Published on March 30th, 2026 by Bob Ciura

The S&P 500 Index performed well in 2025, but is down roughly 6% year-to-date.

Plenty of risks remain. The ongoing wars around the world have elevated geopolitical risk. There is also renewed political risk to the stock market in the form of tariffs.

In times of elevated risks, income investors should pursue recession-proof stocks.

The Dividend Kings are a great example of this. The Dividend Kings have increased their dividends for at least 50 consecutive years.

You can see the full downloadable spreadsheet of all 57 Dividend Kings (along with important financial metrics such as dividend yields, payout ratios, and price-to-earnings ratios) by clicking on the link below:

The 10 recession proof stocks below are Dividend Kings based in the U.S., with 50+ consecutive years of dividend increases.

These 10 stocks also have Dividend Risk Scores of ‘A’, our highest rating. Lastly, they are all given buy ratings due to their high expected returns.

The 10 stocks are ranked by dividend yield below.

Table of Contents

- Recession Proof Stock: PPG Industries (PPG)

- Recession Proof Stock: California Water Service Group (CWT)

- Recession Proof Stock: H2O America (HTO)

- Recession Proof Stock: ABM Industries (ABM)

- Recession Proof Stock: Stepan Co. (SCL)

- Recession Proof Stock: Automatic Data Processing (ADP)

- Recession Proof Stock: Northwest Natural Holding (NWN)

- Recession Proof Stock: PepsiCo Inc. (PEP)

- Recession Proof Stock: Genuine Parts Co. (GPC)

- Recession Proof Stock: Black Hills Corporation (BKH)

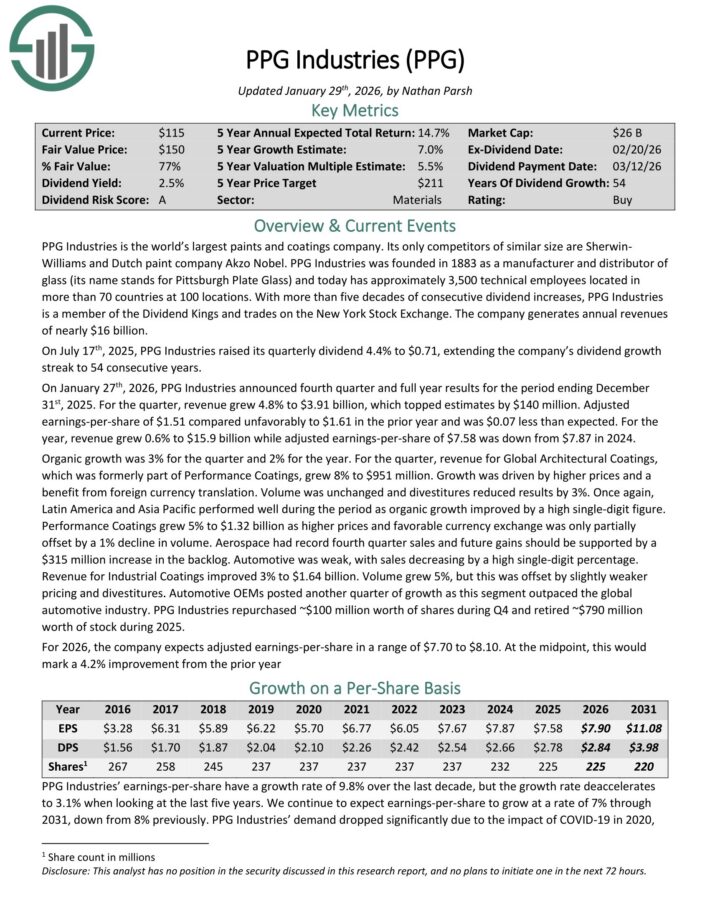

Recession Proof Stock: PPG Industries (PPG)

- Dividend Yield: 2.7%

PPG Industries is the world’s largest paints and coatings company. Its only competitors of similar size are Sherwin-Williams and Dutch paint company Akzo Nobel.

On January 27th, 2026, PPG Industries announced fourth quarter and full year results. For the quarter, revenue grew 4.8% to $3.91 billion, which topped estimates by $140 million. Adjusted earnings-per-share of $1.51 compared unfavorably to $1.61 in the prior year and was $0.07 less than expected.

For the year, revenue grew 0.6% to $15.9 billion while adjusted earnings-per-share of $7.58 was down from $7.87 in 2024. Organic growth was 3% for the quarter and 2% for the year.

For the quarter, revenue for Global Architectural Coatings, which was formerly part of Performance Coatings, grew 8% to $951 million.

