Published on February 24th, 2026 by Bob Ciura

Long-term dividend growth stock investing combines the primary reason most people invest – passive income – with the tried-and-true wisdom that underlies successful investing.

For a company to pay rising dividends year-after-year for decades, it must have favorable long-term economic characteristics and a reasonably competent and honest management team.

Blue-chip stocks are well-established, financially strong, and consistently profitable companies.

This research report has the following resources to help you invest in blue chip stocks:

In addition, we have ranked the top 10 high quality dividend growth stocks for the long run.

The 10 dividend stocks below are expected to grow their future dividends at the highest compound annual rate of all companies we cover in the Sure Analysis Research Database.

They do not have high dividend yields, but their rapid expected earnings growth should allow them to raise their dividends at very high rates each year.

They are ranked in order of 5-year dividend growth rate, in ascending order.

Table of Contents

The table of contents below allows for easy navigation.

- Fast Growing Dividend Stock #10: Comfort Systems USA (FIX)

- Fast Growing Dividend Stock #9: Microchip Technology (MCHP)

- Fast Growing Dividend Stock #8: Mastercard Incorporated (MA)

- Fast Growing Dividend Stock #7: Eli Lilly & Co. (LLY)

- Fast Growing Dividend Stock #6: Power Integrations Inc. (POWI)

- Fast Growing Dividend Stock #5: McKesson Corporation (MCK)

- Fast Growing Dividend Stock #4: Lemaitre Vascular (LMAT)

- Fast Growing Dividend Stock #3: Badger Meter Inc. (BMI)

- Fast Growing Dividend Stock #2: Kinsale Capital Group (KNSL)

- Fast Growing Dividend Stock #1: CME Group Inc. (CME)

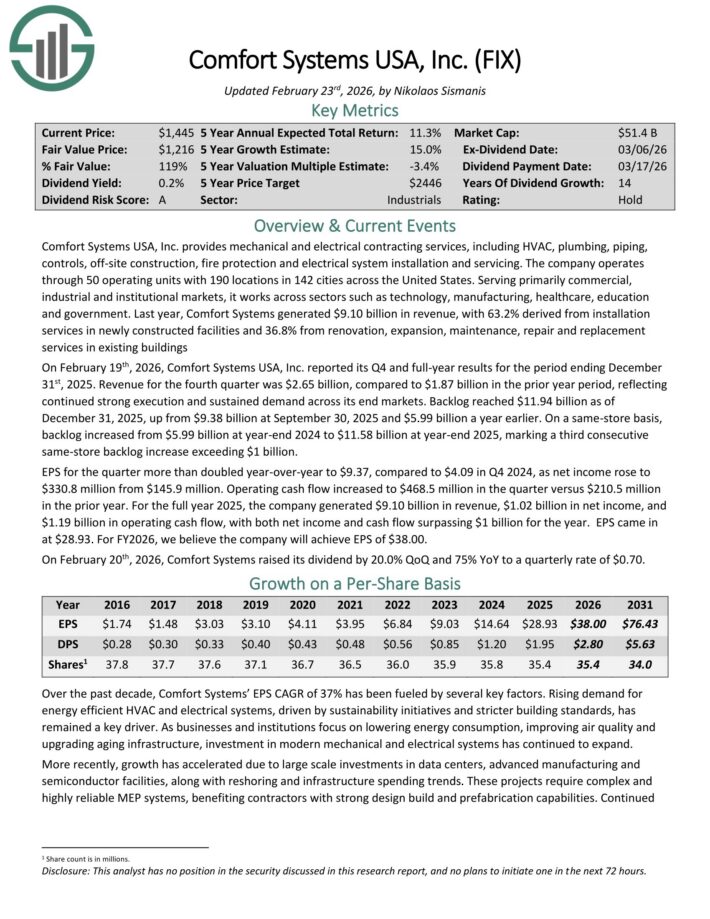

Fast Growing Dividend Stock #10: Comfort Systems USA (FIX)

- Dividend Growth: 15.0%

Comfort Systems USA, Inc. provides mechanical and electrical contracting services, including HVAC, plumbing, piping, controls, off-site construction, fire protection and electrical system installation and servicing.

The company operates through 50 operating units with 190 locations in 142 cities across the United States. Serving primarily commercial, industrial and institutional markets, it works across sectors such as technology, manufacturing, healthcare, education and government.

Last year, Comfort Systems generated $9.10 billion in revenue, with 63.2% derived from installation services in newly constructed facilities and 36.8% from renovation, expansion, maintenance, repair and replacement services in existing buildings.

