Updated on June 15th, 2026 by Bob Ciura

Water is one of the basic necessities of human life. Life as we know it cannot exist without water. For this simple reason, water may be the most valuable commodity on Earth.

It is only natural for investors to consider purchasing water stocks. There are many different companies that can give investors exposure to the water business, such as water utilities. Some other companies are engaged in water purification.

In all, we have compiled a list of over 40 stocks that are in the business of water. The list was derived from two of the top water industry exchange-traded funds:

- Invesco Water Resources ETF (PHO)

- First Trust ISE Water Index Fund (FIW)

You can download a spreadsheet with all 43 water stocks (along with metrics that matter like price-to-earnings ratios and dividend yields) by clicking on the link below:

In addition to the Excel spreadsheet above, this article covers our top 10 water stocks today, that we cover in the Sure Analysis Research Database.

The top water stocks are ranked according to their annual expected returns over the next five years, in order of lowest to highest.

Table of Contents

- Water Stock #10: A.O. Smith (AOS)

- Water Stock #9: Pentair plc (PNR)

- Water Stock #8: Roper Technologies (ROP)

- Water Stock #7: Advanced Drainage Systems (WMS)

- Water Stock #6: Agilent Technologies (A)

- Water Stock #5: Jacobs Solutions (J)

- Water Stock #4: H2O America (HTO)

- Water Stock #3: Tetra Tech (TTEK)

- Water Stock #2: Stantec Inc. (STN)

- Water Stock #1: Badger Meter Inc. (BMI)

Water Stock #10: A.O. Smith (AOS)

- 5-year expected annual returns: 12.5%

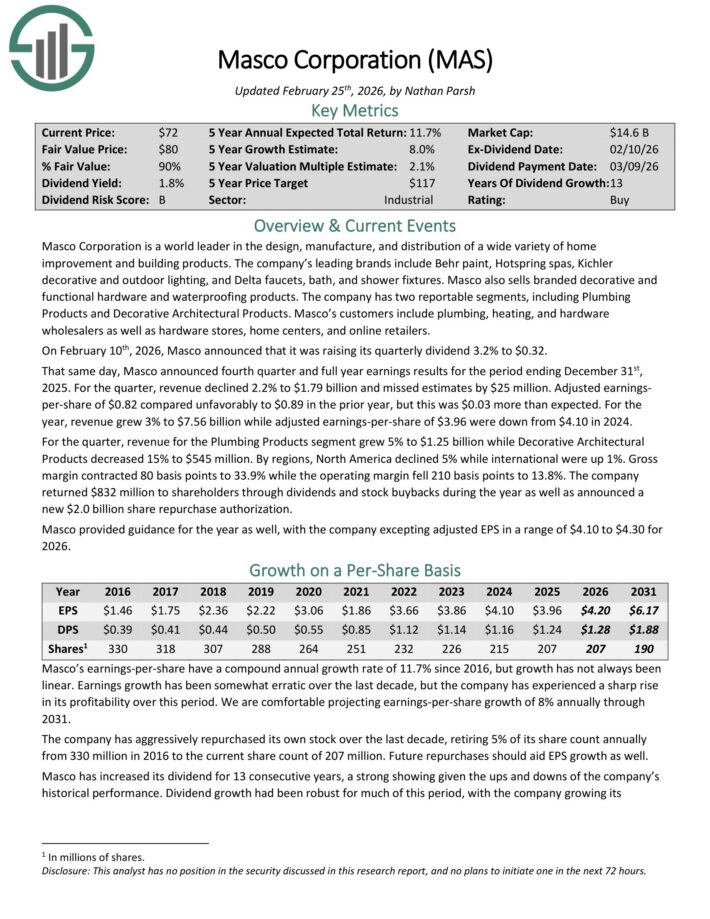

Masco Corporation is a world leader in the design, manufacture, and distribution of a wide variety of home improvement and building products.

The company’s leading brands include Behr paint, Hotspring spas, Kichler decorative and outdoor lighting, and Delta faucets, bath, and shower fixtures.

Masco also sells branded decorative and functional hardware and waterproofing products. The company has two reportable segments, including Plumbing Products and Decorative Architectural Products.

On February 10th, 2026, Masco raised its quarterly dividend 3.2% to $0.32. That same day, Masco announced fourth quarter and full year earnings results.

For the quarter, revenue declined 2.2% to $1.79 billion and missed estimates by $25 million. Adjusted earnings-per-share of $0.82 compared unfavorably to $0.89 in the prior year, but this was $0.03 more than expected.

