Published on March 1st, 2023 by Aristofanis Papadatos

Semiconductor stocks are a major part of the broader tech sector. Chips are manufactured for use in many of the devices we can’t do without, such as computers and smartphones.

Demand for these devices is robust and is not likely to slow any time soon. As a result, the top semiconductor manufacturers are highly profitable. Many of them return excess cash to shareholders through dividends and share repurchases.

Semiconductor stocks could provide attractive future returns. With this in mind, we created a list of 50+ semiconductor stocks.

You can download a copy of the 2023 semiconductor stocks list (along with important financial metrics such as dividend yields and P/E ratios) by clicking on the link below:

This article will give an overview of the semiconductor industry, and the top 10 semiconductor stocks now.

Table of Contents

You can instantly jump to a specific section of the article by clicking on the links below:

- Industry Overview

- Semiconductor Stock #10: Texas Instruments (TXN)

- Semiconductor Stock #9: Lam Research Corp. (LRCX)

- Semiconductor Stock #8: Skyworks Solutions (SWKS)

- Semiconductor Stock #7: Broadcom Inc. (AVGO)

- Semiconductor Stock #6: Monolithic Power Systems (MPWR)

- Semiconductor Stock #5: KLA Corp. (KLAC)

- Semiconductor Stock #4: Microchip Technologies (MCHP)

- Semiconductor Stock #3: Qualcomm Inc. (QCOM)

- Semiconductor Stock #2: Taiwan Semiconductor Manufacturing (TSM)

- Semiconductor Stock #1: ASML Holding NV (ASML)

- Final Thoughts

Industry Overview

A semiconductor is a material with an electrical conductivity value that is in-between conductors and insulators.

The investment case for semiconductors is fairly straightforward: they are a crucial component in manufacturing electronic devices, such as smartphones, tablets, and computers. But they are also used across a number of other industries such as healthcare, defense, communications, transportation, and more.

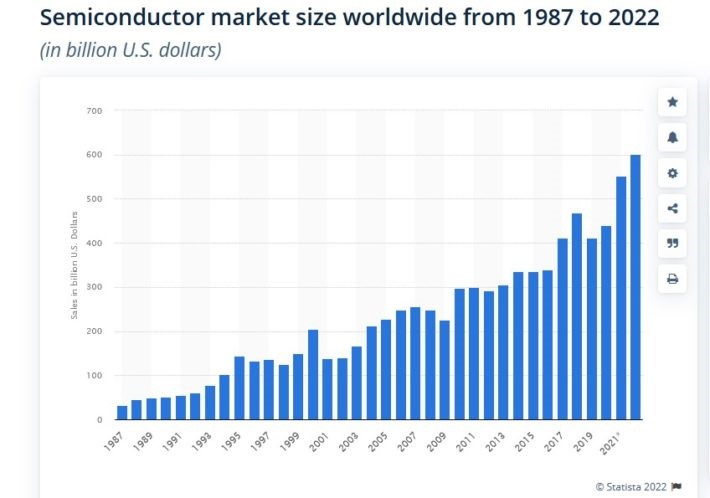

With such importance to our daily lives, it is no wonder the semiconductor industry has grown to its current size. In 2022, semiconductor sales reached an all-time high of $580 billion, up from sales of $556 billion in 2021. According to Statista, the global semiconductor market is expected to have sales around $556 billion in 2023.

Source: Statista

Looking at this kind of impressive growth, it is understandable for investors to be interested in the top semiconductor stocks.

The following section will discuss the top 10 semiconductor stocks today, ranked by expected annual returns according to the Sure Analysis Research Database.

Semiconductor Stock #10: Texas Instruments (TXN)

- 5-year expected annual returns: 6.7%

Texas Instruments is a semiconductor company that operates two business units: Analog and Embedded Processing. Its products include semiconductors that measure sound, temperature and other physical data and convert them to digital signals, as well as semiconductors that are designed to handle specific tasks and applications.

