Updated on March 26th, 2026 by Bob Ciura

The “Dogs of the Dow” investing strategy is a very simple way for investors to achieve diversification and income in their portfolios while remaining in the sphere of more conservative blue chip stocks.

The strategy consists of investing in the 10 highest-yielding stocks in the Dow Jones Industrial Average, an index of 30 U.S. stocks.

High dividend stocks are stocks with a dividend yield well in excess of the market average dividend yield of ~1.3%.

With that in mind, we have created a free list of over 200 high dividend stocks with dividend yields above 4%.

You can download your copy of the high dividend stocks list below:

The “Dogs of the Dow” strategy produces above-average income and concentrates on stocks that typically trade at lower valuations relative to the rest of the DJIA.

Given that the DJIA represents some of the largest companies in the world, its “dogs” are typically companies with strong track records that have hit temporary problems.

This is a great and simple strategy for value investors looking to purchase good businesses that are currently out of favor. To implement this strategy, take the amount of money you have to invest and then divide it equally among the 10 highest-yielding stocks in the DJIA.

Hold these stocks for a whole year and then at the end of 12 months, look at the 30 Dow stocks again and resort them by dividend yield from highest to lowest.

Rebalance and reallocate your capital accordingly and repeat the process. In addition to the simplicity and focus on quality, value, and income that this strategy generates, it also improves discipline by preventing excessive emotion-driven trading.

It also encourages investors to reap the tax benefits from holding positions for at least one year before selling, thereby being taxed at the long-term capital gains tax rate instead of the short-term rate.

2026 Dogs of the Dow

The current list of the 2026 Dogs of the Dow is below, along with the current dividend yield of the top-ten yielding DJIA stocks.

Click on a company’s name to jump directly to analysis on that company.

- Dog of the Dow #10: Merck & Company (MRK)

- Dog of the Dow #9: International Business Machines (IBM)

- Dog of the Dow #8: The Home Depot (HD)

- Dog of the Dow #7: Coca-Cola (KO)

- Dog of the Dow #6: Amgen Inc. (AMGN)

- Dog of the Dow #5: Nike Inc. (NKE)

- Dog of the Dow #4: Procter & Gamble (PG)

- Dog of the Dow #3: UnitedHealth Group (UNH)

- Dog of the Dow #2: Chevron Corporation (CVX)

- Dog of the Dow #1: Verizon Communications (VZ)

- Final Thoughts

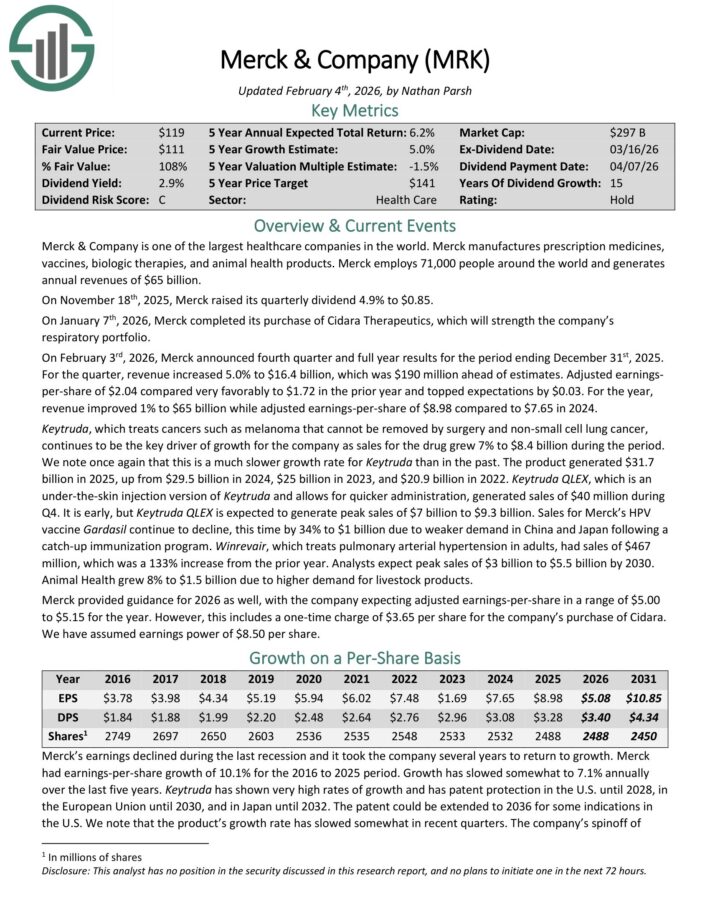

Dog of the Dow #10: Merck & Company (MRK)

- Dividend Yield: 2.7%

Merck & Company is one of the largest healthcare companies in the world. Merck manufactures prescription medicines, vaccines, biologic therapies, and animal health products.