For the year, revenue grew 3% to $7.56 billion while adjusted earnings-per-share of $3.96 were down from $4.10 in 2024.

For the quarter, revenue for the Plumbing Products segment grew 5% to $1.25 billion while Decorative Architectural Products decreased 15% to $545 million. By regions, North America declined 5% while international were up 1%.

Gross margin contracted 80 basis points to 33.9% while the operating margin fell 210 basis points to 13.8%.

The company returned $832 million to shareholders through dividends and stock buybacks during the year as well as announced a new $2.0 billion share repurchase authorization.

Masco provided guidance for the year as well, with the company excepting adjusted EPS in a range of $4.10 to $4.30 for 2026.

Click here to download our most recent Sure Analysis report on MAS (preview of page 1 of 3 shown below):

Water Stock #9: Pentair plc (PNR)

- 5-year expected annual returns: 13.7%

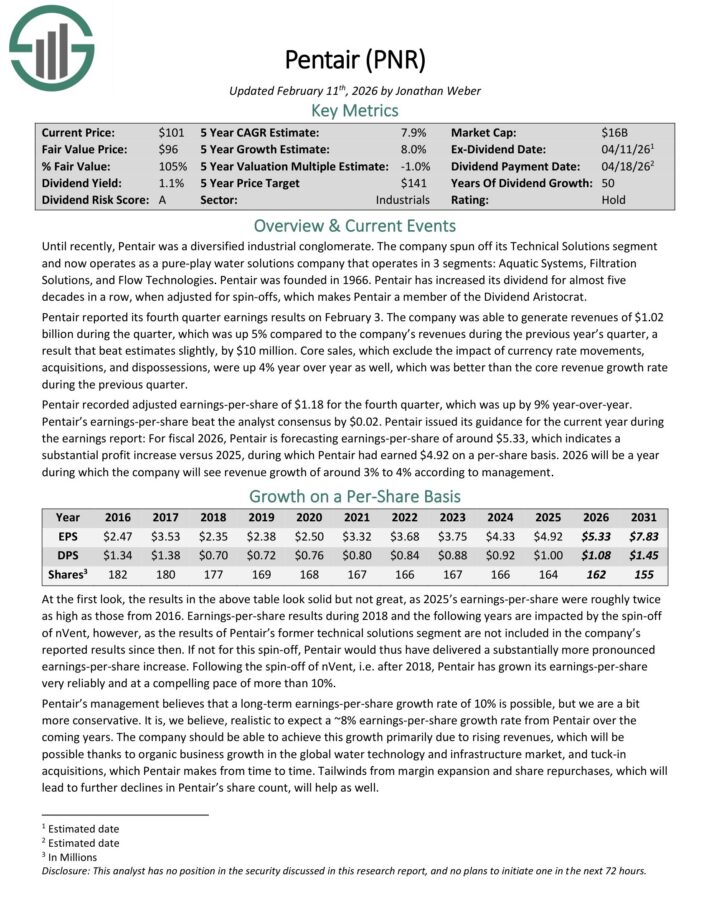

Pentair plc is a pure-play water solutions company that operates in 3 segments: Aquatic Systems, Filtration Solutions, and Flow Technologies.

Pentair was founded in 1966. Pentair has increased its dividend for almost five decades in a row, when adjusted for spin-offs, which makes Pentair a member of the Dividend Aristocrat.

Pentair reported its fourth quarter earnings results on February 3. The company generated revenues of $1.02 billion during the quarter, which was up 5% compared to the company’s revenues during the previous year’s quarter, a result that beat estimates slightly, by $10 million.

Core sales, which exclude the impact of currency rate movements, acquisitions, and dispossessions, were up 4% year over year as well, which was better than the core revenue growth rate during the previous quarter.

Pentair recorded adjusted earnings-per-share of $1.18 for the fourth quarter, which was up by 9% year-over-year. Pentair’s earnings-per-share beat the analyst consensus by $0.02.

For fiscal 2026, Pentair is forecasting earnings-per-share of around $5.33, which indicates a substantial profit increase versus 2025, during which Pentair had earned $4.92 on a per-share basis.

