Updated on February 24th, 2026 by Felix Martinez

When it comes to dividend investing, the Dividend Aristocrats are the “cream of the crop.” The Dividend Aristocrats are a group of S&P 500 stocks with 25+ consecutive years of dividend increases.

There are just 69 companies that have attained Dividend Aristocrat status.

As a result, it is not easy to join the Dividend Aristocrats list. With that in mind, we created a downloadable list of all 69 Dividend Aristocrats, along with key metrics such as dividend yields and price-to-earnings ratios.

You can download a free copy of the Dividend Aristocrats list by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

There are thousands of dividend stocks to choose from, but the Dividend Aristocrats are a unique group. The Dividend Aristocrats have profitable businesses and the ability to grow their profits over time.

This allows them to withstand recessions and continue increasing their dividends each year.

Franklin Resources (BEN) has increased its dividend for 46 consecutive years, and the stock has a high dividend yield of 4.9%.

Franklin Resources has endured a few tough years. Still, given the company’s track record of dividend growth and current yield, Franklin Resources is an attractive stock for income investors.

Business Overview

Franklin Resources is an investment management company. It was founded in 1947 in New York by Rupert H. Johnson Sr., who had previously managed a Wall Street brokerage firm. He named the company after Benjamin Franklin, the founding father who was viewed as a symbol for frugality, saving, and wise investments.

Today, Franklin Resources manages the Franklin and Templeton families of mutual funds.

The past few years have been difficult for Franklin Resources. Franklin Resources was slow to adapt to the changing environment in the asset management industry. The explosive growth in exchange-traded funds and indexing investing surprised traditional mutual funds.

ETFs have become very popular with investors, in large part due to their lower fees compared to traditional mutual funds. In response, the asset management industry has had to cut fees and commissions or risk losing client assets.

Growth Prospects

Despite the difficult operating environment, there are reasons to be optimistic about the company’s long-term growth. First, the U.S. is an aging population. Thousands of Baby Boomers are retiring every day. Combined with rising life expectancy, there is a great need for investment planning for those in or nearing retirement.

Franklin Resources is still investing to drive long-term earnings-per-share growth. In recent years, the company has funded two acquisitions and four investments, and has bought back stock fairly aggressively. In particular, the company has been strategically expanding into alternative investments to build an alternative growth vertical. Some of these include Legg Mason, Lexington Partners, and Alcentra.

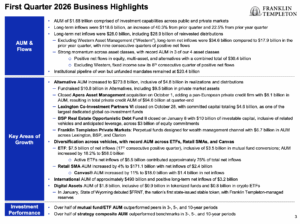

On January 30th, 2026, Franklin Resources reported strong quarterly earnings, with net income rising 117% year over year to $255.5 million and diluted EPS increasing to $0.46 from $0.21.

Operating margin improved significantly to 12.1%, compared with 3.6% in the prior quarter, reflecting cost discipline and normalization following acquisition-related expenses. Adjusted diluted EPS reached $0.70, up from $0.59 a year earlier, while dividends increased modestly to $0.33 per share.

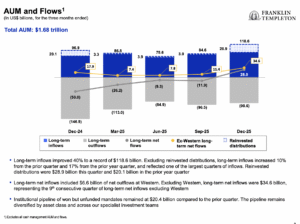

Assets under management (AUM) grew to $1.684 trillion, up from $1.576 trillion year over year, driven by $26.8 billion of total net inflows compared with $50.0 billion of outflows in the prior-year period.

Long-term net inflows totaled $28.0 billion, supported by strength in equity, alternatives, and multi-asset strategies. Alternative assets increased 4% sequentially to $273.8 billion, highlighting continued diversification toward higher-fee investment strategies.

Profitability also strengthened on an adjusted basis, with adjusted operating income of $437 million and an adjusted operating margin of 25.0%, demonstrating improving earnings quality as integration and restructuring costs decline.

The return to positive flows, expanding margins, and growing alternative asset exposure position Franklin Resources for gradual earnings stabilization as global market conditions and investor sentiment improve.

Investors can reasonably expect 6% annualized earnings-per-share growth over the next five years. Earnings-per-share growth will be driven by revenue growth, mainly due to rising AUM, as well as a boost from share repurchases.

Source: Investor presentation

Competitive Advantages & Recession Performance

Asset management is a highly competitive business, and there are not many competitive advantages in the financial services industry. The ability to retain clients depends largely on performance. If funds underperform their benchmarks, clients typically withdraw their funds.

However, Franklin Resources has a few advantages. The first, and perhaps most important, is brand recognition. Franklin Resources has been in operation for over 70 years. That indicates a certain developed expertise and some innate investment abilities. Franklin Resources also still has substantial assets under management, allowing the company to offer clients a wide range of investment opportunities and to generate economies of scale.

Counterbalancing these advantages, Franklin Resources’ most recent recession performance was poor:

- 2007 earnings-per-share of $2.37

- 2008 earnings-per-share of $2.24 (5.5% decline)

- 2009 earnings-per-share of $1.30 (42% decline)

- 2010 earnings-per-share of $2.12 (63% increase)

As you can see, earnings per share fell sharply in 2009, during the worst of the Great Recession. This should come as no surprise since investing is hardly recession-resistant. During recessions, stock markets typically decline. For asset managers, this can lower assets under management and fees. That said, Franklin Resources recovered quickly and saw earnings jump in 2010 and thereafter.

While the company entered another downturn in fiscal 2020 due to the coronavirus pandemic, it remained profitable, which allowed it to continue raising its dividend. Therefore, the company has a strong track record of dividend growth through recessions.

Source: Investor presentation

Valuation & Expected Returns

We expect Franklin Resources to earn $2.62 per share in fiscal year 2026. The stock has a price-to-earnings ratio of 10.3x. This is above our fair value P/E estimate of 9.5x. A compressing valuation multiple could reduce annualized total returns moving forward.

This valuation headwind will likely be offset by earnings-per-share growth and dividends. Franklin Resources has an attractive dividend yield of 6.2% and a secure dividend payout. A breakdown of potential returns is as follows:

- 6.0% earnings-per-share growth

- 4.9% dividend yield

- -1.8% valuation headwind

If Franklin Resources can return to growth, investors buying the stock now could see annualized total returns of 9.1% over the next five years.

Final Thoughts

Franklin Resources’ future growth depends on a strong economy, rising stock prices, and increasing assets under management. Its recent investments in alternative asset managers and aggressive stock buybacks appear to be a good start in that direction.

Franklin Resources could be attractive for income investors with a strong 4.9% dividend yield and a positive growth outlook.

However, given the expected annualized total returns, investors interested in the stock are encouraged to wait for a pullback or an improvement in fundamentals before buying Franklin Resources. As such, the stock is recommended for holding.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.