Published on January 13th, 2026 by Bob Ciura

Dividend stocks are naturally appealing for income investors, but not all dividend stocks are buys.

Income investors generally want to avoid dividend cuts whenever possible. Not only does a dividend cut result in a loss of income, but a company’s share price typically declines after announcing a dividend reduction or suspension.

With this in mind, we compiled a list of high dividend stocks with dividend yields above 4%. You can download your free copy of the high dividend stocks list by clicking on the link below:

Income investors should try to avoid dividend cuts or elimination as much as possible.

The 10 stocks in this article all have Dividend Risk Scores of ‘F’ (our lowest grade) in the Sure Analysis Research Database, with payout ratios above 100%.

A payout ratio above 100% indicates the company is not generating enough underlying earnings to sustain the dividend payout. This leaves a high likelihood of a dividend cut or elimination at some point in the future.

The list is sorted by dividend payout ratio, from lowest to highest.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

- High Risk Dividend Stock #10: Prospect Capital (PSEC)

- High Risk Dividend Stock #9: Plains GP Holdings LP (PAGP)

- High Risk Dividend Stock #8: Oxford Square Capital (OXSQ)

- High Risk Dividend Stock #7: Gladstone Land Corp. (LAND)

- High Risk Dividend Stock #6: Telus Corp. (TU)

- High Risk Dividend Stock #5: Robert Half International (RHI)

- High Risk Dividend Stock #4: Insperity Inc. (NSP)

- High Risk Dividend Stock #3: Source Rock Royalties Ltd. (SRRRF)

- High Risk Dividend Stock #2: Dynex Capital (DX)

- High Risk Dividend Stock #1: Orchid Island Capital (ORC)

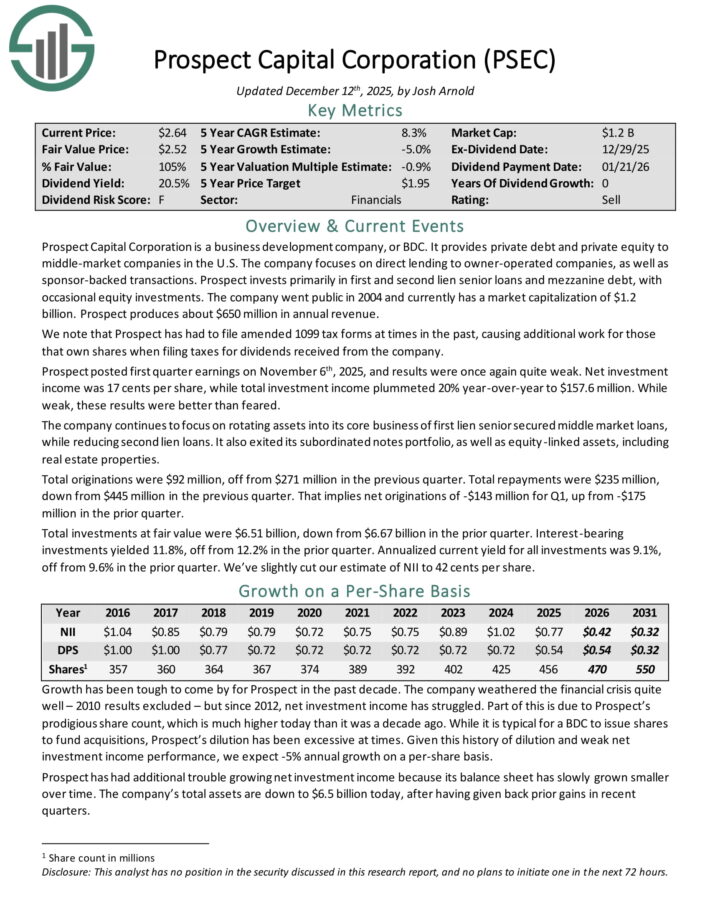

High Risk Dividend Stock #10: Prospect Capital (PSEC)

- Payout Ratio: 128.6%

Prospect Capital Corporation is a Business Development Company, or BDC, that provides private debt and private equity to middle–market companies in the U.S.

