Updated on August 28th, 2025 by Bob Ciura

To invest in great businesses, you have to find them first. That’s where Warren Buffett comes in…

Berkshire Hathaway (BRK.B) has an equity investment portfolio worth approximately $258 billion.

Berkshire Hathaway’s portfolio is filled with quality stocks. You can ‘cheat’ from Warren Buffett stocks to find picks for your portfolio. That’s because Buffett (and other institutional investors) are required to periodically show their holdings in a 13F Filing.

You can see all of Warren Buffett’s stock holdings (along with relevant financial metrics like dividend yields and price-to-earnings ratios) by clicking on the link below:

This article analyzes Warren Buffett’s top 20 stocks based on information disclosed in the Q2 2025 13F filing.

Table of Contents

You can skip to a specific section with the table of contents below. Stocks are listed by percentage of the total portfolio, from highest to lowest.

- How To Use Warren Buffett Stocks To Find Investment Ideas

- Warren Buffett & Dividend Stocks

- #1: Apple, Inc. (AAPL)

- #2: American Express (AXP)

- #3: Bank of America (BAC)

- #4: The Coca-Cola Company (KO)

- #5: Chevron Corporation (CVX)

- #6: Moody’s Corporation (MCO)

- #7: Occidental Petroleum (OXY)

- #8: Kraft Heinz (KHC)

- #9: Chubb Limited (CB)

- #10: Kroger Co. (KR)

- #11: Visa Inc. (V)Citigroup (C)

- #12: Mastercard Inc. (MA)

- #13: Amazon, Inc. (AMZN)

- #14: Constellation Brands (STZ)

- #15: UnitedHealth Group (UNH)

- #16: Capital One Financial (COF)

- #17: Aon plc (AON)

- #18: Domino’s Pizza (DPZ)

- #19: Ally Financial (ALLY)

- #20: Pool Corporation (POOL)

How To Use Warren Buffett Stocks To Find Investment Ideas

Having a database of Warren Buffett stocks is more powerful when you have the ability to filter it based on important investing metrics.

That’s why this article’s Excel download is so useful…

It allows you to search Warren Buffett stocks to find dividend investment ideas that match your specific portfolio.

For those of you unfamiliar with Excel, this section will show you how to filter Warren Buffett stocks for two important investing metrics – price-to-earnings ratio and dividend yield.

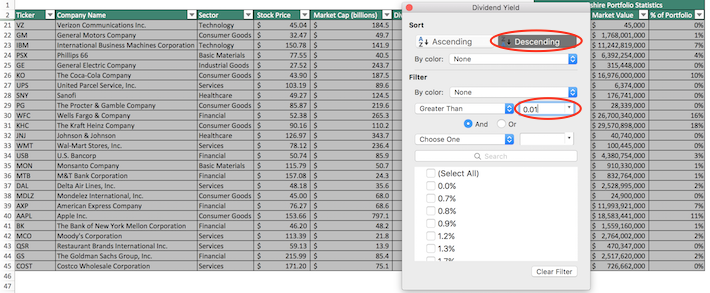

Step 1: Click on the filter icon in the column for dividend yield or price-to-earnings ratio.

Step 2: Filter each metric to find high-quality stocks. Two examples are provided below.

Example 1: To find stocks with dividend yields above 1% and list them in descending order, click the ‘Dividend Yield’ filter and do the following:

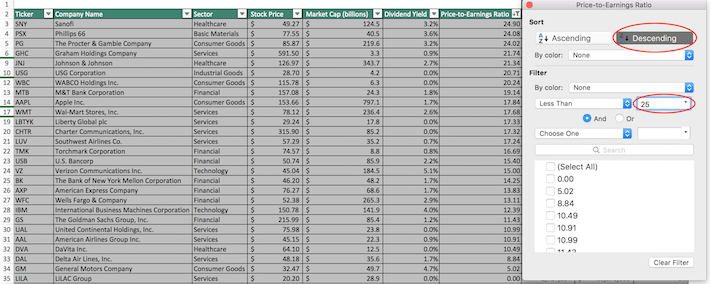

Example 2: To find stocks with price-to-earnings ratios below 25 and list them in descending order, click the ‘Price-to-Earnings Ratio’ filter and do the following:

Warren Buffett & Dividend Stocks

Buffett has grown his wealth by investing in and acquiring businesses with strong competitive advantages trading at fair or better prices.

Most investors know Warren Buffett looks for quality, but few know the degree to which he invests in dividend stocks:

- All of Warren Buffett’s top 10 stocks pay dividends

- His top 5 holdings have an average dividend yield of ~2.2% (and make up 70% of his portfolio)

- Many of his dividend stocks have paid rising dividends over decades

Warren Buffett prefers to invest in shareholder-friendly businesses with long track records of success.

Keep reading this article to see Warren Buffett’s 20 highest conviction stock selections analyzed. These are the 20 stocks with the highest value (most weight) in Berkshire Hathaway’s portfolio.

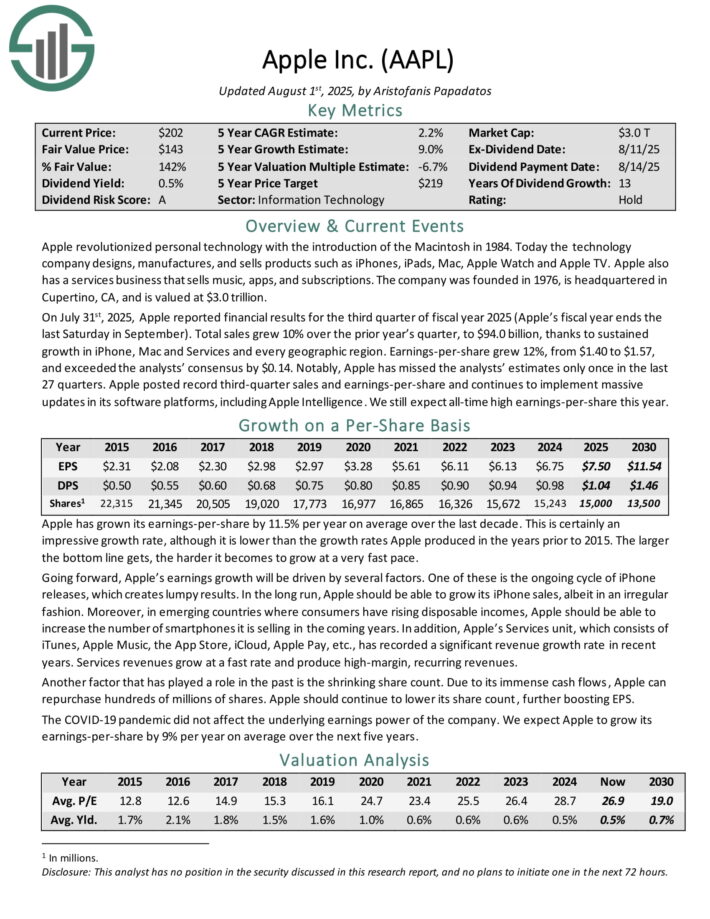

#1: Apple, Inc. (AAPL)

Dividend Yield: 0.4%

Percent of Warren Buffett’s Portfolio: 22.31%

Apple is Berkshire’s largest position by far, due in large part to Apple’s amazing rally over the past few years.

The technology company designs, manufactures and sells products such as iPhones, iPads, Mac, Apple Watch and Apple TV. Apple also has a services business that sells music, apps, and subscriptions.

Apple is also a top holding of other influential investors, such as Kevin O’Leary.

On July 31st, 2025, Apple reported financial results for the third quarter of fiscal year 2025. Total sales grew 10% over the prior year’s quarter, to $94.0 billion, thanks to sustained growth in iPhone, Mac and Services and every geographic region. Earnings-per-share grew 12%, from $1.40 to $1.57, and exceeded the analysts’ consensus by $0.14.

Notably, Apple has missed the analysts’ estimates only once in the last 27 quarters. Apple posted record third-quarter sales and earnings-per-share.

Going forward, Apple’s earnings growth will be driven by several factors. One of these is the ongoing cycle of iPhone releases, which creates lumpy results. In the long run, Apple should be able to grow its iPhone sales, albeit in an irregular fashion.

Moreover, in emerging countries where consumers have rising disposable incomes, Apple should be able to increase the number of smartphones it is selling in the coming years.

In addition, Apple’s Services unit, which consists of iTunes, Apple Music, the App Store, iCloud, Apple Pay, etc., has recorded a significant revenue growth rate in recent years. Services revenues grow at a fast rate and produce high-margin, recurring revenues.