Click here to download our most recent Sure Analysis report on PNR (preview of page 1 of 3 shown below):

Water Stock #8: Roper Technologies (ROP)

- 5-year expected annual returns: 13.7%

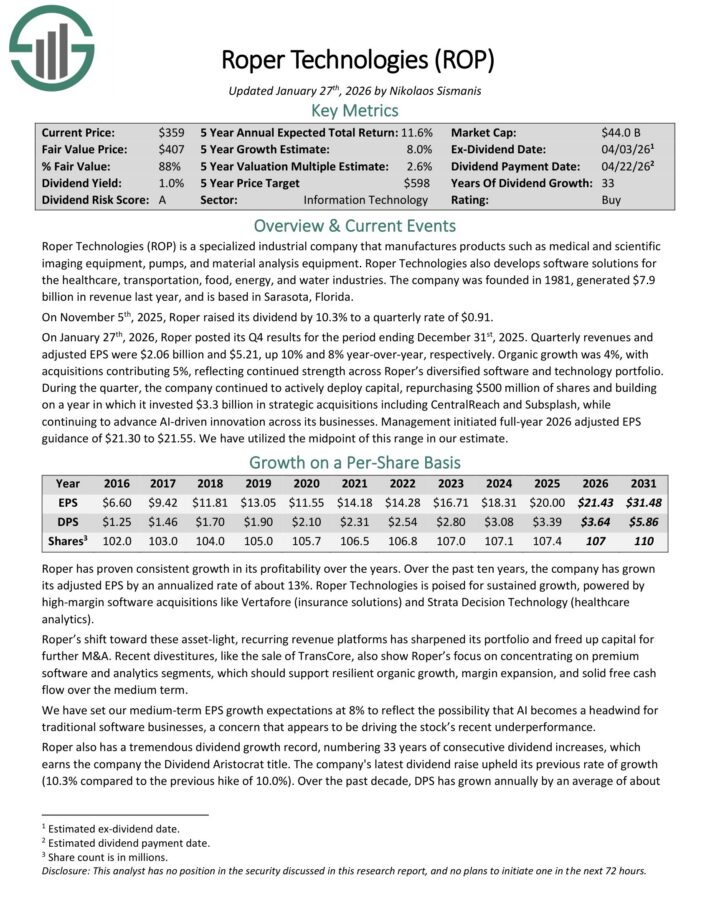

Roper Technologies is a specialized industrial company that manufactures products such as medical and scientific imaging equipment, pumps, and material analysis equipment.

The company also develops software solutions for the healthcare, transportation, food, energy, and water industries. It generated $7.9 billion in revenue last year, and is based in Sarasota, Florida.

On November 5th, 2025, Roper raised its dividend by 10.3% to a quarterly rate of $0.91. The company has increased its dividend for 33 consecutive years.

On January 27th, 2026, Roper posted its Q4 results. Quarterly revenue and adjusted EPS were $2.06 billion and $5.21, up 10% and 8% year-over-year, respectively.

Organic growth was 4%, with acquisitions contributing 5%, reflecting continued strength across Roper’s diversified software and technology portfolio.

During the quarter, the company continued to actively deploy capital, repurchasing $500 million of shares and building on a year in which it invested $3.3 billion in strategic acquisitions including CentralReach and Subsplash, while continuing to advance AI-driven innovation across its businesses.

Management initiated full-year 2026 adjusted EPS guidance of $21.30 to $21.55.

Click here to download our most recent Sure Analysis report on ROP (preview of page 1 of 3 shown below):

Water Stock #7: Advanced Drainage Systems (WMS)

