Updated on September 24th, 2025 by Bob Ciura

Apartment REITs have proved resilient to recessions thanks to the essential nature of their business. They also widely have high dividend yields well above the S&P 500 Index average.

And, with the Fed recently lowering rates, apartment REITs stand to benefit from a lower cost of capital.

You can download our full REIT list, along with important metrics such as dividend yields and market caps, by clicking on the link below:

As a result, apartment REITs are interesting candidates for income investors.

This article will discuss the prospects of the top 10 apartment REITs in our Sure Analysis Research Database.

The following 10 apartment REITs are listed by five-year expected annual returns, in order of lowest to highest:

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

- Apartment REITs #10: Essex Property Trust (ESS)

- Apartment REITs #9: Camden Property Trust (CPT)

- Apartment REITs #8: AvalonBay Communities (AVB)

- Apartment REITs #7: Equity Residential (EQR)

- Apartment REITs #6: Equity LifeStyle Properties (ELS)

- Apartment REITs #5: Mid-America Apartment Communities (MAA)

- Apartment REITs #4: American Homes 4 Rent (AMH)

- Apartment REITs #3: UMH Properties (UMH)

- Apartment REITs #2: UDR, Inc. (UDR)

- Apartment REITs #1: American Assets Trust (AAT)

- Final Thoughts

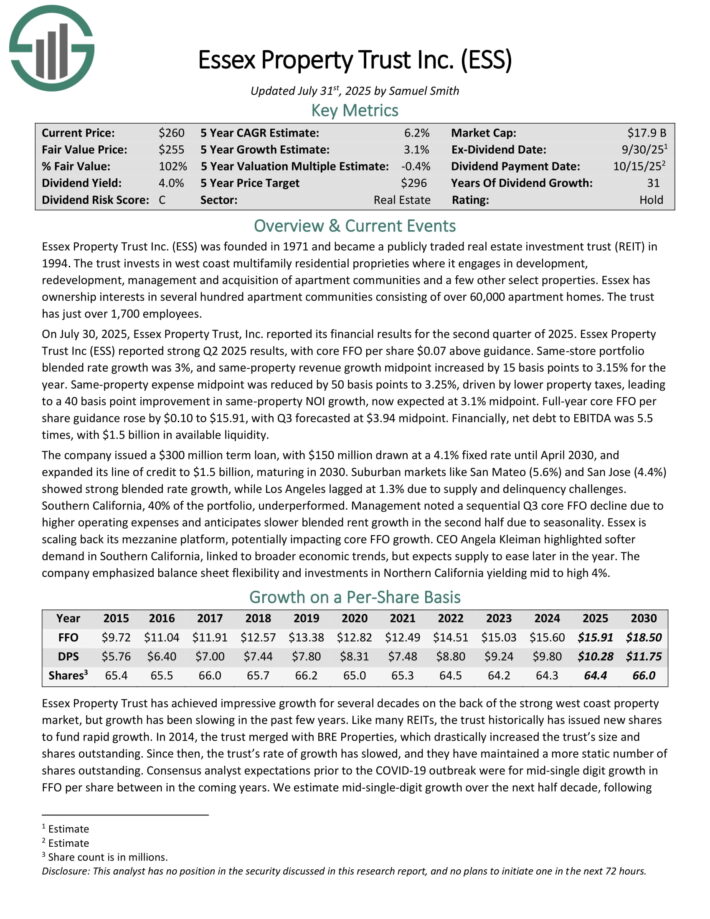

Apartment REITs #10: Essex Property Trust (ESS)

- Annual Expected Returns: 5.9%

Essex Property Trust was founded in 1971. The trust invests in West Coast multi-family residential proprieties where it engages in development, redevelopment, management and acquisition of apartment communities and a few other select properties.

Essex has ownership interests in several hundred apartment communities consisting of over 60,000 apartment homes. The trust has about 1,800 employees and produces approximately $1.6 billion in annual revenue.

Essex is concentrated on the West Coast of the U.S., including cities like Seattle and San Francisco.

On July 30, 2025, Essex Property Trust, Inc. reported its financial results for the second quarter of 2025. Essex Property Trust Inc (ESS) reported strong Q2 2025 results, with core FFO per share $0.07 above guidance.

Same-store portfolio blended rate growth was 3%, and same-property revenue growth midpoint increased by 15 basis points to 3.15% for the year.

Same-property expense midpoint was reduced by 50 basis points to 3.25%, driven by lower property taxes, leading to a 40 basis point improvement in same-property NOI growth, now expected at 3.1% midpoint. Full-year core FFO per share guidance rose by $0.10 to $15.91, with Q3 forecasted at $3.94 midpoint.

Financially, net debt to EBITDA was 5.5 times, with $1.5 billion in available liquidity.