Growth was driven by higher prices and a benefit from foreign currency translation. Volume was unchanged and divestitures reduced results by 3%.

Once again, Latin America and Asia Pacific performed well during the period as organic growth improved by a high single-digit figure.

Performance Coatings grew 5% to $1.32 billion as higher prices and favorable currency exchange was only partially offset by a 1% decline in volume.

Aerospace had record fourth quarter sales and future gains should be supported by a $315 million increase in the backlog. Automotive was weak, with sales decreasing by a high single-digit percentage.

Revenue for Industrial Coatings improved 3% to $1.64 billion. Volume grew 5%, but this was offset by slightly weaker pricing and divestitures. Automotive OEMs posted another quarter of growth as this segment outpaced the global automotive industry.

PPG Industries repurchased ~$100 million worth of shares during Q4 and retired ~$790 million worth of stock during 2025.

Click here to download our most recent Sure Analysis report on PPG (preview of page 1 of 3 shown below):

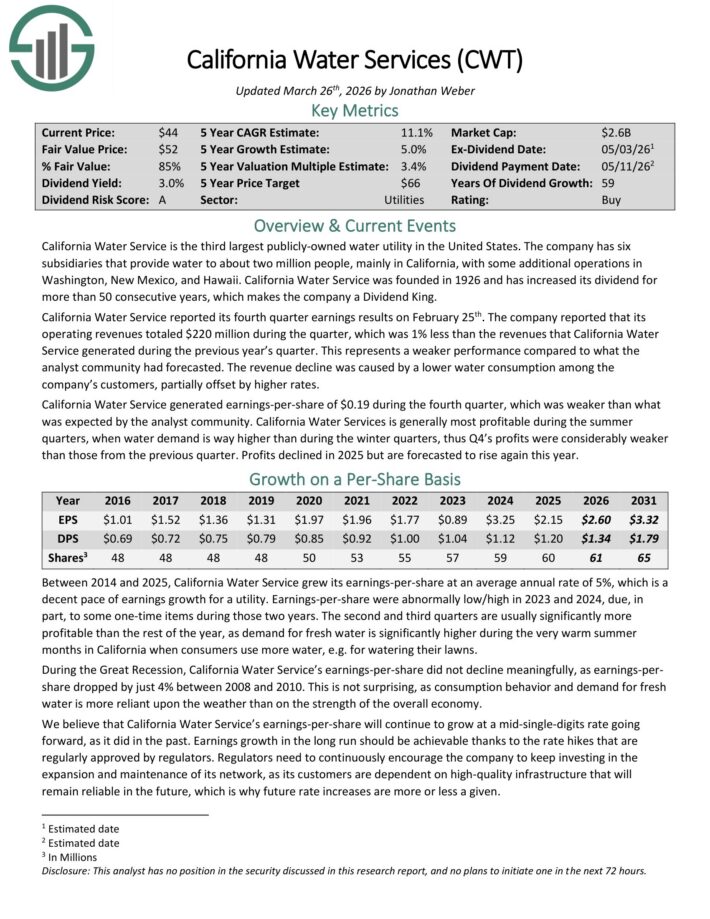

Recession Proof Stock: California Water Service Group (CWT)

- Dividend Yield: 3.0%

California Water Service is the third largest publicly-owned water utility in the United States.

The company has six subsidiaries that provide water to about two million people, mainly in California, with some additional operations in Washington, New Mexico, and Hawaii.

California Water Service was founded in 1926 and has increased its dividend for more than 50 consecutive years, which makes the company a Dividend King.

California Water Service reported its fourth quarter earnings results on February 25th. The company reported that its operating revenues totaled $220 million during the quarter, down 1% year-over-year.

The revenue decline was caused by a lower water consumption among the company’s customers, partially offset by higher rates.

California Water Service generated earnings-per-share of $0.19 during the fourth quarter, which was weaker than what was expected by the analyst community.

Click here to download our most recent Sure Analysis report on CWT (preview of page 1 of 3 shown below):