On February 19th, 2026, Comfort Systems USA, Inc. reported its Q4 and full-year results for the period ending December 31st, 2025. Revenue for the fourth quarter was $2.65 billion, compared to $1.87 billion in the prior year period, reflecting continued strong execution and sustained demand across its end markets.

Backlog reached $11.94 billion as of December 31, 2025, up from $9.38 billion at September 30, 2025 and $5.99 billion a year earlier. On a same-store basis, backlog increased from $5.99 billion at year-end 2024 to $11.58 billion at year-end 2025, marking a third consecutive same-store backlog increase exceeding $1 billion.

EPS for the quarter more than doubled year-over-year to $9.37, compared to $4.09 in Q4 2024, as net income rose to $330.8 million from $145.9 million.

Click here to download our most recent Sure Analysis report on FIX (preview of page 1 of 3 shown below):

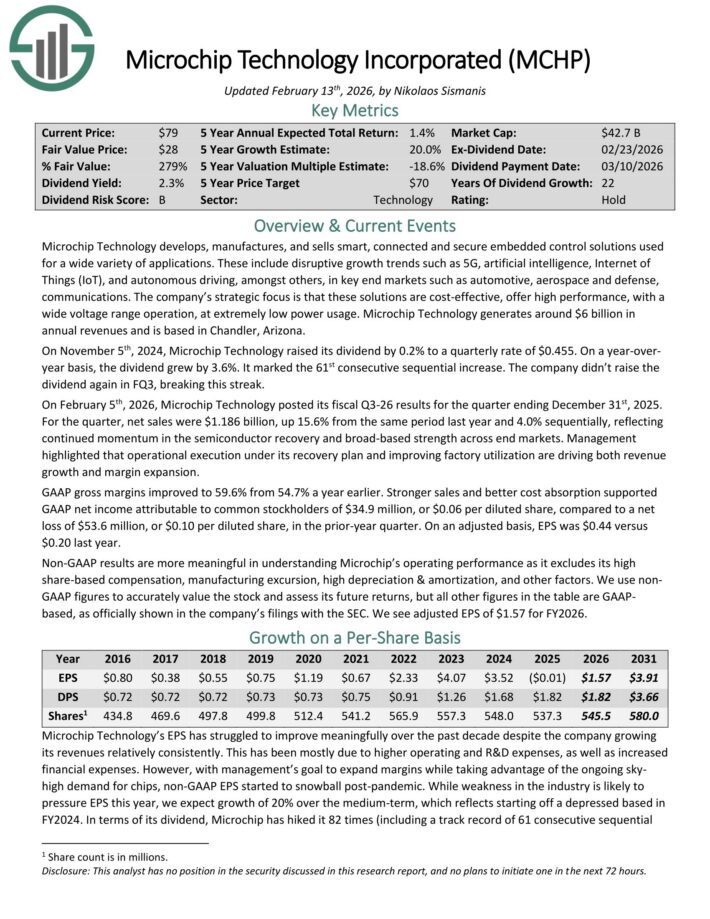

Fast Growing Dividend Stock #9: Microchip Technology (MCHP)

- Dividend Growth: 15.0%

Microchip Technology develops, manufactures, and sells smart, connected and secure embedded control solutions used for a wide variety of applications.

These include disruptive growth trends such as 5G, artificial intelligence, Internet of Things (IoT), and autonomous driving, amongst others, in key end markets such as automotive, aerospace and defense, communications.

On November 5th, 2024, Microchip Technology raised its dividend by 0.2% to a quarterly rate of $0.455. On a year-over-year basis, the dividend grew by 3.6%. It marked the 61st consecutive sequential increase.

On February 5th, 2026, Microchip Technology posted its fiscal Q3-26 results for the quarter ending December 31st, 2025.

For the quarter, net sales were $1.186 billion, up 15.6% from the same period last year and 4.0% sequentially, reflecting continued momentum in the semiconductor recovery and broad-based strength across end markets.

Management highlighted that operational execution under its recovery plan and improving factory utilization are driving both revenue growth and margin expansion.

