Updated on June 5th, 2026 by Bob Ciura

The largest Canadian bank stocks have proven over the past decade that they not only endure recessions, but that they can grow at high rates coming out of a recession as well.

Canadian bank stocks also pay higher dividends than many U.S. bank stocks, making them potentially more appealing for income investors.

Valuations have also remained quite low recently, boosting their respective total return profiles as a result.

In this article, we’ll take a look at the “Big 5” Canadian banks – Canadian Imperial Bank of Commerce (CM), Royal Bank of Canada (RY), The Bank of Nova Scotia (BNS), Bank of Montreal (BMO) and Toronto-Dominion Bank (TD) – and rank them in order of highest expected returns.

Note: Canada imposes a 15% dividend withholding tax on U.S. investors. In many cases, investing in Canadian stocks through a U.S. retirement account waives the dividend withholding tax from Canada, but check with your tax preparer or accountant for more on this issue.

The top 5 big banks in Canada are very shareholder-friendly, with attractive cash returns. With this in mind, we created a full list of financial stocks.

You can download the entire list of ~210 financial sector stocks (along with important financial metrics like dividend yields and price-to-earnings ratios) by clicking the link below:

More information can be found in the Sure Analysis Research Database, which ranks stocks based on their dividend yield, earnings-per-share growth potential, and changes in the valuation multiple.

The stocks are listed in order below, with #1 being the most attractive for investors today.

Read on to see which Canadian bank is ranked highest in our Sure Analysis Research Database.

Table Of Contents

You can use the following table of contents to instantly jump to a specific stock:

- Canadian Bank Stock #5: Toronto-Dominion Bank (TD)

- Canadian Bank Stock #4: Canadian Imperial Bank of Commerce (CM)

- Canadian Bank Stock #3: Bank of Montreal (BMO)

- Canadian Bank Stock #2: Royal Bank of Canada (RY)

- Canadian Bank Stock #1: Bank of Nova Scotia (BNS)

The top 5 Canadian bank stocks are ranked based on total expected returns over the next five years, from lowest to highest.

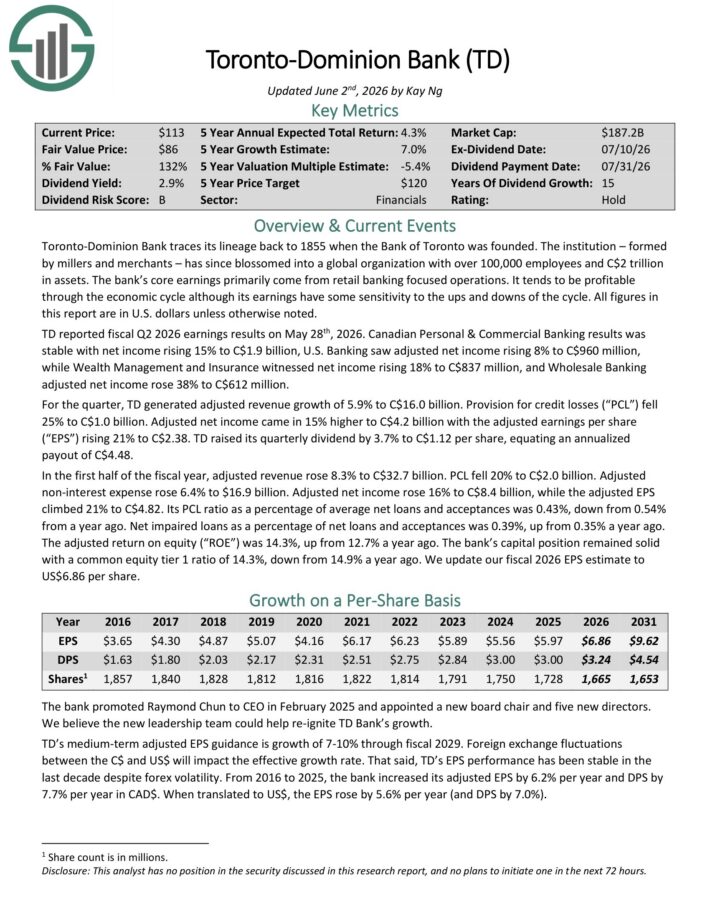

Canadian Bank Stock #5: Toronto-Dominion Bank (TD)

- 5-year expected annual returns: 4.2%

Toronto-Dominion Bank traces its lineage back to 1855 when the Bank of Toronto was founded. It is now a major bank with C$1.9 trillion in assets. The bank produces about C$14 billion in annual net income each year.