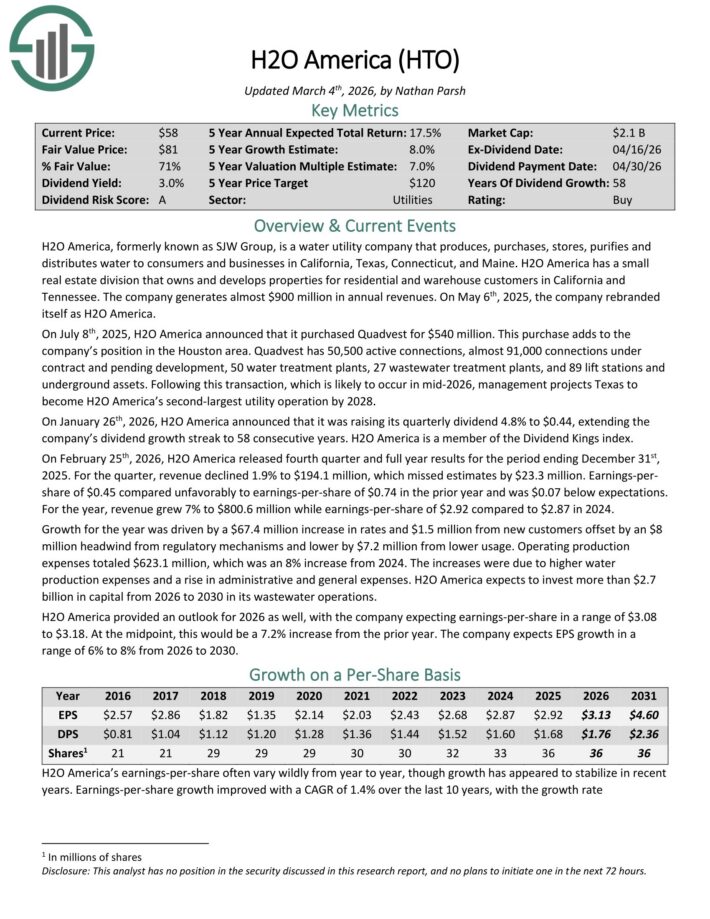

Recession Proof Stock: H2O America (HTO)

- Dividend Yield: 3.0%

H2O America, formerly known as SJW Group, is a water utility company that produces, purchases, stores, purifies and distributes water to consumers and businesses in the Silicon Valley area of California, the area north of San Antonio, Texas, Connecticut, and Maine.

It also has a small real estate division that owns and develops properties for residential and warehouse customers in California and Tennessee. The company generates about $670 million in annual revenues.

On July 8th, 2025, H2O America announced that it purchased Quadvest for $540 million. This purchase adds to the company’s position in the Houston area.

Quadvest has 50,500 active connections, almost 91,000 connections under contract and pending development, 50 water treatment plants, 27 wastewater treatment plants, and 89 lift stations and underground assets.

On January 26th, 2026, H2O America raised its quarterly dividend 4.8% to $0.44, extending the company’s dividend growth streak to 58 consecutive years.

On February 25th, 2026, H2O America released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue declined 1.9% to $194.1 million, which missed estimates by $23.3 million.

Earnings-per-share of $0.45 compared unfavorably to earnings-per-share of $0.74 in the prior year and was $0.07 below expectations.

For the year, revenue grew 7% to $800.6 million while earnings-per-share of $2.92 compared to $2.87 in 2024.

Growth for the year was driven by a $67.4 million increase in rates and $1.5 million from new customers offset by an $8 million headwind from regulatory mechanisms and lower by $7.2 million from lower usage.

Click here to download our most recent Sure Analysis report on HTO (preview of page 1 of 3 shown below):

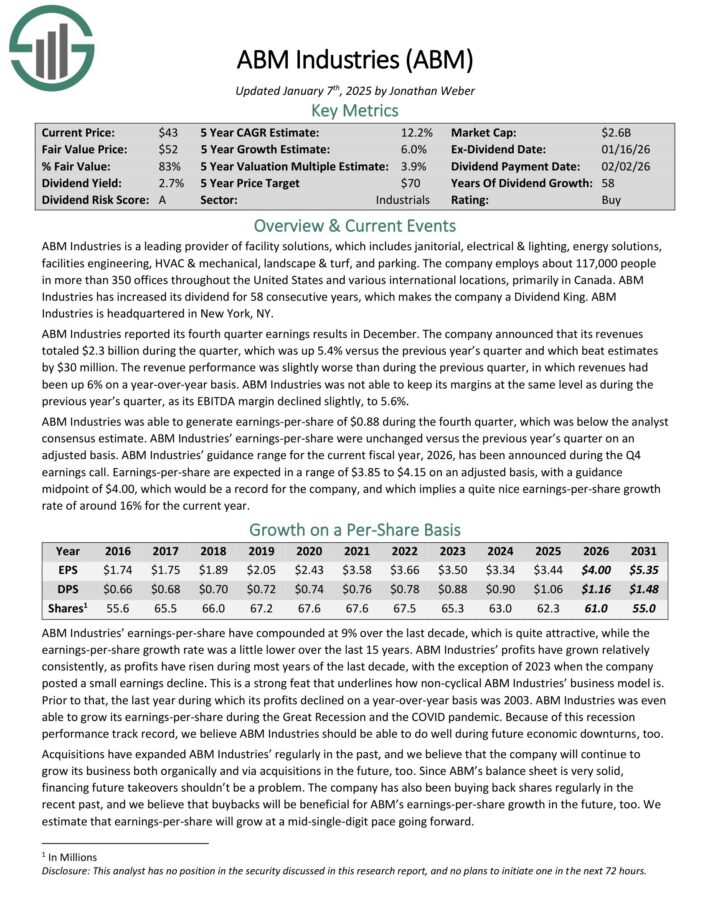

Recession Proof Stock: ABM Industries (ABM)