- 5-year expected annual returns: 14.6%

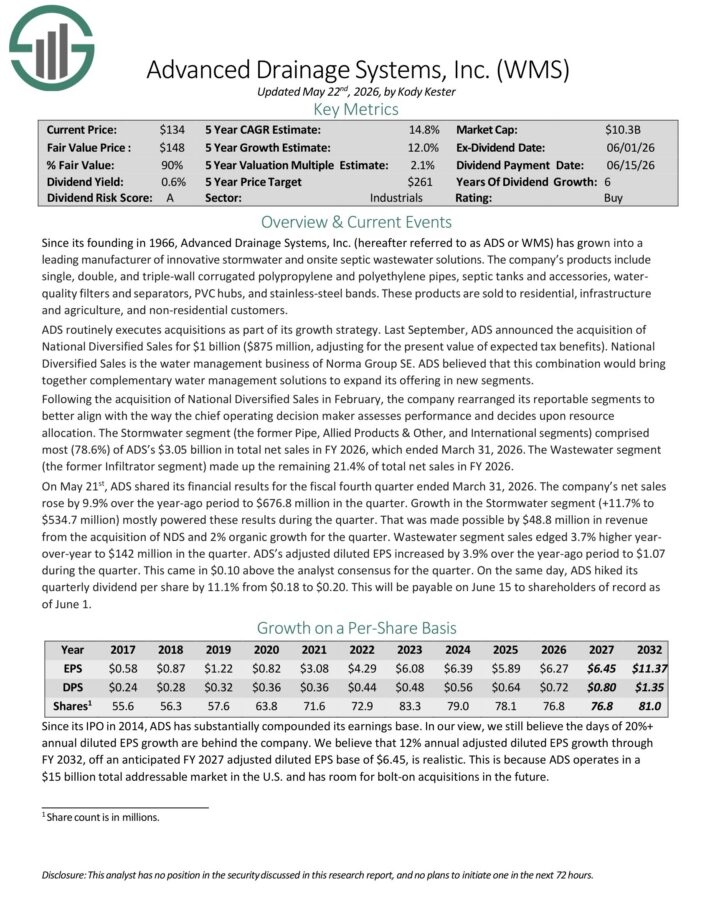

Advanced Drainage Systems is a leading manufacturer of innovative stormwater and onsite septic wastewater solutions.

The company’s products include single, double, and triple-wall corrugated polypropylene and polyethylene pipes, septic tanks and accessories, water quality filters and separators, PVC hubs, and stainless-steel bands.

On May 21st, ADS shared its financial results for the fiscal fourth quarter ended March 31, 2026. The company’s net sales rose by 9.9% over the year-ago period to $676.8 million in the quarter.

Growth in the Stormwater segment (+11.7% to $534.7 million) mostly powered these results during the quarter.

That was made possible by $48.8 million in revenue from the acquisition of NDS and 2% organic growth for the quarter. Wastewater segment sales edged 3.7% higher year-over-year to $142 million in the quarter.

Adjusted diluted EPS increased by 3.9% over the year-ago period to $1.07 during the quarter. This came in $0.10 above the analyst consensus for the quarter.

On the same day, ADS hiked its quarterly dividend per share by 11.1% from $0.18 to $0.20.

Click here to download our most recent Sure Analysis report on WMS (preview of page 1 of 3 shown below):

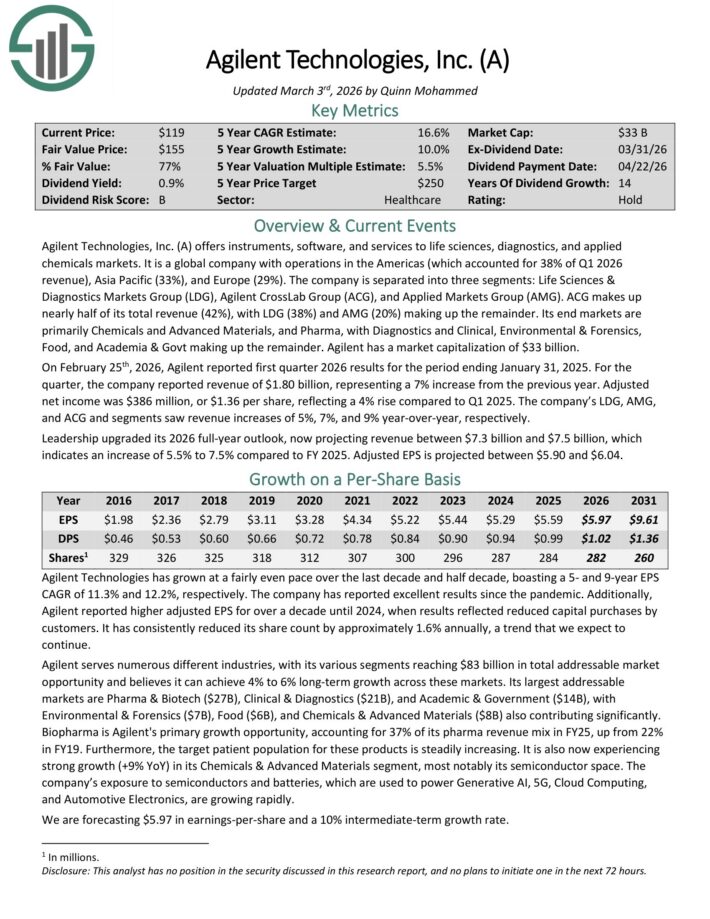

Water Stock #6: Agilent Technologies (A)

- 5-year expected annual returns: 14.8%

Agilent Technologies offers instruments, software, and services to life sciences, diagnostics, and applied chemicals markets.

It is a global company with operations in the Americas, Asia Pacific, and Europe.

The company is separated into three segments: Life Sciences & Diagnostics Markets Group (LDG), Agilent CrossLab Group (ACG), and Applied Markets Group (AMG).

ACG makes up nearly half of its total revenue (42%), with LDG (38%) and AMG (20%) making up the remainder.