Click here to download our most recent Sure Analysis report on ESS (preview of page 1 of 3 shown below):

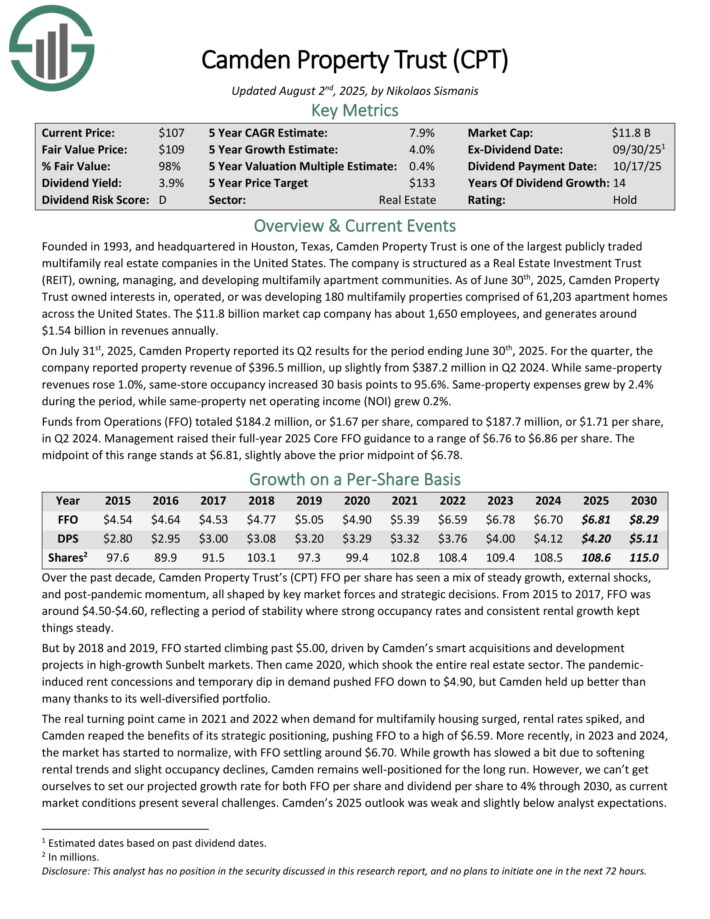

Apartment REITs #9: Camden Property Trust (CPT)

- Annual Expected Returns: 7.7%

Founded in 1993 and headquartered in Houston, Texas, Camden Property Trust is one of the largest publicly traded multifamily real estate companies in the U.S.

The REIT owns, manages and develops multifamily apartment communities. It currently owns 172 properties that contain over 58,000 apartments.

On July 31st, 2025, Camden Property reported its Q2 results. For the quarter, the company reported property revenue of $396.5 million, up slightly from $387.2 million in Q2 2024.

While same-property revenues rose 1.0%, same-store occupancy increased 30 basis points to 95.6%. Same-property expenses grew by 2.4% during the period, while same-property net operating income (NOI) grew 0.2%.

Funds from Operations (FFO) totaled $184.2 million, or $1.67 per share, compared to $187.7 million, or $1.71 per share, in Q2 2024.

Camden has a competitive advantage in its position as one of the largest multifamily REITs in the U.S. Its scale and expertise allow it to leverage its experience across a wide portfolio of properties and actively pursue developments.

The company’s FFO payout ratio has hovered in the 60% to 70% range for the last decade. CPT has increased its dividend for 14 consecutive years.

Click here to download our most recent Sure Analysis report on Camden Property Trust (CPT) (preview of page 1 of 3 shown below):