- Dividend Yield: 3.1%

ABM Industries is a leading provider of facility solutions, which includes janitorial, electrical & lighting, energy solutions, facilities engineering, HVAC & mechanical, landscape & turf, and parking.

The company employs about 117,000 people in more than 350 offices throughout the United States and various international locations, primarily in Canada.

ABM Industries has increased its dividend for 58 consecutive years.

ABM Industries reported its fourth quarter earnings results in December. The company announced that its revenues totaled $2.3 billion during the quarter, which was up 5.4% versus the previous year’s quarter and which beat estimates by $30 million.

ABM Industries was able to generate earnings-per-share of $0.88 during the fourth quarter, which was below the analyst consensus estimate. ABM Industries’ earnings-per-share were unchanged versus the previous year’s quarter on an adjusted basis.

Earnings-per-share are expected in a range of $3.85 to $4.15 on an adjusted basis for 2026, with a guidance midpoint of $4.00, which would be a record for the company.

Click here to download our most recent Sure Analysis report on ABM (preview of page 1 of 3 shown below):

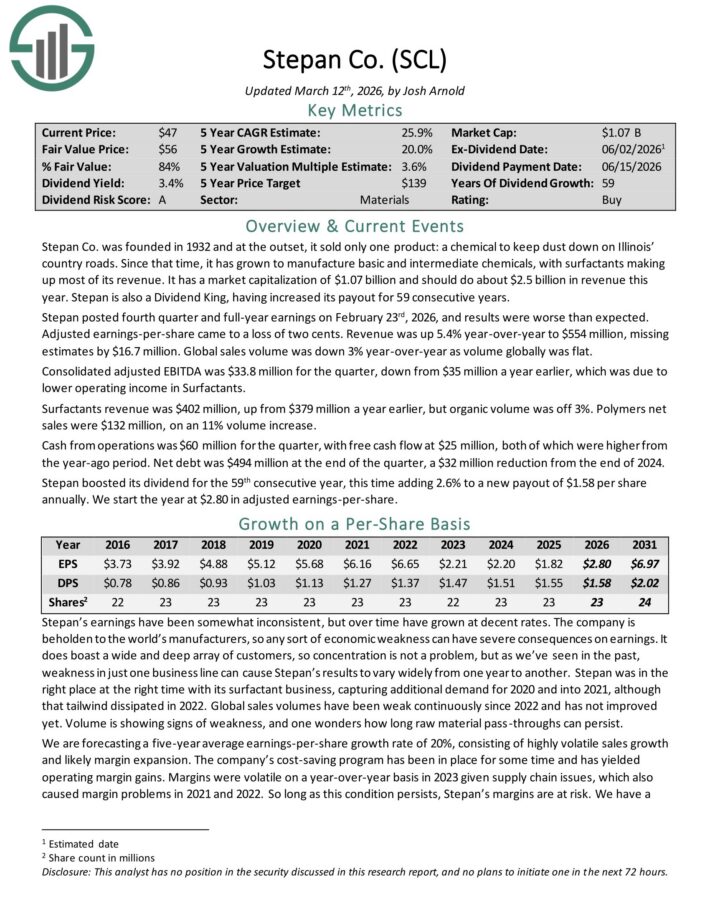

Recession Proof Stock: Stepan Co. (SCL)

- Dividend Yield: 3.2%

Stepan manufactures basic and intermediate chemicals, including surfactants, specialty products, germicidal and fabric softening quaternaries, phthalic anhydride, polyurethane polyols and special ingredients for the food, supplement, and pharmaceutical markets.

It is organized into three distinct business lines: surfactants, polymers, and specialty products. These businesses serve a wide variety of end markets, meaning that Stepan is not beholden to just a handful of industries.

The surfactants business is Stepan’s largest by revenue, accounting for ~68% of total sales in the most recent quarter. A surfactant is an organic compound that contains both water-soluble and water-insoluble components.

Stepan posted fourth quarter and full-year earnings on February 23rd, 2026. Adjusted earnings-per-share came to a loss of two cents.