Click here to download our most recent Sure Analysis report on AAPL (preview of page 1 of 3 shown below):

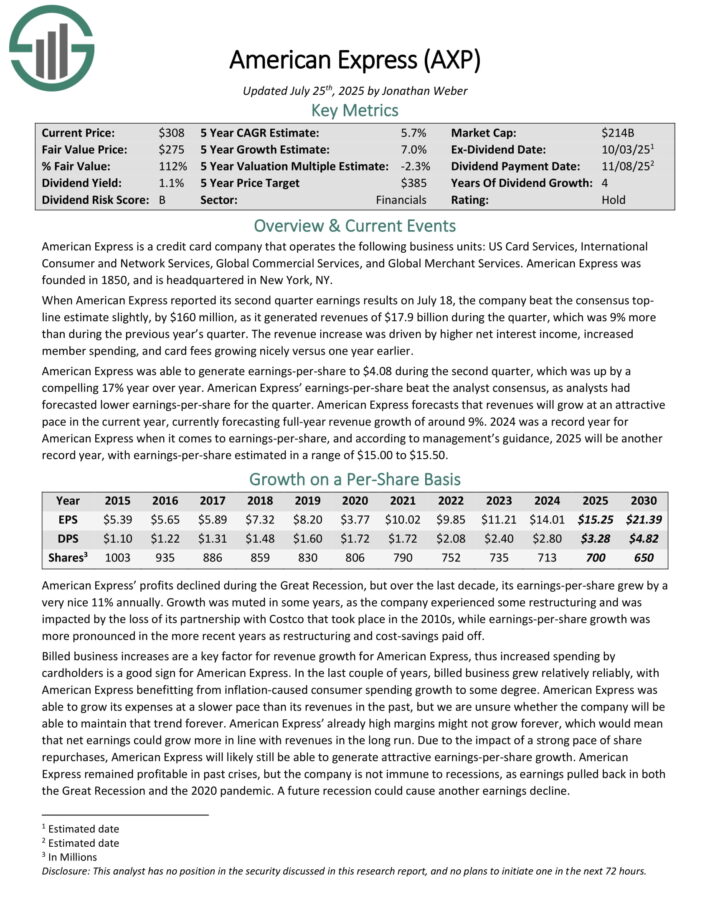

#2: American Express Company (AXP)

Dividend Yield: 1.0%

Percent of Warren Buffett’s Portfolio: 18.78%

American Express is one of Berkshire’s longest-held stocks. American Express is a credit card company that operates the following business units: US Card Services, International Consumer and Network Services, Global Commercial Services, and Global Merchant Services. American Express was founded in 1850.

When American Express reported its second quarter earnings results on July 18, the company beat the consensus topline estimate slightly, by $160 million, as it generated revenues of $17.9 billion during the quarter, which was 9% more than during the previous year’s quarter. The revenue increase was driven by higher net interest income, increased member spending, and card fees growing nicely versus one year earlier.

American Express was able to generate earnings-per-share to $4.08 during the second quarter, which was up by a compelling 17% year over year. American Express’ earnings-per-share beat the analyst consensus, as analysts had forecasted lower earnings-per-share for the quarter.

American Express forecasts that revenues will grow at an attractive pace in the current year, currently forecasting full-year revenue growth of around 9%. 2024 was a record year for American Express when it comes to earnings-per-share, and according to management’s guidance, 2025 will be another record year, with earnings-per-share estimated in a range of $15.00 to $15.50

Click here to download our most recent Sure Analysis report on American Express (preview of page 1 of 3 shown below):

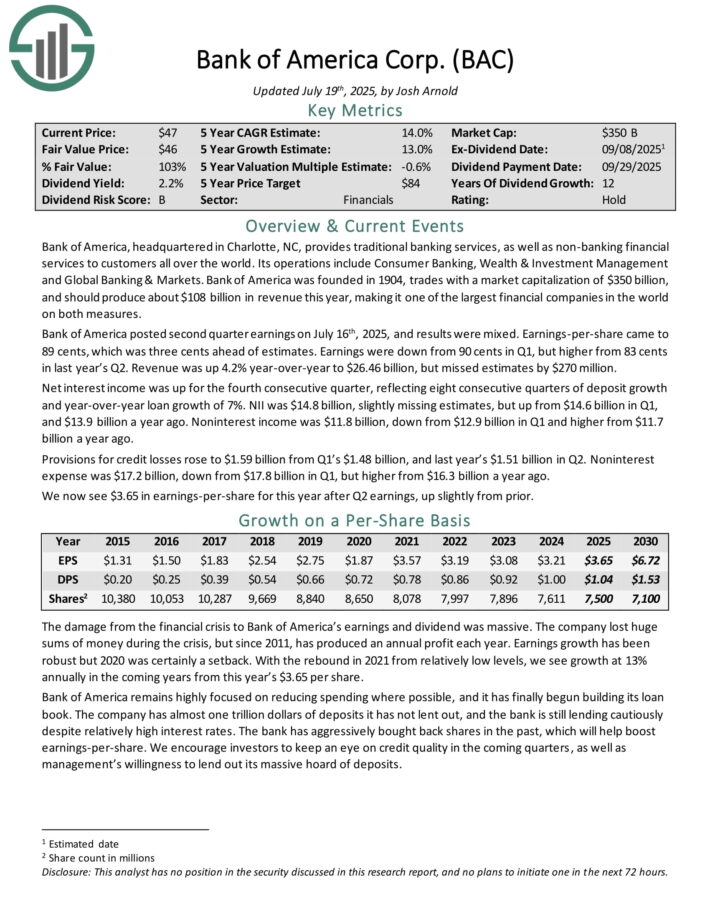

#3: Bank of America Corporation (BAC)

Dividend Yield: 2.2%

Percent of Warren Buffett’s Portfolio: 11.12%

Bank of America, headquartered in Charlotte, NC, provides traditional banking services, as well as non–banking financial services to customers all over the world. Its operations include Consumer Banking, Wealth & Investment Management and Global Banking & Markets.

Bank of America posted second quarter earnings on July 16th, 2025, and results were mixed. Earnings-per-share came to 89 cents, which was three cents ahead of estimates. Earnings were down from 90 cents in Q1, but higher from 83 cents in last year’s Q2. Revenue was up 4.2% year-over-year to $26.46 billion, but missed estimates by $270 million.

Net interest income was up for the fourth consecutive quarter, reflecting eight consecutive quarters of deposit growth and year-over-year loan growth of 7%. NII was $14.8 billion, slightly missing estimates, but up from $14.6 billion in Q1, and $13.9 billion a year ago. Noninterest income was $11.8 billion, down from $12.9 billion in Q1 and higher from $11.7 billion a year ago.

Click here to download our most recent Sure Analysis report on Bank of America (preview of page 1 of 3 shown below):

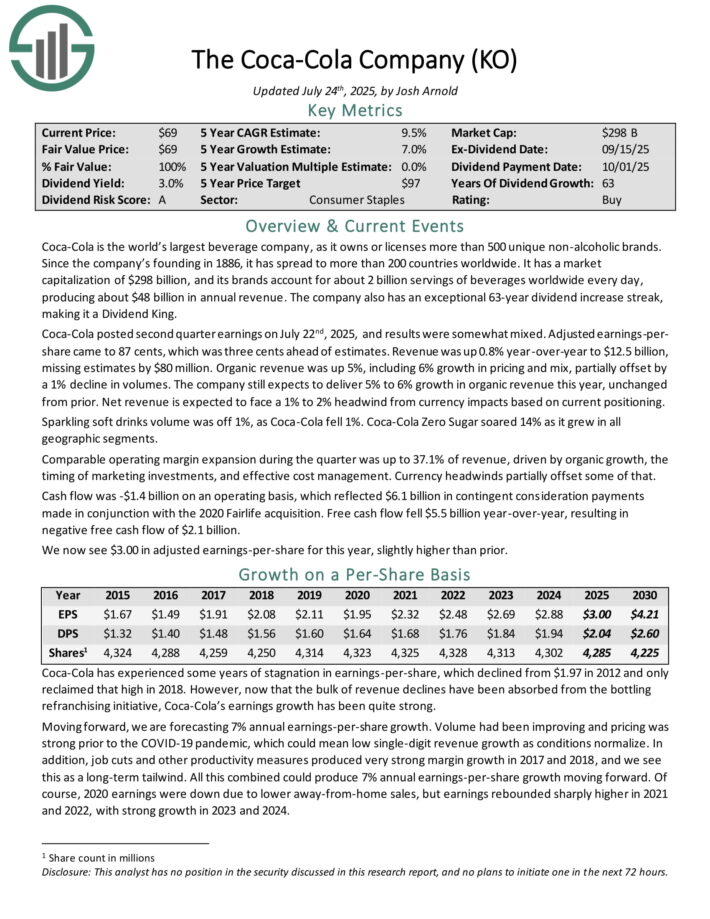

#4: The Coca-Cola Company (KO)

Dividend Yield: 3.0%

Percent of Warren Buffett’s Portfolio: 10.99%

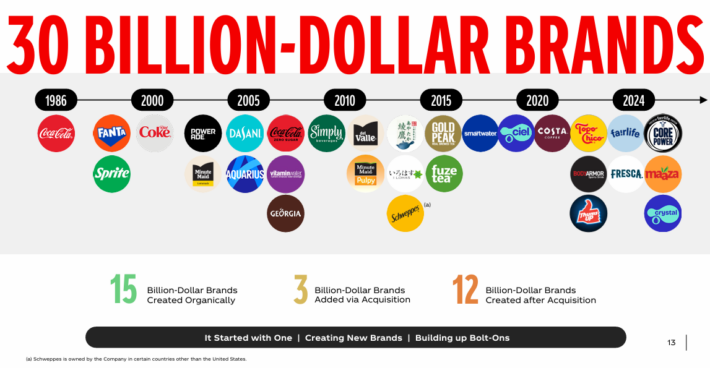

Coca-Cola is the world’s largest beverage company, as it owns or licenses more than 500 unique non–alcoholic brands. Since the company’s founding in 1886, it has spread to more than 200 countries worldwide.