Its end markets are primarily Chemicals and Advanced Materials, and Pharma, with Diagnostics and Clinical, Environmental & Forensics, Food, and Academia & Govt making up the remainder.

On February 25th, 2026, Agilent reported first quarter 2026 results for the period ending January 31, 2025. For the quarter, the company reported revenue of $1.80 billion, representing a 7% increase from the previous year.

Adjusted net income was $386 million, or $1.36 per share, reflecting a 4% rise compared to Q1 2025. The company’s LDG, AMG, and ACG and segments saw revenue increases of 5%, 7%, and 9% year-over-year, respectively.

Leadership upgraded its 2026 full-year outlook, now projecting revenue between $7.3 billion and $7.5 billion, which indicates an increase of 5.5% to 7.5% compared to FY 2025. Adjusted EPS is projected between $5.90 and $6.04.

Click here to download our most recent Sure Analysis report on A (preview of page 1 of 3 shown below):

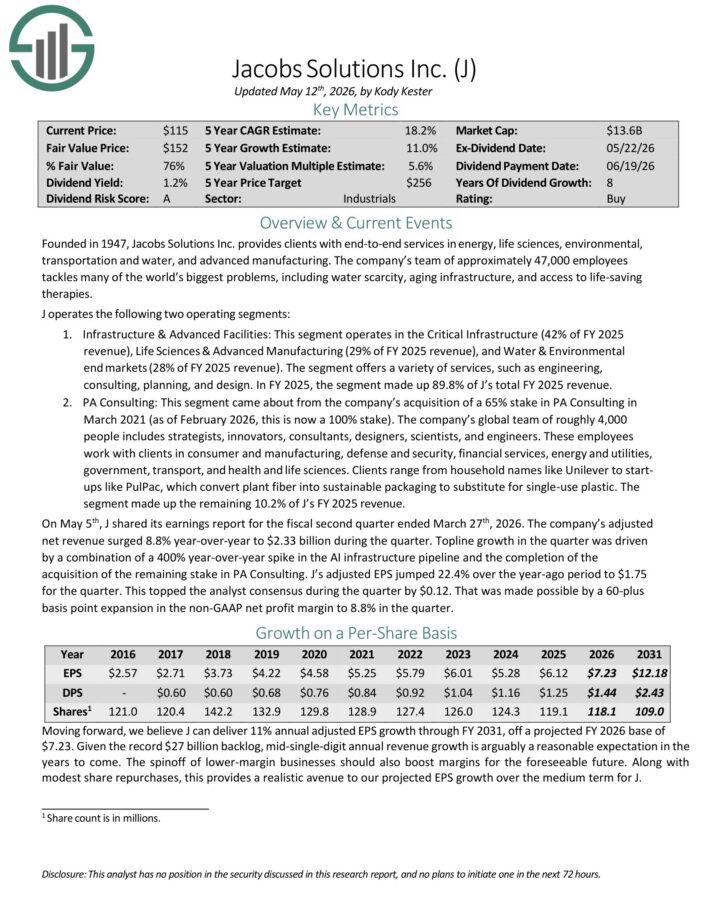

Water Stock #5: Jacobs Solutions (J)

- 5-year expected annual returns: 15.9%

Jacobs Solutions Inc. provides clients with end-to-end services in energy, life sciences, environmental, transportation and water, and advanced manufacturing.

The company operates the following two operating segments: Infrastructure & Advanced Facilities and PA Consulting.

On May 5th, J shared its earnings report for the fiscal second quarter ended March 27th, 2026. Adjusted net revenue surged 8.8% year-over-year to $2.33 billion during the quarter.

Top-line growth in the quarter was driven by a combination of a 400% year-over-year spike in the AI infrastructure pipeline and the completion of the acquisition of the remaining stake in PA Consulting.

Adjusted EPS jumped 22.4% over the year-ago period to $1.75 for the quarter. This topped the analyst consensus during the quarter by $0.12.

Click here to download our most recent Sure Analysis report on J (preview of page 1 of 3 shown below):