TD reported fiscal Q2 2026 earnings results on May 28th, 2026. Canadian Personal & Commercial Banking results was stable with net income rising 15% to C$1.9 billion, U.S. Banking saw adjusted net income rising 8% to C$960 million, while Wealth Management and Insurance witnessed net income rising 18% to C$837 million, and Wholesale Banking adjusted net income rose 38% to C$612 million.

For the quarter, TD generated adjusted revenue growth of 5.9% to C$16.0 billion. Provision for credit losses (“PCL”) fell 25% to C$1.0 billion.

Adjusted net income came in 15% higher to C$4.2 billion with the adjusted earnings per share rising 21% to C$2.38. TD raised its quarterly dividend by 3.7% to C$1.12 per share, equating an annualized payout of C$4.48.

Click here to download our most recent Sure Analysis report on TD (preview of page 1 of 3 shown below):

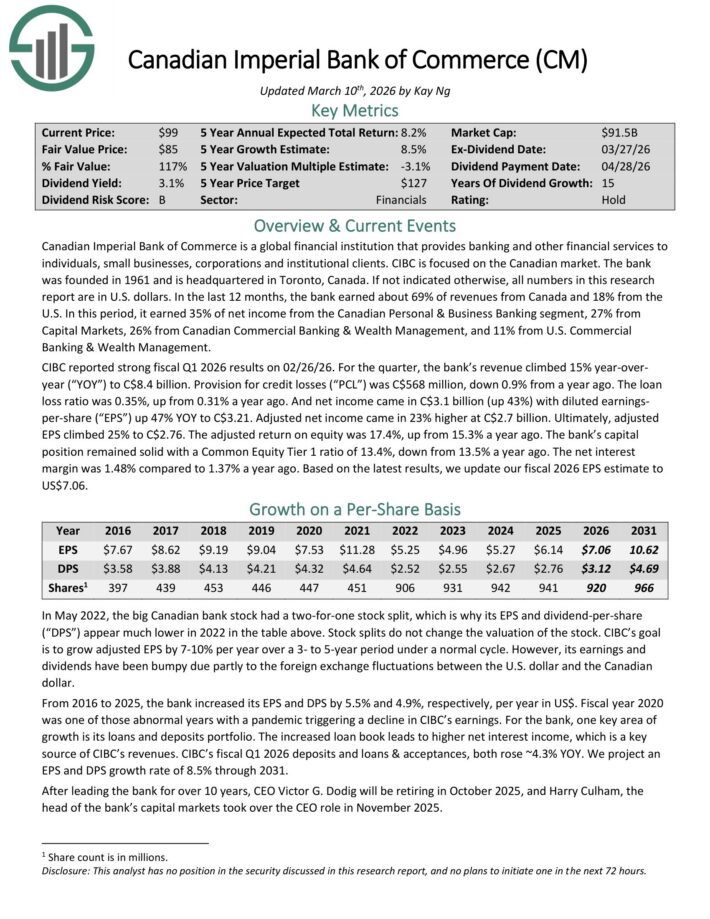

Canadian Bank Stock #4: Canadian Imperial Bank of Commerce (CM)

- 5-year expected returns: 6.3%

Canadian Imperial Bank of Commerce is a global financial institution that provides banking and other financial services to individuals, small businesses, corporations, and institutional clients. CIBC was founded in 1961 and is headquartered in Toronto, Canada.

In addition to trading on the New York Stock Exchange, CM stock trades on the Toronto Stock Exchange, as do the other stocks in this article.

You can download a full list of all TSX 60 stocks below:

CIBC reported strong fiscal Q1 2026 results on 02/26/26. For the quarter, the bank’s revenue climbed 15% year-over-year to C$8.4 billion.

Provision for credit losses was C$568 million, down 0.9% from a year ago. The loan loss ratio was 0.35%, up from 0.31% a year ago.

Net income came in C$3.1 billion (up 43%) with diluted earnings-per-share up 47% YOY to C$3.21. Adjusted net income came in 23% higher at C$2.7 billion. Adjusted EPS climbed 25% to C$2.76.