The company focuses on direct lending to owner–operated companies, as well as sponsor–backed transactions. Prospect invests primarily in first and second lien senior loans and mezzanine debt, with occasional equity investments.

Prospect posted first quarter earnings on November 6th, 2025. Net investment income was 17 cents per share, while total investment income plummeted 20% year-over-year to $157.6 million. While weak, these results were better than feared.

The company continues to focus on rotating assets into its core business of first lien senior secured middle market loans, while reducing second lien loans. It also exited its subordinated notes portfolio, as well as equity-linked assets, including real estate properties.

Total originations were $92 million, off from $271 million in the previous quarter. Total repayments were $235 million, down from $445 million in the previous quarter. That implies net originations of -$143 million for Q1, up from -$175 million in the prior quarter.

Total investments at fair value were $6.51 billion, down from $6.67 billion in the prior quarter. Interest-bearing investments yielded 11.8%, off from 12.2% in the prior quarter.

Click here to download our most recent Sure Analysis report on PSEC (preview of page 1 of 3 shown below):

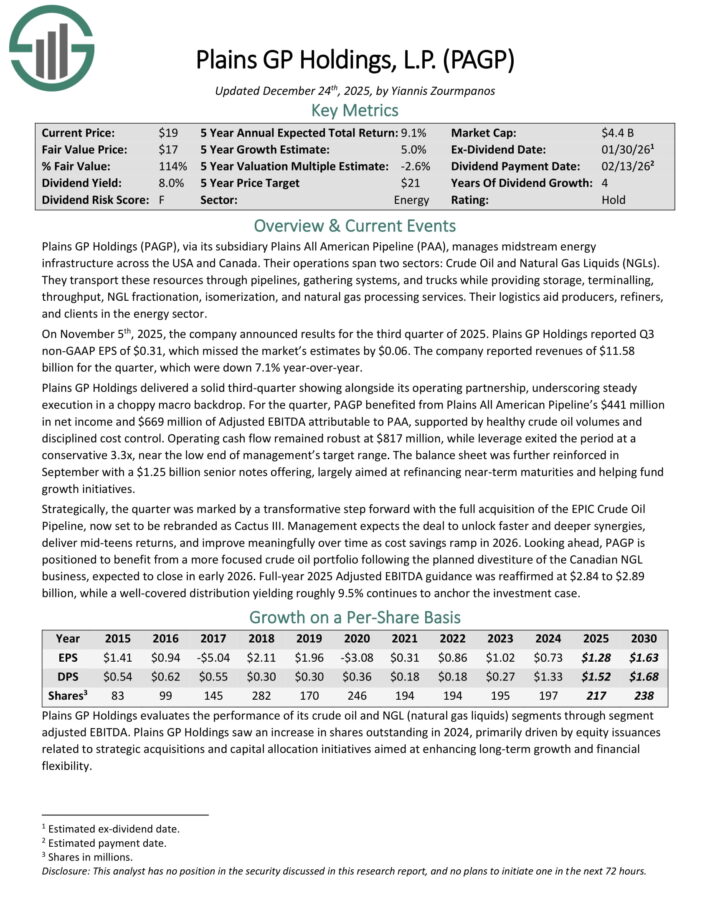

High Risk Dividend Stock #9: Plains GP Holdings LP (PAGP)

- Payout Ratio: 130.5%

Plains GP Holdings, via its subsidiary Plains All American Pipeline (PAA), manages midstream energy infrastructure across the USA and Canada.

Their operations span two sectors: Crude Oil and Natural Gas Liquids (NGLs). They transport these resources through pipelines, gathering systems, and trucks while providing storage, terminaling, throughput, NGL fractionation, isomerization, and natural gas processing services.

Their logistics aid producers, refiners, and clients in the energy sector.

On November 5th, 2025, the company announced results for the third quarter of 2025. Plains GP Holdings reported Q3 non-GAAP EPS of $0.31, which missed the market’s estimates by $0.06. The company reported revenue of $11.58

billion for the quarter, down 7.1% year-over-year.

Operating cash flow remained robust at $817 million, while leverage exited the period at a conservative 3.3x, near the low end of management’s target range.

Looking ahead, PAGP is positioned to benefit from a more focused crude oil portfolio following the planned divestiture of the Canadian NGL business, expected to close in early 2026.

Click here to download our most recent Sure Analysis report on PAGP (preview of page 1 of 3 shown below):

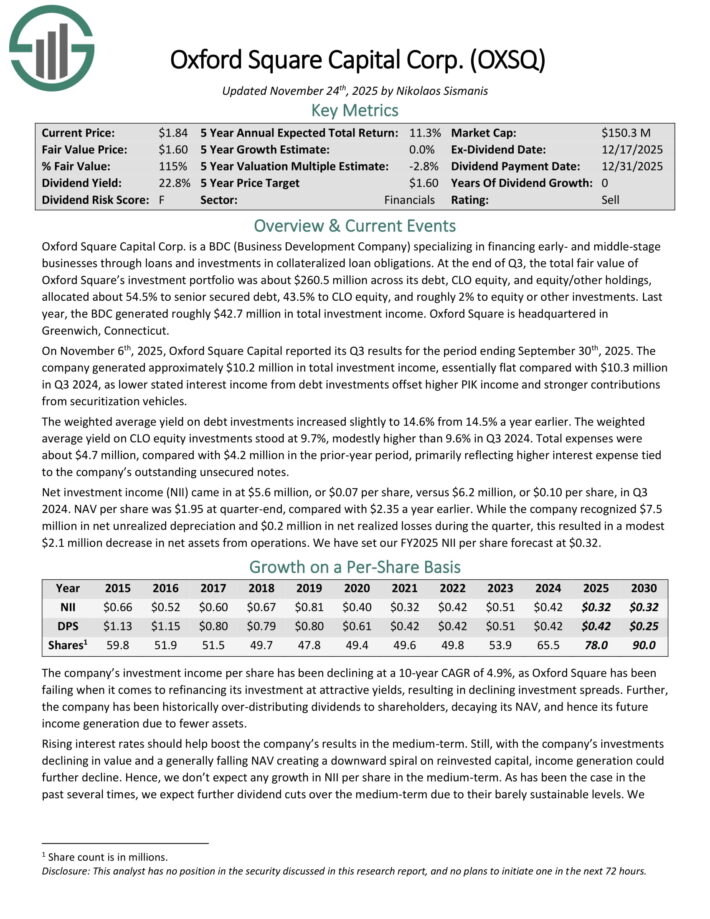

High Risk Dividend Stock #8: Oxford Square Capital (OXSQ)

- Payout Ratio: 131.3%

Oxford Square Capital Corp. is a BDC (Business Development Company) specializing in financing early- and middle-stage businesses through loans and investments in collateralized loan obligations.

At the end of Q3, the total fair value of Oxford Square’s investment portfolio was about $260.5 million across its debt, CLO equity, and equity/other holdings, allocated about 54.5% to senior secured debt, 43.5% to CLO equity, and roughly 2% to equity or other investments. Last year, the BDC generated roughly $42.7 million in total investment income.

On November 6th, 2025, Oxford Square Capital reported its Q3. The company generated approximately $10.2 million in total investment income, essentially flat compared with $10.3 million in Q3 2024, as lower stated interest income from debt investments offset higher PIK income and stronger contributions from securitization vehicles.

The weighted average yield on debt investments increased slightly to 14.6% from 14.5% a year earlier. The weighted average yield on CLO equity investments stood at 9.7%, modestly higher than 9.6% in Q3 2024.

Total expenses were about $4.7 million, compared with $4.2 million in the prior-year period, primarily reflecting higher interest expense tied to the company’s outstanding unsecured notes.

Net investment income (NII) came in at $5.6 million, or $0.07 per share, versus $6.2 million, or $0.10 per share, in Q3 2024.

Click here to download our most recent Sure Analysis report on OXSQ (preview of page 1 of 3 shown below):

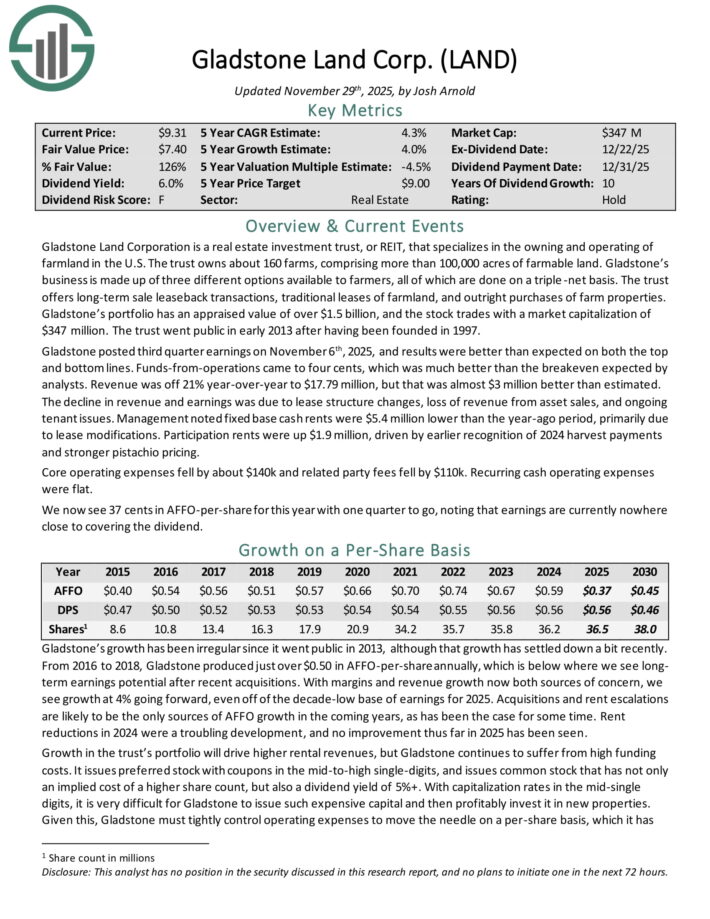

High Risk Dividend Stock #7: Gladstone Land Corp. (LAND)

- Payout Ratio: 151.4%

Gladstone Land Corporation is a REIT that specializes in the owning and operating of farmland in the U.S.

The trust owns about 160 farms, comprising more than 100,000 acres of farmable land. Gladstone’s business is made up of three different options available to farmers, all of which are done on a triple-net basis.

The trust offers long-term sale leaseback transactions, traditional leases of farmland, and outright purchases of farm properties. Gladstone’s portfolio has an appraised value of over $1.5 billion.

Gladstone posted third quarter earnings on November 6th, 2025, and results were better than expected on both the top and bottom lines.

Funds-from-operations came to four cents, which was much better than the breakeven expected by analysts. Revenue was off 21% year-over-year to $17.79 million, but that was almost $3 million better than estimated.

The decline in revenue and earnings was due to lease structure changes, loss of revenue from asset sales, and ongoing tenant issues. Management noted fixed base cash rents were $5.4 million lower than the year-ago period, primarily due to lease modifications.

Participation rents were up $1.9 million, driven by earlier recognition of 2024 harvest payments and stronger pistachio pricing.

Core operating expenses fell by about $140k and related party fees fell by $110k. Recurring cash operating expenses were flat.

Click here to download our most recent Sure Analysis report on LAND (preview of page 1 of 3 shown below):

High Risk Dividend Stock #6: Telus Corp. (TU)

- Payout Ratio: 160.0%

TELUS Corporation is one of the ‘big three’ Canadian telecommunications companies along with BCE, Inc. (BCE) and Rogers Communications (RCI).

TELUS is focused in Western Canada and provides a full range of communication products and services through two business segments: Wireline and Wireless.

In early November, TELUS reported (11/7/25) financial results for the third quarter of fiscal 2025. The company posted decent customer growth.

It posted total mobile customer growth of 82,000, growth of fixed customers by 206,000 and a healthy churn rate of 0.91% at its postpaid mobile business.

However, revenue remained essentially flat over the prior year’s quarter. Earnings-per-share declined -15%, from $0.20 to $0.17, mostly due to thinner operating margins.

Management now expects growth of revenue towards the low end of its guidance for 2%-4% and reiterated its guidance for 3%-5% growth of adjusted EBITDA in 2025.

Click here to download our most recent Sure Analysis report on TU (preview of page 1 of 3 shown below):

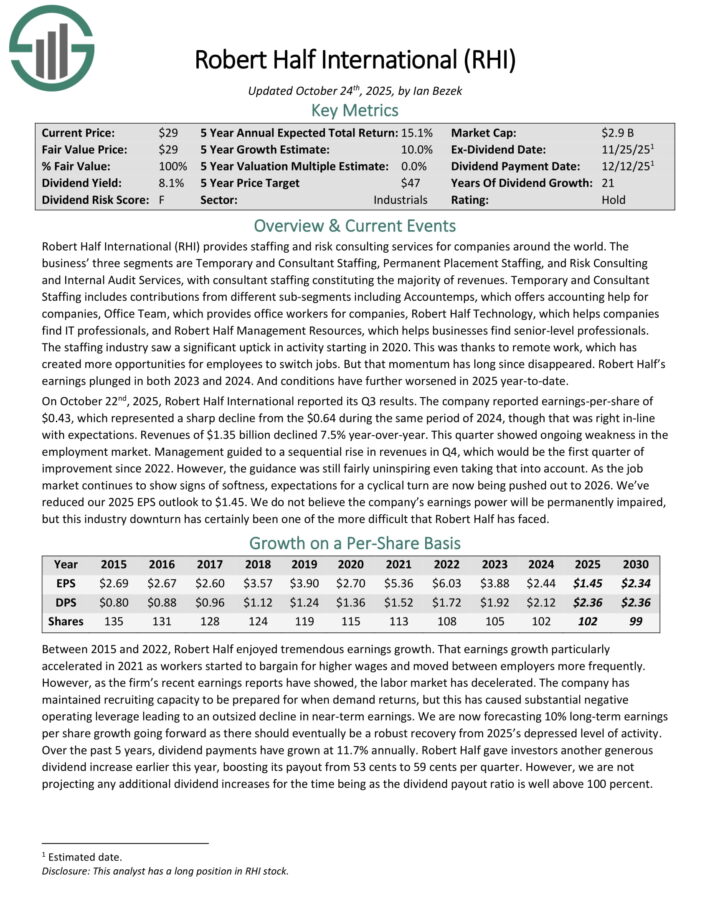

High Risk Dividend Stock #5: Robert Half International (RHI)

- Payout Ratio: 162.8%

Robert Half International provides staffing and risk consulting services for companies around the world.

Its three segments are Temporary and Consultant Staffing, Permanent Placement Staffing, and Risk Consulting and Internal Audit Services, with consultant staffing constituting the majority of revenues.

Temporary and Consultant Staffing includes contributions from different sub-segments including Accountemps, which offers accounting help for companies, Office Team, which provides office workers for companies, Robert Half Technology, which helps companies find IT professionals, and Robert Half Management Resources, which helps businesses find senior-level professionals.

Robert Half’s earnings plunged in both 2023 and 2024, and conditions further worsened in 2025.

On October 22nd, 2025, Robert Half International reported its Q3 results. The company reported earnings-per-share of $0.43, which represented a sharp decline from the $0.64 during the same period of 2024.

Revenue of $1.35 billion declined 7.5% year-over-year. This quarter showed ongoing weakness in the employment market. Management guided to a sequential rise in revenues in Q4, which would be the first quarter of improvement since 2022.

However, the guidance was still fairly uninspiring even taking that into account. As the job market continues to show signs of softness, expectations for a cyclical turn are now being pushed out to 2026.

Click here to download our most recent Sure Analysis report on RHI (preview of page 1 of 3 shown below):

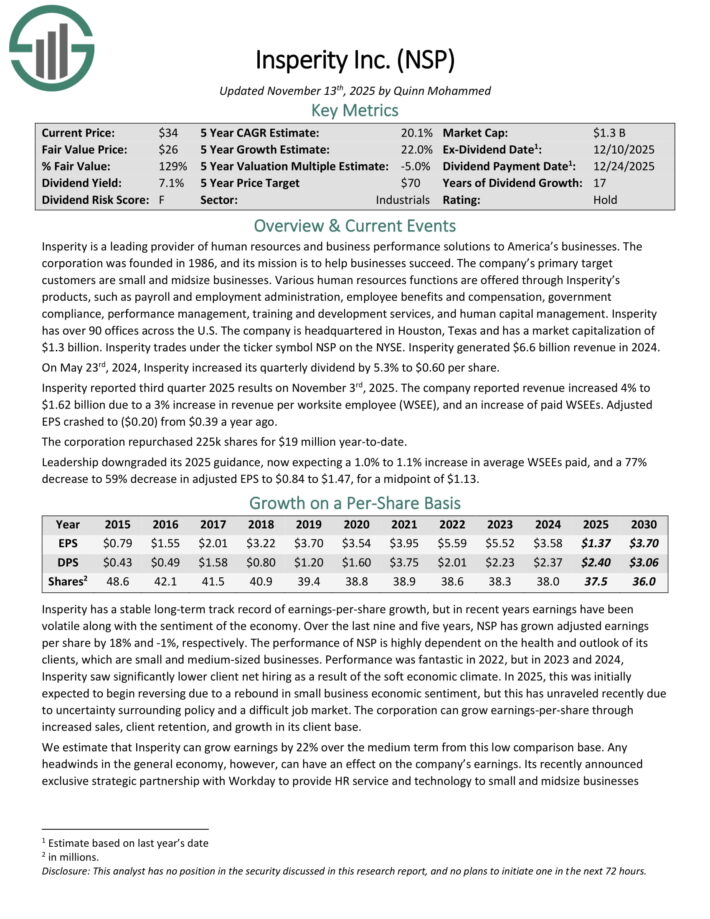

High Risk Dividend Stock #4: Insperity Inc. (NSP)

- Payout Ratio: 175.2%

Insperity is a leading provider of human resources and business performance solutions to businesses. The company’s primary target customers are small and midsize businesses.

Various human resources functions are offered through Insperity’s products, such as payroll and employment administration, employee benefits and compensation, government compliance, performance management, training and development services, and human capital management.

Insperity has over 90 offices across the U.S. and generated $6.6 billion revenue in 2024.

Insperity reported third quarter 2025 results on November 3rd, 2025. The company reported revenue increased 4% to $1.62 billion due to a 3% increase in revenue per worksite employee (WSEE), and an increase of paid WSEEs. Adjusted EPS crashed to ($0.20) from $0.39 a year ago.

The corporation repurchased 225k shares for $19 million year-to-date.

Leadership downgraded its 2025 guidance, now expecting a 1.0% to 1.1% increase in average WSEEs paid, and a 77% decrease to 59% decrease in adjusted EPS to $0.84 to $1.47, for a midpoint of $1.13.

NSP’s payout ratio is elevated at 175% of forecast earnings. The company has never cut its dividend, but this year it is not likely to earn enough to cover it.

