Published on October 21st, 2025 by Felix Martinez

High-yield stocks pay out dividends that are significantly higher than the market average. For example, the S&P 500’s current yield is only ~1.2%.

High-yield stocks can be particularly beneficial in supplementing income after retirement.

LyondellBasell Industries N.V. (LYB) is part of our ‘High Dividend 50’ series, which covers the 50 highest-yielding stocks in the Sure Analysis Research Database.

We have created a spreadsheet of stocks (and closely related REITs, MLPs, etc.) with dividend yields of 4% or more.

You can download your free full list of all securities with 4%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

Next on our list of high-dividend stocks to review is LyondellBasell Industries N.V. (LYB).

Business Overview

LyondellBasell Industries, founded in 1955 in Germany, is one of the world’s largest plastics, chemicals, and refining companies. Headquartered in Houston, Texas (U.S.) and London (global), it operates in over 100 countries and is the world’s largest producer of polymer compounds.

The company provides materials that support food safety, clean water, fuel efficiency, and the performance of electronics and appliances. Its portfolio includes polyolefins, advanced polymers, intermediates, and refining, with a focus on innovation, sustainability, and solutions for the circular economy.

With a market capitalization of $16.6 billion, LyondellBasell generated $40.3 billion in sales last year. The company continues to pursue strategic growth, operational efficiency, and portfolio optimization to maintain its leadership in the global chemical industry.

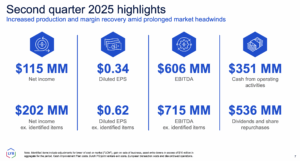

The company reported Q2 2025 net income of $115 million ($0.34 per share), or $202 million ($0.62 per share) excluding one-time items. Revenue was $7.66 billion, down 27% year-over-year but slightly above expectations, and EBITDA reached $606 million ($715 million excluding identified items). The company generated $351 million in operating cash and returned $536 million to shareholders through dividends and share repurchases.

Operationally, North American polyethylene volumes and margins improved after plant turnarounds, supported by strong demand in packaging, healthcare, construction, and infrastructure. European margins benefited from lower feedstock costs and seasonal demand, while Intermediate Chemicals saw higher styrene margins. Oxyfuels’ margins declined due to lower crude prices.

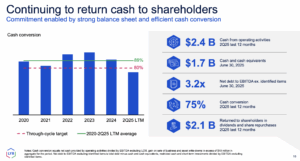

Strategically, LYB continued its three-pillar plan, announcing the sale of select European assets and deferring the Flex-2 project to preserve capital. Its Cash Improvement Plan targets $1.1 billion in savings through 2026. With $6.35 billion in liquidity, the company expects ongoing margin improvement in North America, steady European demand, and is carefully monitoring trade and operating risks.

Source: Investor Relations

Growth Prospects

From 2010 to 2018, LyondellBasell achieved impressive growth, with earnings per share increasing at an average annual rate of 20%. However, this performance is tempered by two factors: the company emerged from Chapter 11 bankruptcy in April 2010, starting from a low base, and earnings declined sharply in 2019 and 2020.

Going forward, LyondellBasell aims to drive growth through a combination of organic expansion and strategic acquisitions. The $2.25 billion purchase of A. Schulman, Inc. in 2018 doubled the company’s compounding business, providing exposure to new markets, including consumer products, appliances, and agriculture. Additionally, a three-pillar strategy and an active share buyback program support sustainable earnings growth.

After two strong years in 2021 and 2022, earnings have stabilized at lower levels. Assuming improving commodity market conditions, earnings are projected to grow at a 6% CAGR from an estimated base of $6.89 per share, with dividends expected to grow at a similar 6% CAGR through 2030. However, commodity price volatility makes precise forecasting challenging.

Source: Investor Relations

Competitive Advantages & Recession Performance

- 2009 earnings-per-share: $0.24

- 2010 earnings-per-share: $2.57

Dividend Analysis

LyondellBasell’s annual dividend is $5.48 per share. At its recent share price, the stock has a high yield of 12.0%.

Given the company’s earnings outlook for 2025, EPS is expected to be $2.72 per share. As a result, the company is expected to pay out roughly twice its EPS to shareholders in dividends.

The dividend appears to be on track to be cut this year or next.

Source: Investor Relations

Final Thoughts

LyondellBasell is a high-quality company with a solid financial position. While not fully recession-proof, it is in a stronger position than it was a decade ago. Although results remain below the pandemic-era peaks, performance is expected to improve as commodity markets stabilize.

We project a total annual return of 16.3%, driven by a 12% yield, 6% earnings growth, and potential valuation gains. The company is rated a hold due to a moderate dividend risk.

High-Yield Individual Security Research

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Super High Dividend REITs

- 5 Highest Yielding Royalty Trusts

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 5%+ dividend yields

- Monthly Dividend Stocks: Individual securities that pay out every month

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more