Updated on February 25th, 2026 by Nathan Parsh

Investors looking for high-quality dividend growth stocks should focus, in part, on companies that maintain long histories of dividend increases.

Steady dividend raises from year to year, regardless of the economic climate, is a sign of a company with durable competitive advantages and long-term growth potential.

With that in mind, every year, we review each of the Dividend Aristocrats, a group of 69 companies in the S&P 500 Index, with 25+ consecutive years of dividend increases.

You can download your copy of the Dividend Aristocrats list, including important metrics like dividend yields and price-to-earnings ratios, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

The next Dividend Aristocrat in the series is healthcare giant Medtronic (MDT).

Medtronic has an impressive history of dividend growth. The company has increased its dividend for 47 years in a row. With an approximately 2.9% yield, Medtronic is not exactly a high-yield stock. However, the stock’s yield is still higher than the average yield of the S&P 500.

And, Medtronic typically raises its dividend at a high rate each year, thanks to its strong earnings and leadership position within the medical devices industry.

These qualities make Medtronic an attractive dividend growth stock for long-term investors.

Business Overview

Medtronic was founded in 1949 as a medical equipment repair shop by Earl Bakken and his brother-in-law, Palmer Hermundslie. Today, Medtronic is one of the largest healthcare companies in the world.

Medtronic PLC is the largest manufacturer of biomedical devices and implantable technologies in the world. Medtronic currently has four operating segments: Cardiovascular, Neuroscience, Medical Surgical, and Diabetes.

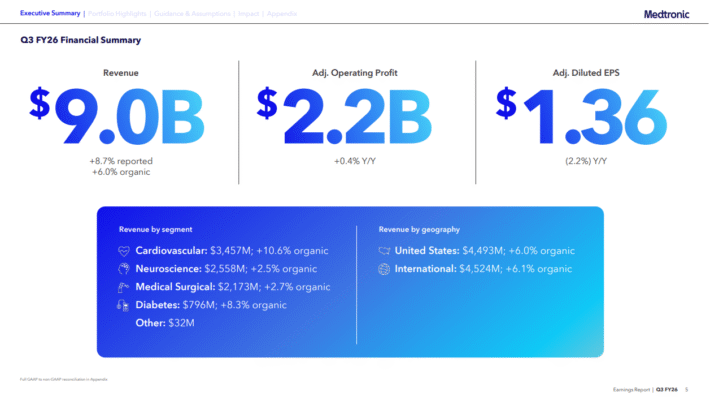

In February 17th, 2026,, Medtronic reported financial results for the third quarter of fiscal year 2026.

Source: Investor Presentation

The company reported solid Q3 FY26 results, surpassing expectations and reaffirming its full-year guidance. Revenue increased 8.7% to $9 billion, with adjusted earnings-per-share of $1.36. Organic growth grew 6% for the quarter, driven by strong results in Cardiovascular and Diabetes. Due to increased selling and administrative expenses, earnings-per-share was lower by $0.03. However, the company did beat expectations on both the top- and bottom-lines.

Additionally, Medtronic reiterated its guidance for 5.5% growth organic revenue and earnings-per-share of $5.62-$5.66 in fiscal 2026. We continue to expect earnings-per-share of $5.64 in fiscal 2026. It should be noted that Medtronic has beaten the analysts’ estimates in 28 of the last 31 quarters, demonstrating the company’s ability to produce strong results on a very regular basis.

With a robust pipeline and presence in high-impact markets, Medtronic expects continued expansion in patient care and market leadership. The company’s diversified growth strategy positions it well for sustained success.

Growth Prospects

Medtronic is investing in growth, both organically via R&D and through acquisitions. The first catalyst for Medtronic is the aging population. There are ~70 million Baby Boomers in the U.S., those aged 51-69 years. Thousands of people are entering retirement every day. Combined with longer life expectancy and rising healthcare spending, the operating environment is very attractive for Medtronic.