The adjusted return on equity was 17.4%, up from 15.3% a year ago. The bank’s capital position remained solid with a Common Equity Tier 1 ratio of 13.4%, down from 13.5% a year ago.

The net interest margin was 1.48% compared to 1.37% a year ago.

Click here to download our most recent Sure Analysis report on CM (preview of page 1 of 3 shown below):

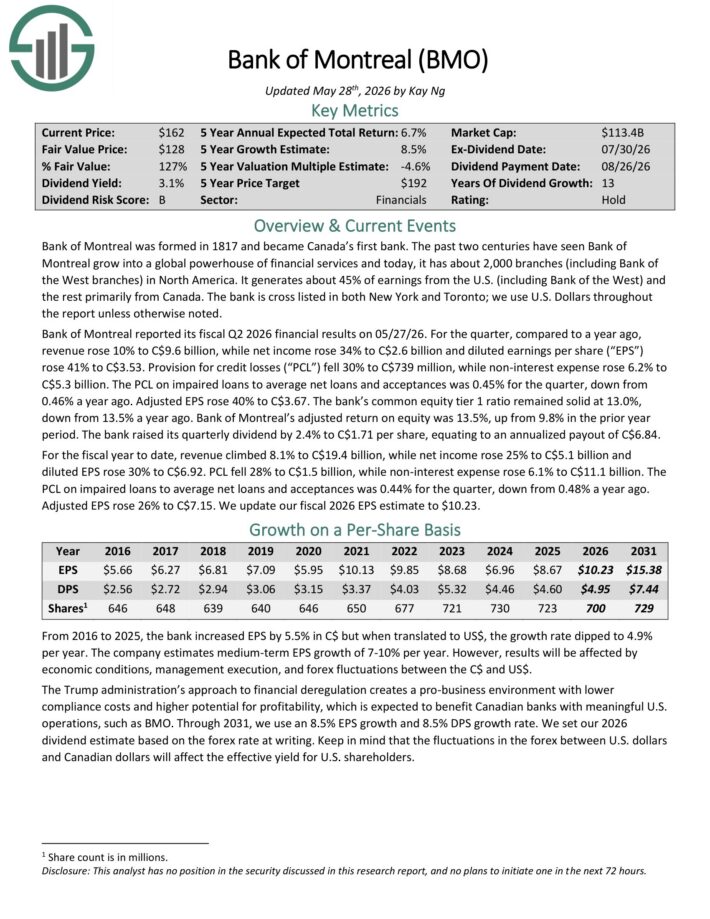

Canadian Bank Stock #3: Bank of Montreal (BMO)

- 5-year expected annual returns: 6.3%

Bank of Montreal was formed in 1817, becoming Canada’s first bank.

The past two centuries have seen Bank of Montreal grow into a global powerhouse of financial services and today, it has about 2,000 branches (including Bank of the West branches) in North America.

It generates about 45% of earnings from the U.S. (including Bank of the West) and the rest primarily from Canada. Bank of Montreal generates about 64% of its adjusted revenue from Canada and about 36% from the U.S.

Bank of Montreal reported its fiscal Q2 2026 financial results on 05/27/26. For the quarter, compared to a year ago, revenue rose 10% to C$9.6 billion, while net income rose 34% to C$2.6 billion and diluted earnings per share rose 41% to C$3.53.

Provision for credit losses (“PCL”) fell 30% to C$739 million, while non-interest expense rose 6.2% to C$5.3 billion. The PCL on impaired loans to average net loans and acceptances was 0.45% for the quarter, down from 0.46% a year ago. Adjusted EPS rose 40% to C$3.67.

The bank’s common equity tier 1 ratio remained solid at 13.0%, down from 13.5% a year ago. Bank of Montreal’s adjusted return on equity was 13.5%, up from 9.8% in the prior year period.

The bank raised its quarterly dividend by 2.4% to C$1.71 per share, equating to an annualized payout of C$6.84.