Merck employs 68,000 people around the world and generates annual revenues of $65 billion.

On February 3rd, 2026, Merck announced fourth quarter and full year results. For the quarter, revenue increased 5.0% to $16.4 billion, which was $190 million ahead of estimates.

Adjusted earnings-per-share of $2.04 compared very favorably to $1.72 in the prior year and topped expectations by $0.03. For the year, revenue improved 1% to $65 billion while adjusted earnings-per-share of $8.98 compared to $7.65 in 2024.

Keytruda, which treats cancers such as melanoma that cannot be removed by surgery and non-small cell lung cancer, continues to be the key driver of growth for the company as sales for the drug grew 7% to $8.4 billion during the period.

Winrevair, which treats pulmonary arterial hypertension in adults, had sales of $467 million, which was a 133% increase from the prior year. Analysts expect peak sales of $3 billion to $5.5 billion by 2030.

Animal Health grew 8% to $1.5 billion due to higher demand for livestock products.

Merck provided guidance for 2026 as well, with the company expecting adjusted earnings-per-share in a range of $5.00 to $5.15 for the year.

However, this includes a one-time charge of $3.65 per share for the company’s purchase of Cidara.

Click here to download our most recent Sure Analysis report on MRK (preview of page 1 of 3 shown below):

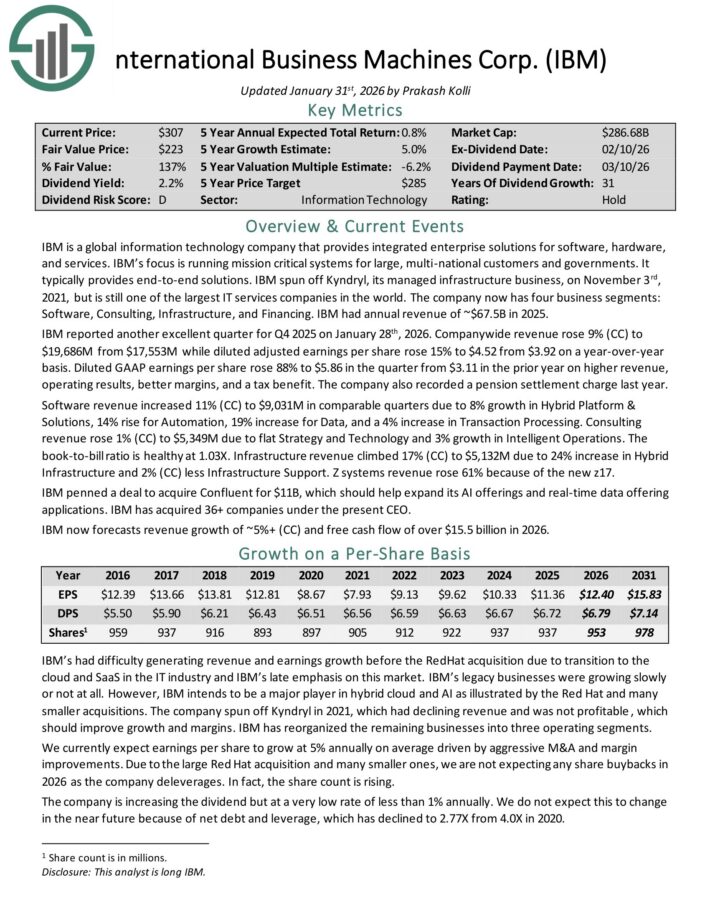

Dog of the Dow #9: International Business Machines (IBM)

- Dividend Yield: 2.8%

IBM is a global information technology company that provides integrated enterprise solutions for software, hardware, and services.

IBM’s focus is running mission critical systems for large, multi-national customers and governments. It typically provides end-to-end solutions. IBM had annual revenue of ~$67.5B in 2024.

IBM reported another excellent quarter for Q4 2025 on January 28th, 2026. Company-wide revenue rose 9% while diluted adjusted earnings per share rose 15% to $4.52 on a year-over-year basis.

Diluted GAAP earnings per share rose 88% to $5.86 in the quarter from $3.11 in the prior year on higher revenue, operating results, better margins, and a tax benefit.

Software revenue increased 11% (constant currency) due to 8% growth in Hybrid Platform & Solutions, 14% rise for Automation, 19% increase for Data, and a 4% increase in Transaction Processing.

The book-to-bill ratio is healthy at 1.03X.

IBM penned a deal to acquire Confluent for $11B, which should help expand its AI offerings and real-time data offering applications.

IBM now forecasts revenue growth of ~5%+ (CC) and free cash flow of over $15.5 billion in 2026.