Click here to download our most recent Sure Analysis report on MCHP (preview of page 1 of 3 shown below):

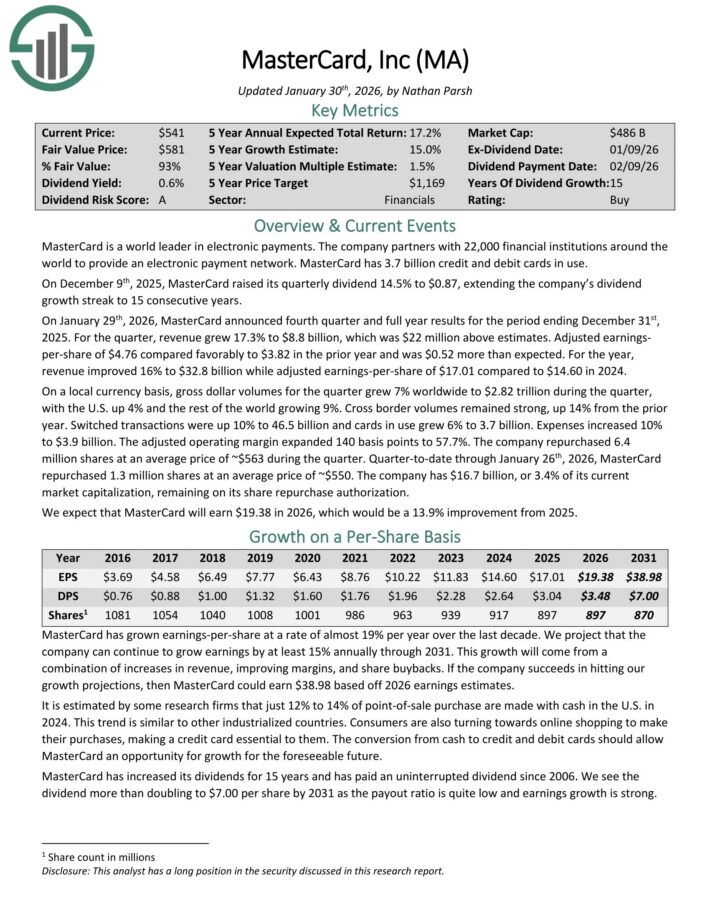

Fast Growing Dividend Stock #8: Mastercard Incorporated (MA)

- Dividend Growth: 15.0%

MasterCard is a world leader in electronic payments. The company partners with 25,000 financial institutions around the world to provide an electronic payment network. MasterCard has more than 3.1 billion credit and debit cards in use.

On January 29th, 2026, MasterCard announced fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue grew 17.3% to $8.8 billion, which was $22 million above estimates.

Adjusted earnings-per-share of $4.76 compared favorably to $3.82 in the prior year and was $0.52 more than expected.

For the year, revenue improved 16% to $32.8 billion while adjusted earnings-per-share of $17.01 compared to $14.60 in 2024.

On a local currency basis, gross dollar volumes for the quarter grew 7% worldwide to $2.82 trillion during the quarter, with the U.S. up 4% and the rest of the world growing 9%. Cross border volumes remained strong, up 14% from the prior year.

Quarter-to-date through January 26th, 2026, MasterCard repurchased 1.3 million shares at an average price of ~$550. The company has $16.7 billion, or 3.4% of its current market capitalization, remaining on its share repurchase authorization.

Click here to download our most recent Sure Analysis report on Mastercard (preview of page 1 of 3 shown below):

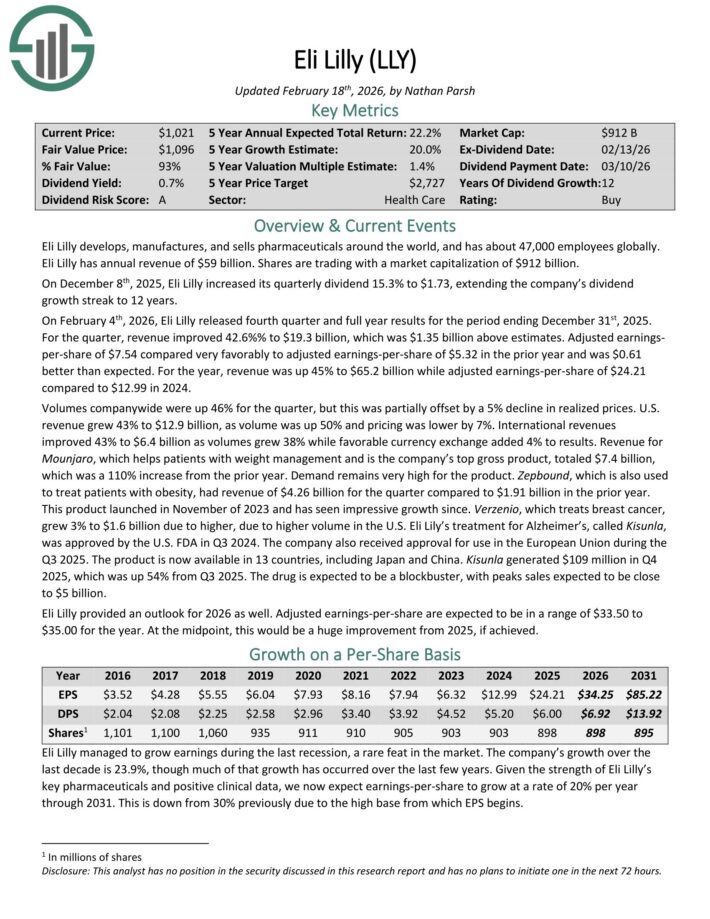

Fast Growing Dividend Stock #7: Eli Lilly & Co. (LLY)

- Dividend Growth: 15.0%

Eli Lilly develops, manufactures, and sells pharmaceuticals around the world, and has about 47,000 employees globally. Eli Lilly has annual revenue of $59 billion.