Click here to download our most recent Sure Analysis report on BMO (preview of page 1 of 3 shown below):

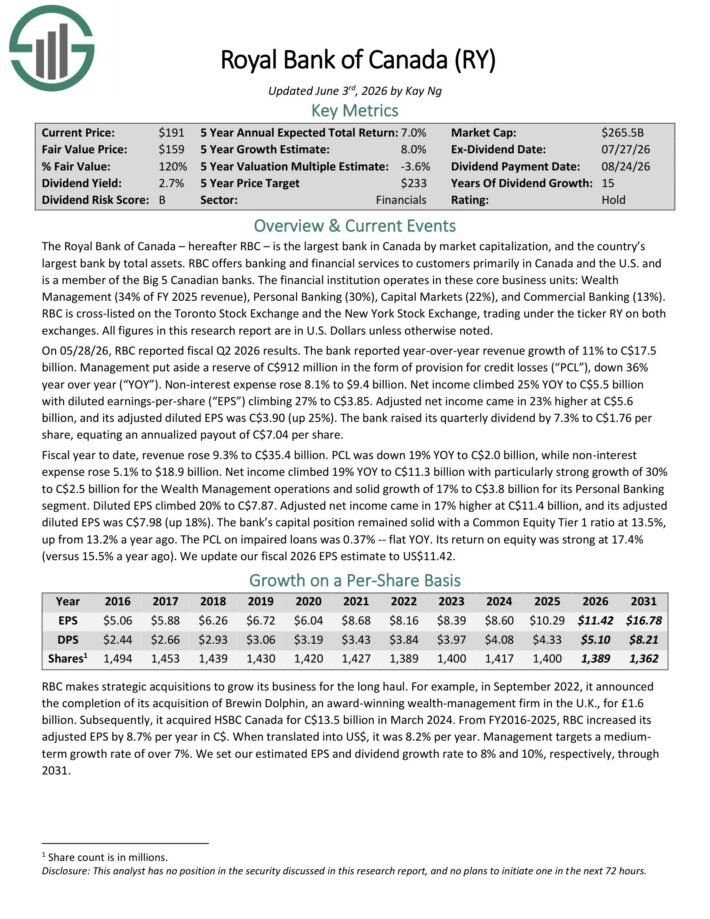

Canadian Bank Stock #2: Royal Bank of Canada (RY)

- 5-year expected returns: 6.6%

The Royal Bank of Canada is the largest bank in Canada by market capitalization, and by total assets. RBC offers banking and financial services to customers primarily in Canada and the U.S.

The financial institution operates in four core business units: Personal & Commercial Banking (39% of FY2023 revenue), Wealth Management (31%), Insurance (10%), and Capital Markets (20%). Its revenue mix is roughly 59% Canada, 25% the U.S., and 16% international.

On 05/28/26, RBC reported fiscal Q2 2026 results. The bank reported year-over-year revenue growth of 11% to C$17.5 billion.

Management put aside a reserve of C$912 million in the form of provision for credit losses, down 36% year over year. Non-interest expense rose 8.1% to $9.4 billion.

Net income climbed 25% YOY to C$5.5 billion with diluted earnings-per-share climbing 27% to C$3.85. Adjusted net income came in 23% higher at C$5.6 billion, and its adjusted diluted EPS was C$3.90 (up 25%).

The bank raised its quarterly dividend by 7.3% to C$1.76 per share, equating an annualized payout of C$7.04 per share.

Click here to download our most recent Sure Analysis report on RY (preview of page 1 of 3 shown below):