Coca-Cola now has 30 billion-dollar brands in its portfolio, which each generate at least $1 billion in annual sales.

Source: Investor Presentation

Coca-Cola posted second quarter earnings on July 22nd, 2025, and results were somewhat mixed. Adjusted earnings-per-share came to 87 cents, which was three cents ahead of estimates. Revenue was up 0.8% year-over-year to $12.5 billion, missing estimates by $80 million.

Organic revenue was up 5%, including 6% growth in pricing and mix, partially offset by a 1% decline in volumes. The company still expects to deliver 5% to 6% growth in organic revenue this year, unchanged from prior. Net revenue is expected to face a 1% to 2% headwind from currency impacts based on current positioning.

Sparkling soft drinks volume was off 1%, as Coca-Cola fell 1%. Coca-Cola Zero Sugar soared 14% as it grew in all geographic segments. Comparable operating margin expansion during the quarter was up to 37.1% of revenue, driven by organic growth, the timing of marketing investments, and effective cost management. Currency headwinds partially offset some of that..

Click here to download our most recent Sure Analysis report on KO (preview of page 1 of 3 shown below):

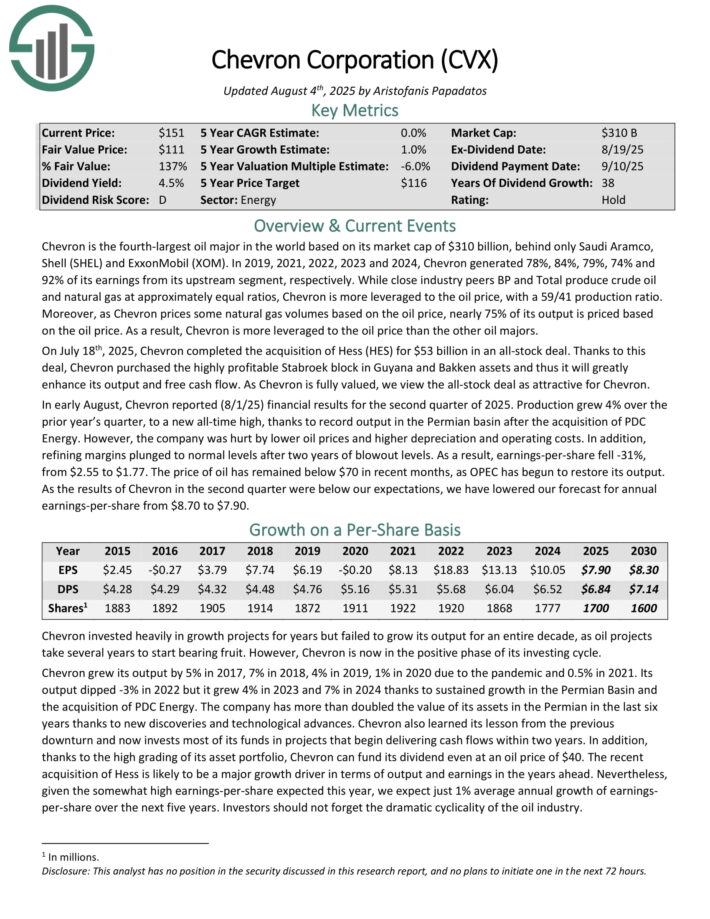

#5: Chevron Corporation (CVX)

Dividend Yield: 4.3%

Percent of Warren Buffett’s Portfolio: 6.79%

Chevron is the fourth-largest oil major in the world based on market cap. Chevron prices some natural gas volumes based on the oil price, meaning nearly 75% of its output is priced based on the oil price. As a result, Chevron is more leveraged to the oil price than the other oil majors.

Chevron has increased its dividend for 38 consecutive years, placing it on the Dividend Aristocrats list.

In early August, Chevron reported (8/1/25) financial results for the second quarter of 2025. Production grew 4% over the prior year’s quarter, to a new all-time high, thanks to record output in the Permian basin after the acquisition of PDC Energy. However, the company was hurt by lower oil prices and higher depreciation and operating costs.

In addition, refining margins plunged to normal levels after two years of blowout levels. As a result, earnings-per-share fell -31%, from $2.55 to $1.77.

The price of oil has remained below $70 in recent months, as OPEC has begun to restore its output.

Chevron’s output dipped -3% in 2022 but it grew 4% in 2023 and 7% in 2024 thanks to sustained growth in the Permian Basin and the acquisition of PDC Energy. The company has more than doubled the value of its assets in the Permian in the last six years thanks to new discoveries and technological advances.

Click here to download our most recent Sure Analysis report on Chevron Corporation (CVX) (preview of page 1 of 3 shown below):

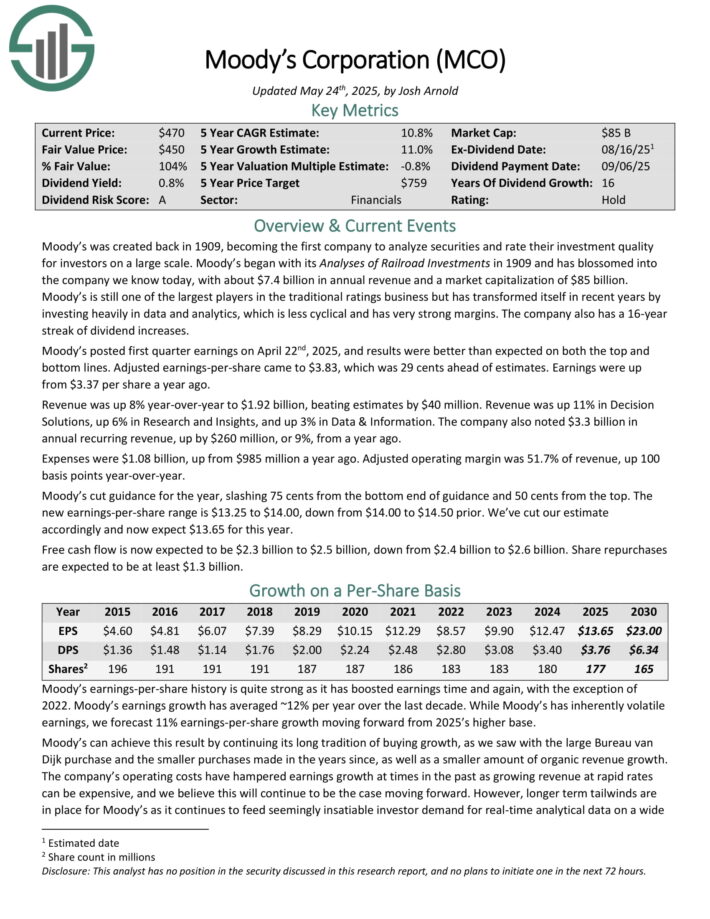

#6: Moody’s Corporation (MCO)

Dividend Yield: 0.7%

Percent of Warren Buffett’s Portfolio: 4.81%

Moody’s was created back in 1909, becoming the first company to analyze securities and rate their investment quality for investors on a large scale. Moody’s began with its Analyses of Railroad Investments in 1909 and has blossomed into the company we know today, with over $6 billion in annual revenue.

Moody’s posted first quarter earnings on April 22nd, 2025, and results were better than expected on both the top and bottom lines. Adjusted earnings-per-share came to $3.83, which was 29 cents ahead of estimates. Earnings were up from $3.37 per share a year ago.

Revenue was up 8% year-over-year to $1.92 billion, beating estimates by $40 million. Revenue was up 11% in Decision Solutions, up 6% in Research and Insights, and up 3% in Data & Information. The company also noted $3.3 billion in annual recurring revenue, up by $260 million, or 9%, from a year ago.

Expenses were $1.08 billion, up from $985 million a year ago. Adjusted operating margin was 51.7% of revenue, up 100 basis points year-over-year.

Moody’s cut guidance for the year, slashing 75 cents from the bottom end of guidance and 50 cents from the top. The new earnings-per-share range is $13.25 to $14.00, down from $14.00 to $14.50 prior. We’ve cut our estimate accordingly and now expect $13.65 for this year.

Free cash flow is now expected to be $2.3 billion to $2.5 billion, down from $2.4 billion to $2.6 billion. Share repurchases are expected to be at least $1.3 billion.