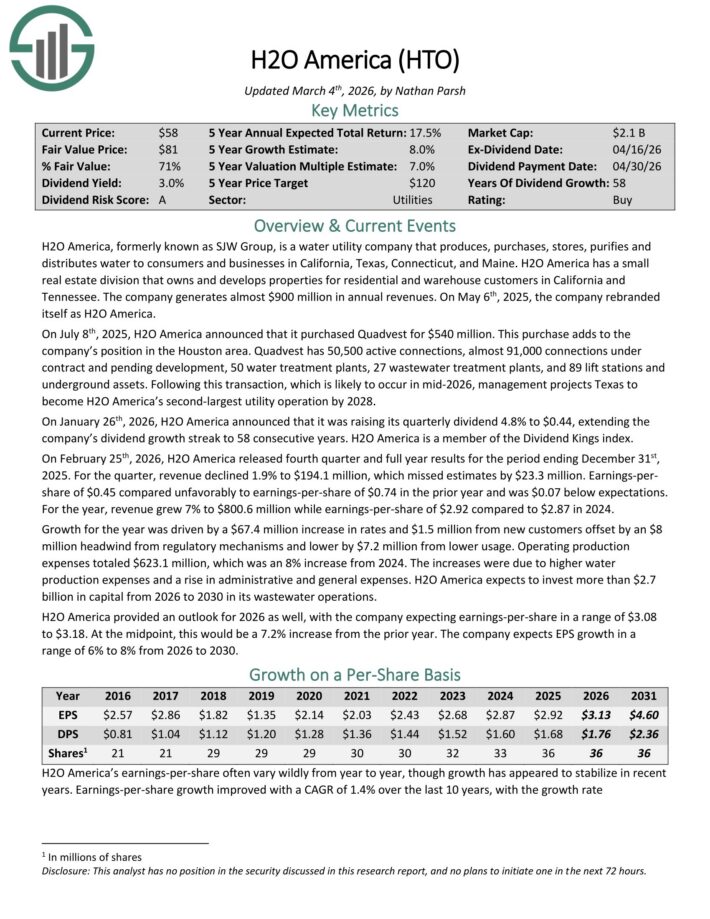

Water Stock #4: H2O America (HTO)

- 5-year expected annual returns: 17.8%

H2O America, formerly known as SJW Group, is a water utility company that produces, purchases, stores, purifies and distributes water to consumers and businesses in the Silicon Valley area of California, the area north of San Antonio, Texas, Connecticut, and Maine.

It also has a small real estate division that owns and develops properties for residential and warehouse customers in California and Tennessee. The company generates about $670 million in annual revenues.

On January 26th, 2026, H2O America raised its quarterly dividend 4.8% to $0.44, extending the company’s dividend growth streak to 58 consecutive years.

On February 25th, 2026, H2O America released fourth quarter and full year results for the period ending December 31st, 2025. For the quarter, revenue declined 1.9% to $194.1 million, which missed estimates by $23.3 million.

Earnings-per-share of $0.45 compared unfavorably to earnings-per-share of $0.74 in the prior year and was $0.07 below expectations.

For the year, revenue grew 7% to $800.6 million while earnings-per-share of $2.92 compared to $2.87 in 2024.

Growth for the year was driven by a $67.4 million increase in rates and $1.5 million from new customers offset by an $8 million headwind from regulatory mechanisms and lower by $7.2 million from lower usage.

H2O America provided an outlook for 2026 as well, with the company expecting earnings-per-share in a range of $3.08 to $3.18. At the midpoint, this would be a 7.2% increase from the prior year.

Click here to download our most recent Sure Analysis report on HTO (preview of page 1 of 3 shown below):