Texas Instruments reported its fourth quarter earnings results on January 24. During the quarter, Texas Instruments generated revenues of $4.7 billion, which represented a decline of 3% versus the previous year’s quarter. This beat analyst estimates by $40 million, as the analyst community had forecasted a weaker sales performance. Texas Instruments managed to keep its gross profit margin at an attractive level of 66%, while operating profit margin of 47% remained strong as well.

Texas Instruments generated earnings-per-share of $2.13 during the fourth quarter, which exceeded the consensus estimate by $0.15. Texas Instruments provided guidance for revenues of $4.4 billion and for earnings-per-share of around $1.77 in the first quarter of 2023. 2022 was a year during which the company hit new record profits, but it looks like the company will generate lower profits in 2023, on the back of the ongoing economic slowdown that hurts semiconductor companies and their profit potential.

Click here to download our most recent Sure Analysis report on TXN (preview of page 1 of 3 shown below):

Semiconductor Stock #9: Lam Research Corp. (LRCX)

- 5-year expected annual returns: 7.2%

Lam Research Corporation designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used to fabricate integrated circuits worldwide. Lam is a major supplier of wafer fabrication equipment and services to the semiconductor industry.

Its products address various applications, including thin film deposition, single–wafer cleaning, and plasma tech. The company has a market capitalization of $65 billion, over 10,700 employees, and produced $17 billion in revenue in 2022.

On January 25, 2023, Lam Research reported the second quarter results for Fiscal Year (FY) 2023, ending on December 25, 2022. Lam Research Corporation ends its fiscal year at the end of June. Revenue grew by over 24% compared to 2Q22, from $4.2 billion to $5.2 billion. Diluted earnings per share grew 27.6% year-over-year. Revenue by region shows that China and Korea represented 24% and 20% of total revenue, respectively. The next closest region is Taiwan, with 19%. The company earned $10.77 for the quarter, 27.6% higher than in the second quarter of the fiscal year 2022 and 3.7% higher than the previous quarter.

Click here to download our most recent Sure Analysis report on LRCX (preview of page 1 of 3 shown below):

Semiconductor Stock #8: Skyworks Solutions (SWKS)

- 5-year expected annual returns: 8.9%

Skyworks Solutions is a semiconductor company that designs, develops, and markets proprietary semiconductor

products used worldwide. Its products include antenna tuners, amplifiers, converters, modulators, receivers, and

switches.

Skyworks’ products are used in diverse industries, including automotive, connected home, industrial, medical, smartphones, and defense. The company traces its roots back to a merger in 2002, is headquartered in Woburn, Massachusetts, employs over 8,400 people, and has a market capitalization of $18 billion.

On February 6th, 2023, Skyworks reported first-quarter results for Fiscal Year (FY) 2023. The fiscal year of the company ends at the end of September. Revenue declined 11.9% to $1.3 billion over the prior year’s quarter, but it still exceeded consensus estimates by $10 million. Operating income decreased 18% and net income declined 23% year-over-year. On a per share basis, the company earned $1.93 per share for 1Q2023, which was 20% lower than in the prior year’s quarter.

Click here to download our most recent Sure Analysis report on SWKS (preview of page 1 of 3 shown below):

Semiconductor Stock #7: Broadcom Inc. (AVGO)

- 5-year expected annual returns: 9.4%

Broadcom designs, develops and sells semiconductors under the following business units: Wired infrastructure, wireless communication, enterprise storage and industrial. Its offerings include data center chips, factory automation, energy systems and power generation, broadband access, and home connectivity. Broadcom is a fabless semiconductor company, which means that the products it designs are manufactured by other companies (so–called foundries).

Broadcom reported its fourth quarter earnings results in December. The company generated revenues of $8.9 billion during the quarter, which represents an increase of 21% compared to the prior year’s quarter. The strong revenue growth performance was possible thanks to beating estimates in the semiconductor solutions unit, while its Infrastructure software business generated solid growth as well.