Click here to download our most recent Sure Analysis report on Moody’s (preview of page 1 of 3 shown below):

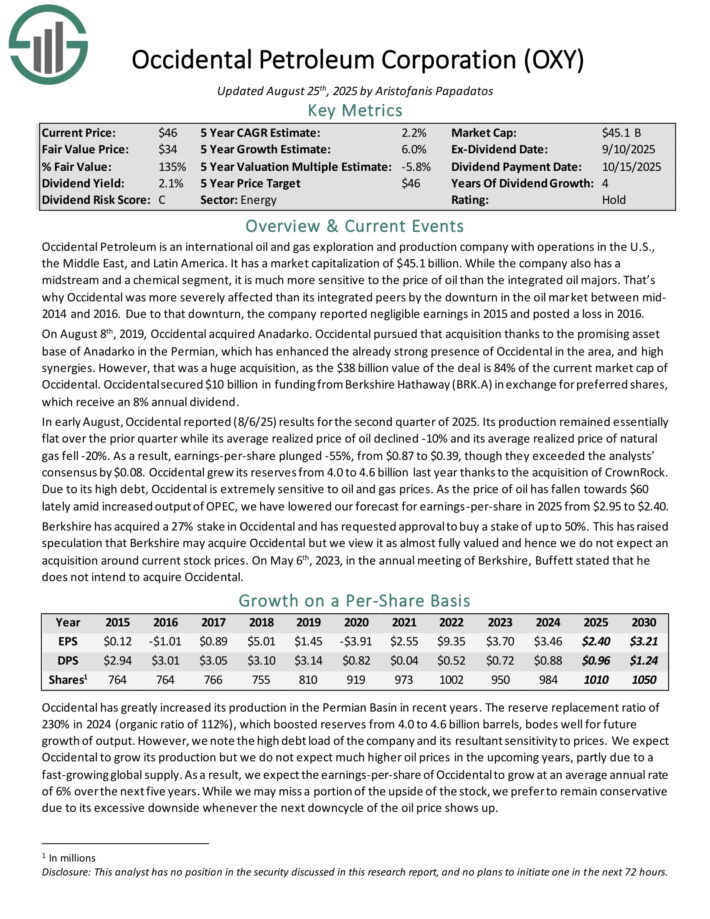

#7: Occidental Petroleum (OXY)

Dividend Yield: 2.1%

Percent of Warren Buffett’s Portfolio: 4.32%

Occidental Petroleum is an international oil and gas exploration and production company with operations in the U.S., the Middle East, and Latin America. While the company also has a midstream and a chemical segment, it is much more sensitive to the price of oil than the integrated oil majors.

In early August, Occidental reported (8/6/25) results for the second quarter of 2025. Its production remained essentially flat over the prior quarter while its average realized price of oil declined -10% and its average realized price of natural gas fell -20%.

As a result, earnings-per-share plunged -55%, from $0.87 to $0.39, though they exceeded the analysts’ consensus by $0.08. Occidental grew its reserves from 4.0 to 4.6 billion last year thanks to the acquisition of CrownRock.

Due to its high debt, Occidental is extremely sensitive to oil and gas prices. As the price of oil has fallen towards $60 lately amid increased output of OPEC, we have lowered our forecast for earnings-per-share in 2025 from $2.95 to $2.40.

Click here to download our most recent Sure Analysis report on OXY (preview of page 1 of 3 shown below):

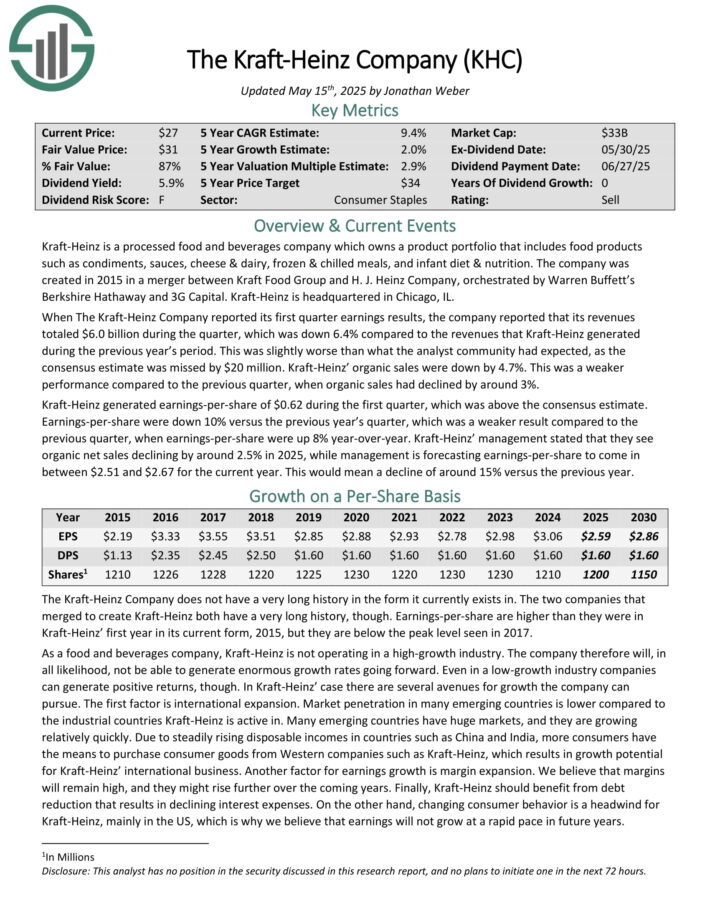

#8: The Kraft-Heinz Company (KHC)

Dividend Yield: 5.7%

Percent of Warren Buffett’s Portfolio: 3.26%

Kraft-Heinz is a processed food and beverages company which owns a product portfolio that includes food products such as condiments, sauces, cheese & dairy, frozen & chilled meals, and infant diet & nutrition.

When The Kraft-Heinz Company reported its first quarter earnings results, the company reported that its revenues totaled $6.0 billion during the quarter, which was down 6.4% compared to the revenues that Kraft-Heinz generated during the previous year’s period.

This was slightly worse than what the analyst community had expected, as the consensus estimate was missed by $20 million. Kraft-Heinz’ organic sales were down by 4.7%.

Kraft-Heinz generated earnings-per-share of $0.62 during the first quarter, which was above the consensus estimate. Earnings-per-share were down 10% versus the previous year’s quarter, which was a weaker result compared to the previous quarter, when earnings-per-share were up 8% year-over-year.

Kraft-Heinz’ management stated that they see organic net sales declining by around 2.5% in 2025, while management is forecasting earnings-per-share to come in between $2.51 and $2.67 for the current year. This would mean a decline of around 15% versus the previous year.

Click here to download our most recent Sure Analysis report on KHC (preview of page 1 of 3 shown below):

#9: Chubb Limited (CB)

Dividend Yield: 1.4%

Percent of Warren Buffett’s Portfolio: 3.04%

Chubb Ltd is a global provider of insurance and reinsurance services headquartered in Zurich, Switzerland. The company provides insurance services including property & casualty insurance, accident & health insurance, life insurance, and reinsurance.

FFor its fiscal second quarter, Chubb Ltd reported net earned premiums of $13.1 billion, which was 7% more than the net earned premiums that Chubb generated during the previous year’s quarter. Net written premiums were up 6% yearover-year in the company’s Global P&C business unit, while other business units such as Life saw solid growth as well.

Chubb was able to generate net investment income of $1.57 billion during the quarter, or $1.69 billion after adjustments, which was up by a nice 8% compared to the previous year’s period.

Chubb generated earnings-per-share of $6.14 during the second quarter, which was above the previous year’s quarter’s level.

Chubb’s above-average profitability during the quarter can be explained by strong premium growth and moderate catastrophe losses that did not cause above-average costs compared to other quarters.

Thanks to written premium growth and tailwinds from share repurchases, Chubb’s profits could be strong in the coming quarters, unless the company feels an impact from above-average catastrophe losses, which generally aren’t predictable. Chubb’s book value was up slightly during the period, ending the quarter at $174.07.

