Updated on April 30th, 2026 by Bob Ciura

There are a number of high-quality investment opportunities available in Canada for purchase by United States investors.

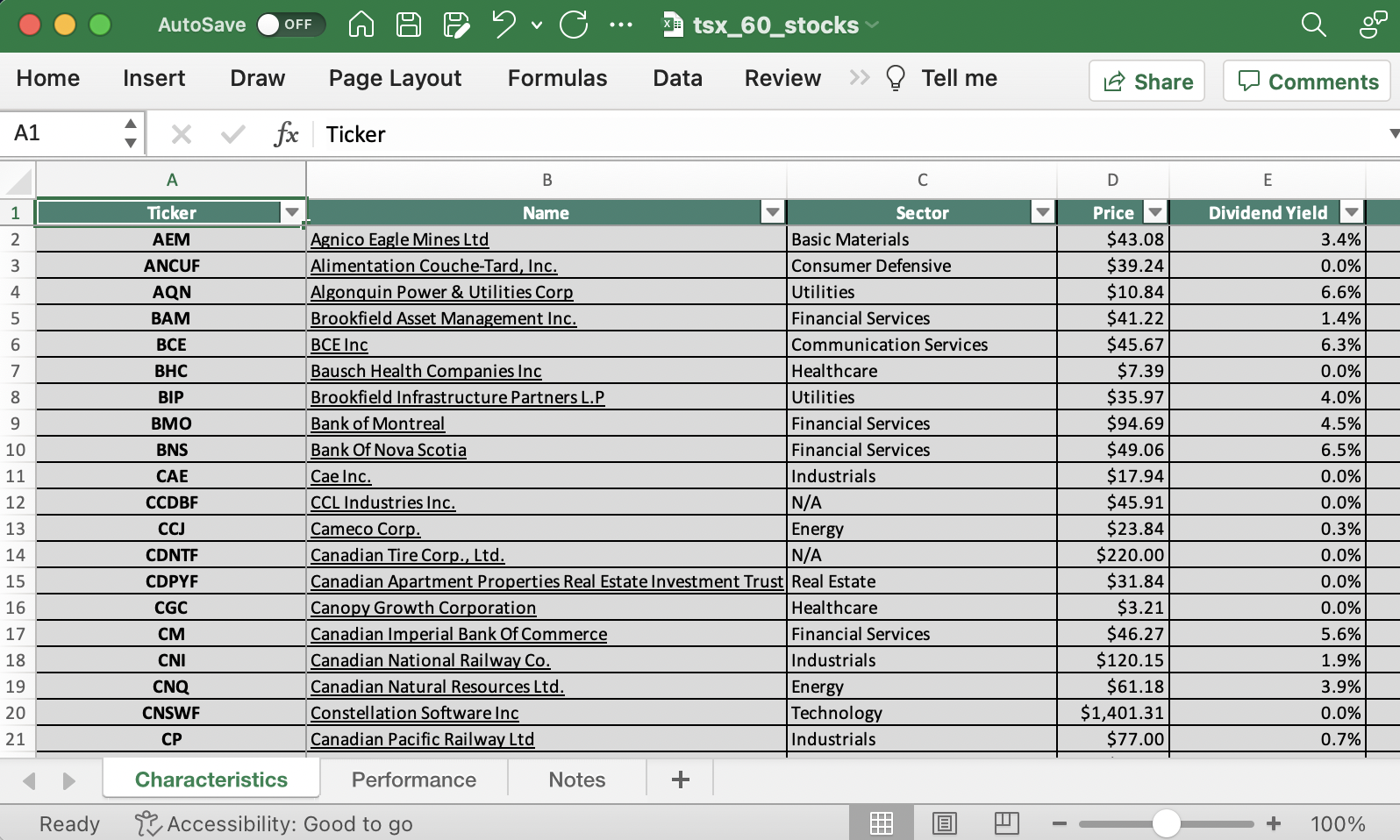

In fact, the TSX 60 – Canada’s stock market index of its 60 largest companies – is full of potential investment opportunities.

You can download your list of TSX 60 stocks using the link below:

One of the complicated factors of investing in Canadian stocks for U.S. residents is the tax implications.

Are Canadian stocks taxed just like their United States counterparts, or are there significant differences?

Do taxes need to be paid to both the IRS and the CRA (the Canadian tax authority), or just the IRS?

This guide will tell you exactly what the tax implications of investing in Canadian securities are before discussing the most tax-efficient way to buy these stocks and directing you to other investing resources for further research.

Table of Contents

You can jump to a particular component of this guide using the links below:

- Capital Gains Tax Implications for Canadian Stocks

- Dividend Tax Implications for Canadian Stocks & The Dividend Tax Treaty

- Owning Dividend Stocks in Retirement Accounts

- Where the Canadian Stock Market Shines

- Final Thoughts & Other Investing Resources

Capital Gains Tax Implications for Canadian Stocks

Capital gains taxes are the most simple components of investing in Canadian stocks. There are two cases that need to be considered.