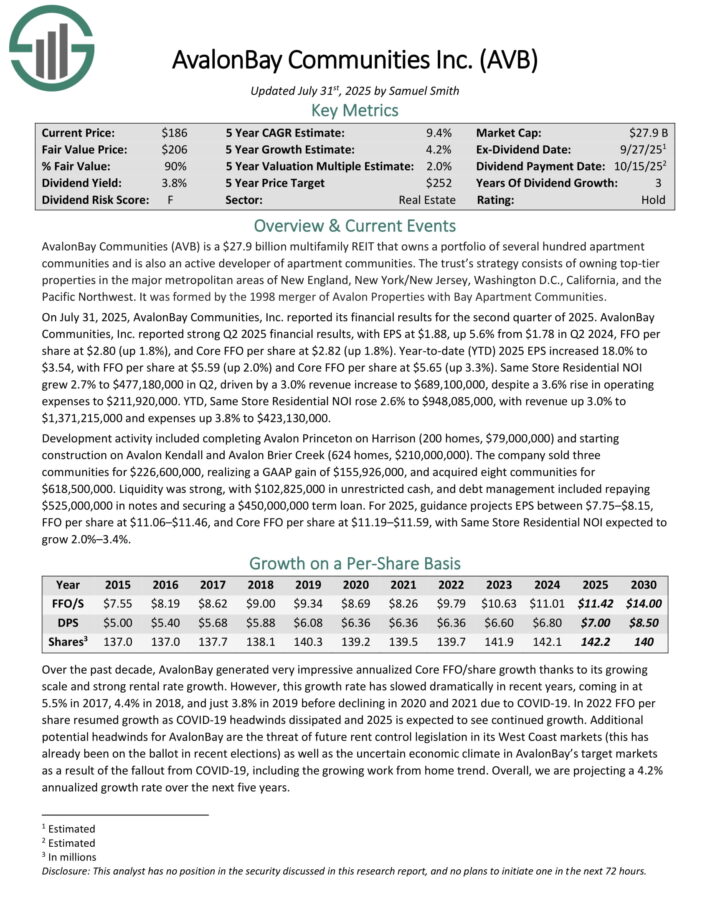

Apartment REITs #8: AvalonBay Communities (AVB)

- Annual Expected Returns: 9.1%

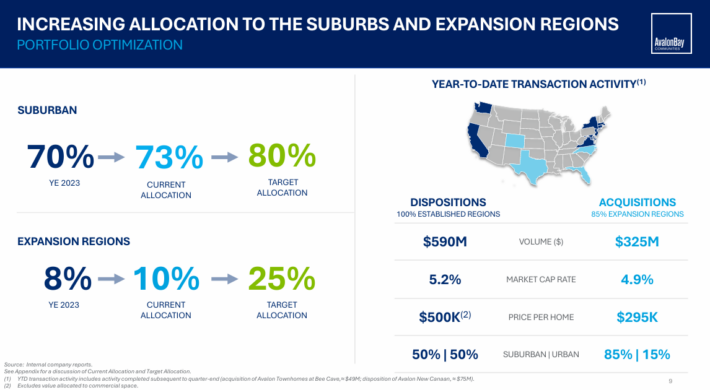

AvalonBay Communities is a multifamily REIT that owns a portfolio of several hundred apartment communities and is also an active developer of apartment communities.

The strategy of the REIT involves owning top-tier properties in the major metropolitan areas of New England, New York/New Jersey, Washington D.C., California, and the Pacific Northwest.

Source: Investor Presentation

On July 31, 2025, AvalonBay Communities, Inc. reported its financial results for the second quarter of 2025. AvalonBay reported EPS at $1.88, up 5.6% from $1.78 in Q2 2024, FFO per share at $2.80 (up 1.8%), and Core FFO per share at $2.82 (up 1.8%).

Year-to-date (YTD) 2025 EPS increased 18.0% to $3.54, with FFO per share at $5.59 (up 2.0%) and Core FFO per share at $5.65 (up 3.3%).

Same Store Residential NOI grew 2.7% to $477,180,000 in Q2, driven by a 3.0% revenue increase to $689,100,000, despite a 3.6% rise in operating expenses to $211,920,000.

Year-to-date, Same Store Residential NOI rose 2.6% to $948,085,000, with revenue up 3.0% to $1,371,215,000 and expenses up 3.8% to $423,130,000.

Click here to download our most recent Sure Analysis report on AvalonBay Communities (AVB) (preview of page 1 of 3 shown below):

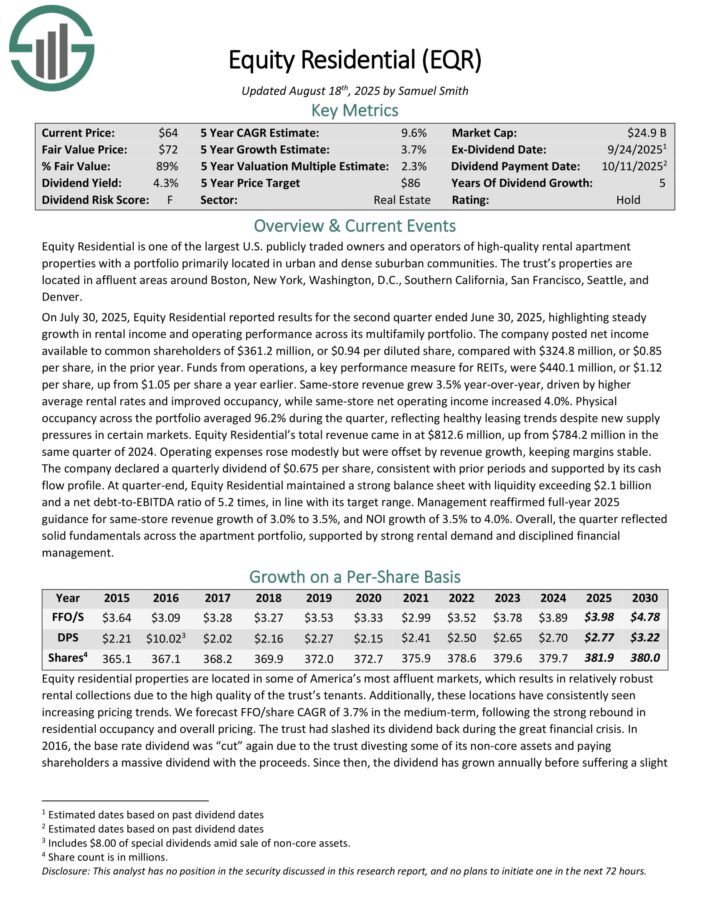

Apartment REITs #7: Equity Residential (EQR)

