Updated on March 4th, 2023 by Nikolaos Sismanis

The renewable energy industry is not well-known for recession-resistant businesses. Companies in the sector tend to be unprofitable and typically do not pay dividends to shareholders.

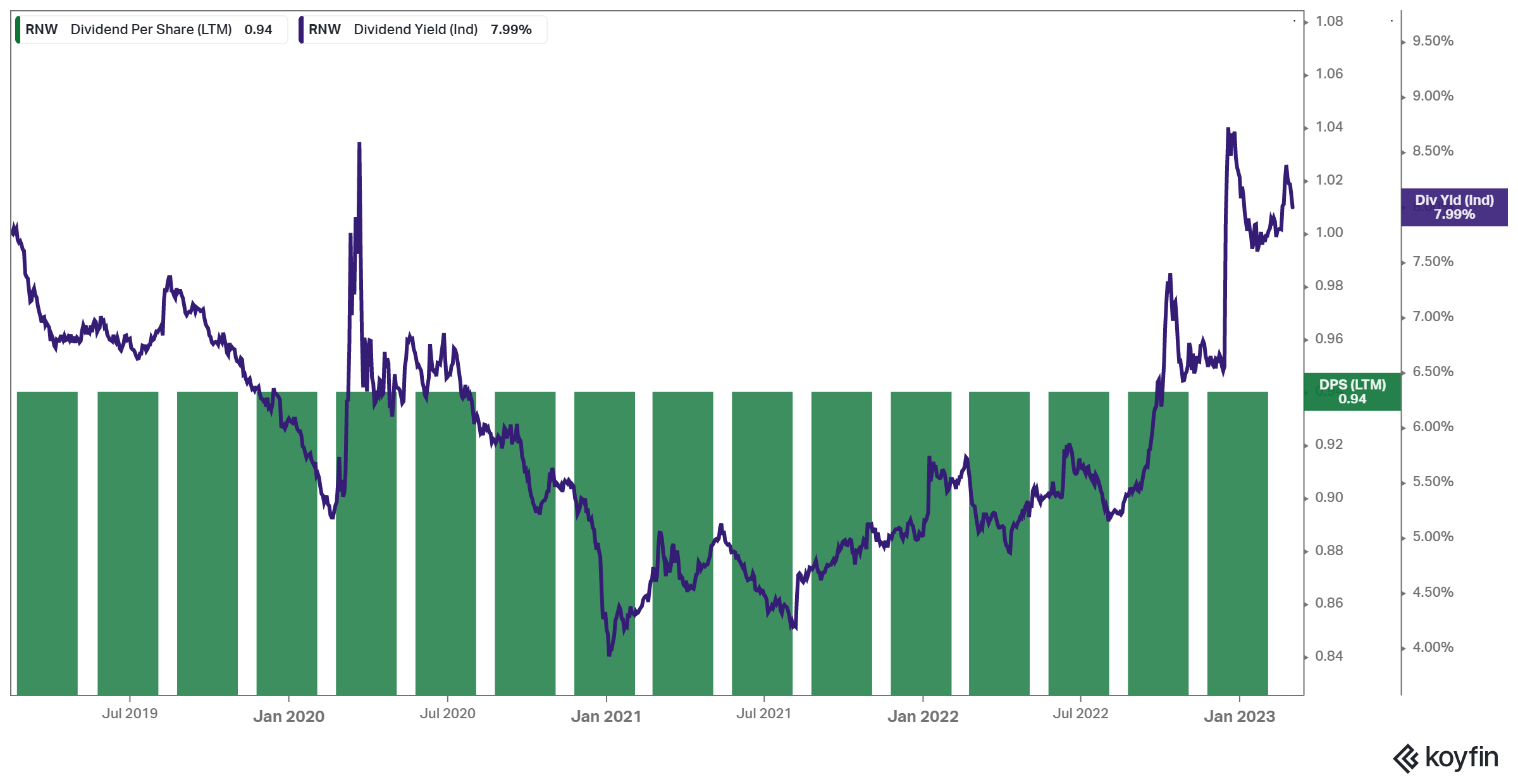

Many investors might avoid the renewables industry as a result, but TransAlta Renewables (TRSWF) is an under-appreciated company in renewable energy. TransAlta is attractive for dividend growth investors for a number of reasons. First, it has a high dividend yield of 8.0%.

Beyond its high dividend yield, TransAlta Renewables is also quite unique because it pays monthly dividends instead of the traditional quarterly distribution schedule.

You can download our full list of 84 monthly dividend stocks (along with relevant financial metrics like dividend yields and payout ratios) by clicking on the link below:

TransAlta Renewables’ high dividend yield and monthly dividend payments are two big reasons why this company stands out to income investors.

That said, proper due diligence is still required for any high-yield stock to ensure that its payout is sustainable.

Business Overview

TransAlta Renewables is a renewable energy infrastructure company headquartered in Calgary, Alberta.

With a market capitalization of $2.3 billion, TransAlta is Canada’s largest producer of wind energy and is one of the country’s largest producers of renewable energy as a whole. The stock is listed in New York and Toronto.