On December 8th, 2025, Eli Lilly increased its quarterly dividend 15.3% to $1.73, extending the company’s dividend growth streak to 12 years.

On February 4th, 2026, Eli Lilly released fourth quarter and full year results for the period ending December 31st, 2025.

For the quarter, revenue improved 42.6%% to $19.3 billion, which was $1.35 billion above estimates. Adjusted earnings-per-share of $7.54 compared very favorably to adjusted earnings-per-share of $5.32 in the prior year and was $0.61 better than expected.

For the year, revenue was up 45% to $65.2 billion while adjusted earnings-per-share of $24.21 compared to $12.99 in 2024.

Volumes were up 46% for the quarter, but this was partially offset by a 5% decline in realized prices. U.S. revenue grew 43% to $12.9 billion, as volume was up 50% and pricing was lower by 7%.

International revenues improved 43% to $6.4 billion as volumes grew 38% while favorable currency exchange added 4% to results..

Click here to download our most recent Sure Analysis report on LLY (preview of page 1 of 3 shown below):

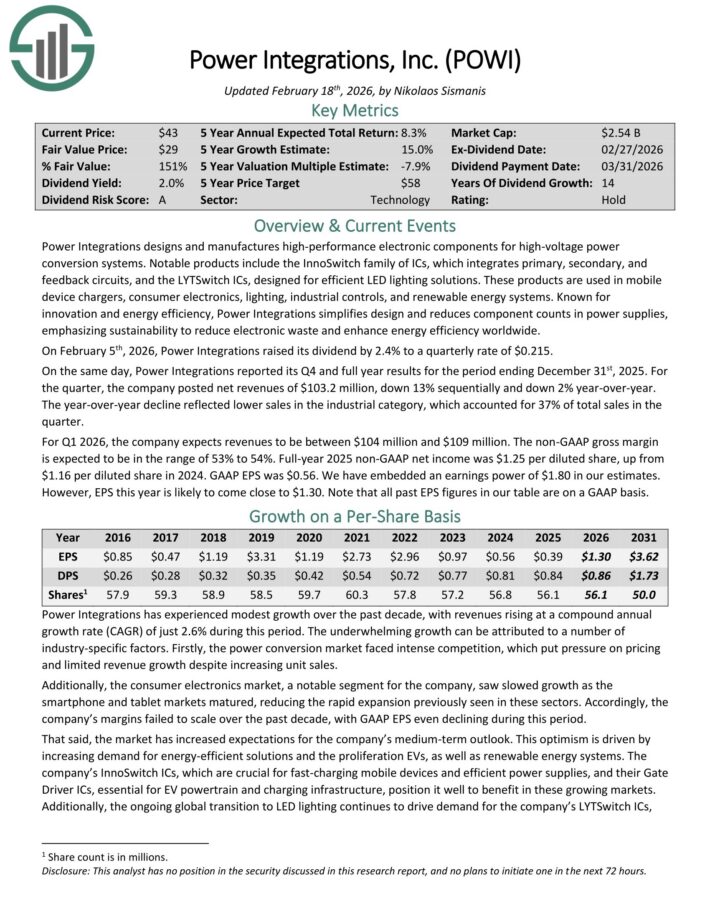

Fast Growing Dividend Stock #6: Power Integrations Inc. (POWI)

- Dividend Growth: 15.0%

Power Integrations designs and manufactures high-performance electronic components for high-voltage power conversion systems.

Notable products include the InnoSwitch family of ICs, which integrates primary, secondary, and feedback circuits, and the LYTSwitch ICs, designed for efficient LED lighting solutions.

These products are used in mobile device chargers, consumer electronics, lighting, industrial controls, and renewable energy systems.

On February 5th, 2026, Power Integrations raised its dividend by 2.4% to a quarterly rate of $0.215.

On the same day, Power Integrations reported its Q4 and full year results for the period ending December 31st, 2025. For the quarter, the company posted net revenues of $103.2 million, down 13% sequentially and down 2% year-over-year.

The year-over-year decline reflected lower sales in the industrial category, which accounted for 37% of total sales in the quarter.