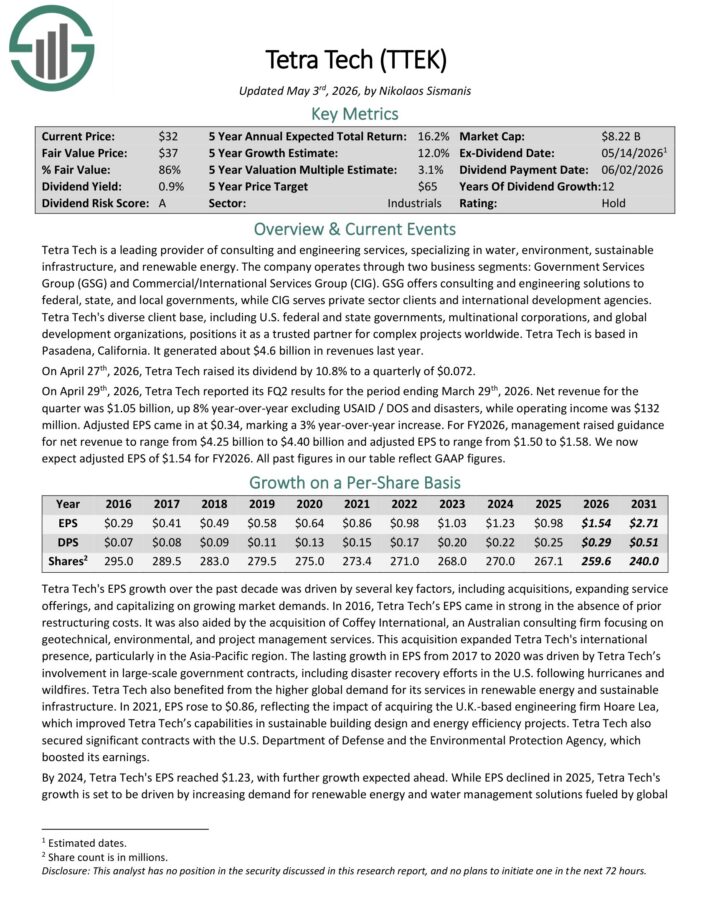

Water Stock #3: Tetra Tech (TTEK)

- 5-year expected annual returns: 18.8%

Tetra Tech is a leading provider of consulting and engineering services, specializing in water, environment, sustainable infrastructure, and renewable energy.

The company operates through two business segments: Government Services Group (GSG) and Commercial/International Services Group (CIG).

GSG offers consulting and engineering solutions to federal, state, and local governments, while CIG serves private sector clients and international development agencies.

On April 27th, 2026, Tetra Tech raised its dividend by 10.8% to a quarterly of $0.072.

On April 29th, 2026, Tetra Tech reported its FQ2 results for the period ending March 29th, 2026. Net revenue for the quarter was $1.05 billion, up 8% year-over-year excluding USAID / DOS and disasters, while operating income was $132 million. Adjusted EPS came in at $0.34, marking a 3% year-over-year increase.

For FY2026, management raised guidance for net revenue to range from $4.25 billion to $4.40 billion and adjusted EPS to range from $1.50 to $1.58. We now expect adjusted EPS of $1.54 for FY2026.

Click here to download our most recent Sure Analysis report on TTEK (preview of page 1 of 3 shown below):

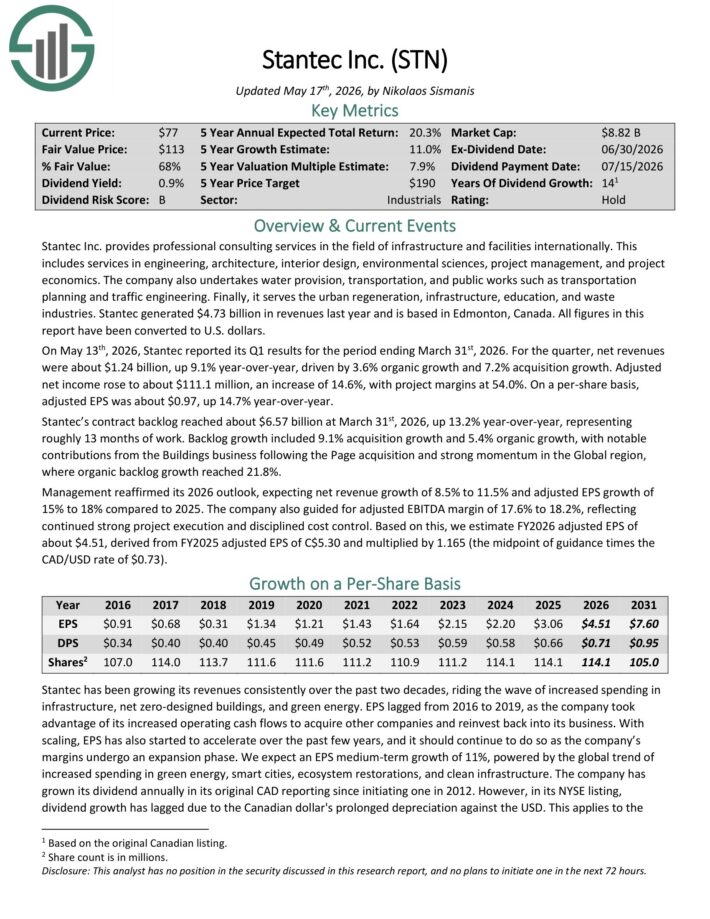

Water Stock #2: Stantec Inc. (STN)

- 5-year expected annual returns: 21.9%

Stantec Inc. provides professional consulting services in the field of infrastructure and facilities internationally.

This includes services in engineering, architecture, interior design, environmental sciences, project management, and project economics.

The company also undertakes water provision, transportation, and public works such as transportation planning and traffic engineering. Finally, it serves the urban regeneration, infrastructure, education, and waste industries.

Stantec generated $4.73 billion in revenues last year and is based in Edmonton, Canada. All figures in this report have been converted to U.S. dollars.