Click here to download our most recent Sure Analysis report on IBM (preview of page 1 of 3 shown below):

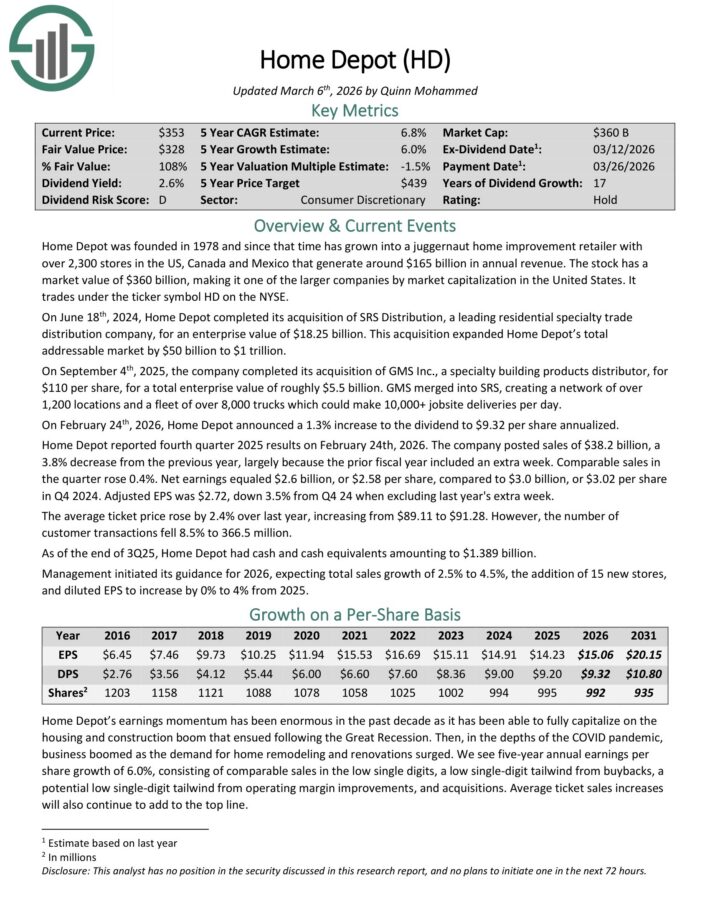

Dog of the Dow #8: The Home Depot (HD)

- Dividend Yield: 2.8%

Home Depot was founded in 1978 and since that time has grown into a juggernaut home improvement retailer with

over 2,300 stores in the US, Canada and Mexico that generate around $165 billion in annual revenue.

On February 24th, 2026, Home Depot announced a 1.3% increase to the dividend to $9.32 per share annualized.

Home Depot reported fourth quarter 2025 results on February 24th, 2026. The company posted sales of $38.2 billion, a 3.8% decrease from the previous year, largely because the prior fiscal year included an extra week.

Comparable sales in the quarter rose 0.4%. Net earnings equaled $2.6 billion, or $2.58 per share, compared to $3.0 billion, or $3.02 per share in Q4 2024.

Adjusted EPS was $2.72, down 3.5% from Q4 24 when excluding last year’s extra week.

The average ticket price rose by 2.4% over last year, increasing from $89.11 to $91.28. However, the number of customer transactions fell 8.5% to 366.5 million.

As of the end of 3Q25, Home Depot had cash and cash equivalents amounting to $1.389 billion.

Management initiated its guidance for 2026, expecting total sales growth of 2.5% to 4.5%, the addition of 15 new stores, and diluted EPS to increase by 0% to 4% from 2025

Click here to download our most recent Sure Analysis report on Home Depot (preview of page 1 of 3 shown below):