Revenue was up 5.4% year-over-year to $554 million, missing estimates by $16.7 million. Global sales volume was down 3% year-over-year as volume globally was flat.

Consolidated adjusted EBITDA was $33.8 million for the quarter, down from $35 million a year earlier, which was due to lower operating income in Surfactants.

Surfactants revenue was $402 million, up from $379 million a year earlier, but organic volume was off 3%. Polymers net sales were $132 million, on an 11% volume increase.

Cash from operations was $60 million for the quarter, with free cash flow at $25 million, both of which were higher from the year-ago period. Net debt was $494 million at the end of the quarter, a $32 million reduction from the end of 2024.

Stepan boosted its dividend for the 59th consecutive year.

Click here to download our most recent Sure Analysis report on SCL (preview of page 1 of 3 shown below):

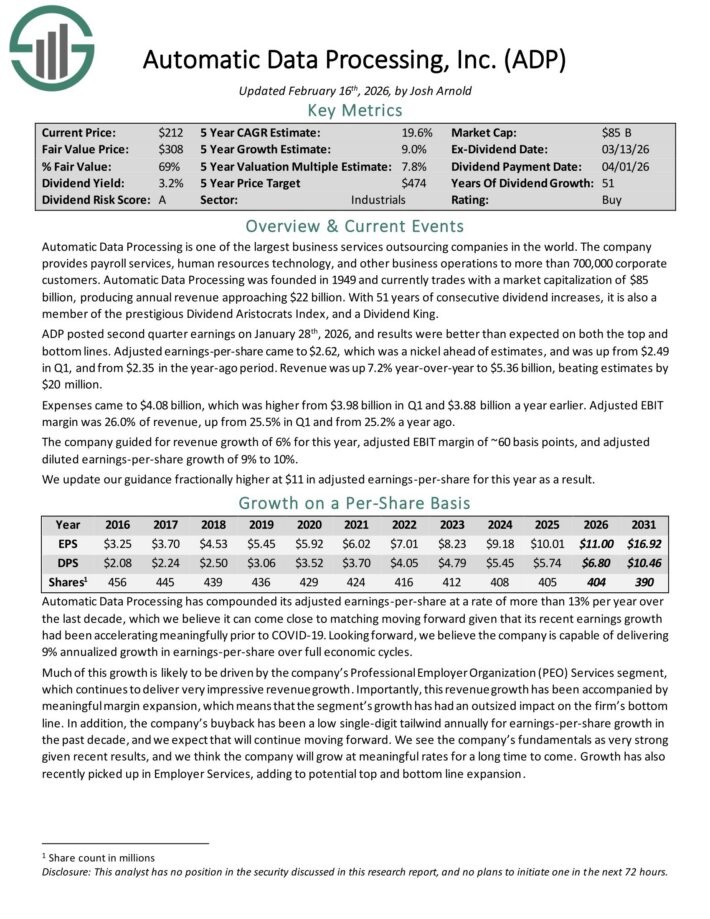

Recession Proof Stock: Automatic Data Processing (ADP)

- Dividend Yield: 3.4%

Automatic Data Processing is one of the largest business services outsourcing companies in the world. The company provides payroll services, human resources technology, and other business operations to more than 700,000 corporate customers.

ADP posted second quarter earnings on January 28th, 2026, and results were better than expected on both the top and bottom lines.

Adjusted earnings-per-share came to $2.62, which was a nickel ahead of estimates, and was up from $2.49 in Q1, and from $2.35 in the year-ago period. Revenue was up 7.2% year-over-year to $5.36 billion, beating estimates by $20 million.

Expenses came to $4.08 billion, which was higher from $3.98 billion in Q1 and $3.88 billion a year earlier. Adjusted EBIT margin was 26.0% of revenue, up from 25.5% in Q1 and from 25.2% a year ago.

The company guided for revenue growth of 6% for this year, adjusted EBIT margin of ~60 basis points, and adjusted diluted earnings-per-share growth of 9% to 10%.