Its history in renewable power generation goes back more than 100 years. In 2013, the company was spun off from TransAlta, which remains a major shareholder in the alternative power generation company.

The company has maintained or increased its dividend yearly since 2014 by an average growth rate of 2.5%. TransAlta Renewables owns or has economic interests in 26 wind facilities, 11 hydroelectric facilities, eight natural gas generation facilities, two solar facilities, one natural gas pipeline, and one battery storage project, representing an ownership interest of 2,965 megawatts of owned generating capacity.

TransAlta attempts to grow over the long term by focusing on renewables and gas-fired power generation. It thus benefits from the secular shift of most countries from fossil fuels to clean energy sources. Even better, this shift has greatly accelerated since the onset of the pandemic.

TransAlta has strong internal cash generation, allowing the company to invest strategically to build out its portfolio. These investments provide the company with a positive growth outlook.

Growth Prospects

TransAlta’s track record of growth has been quite strong. The company has consistently grown capacity over the past several years, thanks to its investments in wind, solar, and hydro assets. That said, higher interest rates and increasingly expensive shares issuance have taken a toll on the company’s Cash Available for Distribution and CAfD per share.

Source: Annual Report

Overall, given the market capitalization of $2.3 billion of the stock, it is evident that TransAlta has invested heavily in its growth projects.

TransAlta has also proved resilient throughout the coronavirus crisis. In contrast to most oil companies, which incurred hefty losses in 2020 due to a collapse in the global demand for oil products, TransAlta posted a benign 12% decrease in its funds from operations per share, from $1.13 in 2019 to $0.99 in 2020 (in USD, as with all figures shown in this article).

The company partly recovered in 2021, growing its funds from operations per share from $0.99 to $1.05. However, it is currently facing an unexpected headwind, as it has suffered a tower collapse at the Kent Hills 1 and 2 wind sites.

After careful inspection of the sites, the company determined that both sites need a full foundation replacement, which will be completed no earlier than the end of 2023. The replacement will cost $75-$100 million. On the bright side, recent progress in deleveraging should help ease interest expenses and boost CAfD.

Moreover, TransAlta has promising growth prospects in the long run, thanks to the secular growth of clean energy sources. Organic growth is a future catalyst, as well as acquisitions. In 2021, the company acquired several renewable energy plants. In 2022 no acquisitions took place due to elevated financing costs, but we expect them to resume taking place once the company deleverages further and frees some room for further debt issuances.

On the other hand, TransAlta has a somewhat volatile performance record, primarily due to the highly unpredictable depreciation of its assets as a result of its excessive investments.

In addition, the issuance of new shares, which are used to fund the excessive investments of the company, has provided a headwind to the growth of the bottom line. Given that shares are trading at a massive yield, we hope that TransAlta won’t issue further stock at this point, as it would be too risky and costly over the long run. As a result, we expect a 1% average annual growth of funds from operations per share over the next five years.

Dividend Analysis

TransAlta Renewables’ dividend is obviously a sizable draw for investors, given that the yield is so high. In addition, since this is not necessarily a growth company, total returns will be highly reliant upon the dividend in the coming years.

The company’s dividend has grown at an annual compound rate of ~2.5% since the IPO in 2013 and, today, stands at $0.94 per share annually in Canadian dollars. In U.S. dollars, the annualized dividend payout is approximately $0.70 per share, representing an 8% dividend yield.

Note: As a Canadian stock, a 15% dividend tax will be imposed on US investors investing in the company outside of a retirement account. See our guide on Canadian taxes for US investors here.

While shares of TransAlta recovered during 2021 from the general marker sell-off caused by the COVID-19 pandemic in the previous year, they have once again declined to multi-year lows. This is likely due to investors questioning the company’s ability to grow in the current environment, as debt and share issuance would come at a huge cost.

Higher interest expenses could also compress the company’s CaFD and threaten the dividend if the company doesn’t deleverage fast enough. Still, we expect the company to maintain its payouts for now. In 2018, the payout ratio in terms of earnings was 71% or 82% using distributable cash. Using distributable cash, the payout ratio was also 66% in 2021 and 75% in 2022. For 2023, we expect a payout ratio of approximately 64%, expecting the recent deleveraging to aid the bottom line.

With this in mind, we see the payout as safe for the foreseeable future. There could even be room for continued dividend growth if the company’s future investments are accretive on a per-share basis.

Final Thoughts

TransAlta Renewables’ high dividend yield and monthly dividend payments are immediately appealing to income investors such as retirees. However, due diligence is required to ensure that such a high dividend yield is sustainable.

This analysis suggests that the company’s dividend is relatively safe, as measured by Cash Available for Distribution or Funds From Operation. Investors looking for a monthly dividend from the renewable energy industry could do well owning TransAlta Renewables, but we also highlight that the dividend should not be blindly trusted.

In the event that the company chooses to pursue costly financing to support its growth, it cannot be ruled out that a dividend reduction may be on the table.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more