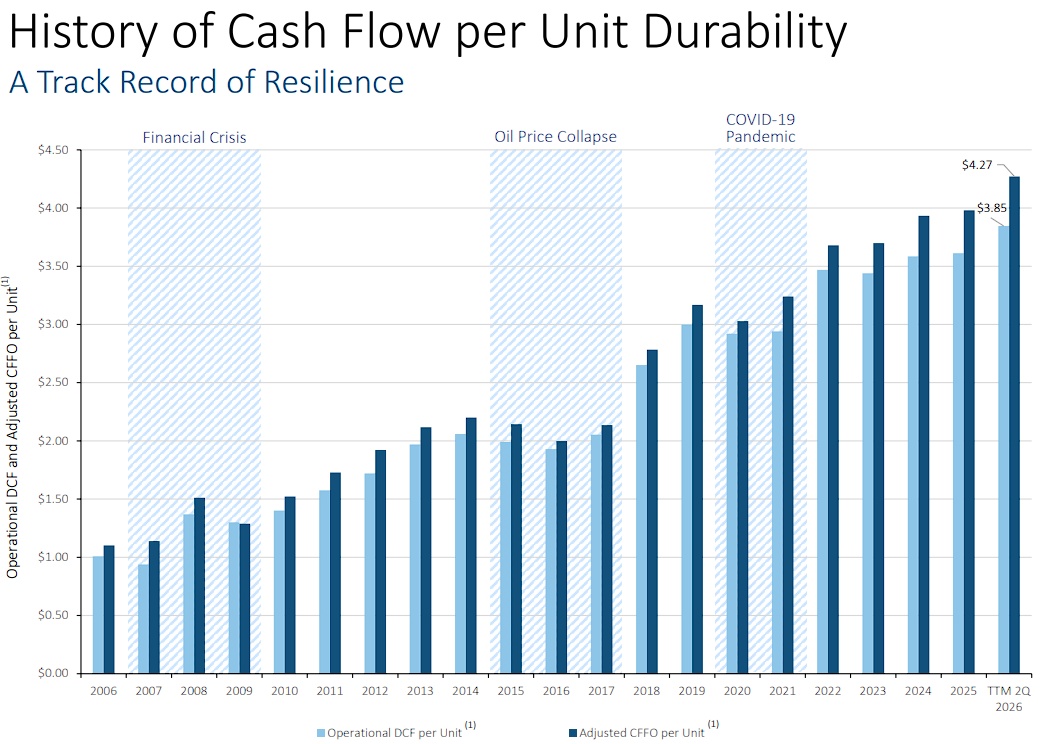

Enterprise is on track for its 28th consecutive year of distribution growth, the longest record among U.S. midstream companies.

Distribution growth has been supported by an equally long and durable history of cash flow per unit growth.

Management expects 2026 growth capital spending of $2.9 billion to $3.4 billion, net of asset-sale proceeds.

Recently completed and upcoming projects should expand capacity and support stronger cash-flow growth in 2027.

Also, the 1.9-times coverage ratio provides a meaningful cushion for the current distribution.

High Dividend Stock #2: Altria Group, Inc. (MO)

- Dividend Risk Score: B

- Dividend Yield: 6.3%

Altria Group, Inc. owns the leading U.S. cigarette brand Marlboro along with Copenhagen, Skoal, on!, and NJOY.

Cigarettes still generate most of its profits, while oral nicotine and other smoke-free products are intended to offset the industry’s persistent volume decline.

Second-quarter 2026 revenue net of excise taxes increased 1.2% to $5.36 billion, and adjusted EPS rose 2.8% to $1.48.

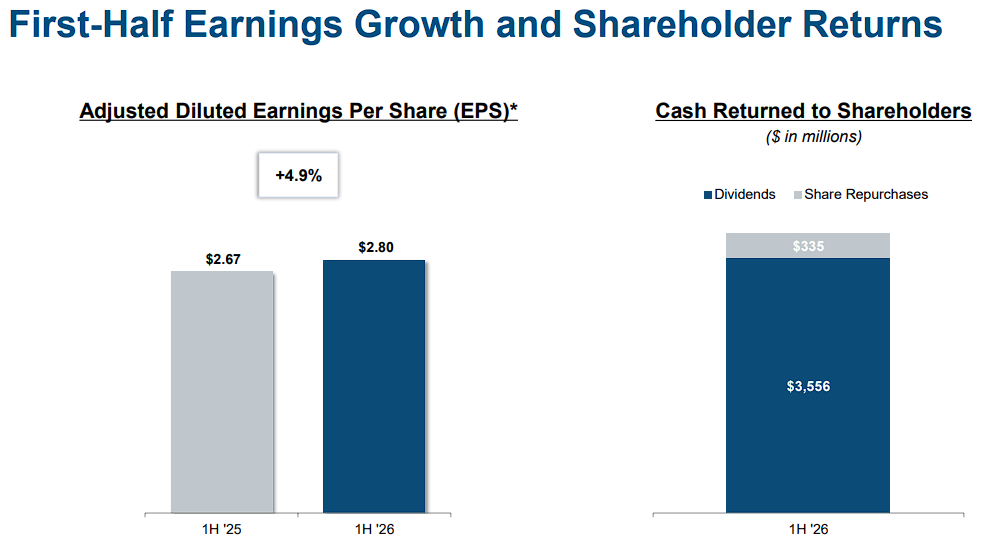

For the first half, adjusted EPS increased 4.9% to $2.80. Pricing and cost control continued to support smokeable-products profit despite lower volumes, while oral-tobacco results were pressured by promotional spending and weaker shipments.