Click here to download our most recent Sure Analysis report on Chubb (preview of page 1 of 3 shown below):

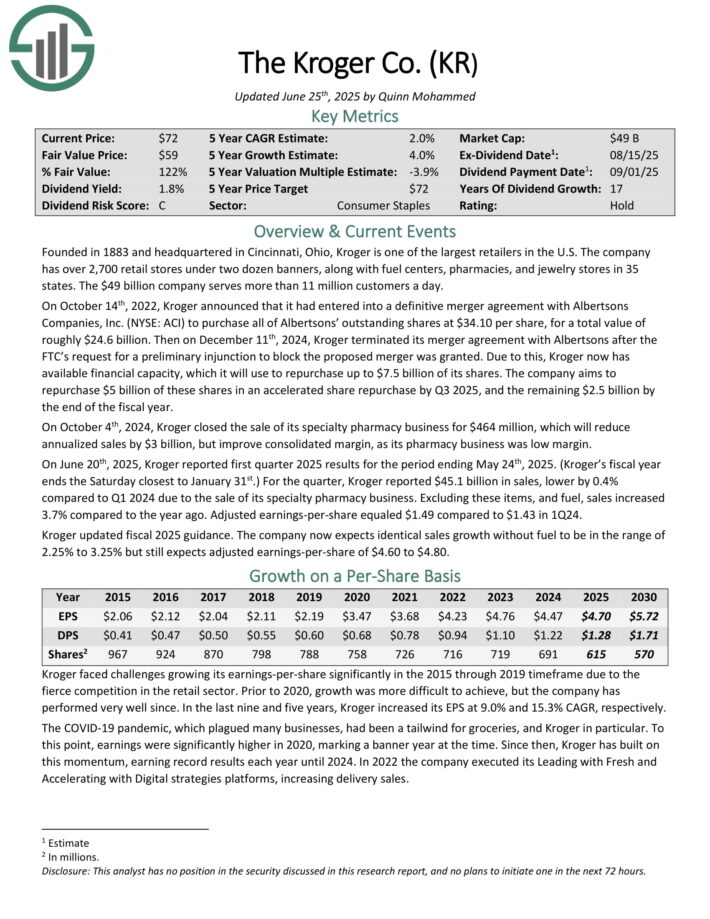

#10: The Kroger Co. (KR)

Dividend Yield: 2.1%

Percent of Warren Buffett’s Portfolio: 1.39%

Founded in 1883 and headquartered in Cincinnati, Ohio, Kroger is one of the largest retailers in the U.S. The company has nearly 2,800 retail stores under two dozen banners, along with fuel centers, pharmacies and jewelry stores in 35 states.

On June 20th, 2025, Kroger reported first quarter 2025 results for the period ending May 24th, 2025. (Kroger’s fiscal year ends the Saturday closest to January 31st.) For the quarter, Kroger reported $45.1 billion in sales, lower by 0.4% compared to Q1 2024 due to the sale of its specialty pharmacy business.

Excluding these items, and fuel, sales increased 3.7% compared to the year ago. Adjusted earnings-per-share equaled $1.49 compared to $1.43 in 1Q24.

Kroger updated fiscal 2025 guidance. The company now expects identical sales growth without fuel to be in the range of 2.25% to 3.25% but still expects adjusted earnings-per-share of $4.60 to $4.80.

Click here to download our most recent Sure Analysis report on Kroger (preview of page 1 of 3 shown below):

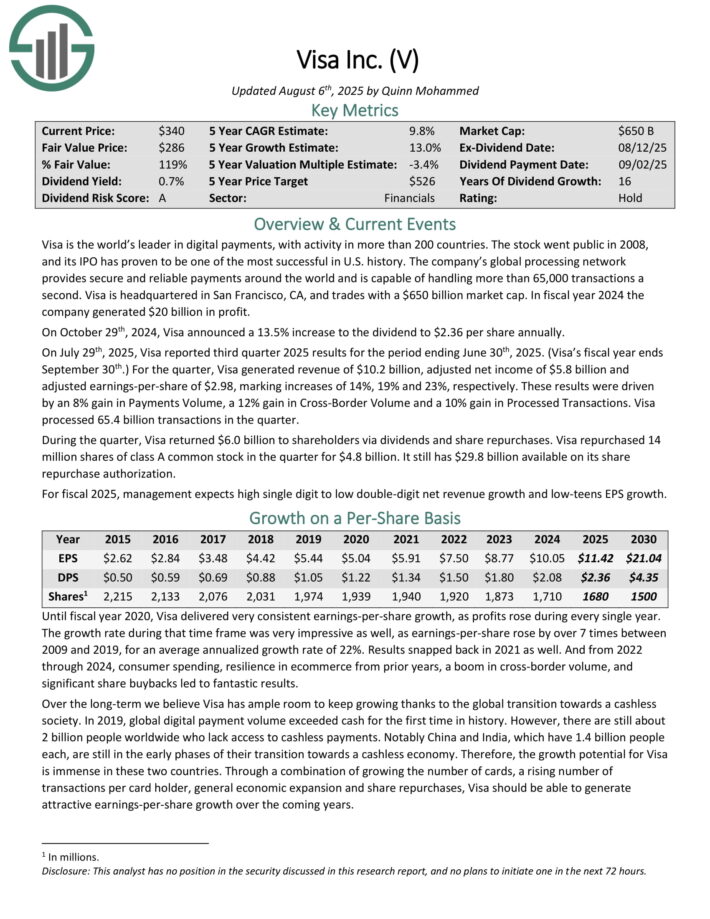

#11: Visa Inc. (V)

Dividend Yield: 0.67%

Percent of Warren Buffett’s Portfolio: 1.14%

Visa is the world’s leader in digital payments, with activity in more than 200 countries. The company’s global processing network provides secure and reliable payments around the world and is capable of handling more than 65,000 transactions a second.

On July 29th, 2025, Visa reported third quarter 2025 results for the period ending June 30th, 2025. (Visa’s fiscal year ends September 30th.) For the quarter, Visa generated revenue of $10.2 billion, adjusted net income of $5.8 billion and adjusted earnings-per-share of $2.98, marking increases of 14%, 19% and 23%, respectively.

These results were driven by an 8% gain in Payments Volume, a 12% gain in Cross-Border Volume and a 10% gain in Processed Transactions. Visa processed 65.4 billion transactions in the quarter.

During the quarter, Visa returned $6.0 billion to shareholders via dividends and share repurchases. Visa repurchased 14 million shares of class A common stock in the quarter for $4.8 billion. It still has $29.8 billion available on its share repurchase authorization. For fiscal 2025, management expects high single digit to low double-digit net revenue growth and low-teens EPS growth.

Click here to download our most recent Sure Analysis report on Visa (preview of page 1 of 3 shown below):

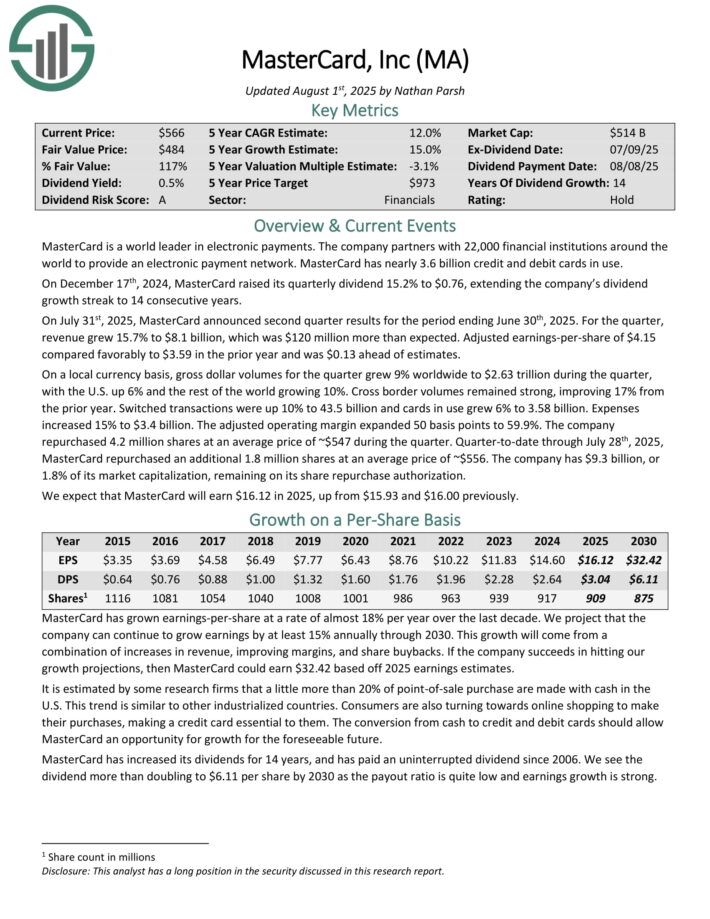

#12: Mastercard Inc. (MA)

Dividend Yield: 0.51%

Percent of Warren Buffett’s Portfolio: 0.87%

MasterCard is a world leader in electronic payments. The company partners with 25,000 financial institutions around the world to provide an electronic payment network. MasterCard has more than 3.1 billion credit and debit cards in use.

On July 31st, 2025, MasterCard announced second quarter results for the period ending June 30th, 2025. For the quarter, revenue grew 15.7% to $8.1 billion, which was $120 million more than expected. Adjusted earnings-per-share of $4.15 compared favorably to $3.59 in the prior year and was $0.13 ahead of estimates.

On a local currency basis, gross dollar volumes for the quarter grew 9% worldwide to $2.63 trillion during the quarter, with the U.S. up 6% and the rest of the world growing 10%. Cross border volumes remained strong, improving 17% from the prior year.

Switched transactions were up 10% to 43.5 billion and cards in use grew 6% to 3.58 billion. Expenses increased 15% to $3.4 billion. The adjusted operating margin expanded 50 basis points to 59.9%.

The company repurchased 4.2 million shares at an average price of ~$547 during the quarter. Quarter-to-date through July 28th, 2025, MasterCard repurchased an additional 1.8 million shares at an average price of ~$556.