Click here to download our most recent Sure Analysis report on NSP (preview of page 1 of 3 shown below):

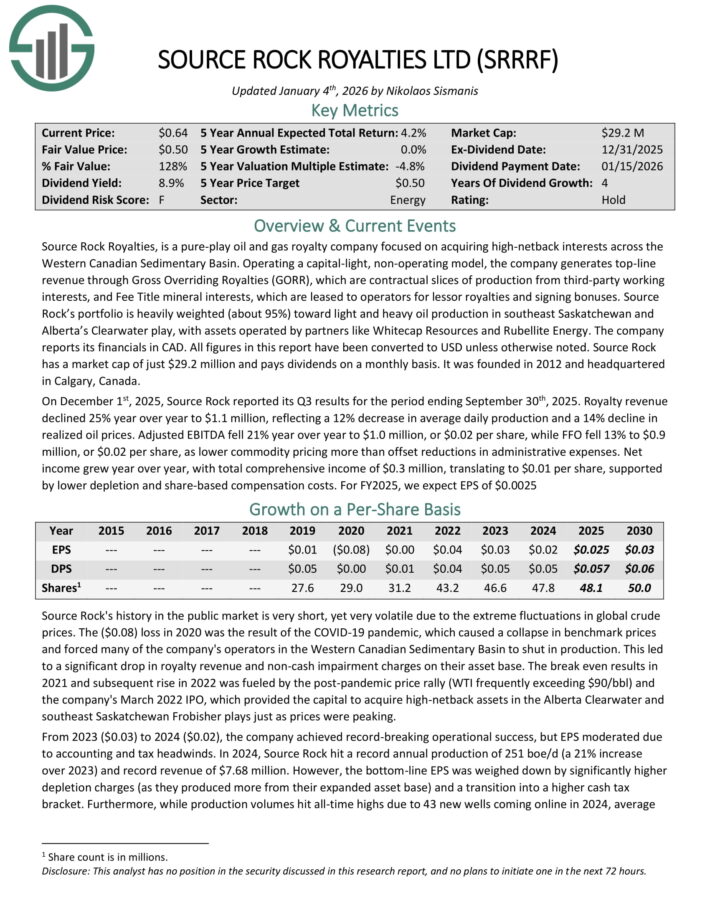

High Risk Dividend Stock #3: Source Rock Royalties Ltd. (SRRRF)

- Payout Ratio: 200.0%

Source Rock Royalties, is a pure-play oil and gas royalty company focused on acquiring high-netback interests across the Western Canadian Sedimentary Basin.

Operating a capital-light, non-operating model, the company generates top-line revenue through Gross Overriding Royalties (GORR), which are contractual slices of production from third-party working interests, and Fee Title mineral interests, which are leased to operators for lessor royalties and signing bonuses.

Source Rock’s portfolio is heavily weighted (about 95%) toward light and heavy oil production in southeast Saskatchewan and Alberta’s Clearwater play, with assets operated by partners like Whitecap Resources and Rubellite Energy.

Source Rock was founded in 2012 and headquartered in Calgary, Canada.

On December 1st, 2025, Source Rock reported its Q3 results. Royalty revenue declined 25% year over year to $1.1 million, reflecting a 12% decrease in average daily production and a 14% decline in realized oil prices.

Adjusted EBITDA fell 21% year over year to $1.0 million, or $0.02 per share, while FFO fell 13% to $0.9 million, or $0.02 per share, as lower commodity pricing more than offset reductions in administrative expenses.

Net income grew year over year, with total comprehensive income of $0.3 million, translating to $0.01 per share, supported by lower depletion and share-based compensation costs.

Click here to download our most recent Sure Analysis report on SRRRF (preview of page 1 of 3 shown below):

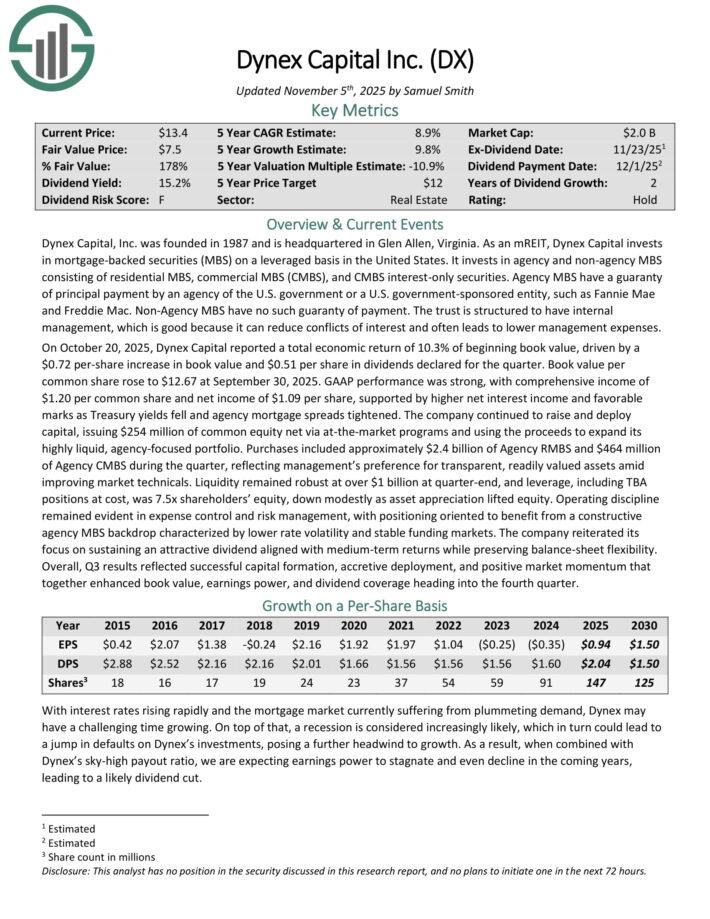

High Risk Dividend Stock #2: Dynex Capital (DX)

- Payout Ratio: 217.0%

Dynex Capital invests in mortgage–backed securities (MBS) on a leveraged basis in the United States. It invests in agency and non–agency MBS consisting of residential MBS, commercial MBS (CMBS), and CMBS interest–only securities.

On October 20, 2025, Dynex Capital reported a total economic return of 10.3% of beginning book value, driven by a $0.72 per-share increase in book value and $0.51 per share in dividends declared for the quarter.

Book value per common share rose to $12.67 at September 30, 2025. GAAP performance was strong, with comprehensive income of $1.20 per common share and net income of $1.09 per share, supported by higher net interest income and favorable marks as Treasury yields fell and agency mortgage spreads tightened.

The company continued to raise and deploy capital, issuing $254 million of common equity net via at-the-market programs and using the proceeds to expand its highly liquid, agency-focused portfolio.

Purchases included approximately $2.4 billion of Agency RMBS and $464 million of Agency CMBS during the quarter, reflecting management’s preference for transparent, readily valued assets amid improving market technicals.

Click here to download our most recent Sure Analysis report on DX (preview of page 1 of 3 shown below):

High Risk Dividend Stock #1: Orchid Island Capital (ORC)

- Payout Ratio: 225%

Orchid Island Capital is a mortgage REIT that is externally managed by Bimini Advisors LLC and focuses on investing in residential mortgage-backed securities (RMBS), including pass-through and structured agency RMBSs.

These financial instruments generate cash flow based on residential loans such as mortgages, subprime, and home-equity loans.

On October 23, 2025, Orchid Island Capital, Inc. reported estimated net income of $0.53 per common share for Q3 2025, with book value per share estimated at $7.33 as of September 30, 2025.

The company declared a monthly dividend of $0.12 per share for October, keeping consistent with its monthly payout strategy.

The RMBS portfolio and derivatives portfolio evolved as the company remained focused on agency residential mortgage-backed securities paired with hedging strategies.

Orchid Island highlighted that the investment backdrop remains attractive with improving spreads and prepayment risk manageable given the portfolio’s coupon distribution and hedges.

Prepayment activity remained a focal point, with management noting the need for continued vigilance given higher coupon pools and refinancing dynamics.

Click here to download our most recent Sure Analysis report on Orchid Island Capital, Inc. (ORC) (preview of page 1 of 3 shown below):

Additional Reading

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Monthly Dividend Stocks: Individual securities that pay out every month