Click here to download our most recent Sure Analysis report on ADP (preview of page 1 of 3 shown below):

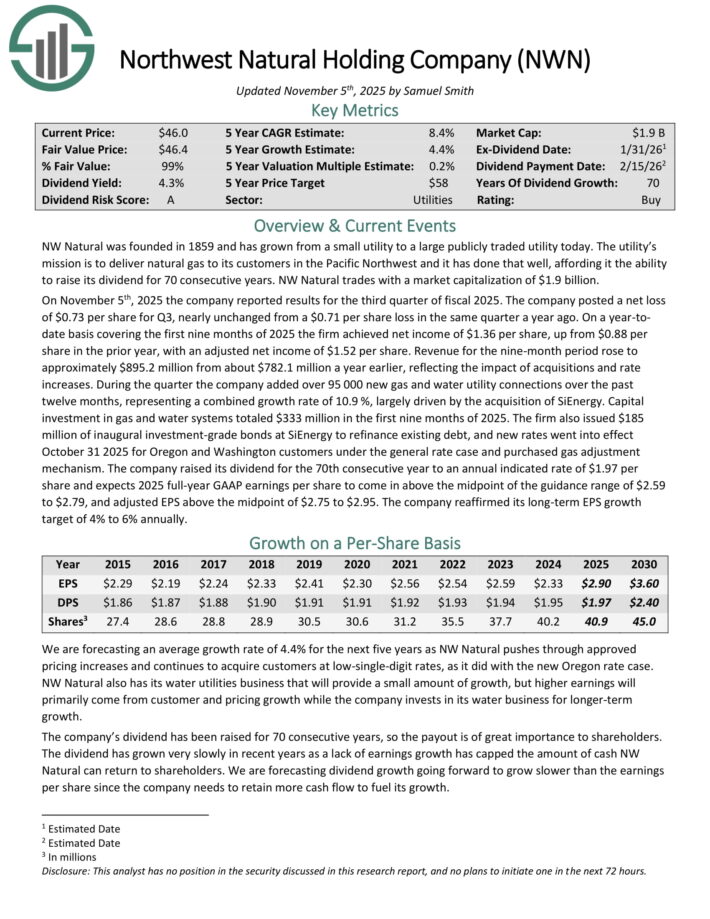

Recession Proof Stock: Northwest Natural Holding (NWN)

- Dividend Yield: 3.7%

NW Natural was founded in 1859 and has grown from just a handful of customers to serving more than 760,000 today. The utility’s mission is to deliver natural gas to its customers in the Pacific Northwest.

The company’s locations served are shown in the image below.

On November 5th, 2025 the company reported results for the third quarter of fiscal 2025. The company posted a net loss of $0.73 per share for Q3, nearly unchanged from a $0.71 per share loss in the same quarter a year ago.

On a year-to-date basis covering the first nine months of 2025 the firm achieved net income of $1.36 per share, up from $0.88 per share in the prior year, with an adjusted net income of $1.52 per share.

Revenue for the nine-month period rose to approximately $895.2 million from about $782.1 million a year earlier, reflecting the impact of acquisitions and rate increases.

Click here to download our most recent Sure Analysis report on NWN (preview of page 1 of 3 shown below):

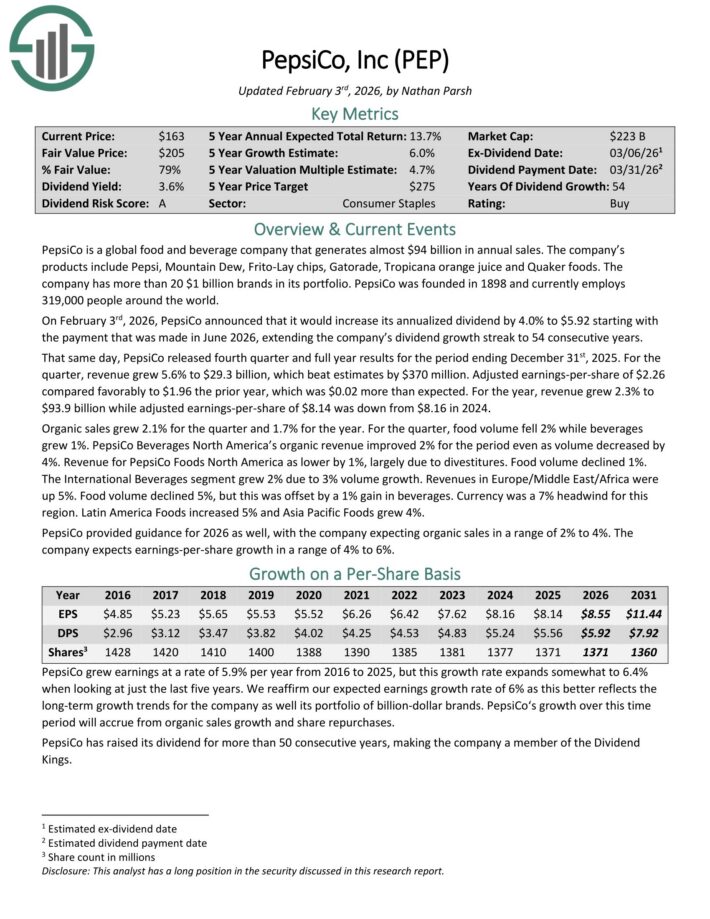

Recession Proof Stock: PepsiCo Inc. (PEP)

- Dividend Yield: 3.9%

PepsiCo is a global food and beverage company that generates almost $94 billion in annual sales. The company’s products include Pepsi, Mountain Dew, Frito-Lay chips, Gatorade, Tropicana orange juice and Quaker foods.