Click here to download our most recent Sure Analysis report on Mastercard (preview of page 1 of 3 shown below):

#13: Amazon Inc. (AMZN)

Dividend Yield: N/A

Percent of Warren Buffett’s Portfolio: 0.85%

Amazon is a massive tech company. It is an online retailer that operates a massive e-commerce platform where consumers can buy virtually anything with their computers or smartphones. Amazon is a mega-cap stock with a market cap above $2 trillion. It operates through the following segments:

- North America

- International

- Amazon Web Services

The North America and International segments include the global retail platform of consumer products through the company’s websites. The Amazon Web Services segment sells subscriptions for cloud computing and storage services to consumers, start-ups, enterprises, government agencies, and academic institutions.

Amazon’s e-commerce operations fueled its massive revenue growth over the past decade.

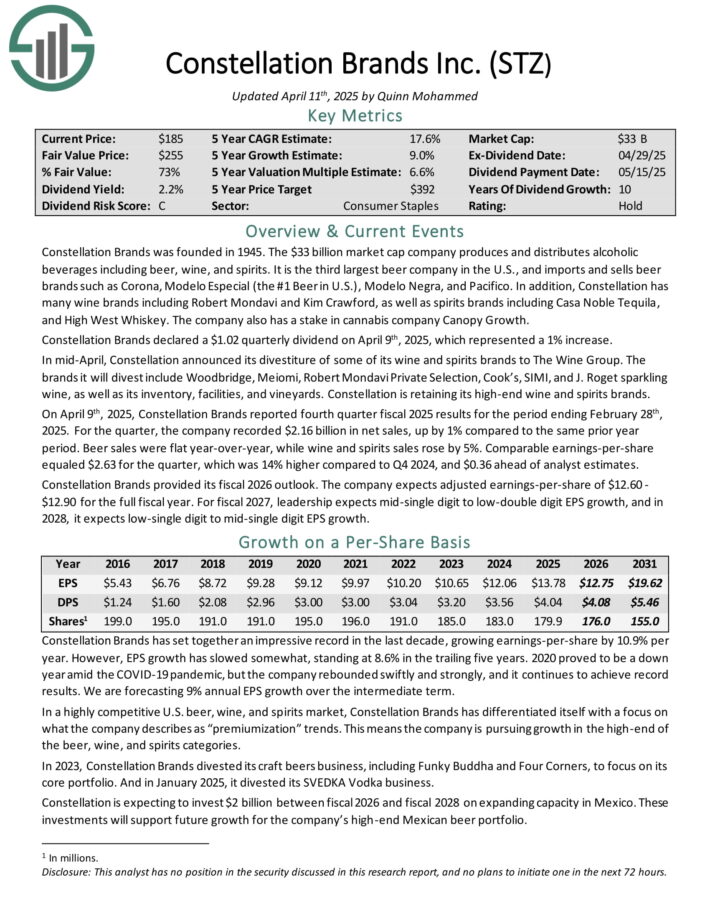

#14: Constellation Brands (STZ)

Dividend Yield: 2.5%

Percent of Warren Buffett’s Portfolio: 0.85%

Constellation Brands was founded in 1945. The $33 billion market cap company produces and distributes alcoholic beverages including beer, wine, and spirits. It is the third largest beer company in the U.S., and imports and sells beer brands such as Corona, Modelo Especial (the #1 Beer in U.S.), Modelo Negra, and Pacifico.

In addition, Constellation has many wine brands including Robert Mondavi and Kim Crawford, as well as spirits brands including Casa Noble Tequila, and High West Whiskey. The company also has a stake in cannabis company Canopy Growth.

On April 9th, 2025, Constellation Brands reported fourth quarter fiscal 2025 results for the period ending February 28th, 2025. For the quarter, the company recorded $2.16 billion in net sales, up by 1% compared to the same prior year period. Beer sales were flat year-over-year, while wine and spirits sales rose by 5%.

Comparable earnings-per-share equaled $2.63 for the quarter, which was 14% higher compared to Q4 2024, and $0.36 ahead of analyst estimates.

Constellation Brands provided its fiscal 2026 outlook. The company expects adjusted earnings-per-share of $12.60 to $12.90 for the full fiscal year.

Click here to download our most recent Sure Analysis report on STZ (preview of page 1 of 3 shown below):

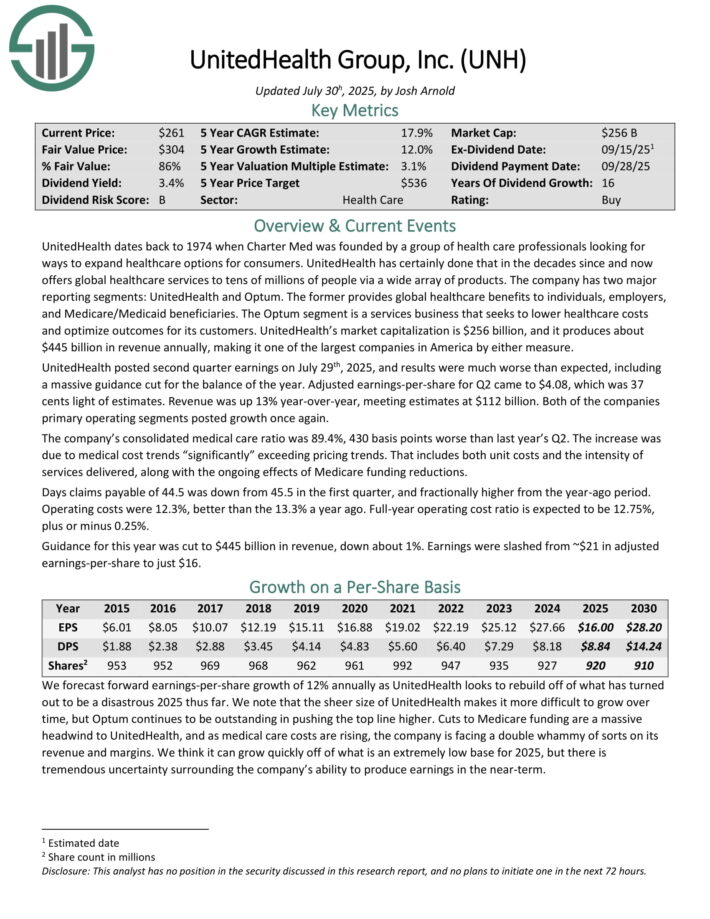

#15: UnitedHealth Group (UNH)

Dividend Yield: 2.9%

Percent of Warren Buffett’s Portfolio: 0.61%

UnitedHealth dates back to 1974 when Charter Med was founded by a group of health care professionals looking for ways to expand healthcare options for consumers. It produces about $445 billion in revenue annually.

The company has two major reporting segments: UnitedHealth and Optum. The former provides global healthcare benefits to individuals, employers, and Medicare/Medicaid beneficiaries.

The Optum segment is a services business that seeks to lower healthcare costs and optimize outcomes for its customers.

UnitedHealth posted second quarter earnings on July 29th, 2025, and results were much worse than expected, including a massive guidance cut for the balance of the year. Adjusted earnings-per-share for Q2 came to $4.08, which was 37 cents light of estimates. Revenue was up 13% year-over-year, meeting estimates at $112 billion. Both of the companies primary operating segments posted growth once again.

The company’s consolidated medical care ratio was 89.4%, 430 basis points worse than last year’s Q2. The increase was due to medical cost trends “significantly” exceeding pricing trends. That includes both unit costs and the intensity of services delivered, along with the ongoing effects of Medicare funding reductions.

Days claims payable of 44.5 was down from 45.5 in the first quarter, and fractionally higher from the year-ago period. Operating costs were 12.3%, better than the 13.3% a year ago.

Full-year operating cost ratio is expected to be 12.75%, plus or minus 0.25%. Guidance for this year was cut to $445 billion in revenue, down about 1%. Earnings were slashed from ~$21 in adjusted earnings-per-share to just $16.