The first is when you’re investing in Canadian companies that are cross-listed on both the Toronto Stock Exchange and the New York Stock Exchange (or another U.S. securities exchange). In this case, your best decision is to purchase the USD-denominated shares of Canadian stocks.

In this case, calculating and paying the capital gains tax that you pay on your investments is exactly the same as for “normal” United States stocks.

The second case to consider is when you’re investing in companies that trade exclusively on the Toronto Stock Exchange. In other words, this case covers stocks that trade in Canada but not on any United States exchange.

In order to buy these stocks, you’ll be required to convert some money over to Canadian dollars to purchase these investments.

The capital gains on which you’ll pay tax will require some manual calculations because they will be the difference between your cost basis and your sales price – both measured in US Dollars.

The cost basis of your investment, as measured in US Dollars, will be based on your Canadian Dollar purchase price and the prevailing exchange rates at the time of the investment.

Similarly, your sale price (measured in US Dollars) will be determined by multiplying your Canadian Dollar purchase price by the prevailing exchange rate at the time of sale.

Once you understand how to calculate the capital gains on which you’ll be required to pay tax on, the calculation of the capital gains tax is the same as for U.S.-domiciled securities.

There are two different rates for capital gains, depending on your holding period:

- Short-term capital gains are defined as capital gains on investments held for 1 year or less and are taxed at your marginal tax rate.

- Long-term capital gains are defined as capital gains on investments held for more than 1 year and are taxed at 15% (except for investors that are in the highest tax bracket, who pay a long-term capital gains tax rate of 20% – still significantly lower than the equivalent short-term capital gains tax rate).

Although this may seem complex, capital gains taxes are actually the most simple tax component of investing in Canadian stocks.

The next section discusses the tax treatment of Canadian dividends before later describing the most tax-efficient way for investors to purchase these stocks.

Dividend Tax Implications for Canadian Stocks & The Dividend Tax Treaty

Dividend taxes are where owning Canadian securities becomes more complicated from a tax perspective.

The reason for this is two-fold.

First, the Canadian government actually claims some tax on dividends paid to United States residents (and residents of all other non-Canadian countries).

More specifically, the Canadian tax authority, which is called the Canada Revenue Agency, generally withholds 30% of all dividends paid to out-of-country investors.

Fortunately, this 30% is reduced to 15% thanks to a tax treaty shared by Canada and the United States. This also comes with additional complicating factors which are explained in Publication 597 from the IRS:

“Dividends (Article X). For Canadian source dividends received by U.S. residents, the Canadian income tax generally may not be more than 15%.

A 5% rate applies to intercorporate dividends paid from a subsidiary to a parent corporation owning at least 10% of the subsidiary’s voting stock. However, a 10% rate applies if the payer of the dividend is a nonresident-owned Canadian investment corporation.

These rates do not apply if the owner of the dividends carries on, or has carried on, a business in Canada through a permanent establishment and the holding on which the income is paid is effectively connected with that permanent establishment.”

For all practical purposes, the only actionable knowledge that you need to know about the withholding rates on Canadian dividends is that the Canada Revenue Agency withholds 15% of every dividend paid to you from a Canadian corporation. Canada has its own form that can be submitted to request a refund of withholding tax.

The second reason why Canadian dividends are complicated from a tax perspective is their treatment by the IRS. As most readers know, quarterly dividend income generated by equity investments is taxable on your U.S. tax return.

What makes this complicated is that U.S. investors may be eligible to claim a credit or deduction against your local taxes with respect to the non-resident withholding taxes.

While this tax credit is beneficial from a financial standpoint, it adds an additional layer of complexity when investing in Canadian stocks.

For this reason, we recommend working with a tax professional to ensure that you are appropriately minimizing the taxes incurred by your investment portfolio.

Many of these tax headaches can be avoided by investing in Canadian dividend stocks through retirement accounts, which is the subject of the next section of this tax guide.

Note: Canadian REITs may still have taxes deducted in a retirement account.

Owning Dividend Stocks in Retirement Accounts

If you have the contribution room available, owning Canadian stocks in U.S. retirement accounts (like a 401(k)) is always your best decision.

There are two reasons for this.

First of all, the 15% withholding tax that is normally imposed by the Canada Revenue Agency is waived when Canadian securities are held within U.S. retirement accounts. This is an important component of the U.S.-Canada tax treaty that was referenced earlier in this tax guide.

The second reason why owning Canadian stocks in retirement accounts is the best decision is not actually unique to Canadian investments, but its worth mentioning nonetheless.

The remainder of the “normal” taxes that you’d pay on these Canadian stocks held in your retirement accounts will be waived as well, including both the capital gains tax and dividend tax paid to the IRS.

This means that holding Canadian stocks in United States retirement accounts has no additional tax burden compared to owning domestic stocks. In other words, owning Canadian stocks in a U.S. retirement account is the same as holding U.S. securities in the same investment account.

Note from Ben Reynolds: A reader recently had this to say regarding withholding tax: “From a practical perspective, those taxes are actually often withheld regardless of the treaty or law involved. This has happened to me at two different brokerages, Etrade and Schwab. In both cases, the stock was traded OTC. Never have I had a problem with an ADR, and that’s at Fidelity, Etrade, and Schwab, but with OTC Canadian stocks, you can count on 15% withholding on dividends. In my efforts to get to the bottom of this, I was able to talk to a trader at Schwab Global, who told me the issue was with the vendor that Schwab uses in Canada, who is the one who actually holds the shares. They withhold the tax, and Schwab has attempted to get them to stop that, but has been unsuccessful.”

Schwab has recently switched to a new vendor for this, so going forward, there should be no Canadian tax withheld on Canadian stocks (both ADRs and foreign ordinaries) when held in an IRA in the U.S. that has an address that’s not a PO box.

To get the 0% tax rate for Canadian stocks held in a 401(k), however, investors would first need to submit form NR301 to reduce the tax rate from 25% to 15%, and then file a form with the Canadian Revenue Authority.

You now have a solid, fundamental understanding of the tax implications of owning Canadian stocks as a U.S. investor. To summarize:

- Capital gains taxes are very similar to those incurred when buying United States-domiciled stocks

- The Canadian government imposes a 15% withholding tax on dividends paid to out-of-country investors, which can be claimed as a tax credit with the IRS and is waived when Canadian stocks are held in US retirement accounts.

The remainder of this article will discuss a few highlight sectors of the Canadian stock market before closing by providing additional investing resources for your use.

Where the Canadian Stock Market Shines

There are two broad sectors in which the Canadian stock market shines in terms of having excellent investment opportunities.

The first is the financial services sector. The “Big 5” Canadian banks are some of the most stable stocks in the world and are often rated as the world’s most conservative financial institutions.

There are broad, fundamental reasons for this, which largely have to do with the government’s treatment of delinquent borrowers. In Canada, a borrower is legally required to repay a mortgage even if they leave the house.

Canadians also benefit from the Canada Mortgage and Housing Corporation (CMHC), which provides mortgage insurance to borrowers who are unable to meet certain minimum down payment requirements.

With all of this in mind, Canada’s Big 5 banks are excellent investment opportunities when they can be acquired at attractive prices. They are listed below:

- The Royal Bank of Canada (RY)

- The Toronto-Dominion Bank (TD)

- The Bank of Nova Scotia (BNS)

- The Bank of Montreal (BMO)

- The Canadian Imperial Bank of Commerce (CM)

The other Canadian stock market sector that stands out is the energy sector.

Canada is an oil-rich country that houses some of the world’s most dominant energy businesses, including:

- Suncor (SU)

- Canadian Natural Resources Limited (CNQ)

- Enbridge (ENB)

While fossil fuels are on the decline, we believe there is still upside in certain high-quality energy stocks as they transition from oil-first business models to more diversified systems that incorporate multiple forms of energy, including renewables.

Final Thoughts & Other Investing Resources

As this guide shows, the tax implications of investing in Canadian stocks for U.S. investors are not as onerous as they might seem.

With that said, Canada is not the only international stock market that investors should consider searching through for investment opportunities.

Alternatively, you may look through these indices and decide that international investing is not for you.

Fortunately, Sure Dividend maintains several databases of domestic stocks, which you can access below:

- The Complete List of Russell 2000 Stocks: if you’re looking to invest in smaller companies with more growth opportunities, the Russell 2000 Index is the place to look. It is the most widely-quoted benchmark for small-cap stocks in the United States.

Searching for stocks with certain dividend characteristics is another useful method for finding investment opportunities.

With that in mind, the following Sure Dividend databases are quite valuable:

- The Dividend Aristocrats List: S&P 500 Index stocks with 25+ years of consecutive dividend increases.

- The Dividend Kings List: stocks with 50+ years of consecutive dividend increases.

- The Complete List of Monthly Dividend Stocks

- The Complete List of High Dividend Stocks with 5%+ Dividend Yields

The last technique we’ll recommend for finding investment ideas is by looking into certain sectors of the stock market.

Sure Dividend maintains the following sector-specific stock market databases for your benefit:

- The Complete List of Energy Stocks

- The Complete List of Financial Stocks

- The Complete List of Utility Stocks

- The Complete List of Materials Stocks

- The Complete List of Technology Stocks

- The Complete List of Communication Services Stocks

- The Complete List of Consumer Discretionary Stocks

- The Complete List of Consumer Staples Stocks

- The Complete List of Healthcare Stocks

- The Complete List of Industrials Stocks