Management narrowed full-year adjusted EPS guidance to $5.61 to $5.72, implying growth of 3.5% to 5.5%.

Altria is expanding on! PLUS nationally, with the product reaching roughly 120,000 stores and additional strengths and flavors planned.

This provides a credible smoke-free growth platform, although NJOY ACE is still not expected to return in 2026.

The company paid $1.8 billion of dividends in the quarter and has increased its dividend for 56 consecutive years.

Its annualized payout of $4.24 per share is high relative to earnings, but the predictable cash generation of the cigarette business supports the B Dividend Risk Score and 6.3% yield.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on Altria Group, Inc. (MO).

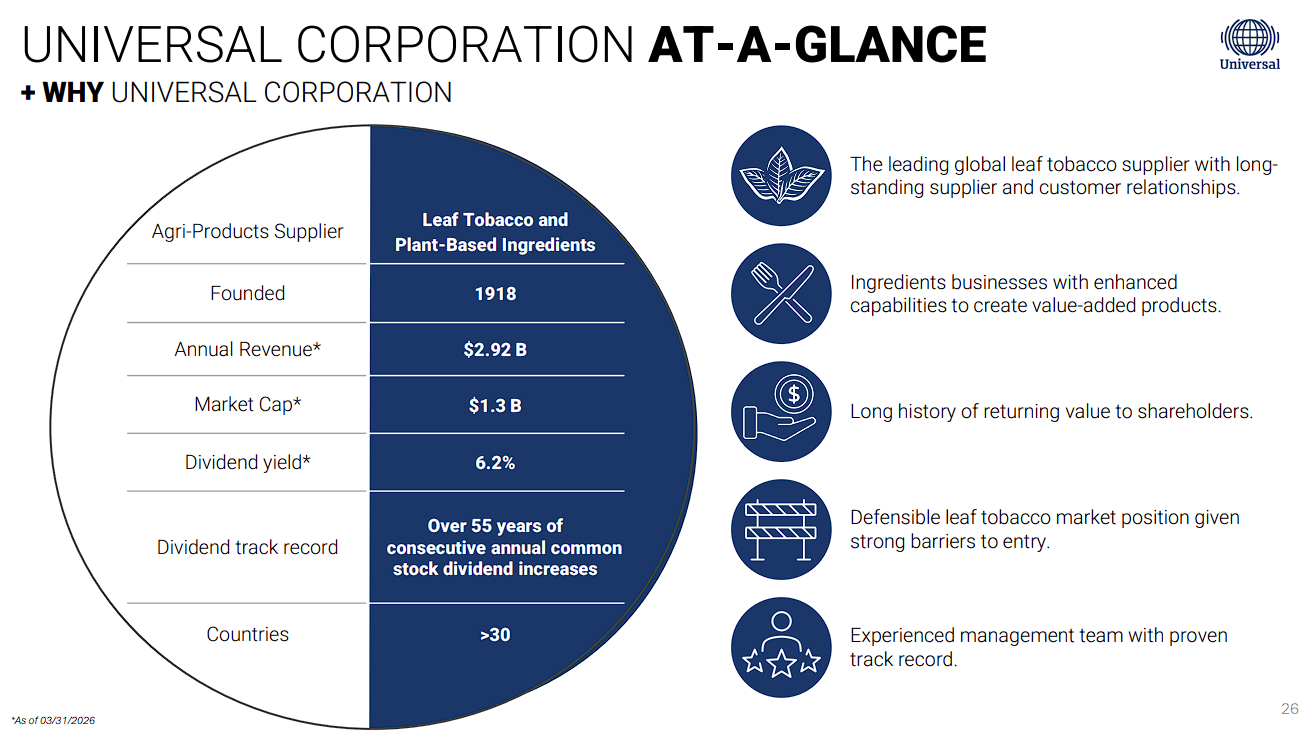

High Dividend Stock #1: Universal Corporation (UVV)

- Dividend Risk Score: C

- Dividend Yield: 6.4%

Universal Corporation is a global business-to-business agriproducts supplier.

It is the leading global leaf-tobacco merchant and processor, sourcing tobacco through a network spanning more than 30 countries.

Its smaller Ingredients Operations segment supplies plant-based ingredients to food and beverage manufacturers.