For Q1 2026, the company expects revenues to be between $104 million and $109 million. The non-GAAP gross margin is expected to be in the range of 53% to 54%.

Full-year 2025 non-GAAP net income was $1.25 per diluted share, up from $1.16 per diluted share in 2024. GAAP EPS was $0.56.

Click here to download our most recent Sure Analysis report on POWI (preview of page 1 of 3 shown below):

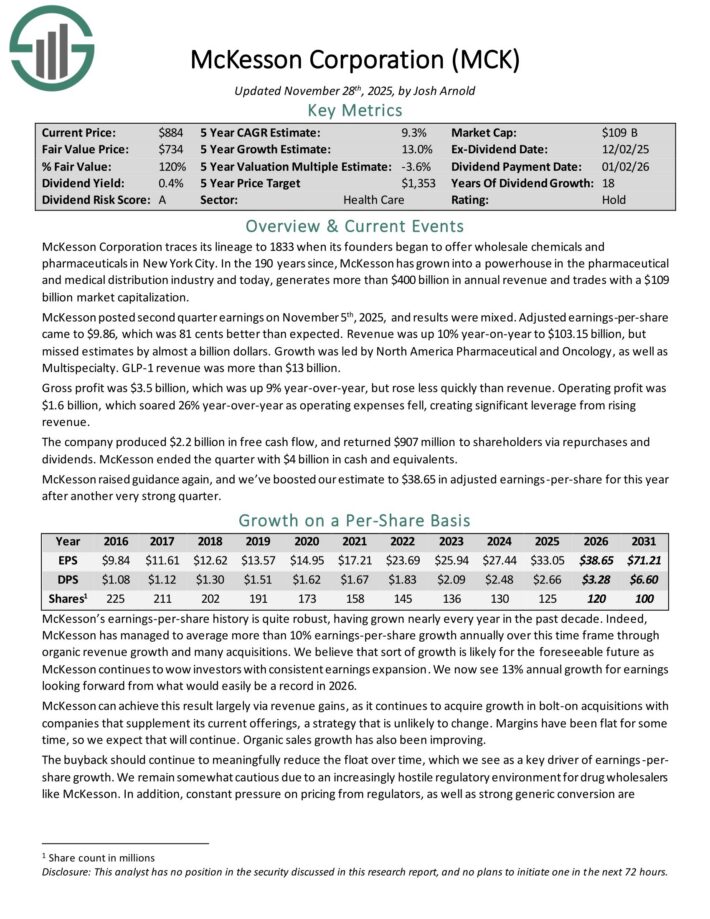

Fast Growing Dividend Stock #5: McKesson Corporation (MCK)

- Dividend Growth: 15.0%

McKesson has grown into a powerhouse in the pharmaceutical and medical distribution industry and today, generates more than $400 billion in annual revenue.

McKesson posted second quarter earnings on November 5th, 2025, and results were mixed. Adjusted earnings-per-share came to $9.86, which was 81 cents better than expected.

Revenue was up 10% year-on-year to $103.15 billion, but missed estimates by almost a billion dollars. Growth was led by North America Pharmaceutical and Oncology, as well as Multispecialty. GLP-1 revenue was more than $13 billion.

Gross profit was $3.5 billion, which was up 9% year-over-year, but rose less quickly than revenue. Operating profit was $1.6 billion, which soared 26% year-over-year as operating expenses fell, creating significant leverage from rising revenue.

The company produced $2.2 billion in free cash flow, and returned $907 million to shareholders via repurchases and dividends. McKesson ended the quarter with $4 billion in cash and equivalents.

Click here to download our most recent Sure Analysis report on MCK (preview of page 1 of 3 shown below):