- Annual Expected Returns: 9.1%

Equity Residential is one of the largest U.S. publicly-traded owners and operators of high-quality rental apartment properties with a portfolio primarily located in urban and dense suburban communities.

The properties of the trust are located in affluent areas around Boston, New York, Washington, D.C., Southern California, San Francisco, Seattle, and Denver.

Equity Residential greatly benefits from the favorable characteristics of its target group. Affluent renters are highly educated, well employed and earn high incomes.

As a result, they pay approximately 20% of their incomes on rent and hence they are not burdened by their rent. Thanks to their strong earnings potential, the REIT can easily grow its rent rates year after year.

On July 30, 2025, Equity Residential reported results for the second quarter ended June 30, 2025. The company posted net income available to common shareholders of $361.2 million, or $0.94 per diluted share, compared with $324.8 million, or $0.85 per share, in the prior year.

Funds from operations, a key performance measure for REITs, were $440.1 million, or $1.12 per share, up from $1.05 per share a year earlier.

Same-store revenue grew 3.5% year-over-year, driven by higher average rental rates and improved occupancy, while same-store net operating income increased 4.0%.

Physical occupancy across the portfolio averaged 96.2% during the quarter, reflecting healthy leasing trends despite new supply pressures in certain markets. Total revenue came in at $812.6 million, up from $784.2 million in the same quarter of 2024.

Click here to download our most recent Sure Analysis report on Equity Residential (EQR) (preview of page 1 of 3 shown below):

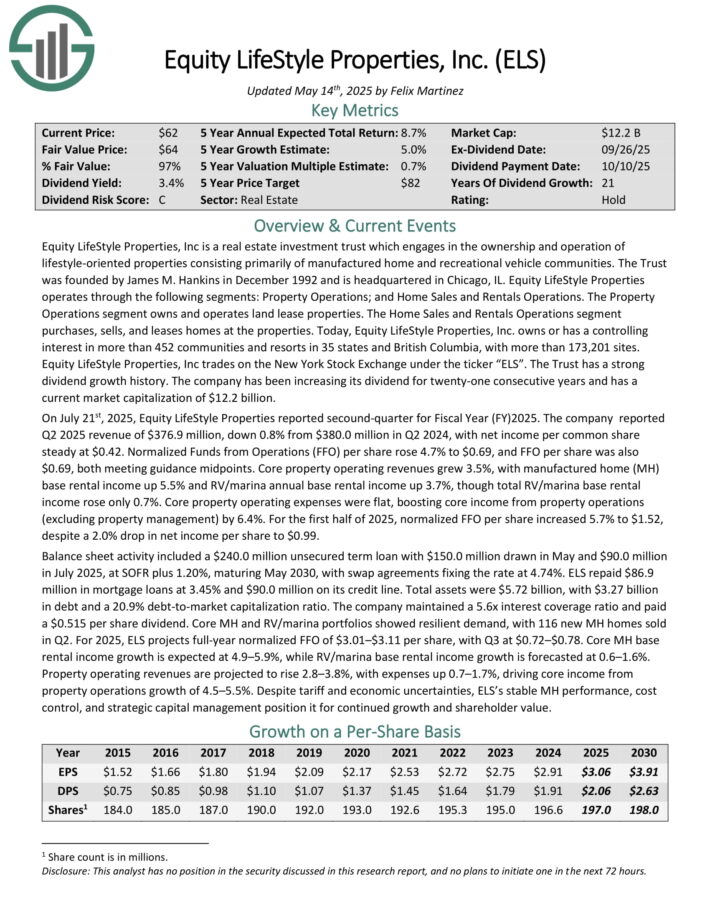

Apartment REITs #6: Equity LifeStyle Properties (ELS)

- Annual Expected Returns: 9.2%

Equity LifeStyle Properties, Inc is a real estate investment trust which engages in the ownership and operation of lifestyle-oriented properties consisting primarily of manufactured home and recreational vehicle communities.

Equity LifeStyle Properties operates through the following segments: Property Operations; and Home Sales and Rentals Operations.

The Property Operations segment owns and operates land lease properties. The Home Sales and Rentals Operations segment purchases, sells, and leases homes at the properties.