For fiscal 2026, revenue declined 1% to $2.92 billion. Operating income fell 28% to $168.5 million, while adjusted operating income decreased 13% to $211.3 million.

Results were hurt by a $41.1 million noncash goodwill impairment related to the Shank’s ingredients business and $52.0 million of inventory write-downs, mainly involving dark air-cured tobacco.

Tobacco-segment revenue and volume each declined modestly from an unusually strong prior year, although the ingredients segment delivered higher revenue and sales volumes.

Universal’s investment case rests on its entrenched relationships with tobacco manufacturers, global sourcing network, and ability to manage crops across regions.

Oversupply in certain tobacco styles and continued weakness in packaged-food ingredients remain near-term challenges.

Even so, the board raised the quarterly dividend to $0.83 per share in May, marking the company’s 56th consecutive annual increase.

The dividend consumes roughly 77% of expected earnings, leaving less room for error than some peers.

Still, the long record and 6.4% yield make Universal the highest-yielding eligible security in this ranking.

The High Dividend 50 Series

The High Dividend 50 Series includes download links for our 3-Page Sure Analysis PDF Reports for the 50 highest-yielding Sure Analysis Research Database securities.

Securities are organized by yield, from highest to lowest.

- Bridgemarq Real Estate Services Inc. (BREUF)

- Oxford Square Capital Corp. (OXSQ)

- PennantPark Investment Corporation (PNNT)

- Shutterstock, Inc. (SSTK)

- Ellington Credit Co. (EARN)

- Invesco Mortgage Capital Inc. (IVR)

- Prospect Capital Corp. (PSEC)

- Orchid Island Capital Inc. (ORC)

- ARMOUR Residential REIT Inc (ARR)

- CION Investment Corporation (CION)

- Stellus Capital Investment Corp (SCM)

- Dynex Capital, Inc. (DX)

- Horizon Technology Finance Corp (HRZN)

- Saratoga Investment Corp. (SAR)

- BCP Investment Corporation (BCIC)

- AGNC Investment Corp (AGNC)

- PennantPark Floating Rate Capital Ltd (PFLT)

- Innovative Industrial Properties Inc (IIPR)

- Telus Corp. (TU)

- Community Healthcare Trust Inc (CHCT)

- Ellington Financial Inc. (EFC)

- Trinity Capital Inc. (TRIN)

- Timbercreek Financial Corp. (TBCRF)

- MSC Income Fund, Inc. (MSIF)

- Mesa Royalty Trust (MTR)

- PermRock Royalty Trust (PRT)

- Perrigo Company plc (PRGO)

- Capital Southwest Corp. (CSWC)

- Gladstone Commercial Corp (GOOD)

- Gladstone Capital Corp. (GLAD)

- NexPoint Residential Trust Inc (NXRT)

- Boston Pizza Royalties Income Fund (BPZZF)

- Source Rock Royalties Ltd. (SRRRF)

- Nexus Industrial REIT (EFRTF)

- Silvercrest Asset Management Group Inc (SAMG)

- Atrium Mortgage Investment Corporation (AMIVF)

- BTB Real Estate Investment Trust (BTBIF)

- Firm Capital Mortgage Investment Corp. (FCMGF)

- Blue Owl Capital Inc (OWL)

- True North Commercial REIT (TUERF)

- Hess Midstream LP (HESM)

- Western Midstream Partners, LP (WES)

- SIR Royalty Income Fund (SIRZF)

- Allied Properties Real Estate Investment Trust (APYRF)

- Delek Logistics Partners, LP (DKL)

- Permianville Royalty Trust (PVL)

- Banco Bradesco S.A. (BBD)

- Firm Capital Property Trust (FRMUF)

- Gaming and Leisure Properties Inc (GLPI)

- InPlay Oil Corp. (IPOOF)

Final Thoughts

Our ranking shows that a high yield can come from very different business models.

Enterprise Products, Realty Income, and NNN pair their yields with long distribution-growth records and contract-backed cash flows.

Altria and Universal offer the largest yields, but both remain tied to tobacco demand.

The community banks provide locally focused income, while Edison’s utility growth is accompanied by wildfire risk.

Albertsons and Comcast offer greater turnaround or restructuring potential, but also less near-term visibility.

Dividend Risk Scores of C or better provide an initial quality screen, not a guarantee that every payout will remain unchanged.

The most useful next step is to compare each security’s payout coverage, balance sheet, growth outlook, and company-specific risks in the linked Sure Analysis reports.

When a high yield is supported by durable cash flow and purchased at a reasonable valuation, it can contribute meaningfully to both portfolio income and long-term total returns.

Additional dividend-stock resources include:

- The Dividend Kings List: stocks with at least 50 consecutive years of dividend growth.

- The Dividend Aristocrats: S&P 500 stocks with 25+ years of consecutive dividend increases.

- The Monthly Dividend Stocks List: stocks that make 12 dividend payments per year.