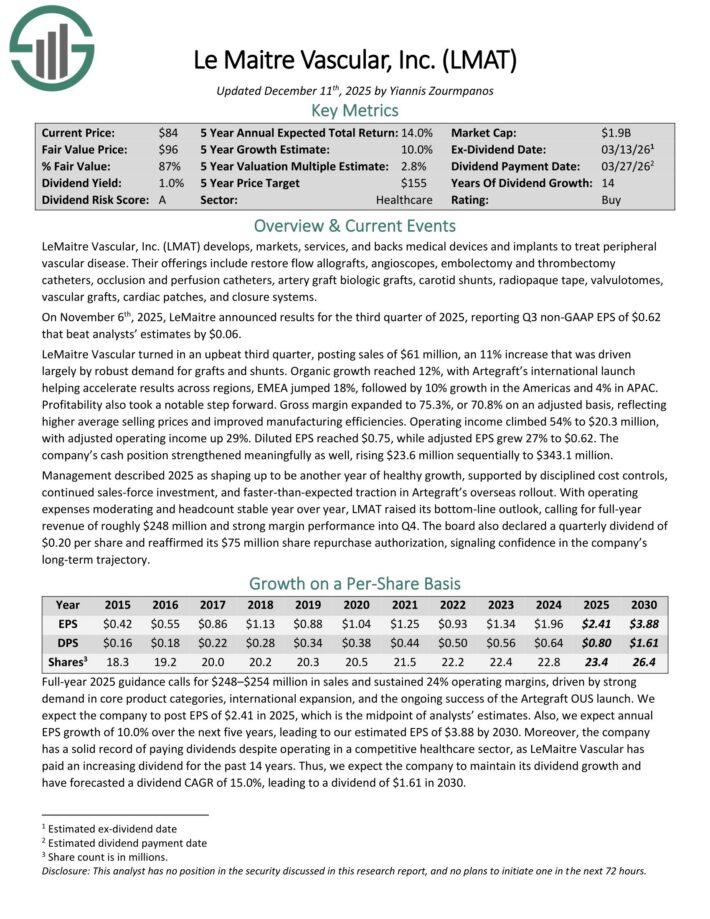

Fast Growing Dividend Stock #4: Lemaitre Vascular (LMAT)

- Dividend Growth: 15.0%

LeMaitre Vascular develops, markets, services, and backs medical devices and implants to treat peripheral vascular disease.

Their offerings include restore flow allografts, angioscopes, embolectomy and thrombectomy catheters, occlusion and perfusion catheters, artery graft biologic grafts, carotid shunts, radiopaque tape, valvulotomes, vascular grafts, cardiac patches, and closure systems.

On November 6th, 2025, LeMaitre announced results for the third quarter of 2025, reporting Q3 non-GAAP EPS of $0.62 that beat analysts’ estimates by $0.06.

LeMaitre Vascular turned in an upbeat third quarter, posting sales of $61 million, an 11% increase that was driven largely by robust demand for grafts and shunts.

Organic growth reached 12%, with Artegraft’s international launch helping accelerate results across regions, EMEA jumped 18%, followed by 10% growth in the Americas and 4% in APAC.

Profitability also took a notable step forward. Gross margin expanded to 75.3%, or 70.8% on an adjusted basis, reflecting higher average selling prices and improved manufacturing efficiencies.

Operating income climbed 54% to $20.3 million, with adjusted operating income up 29%. Diluted EPS reached $0.75, while adjusted EPS grew 27% to $0.62.

The company’s cash position strengthened meaningfully as well, rising $23.6 million sequentially to $343.1 million.

Management described 2025 as shaping up to be another year of healthy growth, supported by disciplined cost controls, continued sales-force investment, and faster-than-expected traction in Artegraft’s overseas rollout.

With operating expenses moderating and headcount stable year over year, LMAT raised its bottom-line outlook, calling for full-year revenue of roughly $248 million and strong margin performance into Q4.

The board also declared a quarterly dividend of $0.20 per share and reaffirmed its $75 million share repurchase authorization.

Click here to download our most recent Sure Analysis report on LMAT (preview of page 1 of 3 shown below):