Today, Equity LifeStyle Properties, Inc. owns or has a controlling interest in more than 400 communities and resorts in 33 states and British Columbia, with more than 165,000 sites.

On July 21st, 2025, Equity LifeStyle Properties reported second-quarter for Fiscal Year (FY) 2025. The company reported Q2 2025 revenue of $376.9 million, down 0.8% from $380.0 million in Q2 2024, with net income per common share steady at $0.42.

Normalized Funds from Operations (FFO) per share rose 4.7% to $0.69, and FFO per share was also $0.69, both meeting guidance midpoints.

Core property operating revenues grew 3.5%, with manufactured home (MH) base rental income up 5.5% and RV/marina annual base rental income up 3.7%, though total RV/marina base rental income rose only 0.7%.

Click here to download our most recent Sure Analysis report on ELS (preview of page 1 of 3 shown below):

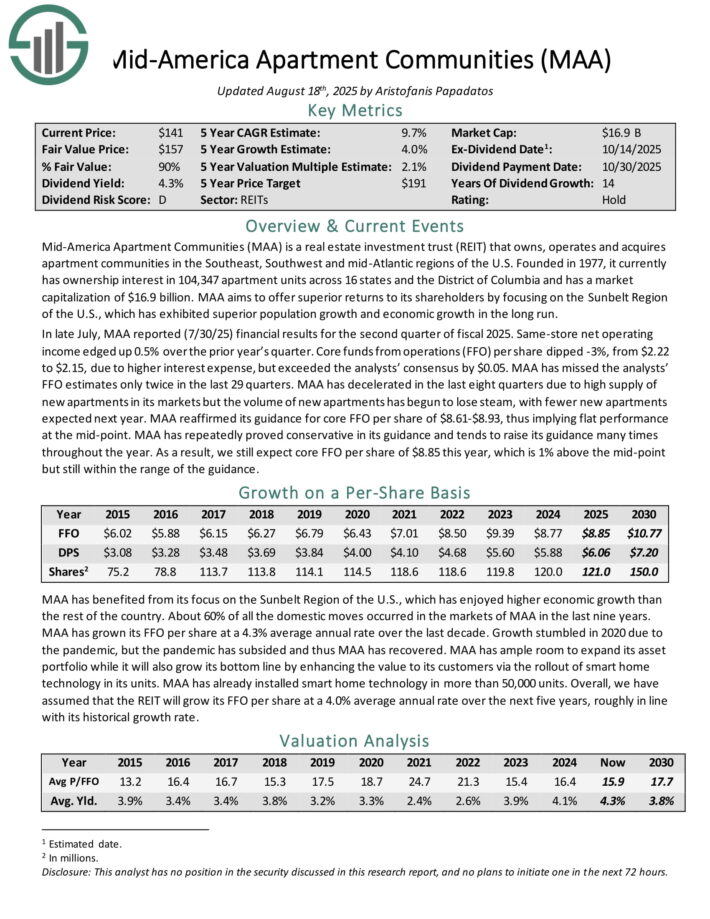

Apartment REITs #5: Mid-America Apartment Communities (MAA)

- Annual Expected Returns: 9.8%

Mid-America Apartment Communities is a REIT that owns, operates and acquires apartment communities in the Southeast, Southwest and mid-Atlantic regions of the U.S.

It currently has ownership interest in ~102,000 apartment units across 16 states and the District of Columbia.

MAA is focused on the Sunbelt Region of the U.S., which has exhibited superior population growth and economic growth in the long run.

In late July, MAA reported (7/30/25) financial results for the second quarter of fiscal 2025. Same-store net operating income edged up 0.5% over the prior year’s quarter. Core funds from operations (FFO) per share dipped -3%, from $2.22 to $2.15, due to higher interest expense, but exceeded the analysts’ consensus by $0.05.

MAA has missed the analysts’ FFO estimates only twice in the last 29 quarters. MAA has decelerated in the last eight quarters due to high supply of new apartments in its markets but the volume of new apartments has begun to lose steam, with fewer new apartments expected next year.

MAA reaffirmed its guidance for core FFO per share of $8.61-$8.93, thus implying flat performance at the mid-point.