Click here to download our most recent Sure Analysis report on UNH (preview of page 1 of 3 shown below):

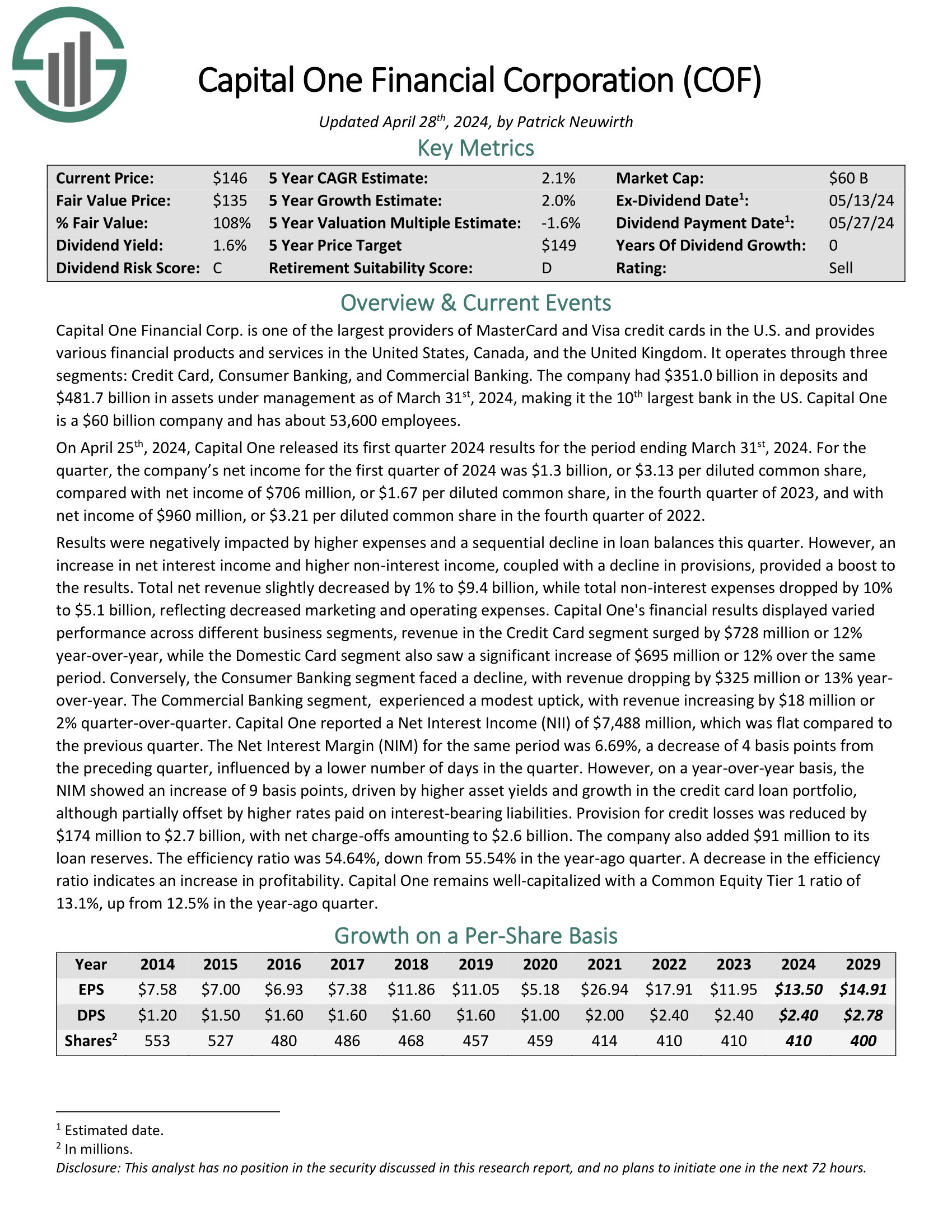

#16: Capital One Financial (COF)

Dividend Yield: 1.1%

Percent of Warren Buffett’s Portfolio: 0.59%

Capital One Financial Corp. is one of the largest providers of MasterCard and Visa credit cards in the U.S. and provides various financial products and services in the United States, Canada, and the United Kingdom. It operates through three segments: Credit Card, Consumer Banking, and Commercial Banking.

The company had $348.0 billion in deposits and $478 billion in assets under management as of the end of 2023, making it the 10th largest bank in the US.

On April 25th, 2024, Capital One released its first quarter 2024 results for the period ending March 31st, 2024. For the quarter, net income was $1.3 billion, or $3.13 per diluted common share, compared with $1.67 per diluted common share, in the fourth quarter of 2023.

Click here to download our most recent Sure Analysis report on COF (preview of page 1 of 3 shown below):

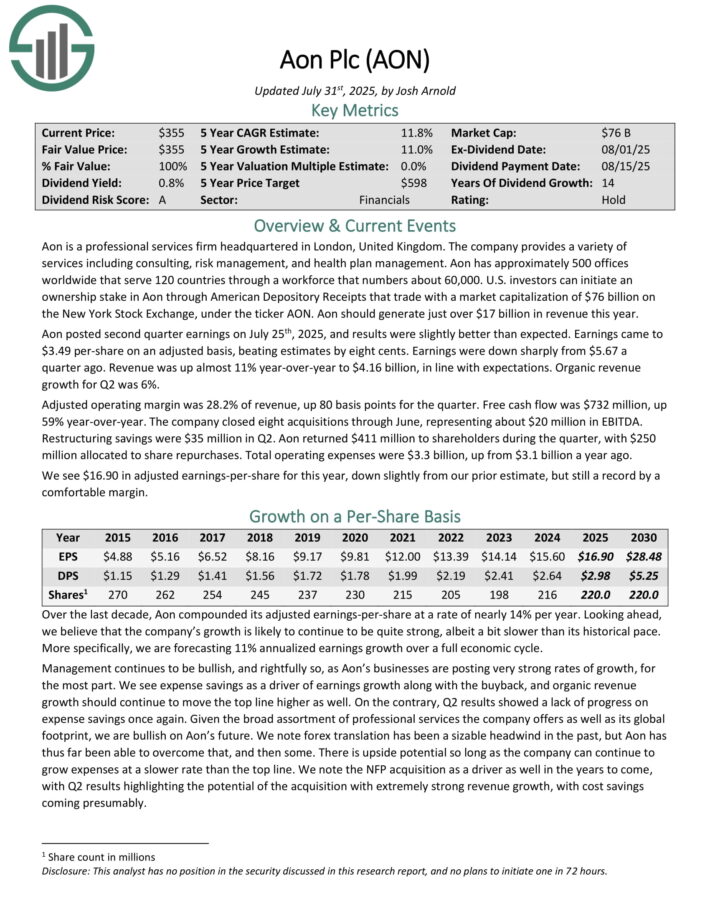

#17: Aon plc (AON)

Dividend Yield: 0.81%

Percent of Warren Buffett’s Portfolio: 0.57%

Aon is a professional services firm headquartered in London, United Kingdom. The company provides a variety of services including consulting, risk management, and health plan management.

Aon has approximately 500 offices worldwide that serve 120 countries through a workforce that numbers about 50,000.

Aon posted second quarter earnings on July 25th, 2025, and results were slightly better than expected. Earnings came to $3.49 per-share on an adjusted basis, beating estimates by eight cents. Earnings were down sharply from $5.67 a quarter ago. Revenue was up almost 11% year-over-year to $4.16 billion, in line with expectations. Organic revenue growth for Q2 was 6%.

Adjusted operating margin was 28.2% of revenue, up 80 basis points for the quarter. Free cash flow was $732 million, up 59% year-over-year. The company closed eight acquisitions through June, representing about $20 million in EBITDA.

Restructuring savings were $35 million in Q2. Aon returned $411 million to shareholders during the quarter, with $250 million allocated to share repurchases. Total operating expenses were $3.3 billion, up from $3.1 billion a year ago. .

Click here to download our most recent Sure Analysis report on Aon (preview of page 1 of 3 shown below):

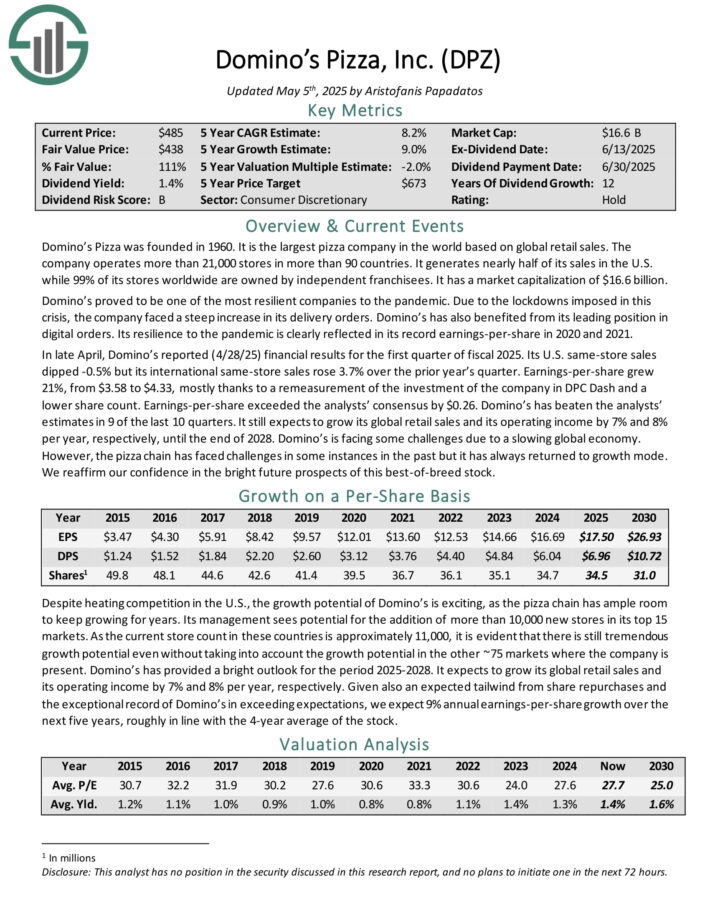

#18: Domino’s Pizza (DPZ)

Dividend Yield: 1.5%

Percent of Warren Buffett’s Portfolio: 0.46%

Domino’s Pizza was founded in 1960. It is the largest pizza company in the world based on global retail sales. The company operates more than 21,000 stores in more than 90 countries.