The company has more than 20 $1 billion brands in its portfolio.

On February 3rd, 2026, PepsiCo announced that it would increase its annualized dividend by 4.0% to $5.92 starting with the payment that was made in June 2026, extending the company’s dividend growth streak to 54 consecutive years.

That same day, PepsiCo released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue grew 5.6% to $29.3 billion, which beat estimates by $370 million.

Adjusted earnings-per-share of $2.26 compared favorably to $1.96 the prior year, which was $0.02 more than expected.

For the year, revenue grew 2.3% to $93.9 billion while adjusted earnings-per-share of $8.14 was down from $8.16 in 2024. Organic sales grew 2.1% for the quarter and 1.7% for the year.

For the quarter, food volume fell 2% while beverages grew 1%. PepsiCo Beverages North America’s organic revenue improved 2% for the period even as volume decreased by 4%.

Revenue for PepsiCo Foods North America as lower by 1%, largely due to divestitures. Food volume declined 1%.

The International Beverages segment grew 2% due to 3% volume growth. Revenues in Europe/Middle East/Africa were up 5%. Food volume declined 5%, but this was offset by a 1% gain in beverages.

Currency was a 7% headwind for this region. Latin America Foods increased 5% and Asia Pacific Foods grew 4%.

PepsiCo provided guidance for 2026 as well, with the company expecting organic sales in a range of 2% to 4%. The company expects earnings-per-share growth in a range of 4% to 6%.

Click here to download our most recent Sure Analysis report on PEP (preview of page 1 of 3 shown below):

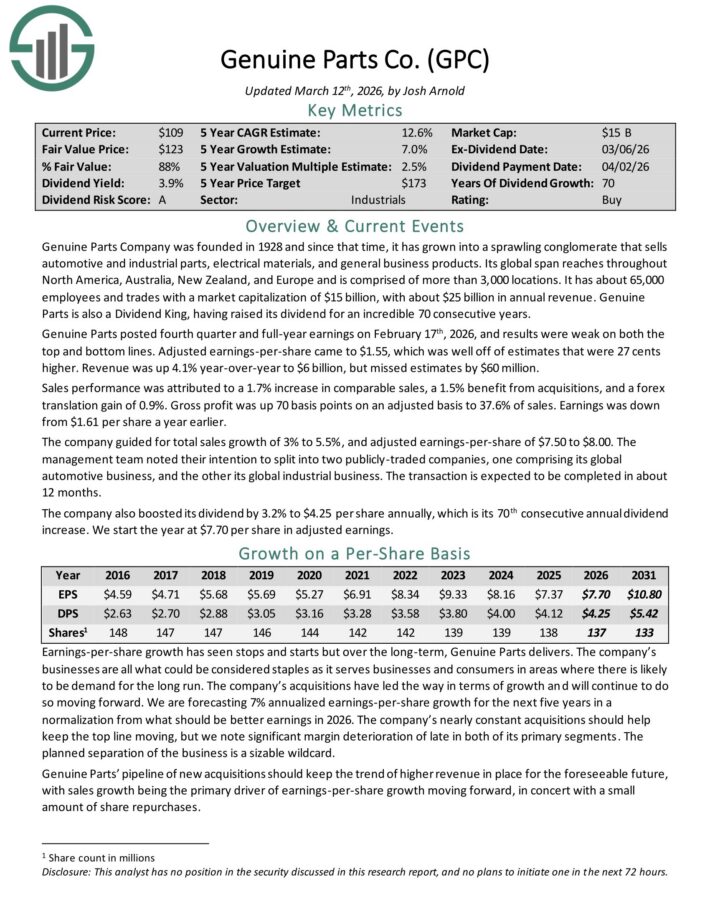

Recession Proof Stock: Genuine Parts Co. (GPC)

- Dividend Yield: 4.0%

Genuine Parts Company was founded in 1928 and since that time, it has grown into a sprawling conglomerate that sells automotive and industrial parts, electrical materials, and general business products.

Its global span reaches throughout North America, Australia, New Zealand, and Europe and is comprised of more than 3,000 locations. It has about 63,000 employees with about $24 billion in annual revenue.

Genuine Parts is also a Dividend King, having raised its dividend for an incredible 69 consecutive years.