Click here to download our most recent Sure Analysis report on Mid-America Apartment Communities (MAA) (preview of page 1 of 3 shown below):

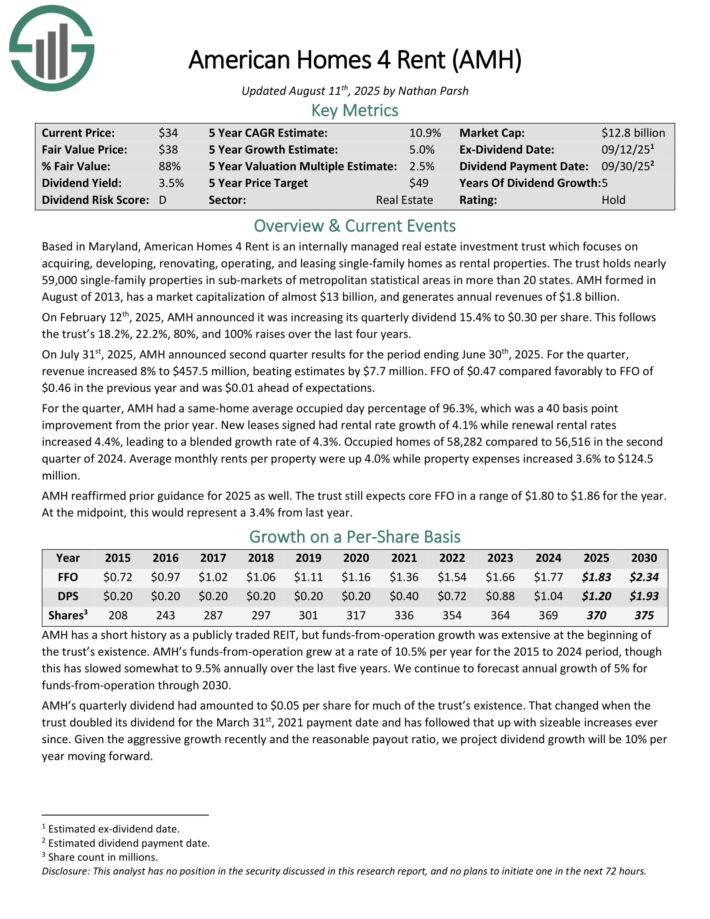

Apartment REITs #4: American Homes 4 Rent (AMH)

- Annual Expected Returns: 11.0%

Based in Maryland, American Homes 4 Rent is an internally managed REIT that focuses on acquiring, developing, renovating, operating and leasing single-family homes as rental properties. AMH was formed in 2013 and has a market capitalization of $14 billion.

The REIT holds nearly 58,000 single-family properties in more than 30 sub-markets of metropolitan statistical areas in 21 states.

On February 12th, 2025, AMH announced it was increasing its quarterly dividend 15.4% to $0.30 per share.

On July 31st, 2025, AMH announced second quarter results for the period ending June 30th, 2025. For the quarter, revenue increased 8% to $457.5 million, beating estimates by $7.7 million. FFO of $0.47 compared favorably to FFO of $0.46 in the previous year and was $0.01 ahead of expectations.

For the quarter, AMH had a same-home average occupied day percentage of 96.3%, which was a 40 basis point improvement from the prior year. New leases signed had rental rate growth of 4.1% while renewal rental rates increased 4.4%, leading to a blended growth rate of 4.3%.

Occupied homes of 58,282 compared to 56,516 in the second quarter of 2024. Average monthly rents per property were up 4.0% while property expenses increased 3.6% to $124.5 million.

Click here to download our most recent Sure Analysis report on American Homes 4 Rent (AMH) (preview of page 1 of 3 shown below):

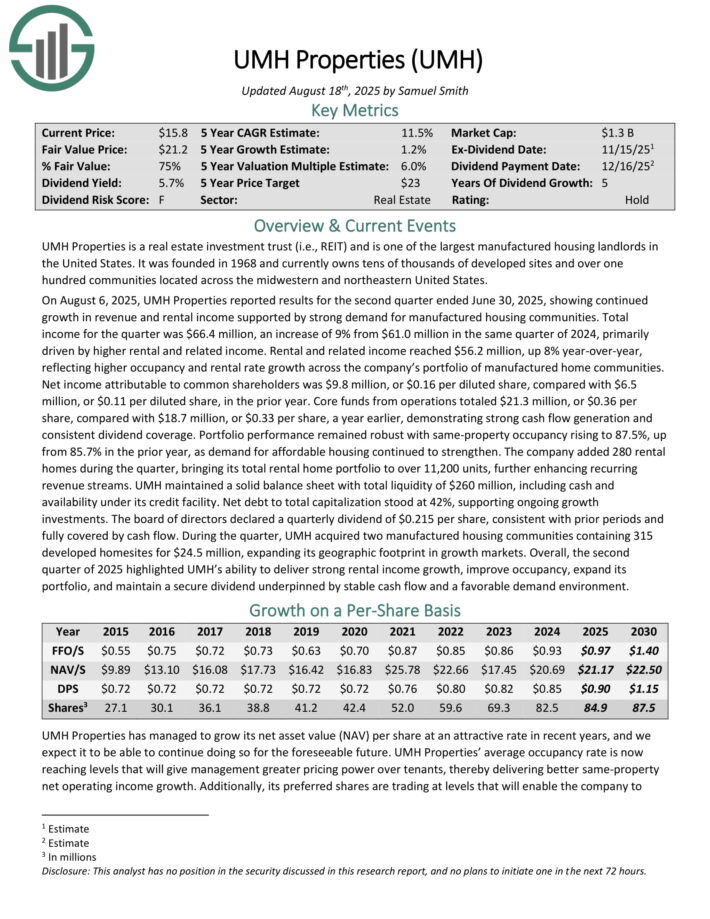

Apartment REITs #3: UMH Properties (UMH)

- Annual Expected Returns: 13.1%

UMH Properties is a REIT that is one of the largest manufactured housing landlords in the U.S. It was founded in 1968 and currently owns tens of thousands of developed sites and 135 communities located across the midwestern and northeastern U.S.

As manufactured homes are cheaper than conventional homes, UMH Properties has proved resilient to recessions.

On August 6, 2025, UMH Properties reported results for the second quarter ended June 30, 2025, showing continued growth in revenue and rental income supported by strong demand for manufactured housing communities.

Total income for the quarter was $66.4 million, an increase of 9% from $61.0 million in the same quarter of 2024, primarily driven by higher rental and related income.

Rental and related income reached $56.2 million, up 8% year-over-year, reflecting higher occupancy and rental rate growth across the company’s portfolio of manufactured home communities.

Net income attributable to common shareholders was $9.8 million, or $0.16 per diluted share, compared with $6.5 million, or $0.11 per diluted share, in the prior year.

Core funds from operations totaled $21.3 million, or $0.36 per share, compared with $18.7 million, or $0.33 per share, a year earlier, demonstrating strong cash flow generation and consistent dividend coverage.

Portfolio performance remained robust with same-property occupancy rising to 87.5%, up from 85.7% in the prior year, as demand for affordable housing continued to strengthen. The company added 280 rental homes during the quarter, bringing its total rental home portfolio to over 11,200 units.

Click here to download our most recent Sure Analysis report on UMH Properties (UMH) (preview of page 1 of 3 shown below):

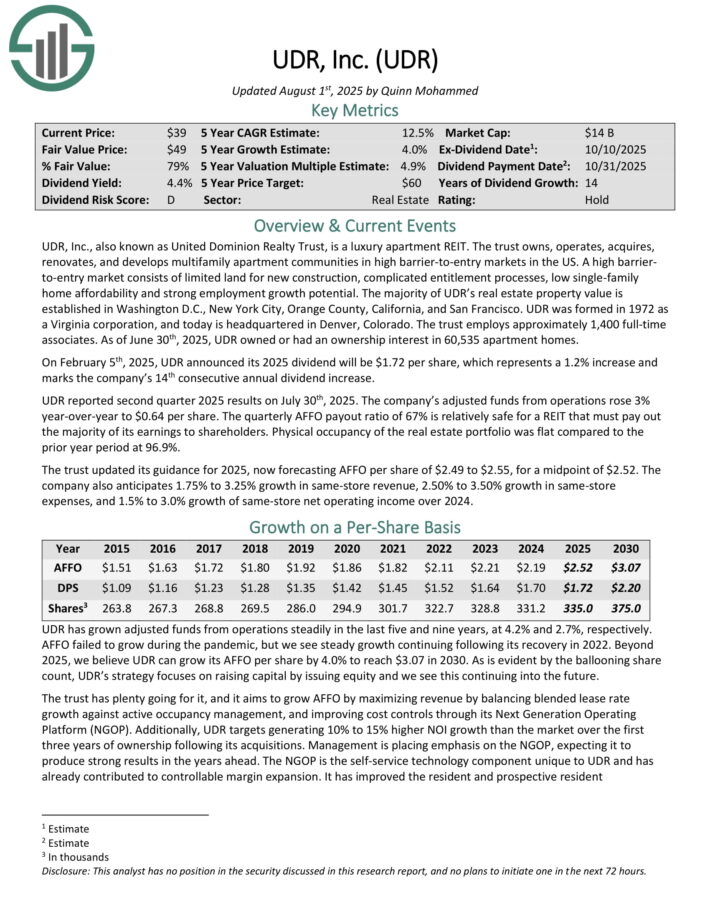

Apartment REITs #2: UDR, Inc. (UDR)

- Annual Expected Returns: 13.2%

UDR, also known as United Dominion Realty Trust, is a luxury apartment REIT. The trust owns, operates, acquires, renovates, and develops multifamily apartment communities in high barrier-to-entry markets in the U.S.

A high barrier-to-entry market consists of limited land for new construction, complicated entitlement processes, low single-family home affordability and strong employment growth potential.

The majority of UDR’s real estate property value is established in Washington D.C., New York City, Orange County, California, and San Francisco.