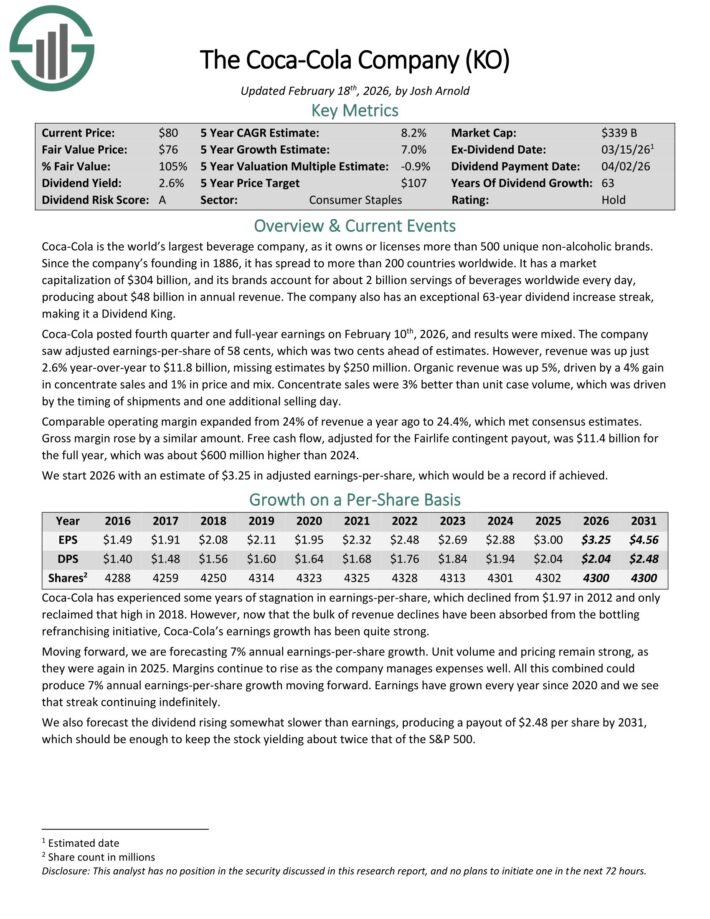

Dog of the Dow #7: Coca-Cola (KO)

- Dividend Yield: 2.8%

Coca-Cola is the world’s largest beverage company, as it owns or licenses more than 500 unique non-alcoholic brands.

Since the company’s founding in 1886, it has spread to more than 200 countries worldwide. Its brands account for about 2 billion servings of beverages worldwide every day, producing about $48 billion in annual revenue.

The company also has an exceptional 63-year dividend increase streak, making it a Dividend King.

Coca-Cola posted fourth quarter and full-year earnings on February 10th, 2026, and results were mixed. The company saw adjusted earnings-per-share of 58 cents, which was two cents ahead of estimates.

However, revenue was up just 2.6% year-over-year to $11.8 billion, missing estimates by $250 million. Organic revenue was up 5%, driven by a 4% gain in concentrate sales and 1% in price and mix.

Concentrate sales were 3% better than unit case volume, which was driven by the timing of shipments and one additional selling day.

Comparable operating margin expanded from 24% of revenue a year ago to 24.4%, which met consensus estimates. Gross margin rose by a similar amount.

Free cash flow, adjusted for the Fairlife contingent payout, was $11.4 billion for the full year, which was about $600 million higher than 2024.

Click here to download our most recent Sure Analysis report on KO (preview of page 1 of 3 shown below):

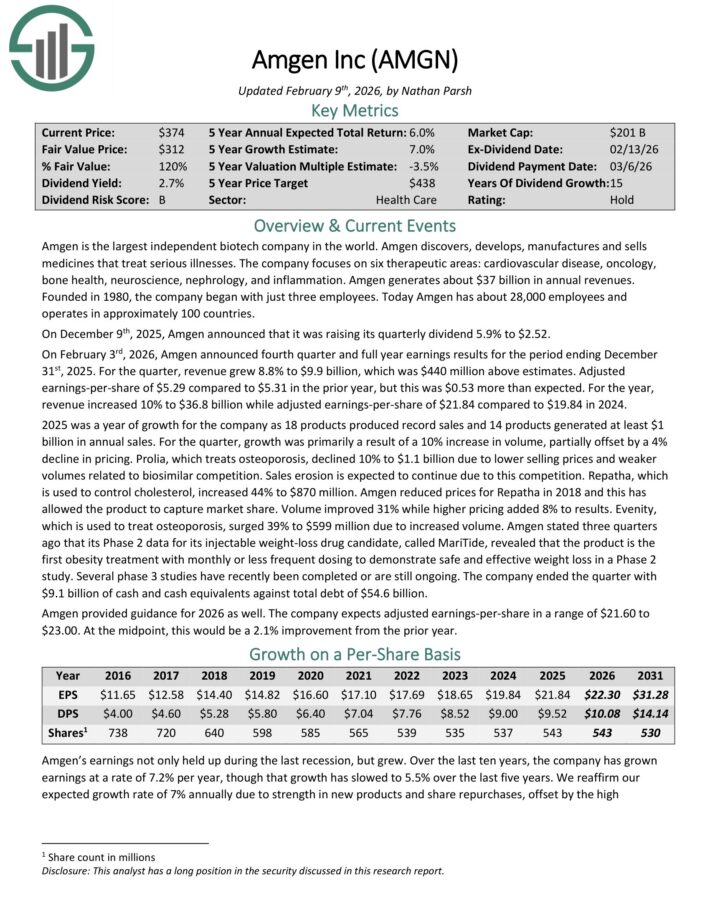

Dog of the Dow #6: Amgen Inc. (AMGN)

- Dividend Yield: 2.9%

Amgen is the largest independent biotech company in the world. Amgen discovers, develops, manufactures, and sells medicines that treat serious illnesses.

The company focuses on six therapeutic areas: cardiovascular disease, oncology, bone health, neuroscience, nephrology, and inflammation.