It generates nearly half of its sales in the U.S. while 99% of its stores worldwide are owned by independent franchisees.

In late April, Domino’s reported (4/28/25) financial results for the first quarter of fiscal 2025. Its U.S. same-store sales dipped -0.5% but its international same-store sales rose 3.7% over the prior year’s quarter. Earnings-per-share grew 21%, from $3.58 to $4.33, mostly thanks to a re-measurement of the investment of the company in DPC Dash and a lower share count.

Earnings-per-share exceeded the analysts’ consensus by $0.26. Domino’s has beaten the analysts’ estimates in 9 of the last 10 quarters. It still expects to grow its global retail sales and its operating income by 7% and 8% per year, respectively, until the end of 2028.

Click here to download our most recent Sure Analysis report on DPZ (preview of page 1 of 3 shown below):

.

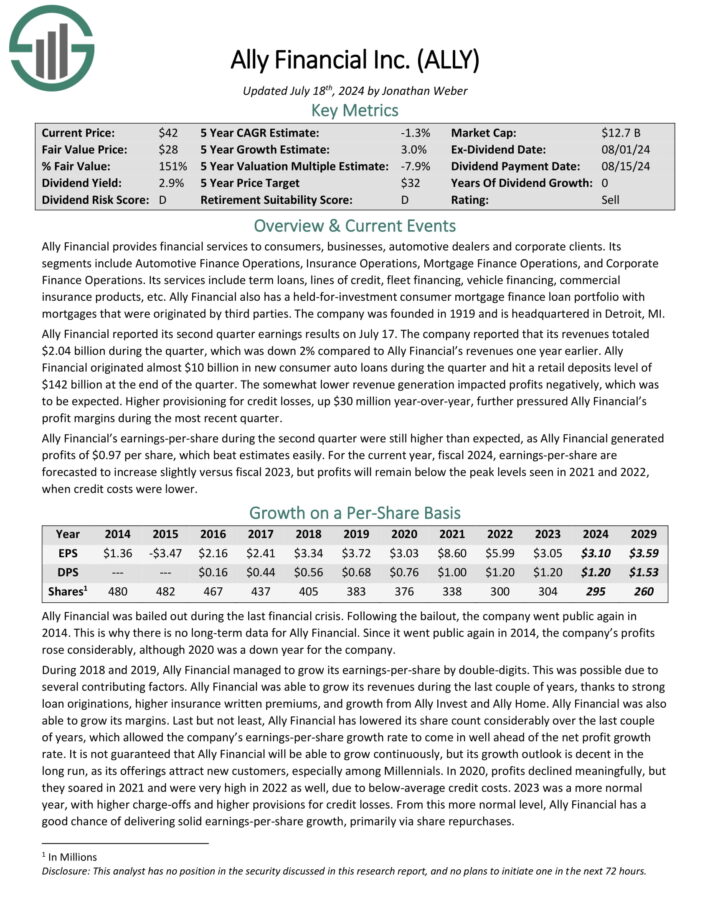

#19: Ally Financial (ALLY)

Dividend Yield: 2.9%

Percent of Warren Buffett’s Portfolio: 0.44%

Ally Financial provides financial services to consumers, businesses, automotive dealers and corporate clients. Its segments include Automotive Finance Operations, Insurance Operations, Mortgage Finance Operations, and Corporate Finance Operations.

Its services include term loans, lines of credit, fleet financing, vehicle financing, commercial insurance products, etc. Ally Financial also has a held-for-investment consumer mortgage finance loan portfolio with mortgages that were originated by third parties. The company was founded in 1919 and is headquartered in Detroit, MI.

Ally Financial reported its second quarter earnings results on July 17. The company reported that its revenues totaled $2.04 billion during the quarter, which was down 2% compared to Ally Financial’s revenues one year earlier.

Ally Financial originated almost $10 billion in new consumer auto loans during the quarter and hit a retail deposits level of $142 billion at the end of the quarter. The somewhat lower revenue generation impacted profits negatively, which was to be expected. Higher provisioning for credit losses, up $30 million year-over-year, further pressured Ally Financial’s profit margins during the most recent quarter.

Ally Financial’s earnings-per-share during the second quarter were still higher than expected, as Ally Financial generated profits of $0.97 per share, which beat estimates easily. For the current year, fiscal 2024, earnings-per-share are forecasted to increase slightly versus fiscal 2023.

Click here to download our most recent Sure Analysis report on ALLY (preview of page 1 of 3 shown below):

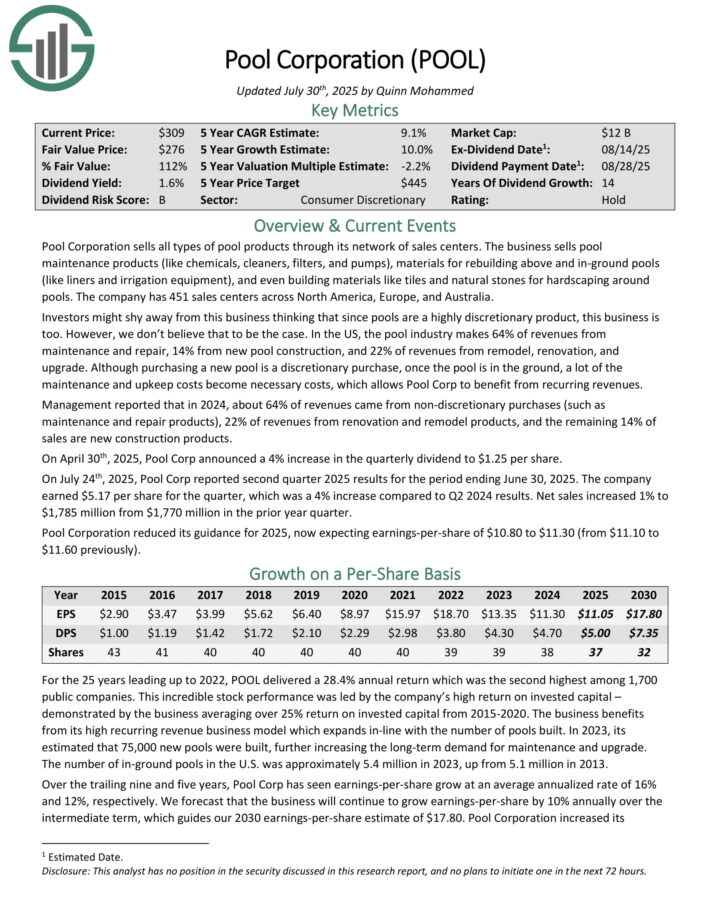

#20: Pool Corporation (POOL)

Dividend Yield: 1.57%

Percent of Warren Buffett’s Portfolio: 0.39%

Pool Corporation sells all types of pool products through its network of sales centers. The business sells pool maintenance products (like chemicals, cleaners, filters, and pumps), materials for rebuilding above and in-ground pools (like liners and irrigation equipment), and even building materials like tiles and natural stones for hardscaping around pools. The company has 451 sales centers across North America, Europe, and Australia.

Investors might shy away from this business thinking that since pools are a highly discretionary product, this business is too. However, we don’t believe that to be the case. In the US, the pool industry makes 64% of revenues from maintenance and repair, 14% from new pool construction, and 22% of revenues from remodel, renovation, and upgrade. Although purchasing a new pool is a discretionary purchase, once the pool is in the ground, a lot of the maintenance and upkeep costs become necessary costs, which allows Pool Corp to benefit from recurring revenues.

Management reported that in 2024, about 64% of revenues came from non-discretionary purchases (such as maintenance and repair products), 22% of revenues from renovation and remodel products, and the remaining 14% of sales are new construction products.

On April 30th, 2025, Pool Corp announced a 4% increase in the quarterly dividend to $1.25 per share.

On July 24th, 2025, Pool Corp reported second quarter 2025 results for the period ending June 30, 2025. The company earned $5.17 per share for the quarter, which was a 4% increase compared to Q2 2024 results. Net sales increased 1% to $1,785 million from $1,770 million in the prior year quarter.

Click here to download our most recent Sure Analysis report on POOL (preview of page 1 of 3 shown below):

Final Thoughts

You can see the following additional articles regarding Warren Buffett:

- Warren Buffett’s 106 Best Quotes Of All Time

- Snowball Effect Investing | Compound Your Wealth Like Warren Buffett

Warren Buffett stocks represent many of the strongest, most long-lived businesses around. You can see more high-quality dividend stocks in the following Sure Dividend databases:

- The 2024 Dividend Kings List: Dividend Stocks With 50+ Years of Rising Dividends

- The 2024 Dividend Aristocrats List: 25+ Years of Rising Dividends

- The 20 Highest Yielding Dividend Aristocrats Now

- Blue Chips List: Stocks With 10+ Years of Rising Dividends

You might also be looking to create a highly customized dividend income stream to pay for life’s expenses.

The following two lists provide useful information on high dividend stocks and stocks that pay monthly dividends: