Updated on July 11th, 2025 by Nathan Parsh

Target Corporation (TGT) has increased its dividend for 57 consecutive years. As a result, Target has a position on the exclusive list of Dividend Kings.

The Dividend Kings have raised their dividend payouts for at least 50 consecutive years.

You can see all 55 Dividend Kings here.

You can download the full list of Dividend Kings, plus important financial metrics such as dividend yields and price-to-earnings ratios, by clicking on the link below:

To raise dividends for 50+ years in a row, a company must have durable competitive advantages and long-term growth potential. It must also possess a recession-resistant business and a management team that is committed to increasing the dividend each year.

Target possesses all of these qualities.

This article will discuss Target’s business model, growth catalysts, and expected returns.

Business Overview

Target was founded in 1902. Today, its business consists of nearly 2,000 big-box stores. These stores offer general merchandise and food, and also serve as distribution points for its e-commerce business. Target produced about $107 billion in total revenue in 2024.

Growth Prospects

Target’s growth has accelerated over the past few years. The 2020 coronavirus pandemic had only a slight impact on its growth, demonstrating the resilience of Target’s stores and e-commerce businesses.

Target has invested heavily in growing new sales channels, which have greatly paid off.

First, Target has invested heavily in e-commerce. The rise in e-commerce initially caught many retail companies flat-footed. Target has really revamped its online offerings and has seen incredible growth rates.

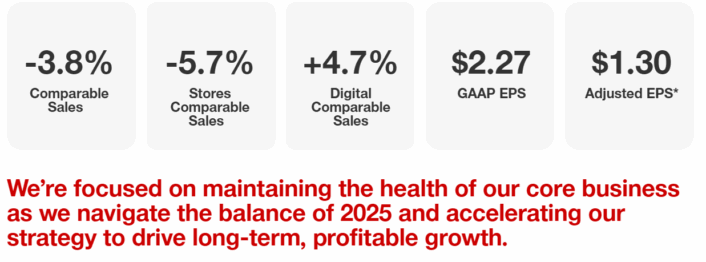

Target’s digital efforts are also working extremely nicely, as we saw again in Q1 results, though comparable sales have been weak.

Share repurchases will be an additional catalyst for earnings-per-share growth. The company has reduced its share count by about 3.6% per year in the last 10 years. The company has a massive share repurchase authorization considering that its current market capitalization is less than $48 billion.

Overall, we expect Target to grow earnings per share by 5% per year over the next five years.

Competitive Advantages & Recession Performance

Target operates in a complex industry – the highly competitive retail industry. For consumers, retail brands often take a back seat to price and convenience.

This is why Target has invested so heavily in store redevelopment. That has enabled the company to retain its brand strength, even in a fiercely competitive industry.

Most importantly, it has massive distribution and scale capabilities, which allow it to keep prices low.

In addition, Target operates in a defensive retail niche. Discount retail tends to hold relatively well during economic downturns, when consumers typically shift from higher-priced retailers.

Target’s earnings-per-share during the Great Recession are as follows:

- 2007 earnings-per-share of $3.33

- 2008 earnings-per-share of $2.86 (14% decline)

- 2009 earnings-per-share of $3.30 (15% increase)

- 2010 earnings-per-share of $3.88 (17% increase)

Target was remarkably resilient during the Great Recession. Although it suffered a 14% decline in 2008, it followed this with three consecutive years of double-digit earnings growth.

Target again performed very well in 2020, when the U.S. economy entered a recession due to the pandemic. And yet, Target continues to increase its dividend reliably each year, though at a lower rate over the past three years.

Valuation & Expected Returns

We expect Target to generate earnings per share of $7.40 this year. As a result, the stock is currently trading at a price-to-earnings ratio of 14.2. This is below our fair value estimate of 15.0 times earnings, meaning the stock appears undervalued right now.

If the P/E multiple grows from 14.2 to 15.0 over the next five years, then multiple expansion would add 1.1% to total returns over this period of time.

In addition, Target shares currently yield 4.4%. We expect 5% annual EPS growth over the next five years, so Target stock is expected to generate annual returns of 9.9% over the next five years.

Final Thoughts

After raising its dividend this year, Target eclipsed 57 years of annual dividend increases, cementing its position in the exclusive Dividend Kings list.

Due to its leading position in the retail industry, it has maintained so many years of dividend increases. It has also adapted well to the challenging climate for brick-and-mortar retailers, thanks to new store formats and considerable investments in e-commerce.

That said, recent results have been weak, and the dividend has grown by less than 2% each of the last three years. We believe that the company should continue to grow its dividend moving forward, something it has done through multiple economic cycles.

Given the total return potential and the nearly six decades of dividend growth, Target continues to earn a buy recommendation.

The following articles contain stocks with very long dividend or corporate histories, ripe for selection for dividend growth investors:

- The High Yield Dividend Aristocrats List is comprised of the 20 Dividend Aristocrats with the highest current yields.

- The Dividend Achievers List is comprised of ~400 stocks with 10+ years of consecutive dividend increases.

- The High Yield Dividend Kings List is comprised of the 20 Dividend Kings with the highest current yields.

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

- The Dividend Champions List: stocks that have increased their dividends for 25+ consecutive years.

Note: Not all Dividend Champions are Dividend Aristocrats because Dividend Aristocrats have additional requirements like being in The S&P 500.