On December 9th, 2025, Amgen raised its quarterly dividend 5.9% to $2.52.

On February 3rd, 2026, Amgen announced fourth quarter and full year earnings results. For the quarter, revenue grew 8.8% to $9.9 billion, which was $440 million above estimates.

Adjusted earnings-per-share of $5.29 compared to $5.31 in the prior year, but this was $0.53 more than expected.

For the year, revenue increased 10% to $36.8 billion while adjusted earnings-per-share of $21.84 compared to $19.84 in 2024.

In 2025, 18 products produced record sales and 14 products generated at least $1 billion in annual sales. For the quarter, growth was primarily a result of a 10% increase in volume, partially offset by a 4% decline in pricing.

Amgen provided guidance for 2026 as well. The company expects adjusted earnings-per-share in a range of $21.60 to $23.00. At the midpoint, this would be a 2.1% improvement from the prior year.

Click here to download our most recent Sure Analysis report on Amgen Inc. (AMGN) (preview of page 1 of 3 shown below):

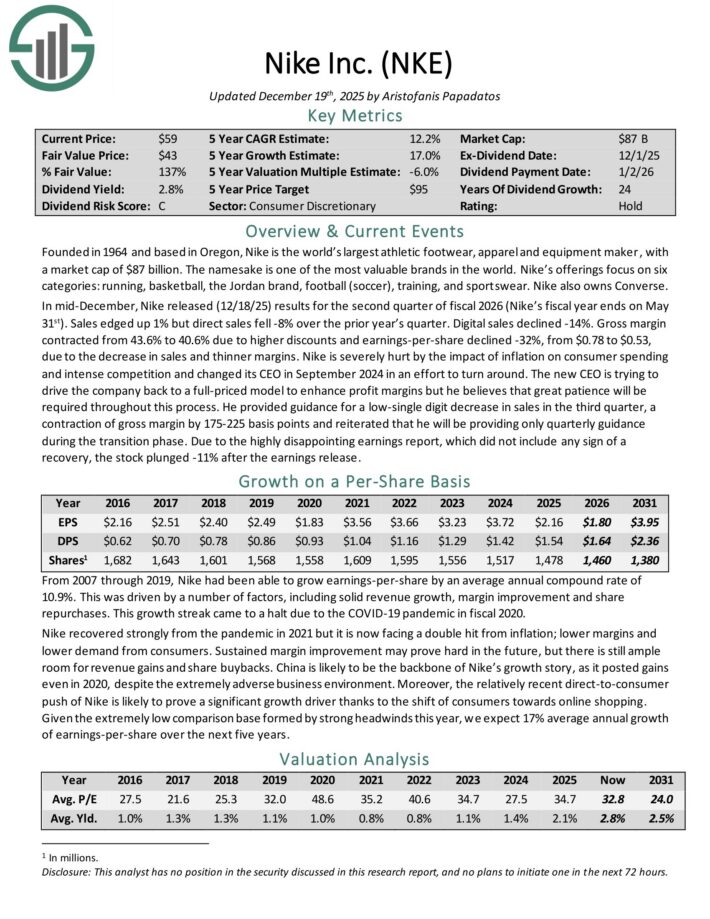

Dog of the Dow #5: Nike Inc. (NKE)

- Dividend Yield: 2.9%

Nike is the world’s largest athletic footwear, apparel and equipment maker. The namesake is one of the most valuable brands in the world.

Nike’s offerings focus on six categories: running, basketball, the Jordan brand, football (soccer), training, and sportswear. Nike also owns Converse.

In mid-December, Nike released (12/18/25) results for the second quarter of fiscal 2026 (Nike’s fiscal year ends on May 31st).

Sales edged up 1% but direct sales fell -8% over the prior year’s quarter. Digital sales declined -14%.

Gross margin contracted from 43.6% to 40.6% due to higher discounts and earnings-per-share declined -32%, from $0.78 to $0.53, due to the decrease in sales and thinner margins.

Nike is severely hurt by the impact of inflation on consumer spending and intense competition and changed its CEO in September 2024 in an effort to turn around.

The new CEO is trying to drive the company back to a full-priced model to enhance profit margins but he believes that great patience will be required throughout this process.

He provided guidance for a low-single digit decrease in sales in the third quarter, a contraction of gross margin by 175-225 basis points and reiterated that he will be providing only quarterly guidance during the transition phase.

