Published on October 20th, 2025 by Felix Martinez

High-yield stocks pay out dividends that are significantly more than the market average dividends. For example, the S&P 500’s current yield is only ~1.2%.

High-yield stocks can be very helpful to shore up income after retirement.

PennantPark Floating Rate (PFLT) is part of our ‘High Dividend 50’ series, which covers the 50 highest-yielding stocks in the Sure Analysis Research Database.

We have created a spreadsheet of stocks (and closely related REITs and MLPs, etc.) with dividend yields of 4% or more…

You can download your free full list of all securities with 4%+ yields (along with important financial metrics such as dividend yield and payout ratio) by clicking on the link below:

Next on our list of high-dividend stocks to review is PennantPark Floating Rate (PFLT)

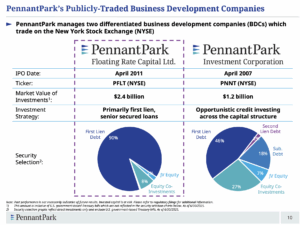

Business Overview

Growth Prospects

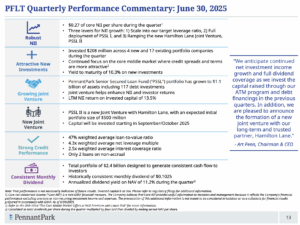

PennantPark has a track record of successful investments. However, its exposure to floating-rate instruments has caused its average portfolio yield to fall over the past several years. The yield on PennantPark’s portfolio peaked at just over 9% at the end of 2018, but the company faced declines in the subsequent years.

As PennantPark’s portfolio is comprised of floating rate instruments – mostly tied to LIBOR – it benefits when interest rates increase. Low rates over the past decade suppressed the company’s investment income, but the potential for higher rates is a future catalyst.

Competitive Advantages & Recession Performance

PennantPark focuses on first-lien, middle-market loans, giving it priority in repayments and higher yields. Its experienced management, strong deal-sourcing network, and partnerships like the joint venture with Hamilton Lane enable efficient portfolio growth. High exposure to variable-rate debt also allows the company to benefit from rising interest rates, supporting income and dividends.

The company has shown resilience in moderate downturns, but high leverage and a near-100% payout ratio make it vulnerable in severe recessions. Non-accrual loans remain low, yet prolonged economic stress or falling rates could pressure income and dividends. Investors should monitor credit quality and market conditions closely.

Dividend Analysis

PennantPark pays a monthly dividend of $0.1025 per share, translating to an attractive annualized yield of ~14%. Its monthly distribution schedule is a bonus for investors seeking more frequent income.

However, such a high yield warrants scrutiny. While BDCs typically offer elevated yields, PennantPark’s 14% payout is high even by industry standards. The company carries a highly leveraged balance sheet, and its payout ratio often approaches or exceeds 100% of earnings. This model has been sustainable in stable economic conditions, but a prolonged downturn or underperforming loans could threaten the dividend.

Currently, PennantPark’s net investment income (NII) is expected to cover distributions, with a projected payout ratio of 93%. While a dividend cut is not anticipated, any deterioration in credit quality or a drop in interest rates could pressure earnings and make a reduction possible. Investors should recognize that the dividend is not immediately at risk but should be monitored closely, especially given the company’s reliance on floating-rate instruments and high leverage.

Final Thoughts

The old adage “high-risk, high-reward” fits PennantPark well. Its dividend yield is compelling, but a decline in interest rates could put future payouts at risk.

If operations proceed smoothly, the yield alone could deliver nearly double-digit annual returns. However, the company carries significant risk—if investment income growth falters, a dividend reduction may become necessary, though we do not currently expect this.

Investors should proceed with caution. PennantPark is best suited for those with a higher risk tolerance who are comfortable prioritizing yield despite potential volatility.

High-Yield Individual Security Research

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Super High Dividend REITs

- 5 Highest Yielding Royalty Trusts

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 5%+ dividend yields

- Monthly Dividend Stocks: Individual securities that pay out every month

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more