Genuine Parts posted fourth quarter and full-year earnings on February 17th, 2026, and results were weak on both the top and bottom lines. Adjusted earnings-per-share came to $1.55, which was well off of estimates that were 27 cents higher. Revenue was up 4.1% year-over-year to $6 billion, but missed estimates by $60 million.

Sales performance was attributed to a 1.7% increase in comparable sales, a 1.5% benefit from acquisitions, and a forex translation gain of 0.9%. Gross profit was up 70 basis points on an adjusted basis to 37.6% of sales. Earnings was down from $1.61 per share a year earlier.

The company guided for total sales growth of 3% to 5.5%, and adjusted earnings-per-share of $7.50 to $8.00.

Click here to download our most recent Sure Analysis report on GPC (preview of page 1 of 3 shown below):

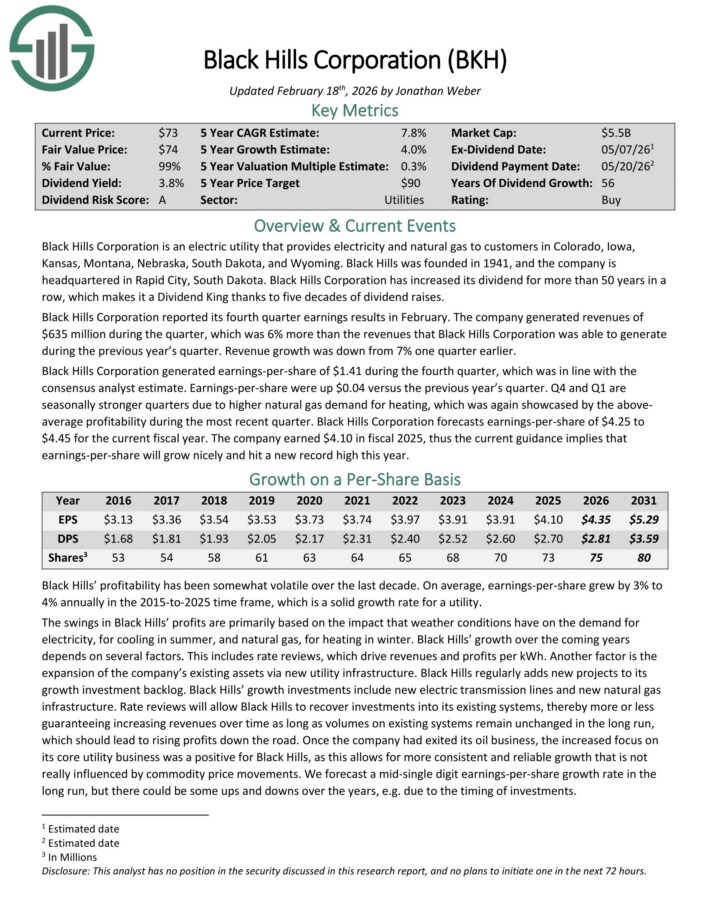

Recession Proof Stock: Black Hills Corporation (BKH)

- Dividend Yield: 4.1%

Black Hills Corporation is an electric utility that provides electricity and natural gas to customers in Colorado, Iowa, Kansas, Montana, Nebraska, South Dakota, and Wyoming.

The company has 1.35 million utility customers in eight states. Its natural gas assets include 49,200 miles of natural gas lines. Separately, it has ~9,200 miles of electric lines and 1.4 gigawatts of electric generation capacity.

Black Hills Corporation reported its fourth quarter earnings results in February. The company generated revenue of $635 million during the quarter, which was 6% more than the previous year’s fourth quarter.

Black Hills Corporation generated earnings-per-share of $1.41 during the fourth quarter, which was in line with the consensus analyst estimate. Earnings-per-share were up $0.04 versus the previous year’s quarter.

Q4 and Q1 are seasonally stronger quarters due to higher natural gas demand for heating, which was again showcased by the above-average profitability during the most recent quarter. Black Hills Corporation forecasts earnings-per-share of $4.25 to $4.45 for the current fiscal year.

Click here to download our most recent Sure Analysis report on BKH (preview of page 1 of 3 shown below):

Additional Resources

The Dividend Kings are not the only high-quality dividend growth stock ideas.

Sure Dividend maintains similar databases on the following useful universes of stocks:

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Dividend Aristocrats: S&P 500 stocks with 25+ years of consecutive dividend increases.

- The Complete List of High Dividend Stocks: Stocks with 5%+ dividend yields.

- The Complete List of Monthly Dividend Stocks: our database currently contains roughly 80 stocks that pay dividends every month.