On February 25th, 2026, Stantec raised its dividend by 8.9% to a quarterly rate of C$0.245.

On May 13th, 2026, Stantec reported its Q1 results for the period ending March 31st, 2026. For the quarter, net revenue was about $1.24 billion, up 9.1% year-over-year, driven by 3.6% organic growth and 7.2% acquisition growth.

Adjusted net income rose to about $111.1 million, an increase of 14.6%, with project margins at 54.0%. On a per-share basis, adjusted EPS was about $0.97, up 14.7% year-over-year.

Stantec’s contract backlog reached about $6.57 billion at March 31st, 2026, up 13.2% year-over-year, representing roughly 13 months of work.

Backlog growth included 9.1% acquisition growth and 5.4% organic growth, with notable contributions from the Buildings business following the Page acquisition and strong momentum in the Global region, where organic backlog growth reached 21.8%.

Click here to download our most recent Sure Analysis report on STN (preview of page 1 of 3 shown below):

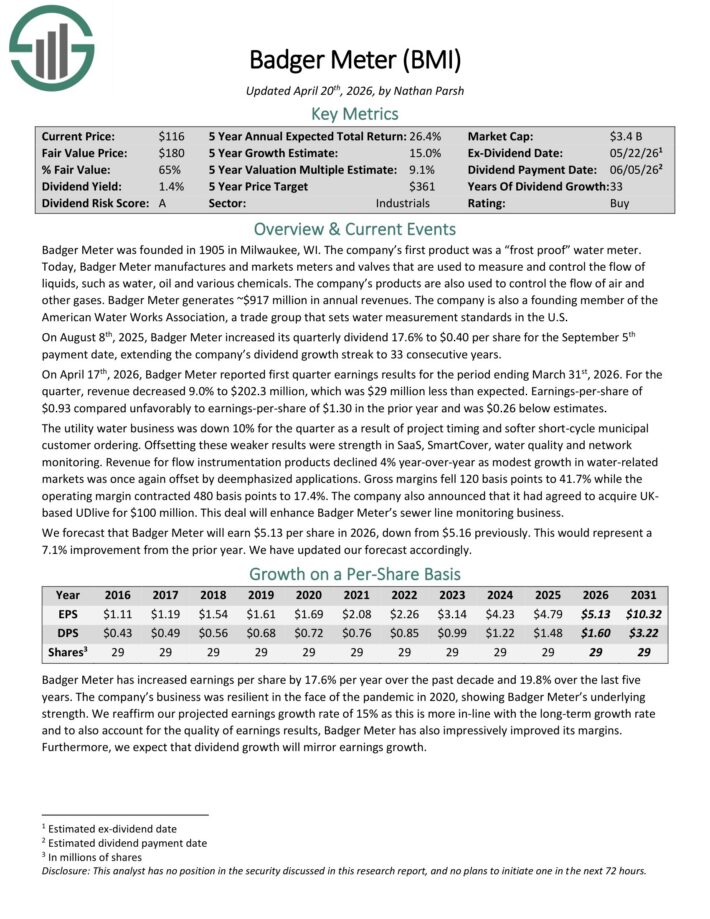

Water Stock #1: Badger Meter (BMI)

- 5-year expected annual returns: 23.2%

Badger Meter manufactures and markets meters and valves that are used to measure and control the flow of liquids, such as water, oil and various chemicals.

The company’s products are also used to control the flow of air and other gases. Badger Meter generates ~$917 million in annual revenues.

On April 17th, 2026, Badger Meter reported first quarter earnings results for the period ending March 31st, 2026. For the quarter, revenue decreased 9.0% to $202.3 million, which was $29 million less than expected.

Earnings-per-share of $0.93 compared unfavorably to earnings-per-share of $1.30 in the prior year and was $0.26 below estimates.

The utility water business was down 10% for the quarter as a result of project timing and softer short-cycle municipal customer ordering.

Offsetting these weaker results were strength in SaaS, SmartCover, water quality and network monitoring.

Click here to download our most recent Sure Analysis report on BMI (preview of page 1 of 3 shown below):

Final Thoughts

Water could be one of the biggest investing themes over the next several decades. An increasing global population is only going to cause demand for water to rise in the future.

And, given the fact that water is a necessity of human life, demand for water should hold up extremely well, even during the worst recessions.

These factors make water stocks appealing for risk-averse investors looking for stability from their stock investments.

Additional Resources

It may be useful to browse through the following databases of dividend growth stocks:

- The Dividend Aristocrats List: S&P 500 stocks with 25+ years of dividend increases.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 58 stocks with 50+ years of consecutive dividend increases.

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.