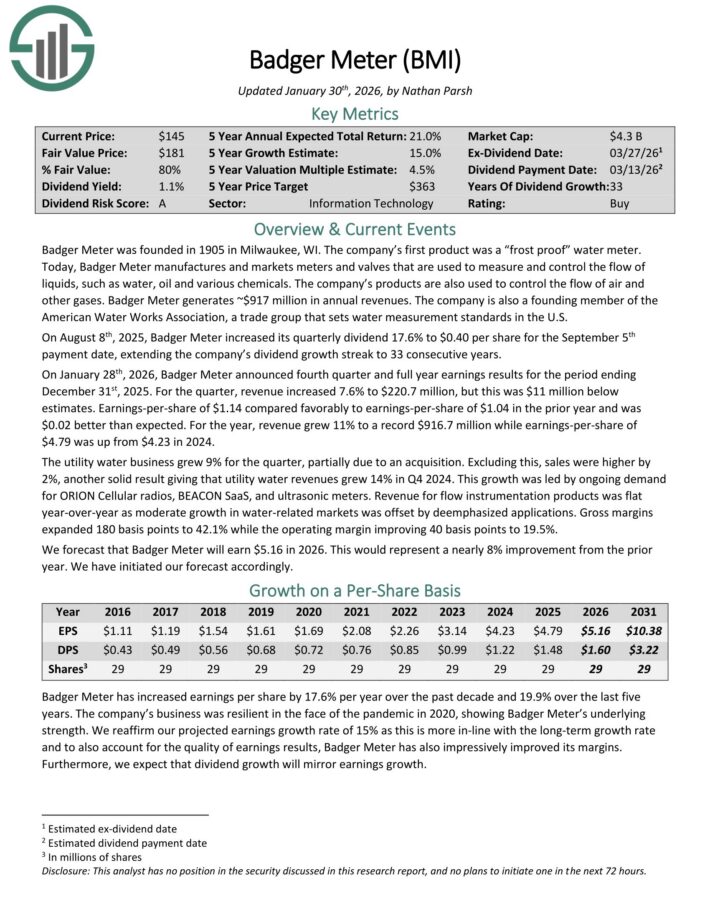

Fast Growing Dividend Stock #3: Badger Meter Inc. (BMI)

- Dividend Growth: 15.0%

Badger Meter manufactures and markets meters and valves that are used to measure and control the flow of liquids, such as water, oil and various chemicals.

The company’s products are also used to control the flow of air and other gases. Badger Meter generates ~$917 million in annual revenues.

On January 28th, 2026, Badger Meter announced fourth quarter and full year earnings results. For the quarter, revenue increased 7.6% to $220.7 million, but this was $11 million below estimates.

Earnings-per-share of $1.14 compared favorably to earnings-per-share of $1.04 in the prior year and was $0.02 better than expected. For the year, revenue grew 11% to a record $916.7 million while earnings-per-share of $4.79 was up from $4.23 in 2024.

The utility water business grew 9% for the quarter, partially due to an acquisition. Excluding this, sales were higher by 2%, another solid result giving that utility water revenues grew 14% in Q4 2024. This growth was led by ongoing demand for ORION Cellular radios, BEACON SaaS, and ultrasonic meters.

Revenue for flow instrumentation products was flat year-over-year as moderate growth in water-related markets was offset by deemphasized applications.

Click here to download our most recent Sure Analysis report on BMI (preview of page 1 of 3 shown below):

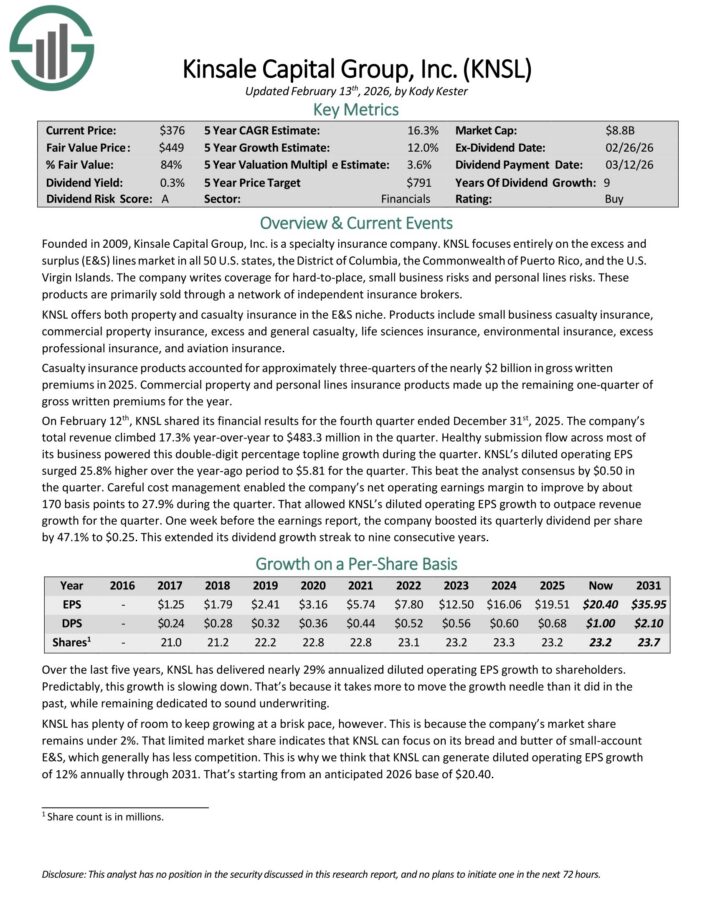

Fast Growing Dividend Stock #2: Kinsale Capital Group (KNSL)

- Dividend Growth: 16.0%

Kinsale Capital Group is a specialty insurance company. KNSL focuses entirely on the excess and surplus (E&S) lines market in all 50 U.S. states, the District of Columbia, the Commonwealth of Puerto Rico, and the U.S. Virgin Islands.

The company writes coverage for hard-to-place, small business risks and personal lines risks. These products are primarily sold through a network of independent insurance brokers.