Click here to download our most recent Sure Analysis report on NKE (preview of page 1 of 3 shown below):

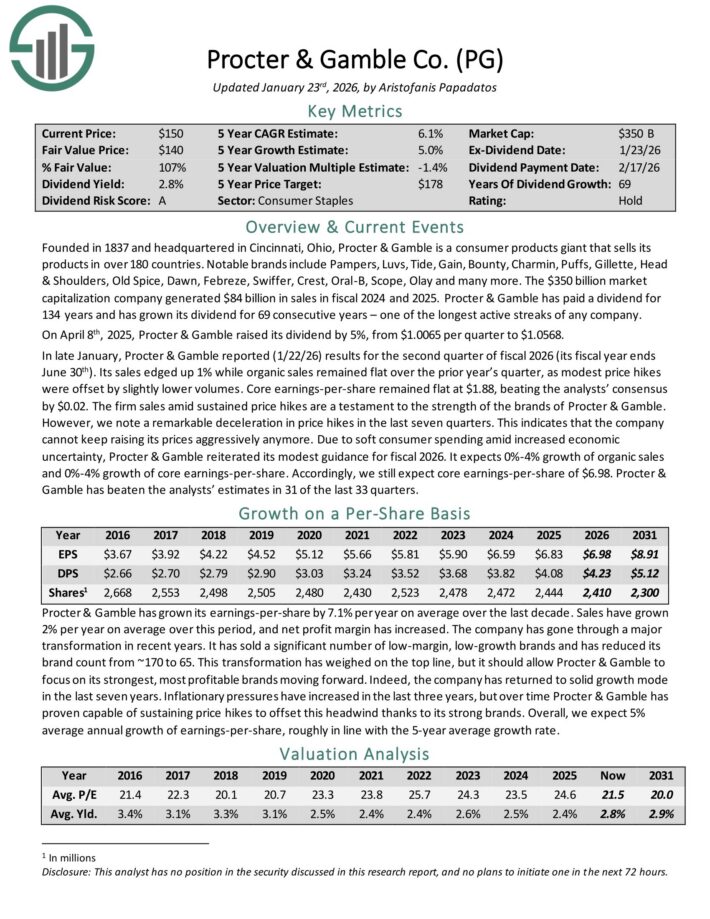

Dog of the Dow #4: Procter & Gamble (PG)

- Dividend Yield: 3.0%

Procter & Gamble is a consumer products giant that sells its products in over 180 countries.

Notable brands include Pampers, Luvs, Tide, Gain, Bounty, Charmin, Puffs, Gillette, Head & Shoulders, Old Spice, Dawn, Febreze, Swiffer, Crest, Oral-B, Scope, Olay and many more.

The company generated $84 billion in sales in fiscal 2024 and 2025. Procter & Gamble has paid a dividend for 134 years and has grown its dividend for 69 consecutive years – one of the longest active streaks of any company.

In late January, Procter & Gamble reported (1/22/26) results for the second quarter of fiscal 2026. Its sales edged up 1% while organic sales remained flat over the prior year’s quarter, as modest price hikes were offset by slightly lower volumes.

Core earnings-per-share remained flat at $1.88, beating the analysts’ consensus by $0.02. The firm sales amid sustained price hikes are a testament to the strength of the brands of Procter & Gamble.

However, we note a remarkable deceleration in price hikes in the last seven quarters. This indicates that the company cannot keep raising its prices aggressively anymore.

Due to soft consumer spending amid increased economic uncertainty, Procter & Gamble reiterated its modest guidance for fiscal 2026. It expects 0%-4% growth of organic sales and 0%-4% growth of core earnings-per-share.

Click here to download our most recent Sure Analysis report on PG (preview of page 1 of 3 shown below):