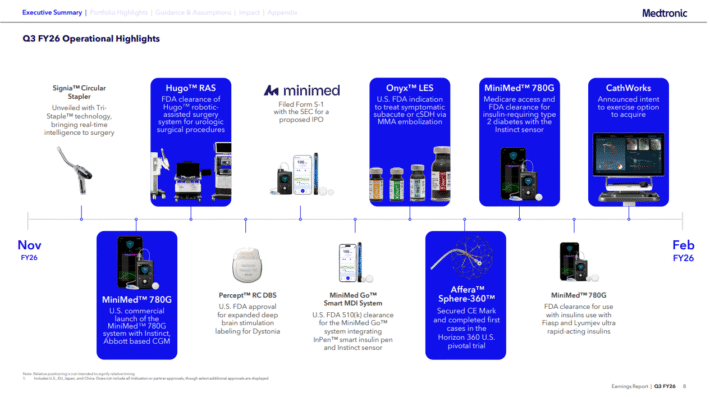

The company has had many regulatory product approvals in the past year. The new products should drive growth, allowing the company to maintain or gain market share.

Source: Investor Presentation

Medtronic also has a major growth opportunity in new geographic markets. Specifically, Medtronic has a presence in several emerging markets, such as China, India, Africa, and more. These countries have large populations and high economic growth rates.

Medtronic’s emerging market revenue has consistently grown double-digit for many years. While the U.S. currently accounts for just over half of Medtronic’s revenue, emerging markets are growing faster.

Medtronic is acquiring tuck-in acquisitions and has spent more than $3.3 billion on nine acquisitions since 2021. These companies include Acutus Medical, Medicrea, RIST, Avenu Medical, Companion Medical, Sonarmed, intersect ENT, AFFERA, and AI Biomed.

Overall, we expect Medtronic to grow its earnings-per-share by 6.0% per year on average until 2031.

Competitive Advantages & Recession Performance

The main competitive advantage for Medtronic is its research and development capabilities. The company spends heavily on R&D each year, which provides it with product innovation. Medtronic’s R&D investments over the past few years exceed $2 billion each year.

The result of all this spending is that the company has a huge intellectual property portfolio with nearly 86,000 awarded patents. This fact has allowed Medtronic to build a strong product pipeline across each of its business segments.

In addition, Medtronic benefits tremendously from its global scale. The company operates in over 140 countries around the world. It has the operational flexibility to generate industry-leading profit margins, which helps fuel its growth.

Another competitive advantage for Medtronic is that it operates in a defensive industry. Consumers often cannot forego medical treatments, even when the economy is in recession.

Medtronic’s earnings-per-share during the Great Recession are as follows:

- 2007 earnings-per-share of $2.61

- 2008 earnings-per-share of $2.92 (12% increase)

- 2009 earnings-per-share of $3.22 (10% increase)

- 2010 earnings-per-share of $3.37 (5% increase)

Medtronic had the rare achievement of earnings growth each year during the recession. The company also showed remarkable strength during the pandemic. This demonstrates its recession-resistant business model.

Medtronic should be able to continue growing its dividend each year in both economic recessions and expansions.

Valuation & Expected Returns

Based on the recent share price of ~$97 and expected earnings-per-share of $5.64 in fiscal 2026, Medtronic stock trades for a price-to-earnings ratio of 17.2. The stock’s current valuation is below that of the broader S&P 500 Index and modestly above its long-term average.

In the last decade, shares of Medtronic have traded hands at an average price-to-earnings ratio of 17.0. We believe that this is a fair valuation baseline.

As a result, Medtronic shares appear to be slightly overvalued today. If the stock valuation expands to our fair value estimate by 2031, the corresponding multiple compression will decrease shareholder returns by approximately 0.2% per year over this period.

Offsetting this small headwind is our expectation for 6% annual earnings growth through 2031, and the stock’s 2.9% dividend yield.

Total returns would consist of the following:

- 6.0% earnings growth rate

- 0.2% multiple compression

- 2.9% dividend yield

Medtronic is expected to return 8.3% annually over the next five years. This is an attractive potential rate of return, but below our threshold to warrant a buy rating. Despite a strong dividend risk score, we rate the stock as a hold due to projected returns.

As far as the dividend is concerned, there appears to be plenty of room for continued raises each year. With a dividend payout ratio of just over 50%, and a positive earnings growth outlook, Medtronic should continue its streak of annual dividend increases.

Final Thoughts

Medtronic has virtually all of the qualities dividend growth investors should look for. It possesses a highly profitable business, a leadership position in its core markets, and long-term growth potential. It also has multiple catalysts for future growth and the ability to keep growing its dividend even during recessions.

Medtronic has increased its dividend for more than four decades, which is highly impressive given the continued headwinds from a tough macroeconomic environment.

Medtronic stock appears to be offering a compelling investment opportunity for long-term dividend growth investors. However, we rate shares as a hold due to projected returns.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.