Source: Investor Presentation

On February 5th, 2025, UDR announced its 2025 dividend will be $1.72 per share, which represents a 1.2% increase and marks the company’s 14th consecutive annual dividend increase.

UDR reported second quarter 2025 results on July 30th, 2025. Adjusted funds from operations rose 3% year-over-year to $0.64 per share. The quarterly AFFO payout ratio of 67% is relatively safe for a REIT that must pay out the majority of its earnings to shareholders.

Physical occupancy of the real estate portfolio was flat compared to the prior year period at 96.9%. The trust updated its guidance for 2025, now forecasting AFFO per share of $2.49 to $2.55, for a midpoint of $2.52.

Click here to download our most recent Sure Analysis report on UDR (preview of page 1 of 3 shown below):

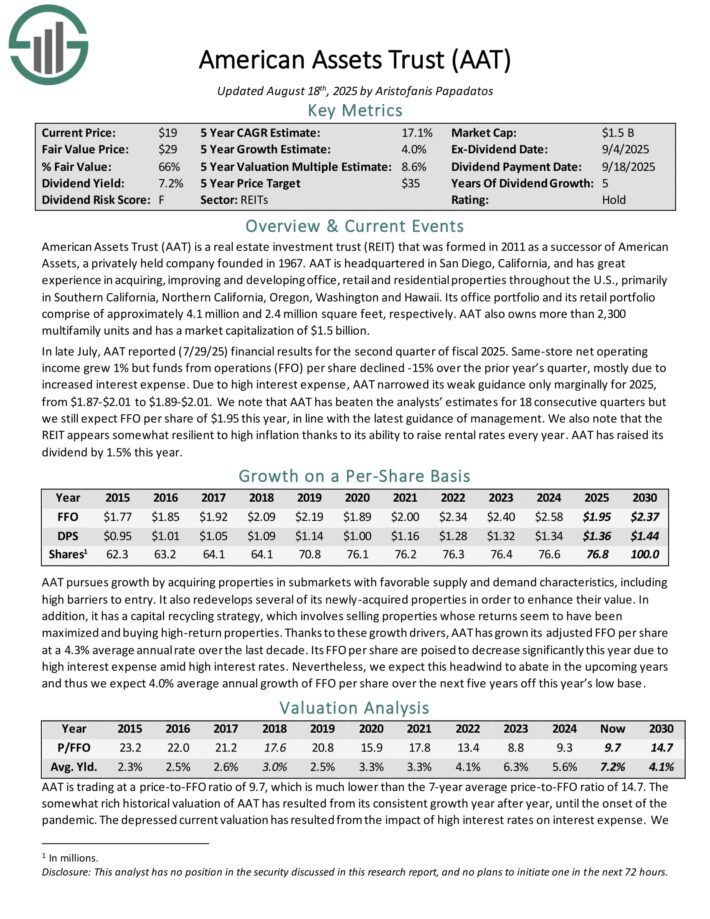

Apartment REITs #1: American Assets Trust (AAT)

- Annual Expected Returns: 15.2%

American Assets Trust is a REIT that was formed in 2011 as a successor of American Assets, a privately held company founded in 1967.

AAT has great experience in acquiring, improving and developing office, retail and residential properties throughout the U.S., primarily in Southern California, Northern California, Oregon, Washington and Hawaii.

Its office portfolio and its retail portfolio comprise of approximately 4.0 million and 3.1 million square feet, respectively. AAT also owns more than 2,000 multifamily units.

In late July, AAT reported (7/29/25) financial results for the second quarter of fiscal 2025. Same-store net operating income grew 1% but funds from operations (FFO) per share declined -15% over the prior year’s quarter, mostly due to increased interest expense.

Due to high interest expense, AAT narrowed its weak guidance only marginally for 2025, from $1.87-$2.01 to $1.89-$2.01.

Click here to download our most recent Sure Analysis report on American Assets Trust (AAT) (preview of page 1 of 3 shown below):

Final Thoughts

Many apartment REITs pass under the radar of the majority of investors due to their mundane business model.

However, some of these REITs have offered exceptionally high returns to their shareholders. In addition, apartment REITs have proved resilient to recessions, as the demand for housing remains strong even during rough economic periods.

The above 10 apartment REITs are interesting candidates for the portfolios of income-oriented investors, especially given the increasing risk of an upcoming recession.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

- 15 Highest-Yielding BDCs

- 15 Highest-Yielding MLPs

- 20 Highest Yielding Dividend Kings

- 20 High-Dividend Stocks Under $10

- 20 Undervalued High-Dividend Stocks

- 20 Highest Yielding Monthly Dividend Stocks

- 20 Highest-Yielding Small Cap Dividend Stocks

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 5%+ dividend yields

- Monthly Dividend Stocks: Individual securities that pay out every month

- MLPs: List of MLPs and more

- BDCs: List of BDCs and more