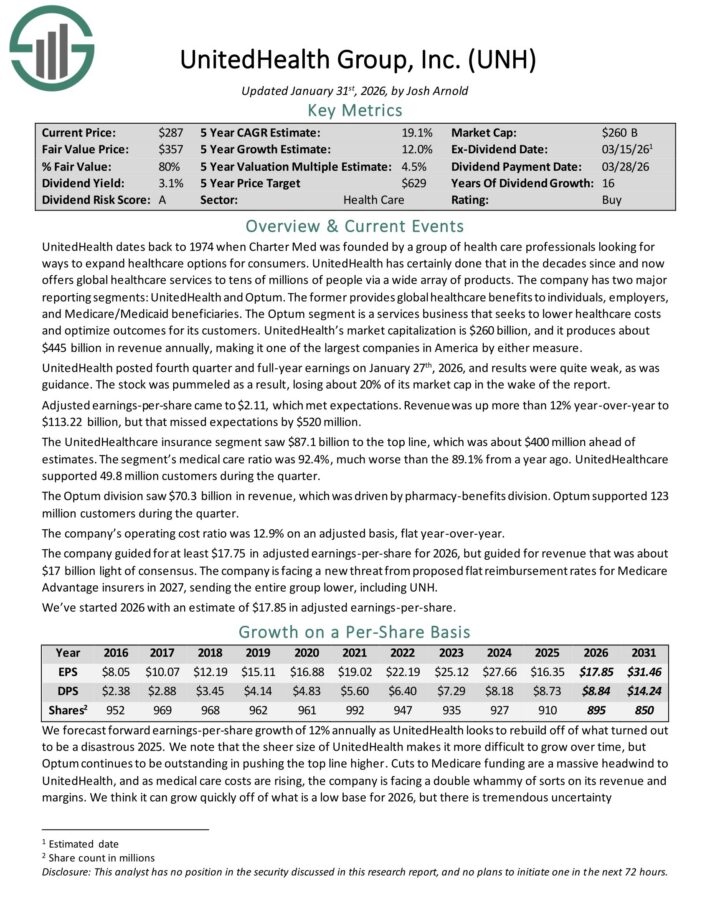

Dog of the Dow #3: UnitedHealth Group (UNH)

- Dividend Yield: 3.3%

UnitedHealth offers global healthcare services to tens of millions of people via a wide array of products. The company has two major reporting segments: UnitedHealth and Optum.

It provides global healthcare benefits to individuals, employers, and Medicare/Medicaid beneficiaries. The Optum segment is a services business that seeks to lower healthcare costs and optimize outcomes for its customers.

UnitedHealth posted fourth quarter and full-year earnings on January 27th, 2026. Adjusted earnings-per-share came to $2.11, which met expectations. Revenue was up more than 12% year-over-year to $113.22 billion, but that missed expectations by $520 million.

The UnitedHealthcare insurance segment saw $87.1 billion to the top line, which was about $400 million ahead of estimates.

The segment’s medical care ratio was 92.4%, much worse than the 89.1% from a year ago. UnitedHealthcare supported 49.8 million customers during the quarter.

The Optum division saw $70.3 billion in revenue, which was driven by pharmacy-benefits division. Optum supported 123 million customers during the quarter. The company’s operating cost ratio was 12.9% on an adjusted basis, flat year-over-year.

The company guided for at least $17.75 in adjusted earnings-per-share for 2026, but guided for revenue that was about $17 billion light of consensus.

Click here to download our most recent Sure Analysis report on UNH (preview of page 1 of 3 shown below):

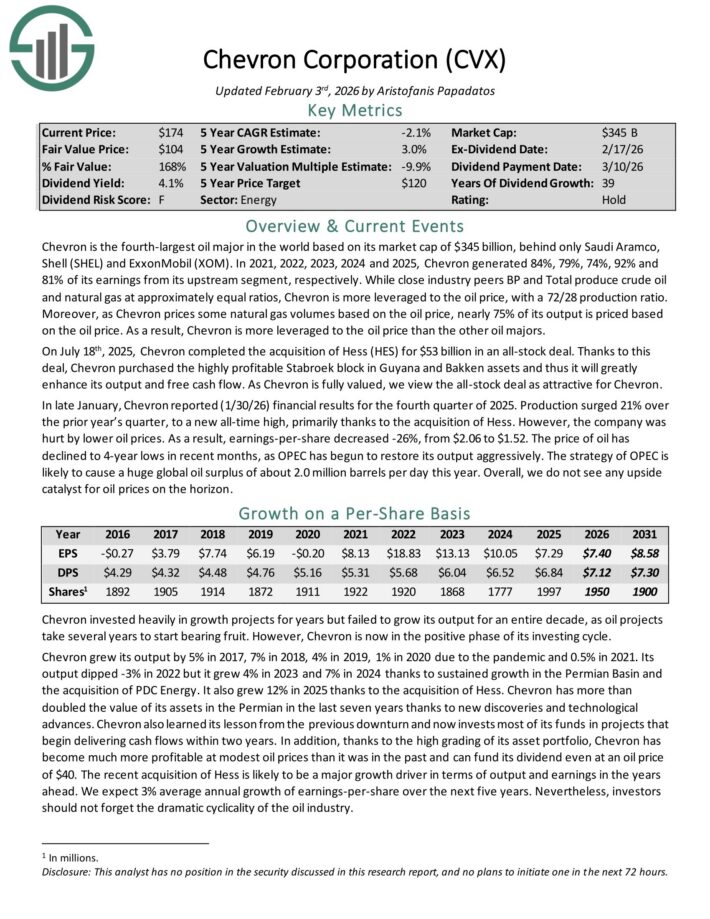

Dog of the Dow #2: Chevron Corporation (CVX)

- Dividend Yield: 3.4%

Chevron is the fourth-largest oil major in the world based on its market cap of $378 billion, behind only Saudi Aramco, Shell (SHEL) and ExxonMobil (XOM). In 2025, Chevron generated 81% of its earnings from its upstream segment.

In late January, Chevron reported (1/30/26) financial results for the fourth quarter of 2025. Production surged 21% over the prior year’s quarter, to a new all-time high, primarily thanks to the acquisition of Hess.