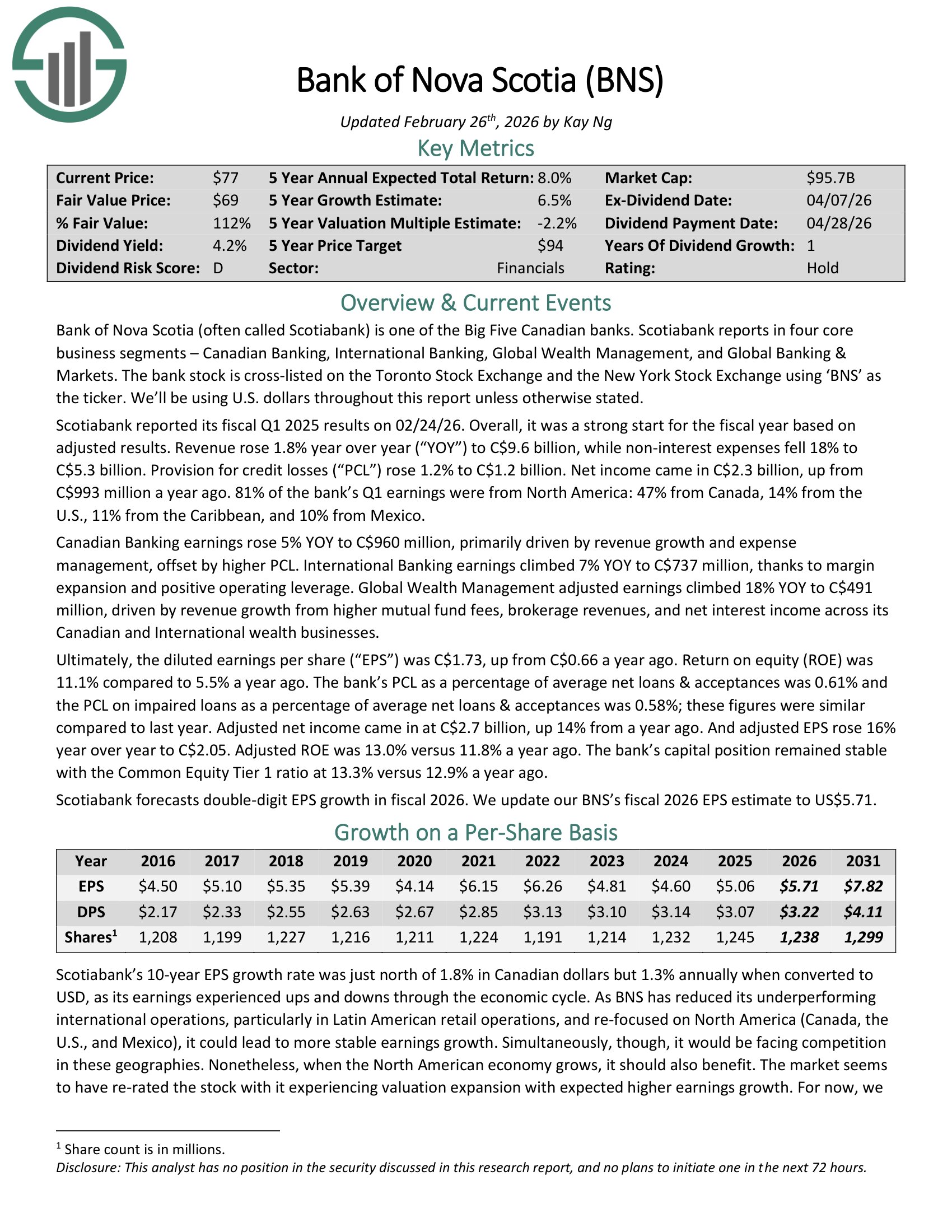

Canadian Bank Stock #1: Bank of Nova Scotia (BNS)

- 5-year expected annual returns: 7.7%

Bank of Nova Scotia (often called Scotiabank) is the fourth-largest financial institution in Canada behind the Royal Bank of Canada, the Toronto-Dominion Bank and Bank of Montreal.

Scotiabank reported its fiscal Q2 2025 results on 05/27/26. Overall, it was a strong continuation for the fiscal year based on adjusted results.

Revenue rose 8.2% year over year to C$9.8 billion, while non-interest expenses rose 2.0% to C$5.2 billion. Provision for credit losses (“PCL”) fell 13% to C$1.2 billion. Net income came in C$2.7 billion, up 28% YOY.

Adjusted earnings per share was C$2.02, up 33% YOY. Adjusted return on equity (“ROE”) was 13.2% versus 10.4% a year ago.

The bank’s capital position remained stable with the Common Equity Tier 1 ratio at 13.3% versus 13.2% a year ago. The bank raised its quarterly dividend by 3.6%.

Click here to download our most recent Sure Analysis report on BNS (preview of page 1 of 3 shown below):

Final Thoughts

Canadian bank stocks do not get nearly as much coverage as the major U.S. banks. However, income and value investors should pay attention to the big 5 Canadian bank stocks.

Royal Bank of Canada, TD Bank, Bank of Nova Scotia, Bank of Montreal, and Canadian Imperial Bank of Commerce are all profitable banks.

And, all 5 have reasonable valuations, with dividend yields that are well above the U.S. bank stocks.

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 4% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500. - The Best DRIP Stocks: The top 15 Dividend Champions with no-fee dividend reinvestment plans.

- The Complete List of Russell 2000 Stocks