KNSL offers both property and casualty insurance in the E&S niche. Products include small business casualty insurance, commercial property insurance, excess and general casualty, life sciences insurance, environmental insurance, excess professional insurance, and aviation insurance.

On February 12th, KNSL shared its financial results for the fourth quarter ended December 31st, 2025. The company’s total revenue climbed 17.3% year-over-year to $483.3 million in the quarter. Healthy submission flow across most of its business powered this double-digit percentage topline growth during the quarter.

KNSL’s diluted operating EPS surged 25.8% higher over the year-ago period to $5.81 for the quarter. This beat the analyst consensus by $0.50 in the quarter. Careful cost management enabled the company’s net operating earnings margin to improve by about 170 basis points to 27.9% during the quarter.

That allowed KNSL’s diluted operating EPS growth to outpace revenue growth for the quarter. One week before the earnings report, the company boosted its quarterly dividend per share by 47.1% to $0.25.

Click here to download our most recent Sure Analysis report on KNSL (preview of page 1 of 3 shown below):

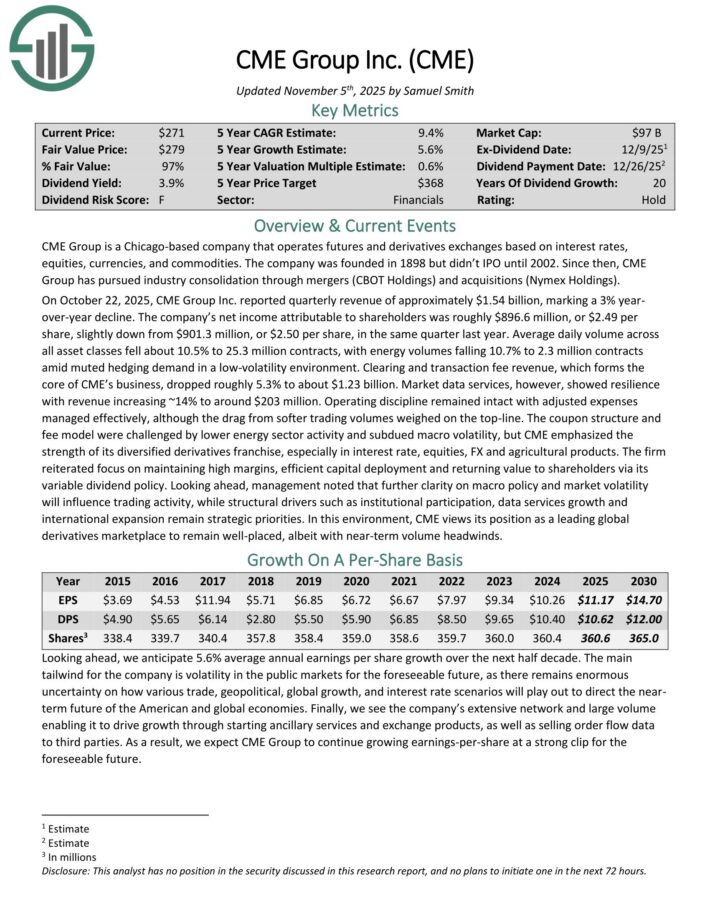

Fast Growing Dividend Stock #1: CME Group Inc. (CME)

- Dividend Growth: 18.2%

CME Group is a Chicago-based company that operates futures and derivatives exchanges based on interest rates, equities, currencies, and commodities. The company was founded in 1898 but didn’t IPO until 2002.

Since then, CME Group has pursued industry consolidation through mergers (CBOT Holdings) and acquisitions (Nymex Holdings).

On October 22, 2025, CME Group Inc. reported quarterly revenue of approximately $1.54 billion, marking a 3% year-over-year decline.

The company’s net income attributable to shareholders was roughly $896.6 million, or $2.49 per share, slightly down from $901.3 million, or $2.50 per share, in the same quarter last year.

Average daily volume across all asset classes fell about 10.5% to 25.3 million contracts, with energy volumes falling 10.7% to 2.3 million contracts amid muted hedging demand in a low-volatility environment.

Clearing and transaction fee revenue, which forms the core of CME’s business, dropped roughly 5.3% to about $1.23 billion. Market data services, however, showed resilience with revenue increasing ~14% to around $203 million.

Click here to download our most recent Sure Analysis report on CME (preview of page 1 of 3 shown below):

Other Blue Chip Stock Resources

The resources below will give you a better understanding of dividend growth investing:

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Kings: 50+ Consecutive years of dividend increases

- Dividend Champions: 25+ Consecutive years of dividend increases

- The Best DRIP Stocks: The top 15 Dividend Champions with no-fee dividend reinvestment plans