However, the company was hurt by lower oil prices. As a result, earnings-per-share decreased -26%, from $2.06 to $1.52.

Chevron grew 4% in 2023 and 7% in 2024 thanks to sustained growth in the Permian Basin and the acquisition of PDC Energy. It also grew 12% in 2025 thanks to the acquisition of Hess.

Chevron has more than doubled the value of its assets in the Permian in the last seven years thanks to new discoveries and technological advances.

Chevron is a member of the exclusive Dividend Aristocrats list thanks to its 39 consecutive years of dividend increases.

Click here to download our most recent Sure Analysis report on Chevron Corporation (CVX) (preview of page 1 of 3 shown below):

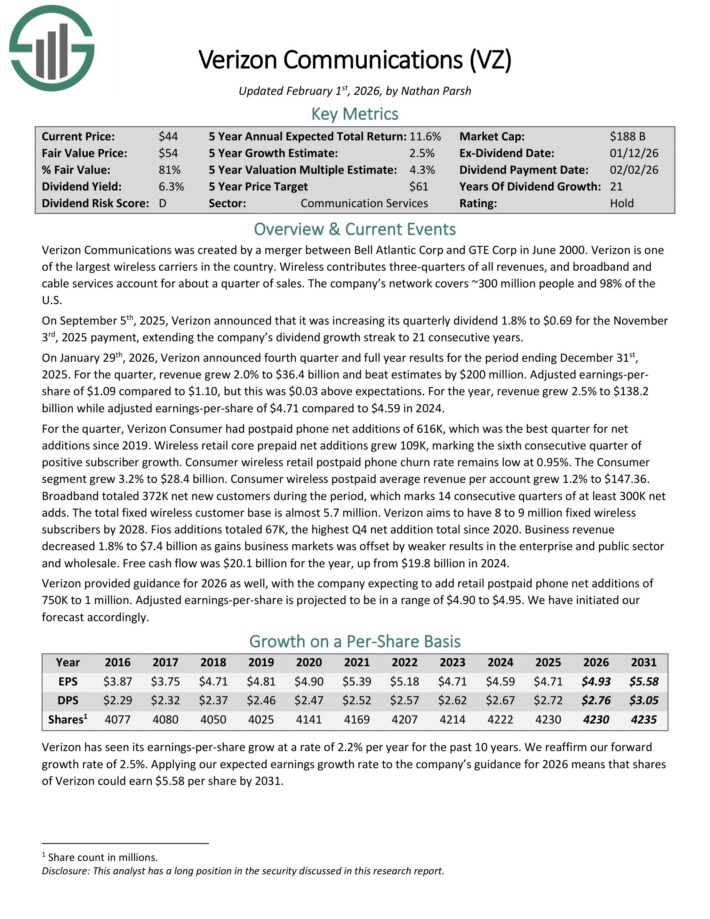

Dog of the Dow #1: Verizon Communications (VZ)

- Dividend Yield: 5.5%

Verizon Communications is one of the largest wireless carriers in the country. Wireless contributes three-quarters of all revenues, and broadband and cable services account for about a quarter of sales. The company’s network covers ~300 million people and 98% of the U.S.

On September 5th, 2025, Verizon increased its quarterly dividend 1.8% to $0.69 for the November 3rd, 2025 payment, extending the company’s dividend growth streak to 21 consecutive years.

On January 29th, 2026, Verizon announced fourth quarter and full year results. For the quarter, revenue grew 2.0% to $36.4 billion and beat estimates by $200 million.

Adjusted earnings-per-share of $1.09 compared to $1.10, but this was $0.03 above expectations. For the year, revenue grew 2.5% to $138.2 billion while adjusted earnings-per-share of $4.71 compared to $4.59 in 2024.

For the quarter, Verizon Consumer had postpaid phone net additions of 616K, which was the best quarter for net additions since 2019.

Wireless retail core prepaid net additions grew 109K, marking the sixth consecutive quarter of positive subscriber growth.

Click here to download our most recent Sure Analysis report on VZ (preview of page 1 of 3 shown below):

Final Thoughts

Given the descriptions above, the Dogs of the Dow are clearly a very diverse group of blue-chip stocks that each enjoy significant competitive advantages and lengthy histories of paying rising dividends.

As a result, this investing strategy is a good way for unsophisticated investors to approach dividend growth investing.

While it may not outperform the broader market every year, it is virtually guaranteed to provide investors with a combination of attractive current yield with steadily rising income over time.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

- 20 Highest Yielding Dividend Kings

- 20 Undervalued High-Dividend Stocks

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Super High Dividend REITs

- Highest Yielding Royalty Trusts

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Monthly Dividend Stocks: Individual securities that pay out every month

- Blue Chip Stocks: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more