Broadcom reported earnings-per-share of $10.45 for the fourth quarter, which was ahead of the analyst consensus estimate. The company expects that revenues will come in at $8.9 billion during the first quarter of the current fiscal year, which would represent flat revenues versus the previous quarter. Broadcom’s proposed acquisition of VMWare is still pending and will likely take several more quarters to materialize.

Click here to download our most recent Sure Analysis report on AVGO (preview of page 1 of 3 shown below):

Semiconductor Stock #6: Monolithic Power Systems (MPWR)

- 5-year expected annual returns: 9.7%

Monolithic Power Systems is a leading semiconductor company that designs, develops, and markets high–performance power solutions.

The company utilizes its deep system–level and applications expertise to develop highly integrated monolithic systems used in computing and storage, automotive, industrial, communications, and consumer applications industries. Its mission is to reduce total energy consumption in its customers’ systems with green, practical, and compact solutions. Monolithic Power generates about $1.8 billion in annual revenues.

On February 8th, 2023, Monolithic Power reported its Q4 2022 and full-year results for the period ending December 31st, 2022. For the quarter, revenues grew by 36.7% year-over-year to $460 million, once again powered by Monolithic’s diversified growth strategy, technological innovation, investment in production capacity, and, importantly, broad-based market share gains.

Notably, Storage, and Computing revenues grew by 55% to $120.8 million, while Enterprise Data revenues jumped to $68.4 million, a gain of 69% versus the prior-year period. Following strong top-line growth, adjusted EPS skyrocketed by 49.5% to $3.17 compared to Q4 2021. For the year, adjusted EPS was $12.84, up 65% against FY2021.

As a result of excellent market dynamics, Monolithic expects Q1 revenues in the range of $440 million to $460 million, suggesting year-over-year growth of 19% at the midpoint of this outlook. Based on this estimate, the current market fundamentals, and Monolithic’s net income margin expansion trajectory, we expect FY2023 adjusted EPS of $13.00.

Click here to download our most recent Sure Analysis report on MPWR (preview of page 1 of 3 shown below):

Semiconductor Stock #5: KLA Corp. (KLAC)

- 5-year expected annual returns: 11.2%

KLA Corporation is a supplier to the semiconductor industry. The company supplies process control and yield management systems for semiconductor producers such as TSMC, Samsung and Micron. KLA was created in 1997, through a merger between KLA Instruments and Tencor Instruments, and has grown through a range of acquisitions since then.

KLA Corporation reported its first quarter (fiscal 2023) earnings results on October 26. The company reported revenues of $2.72 billion for the quarter, which represents an increase of 31% compared to the prior year’s quarter. This revenue growth rate was stronger than what the analyst community had expected, as KLA’s top line beat the analyst consensus by $120 million. KLA’s solid revenue performance can be explained by the fact that many semiconductor companies have increased their investments into manufacturing capacity thanks to ongoing healthy chip demand.

KLA generated earnings-per-share of $7.06 during its fiscal first quarter, which beat estimates by $0.83, and which was up by a hefty 52% compared to the previous year’s quarter. This follows strong earnings growth in recent quarters.

Click here to download our most recent Sure Analysis report on KLAC (preview of page 1 of 3 shown below):

Semiconductor Stock #4: Microchip Technologies (MCHP)

- 5-year expected annual returns: 13.0%

Microchip Technology develops, manufactures, and sells smart, connected and secure embedded control solutions used for a wide variety of applications. These include disruptive growth trends such as 5G, artificial intelligence, Internet of Things (IoT), and autonomous driving, amongst others, in key end markets such as automotive, aerospace and defense, communications.

The company’s strategic focus is that these solutions are cost–effective, offer high performance, with a wide voltage range operation, at extremely low power usage. Microchip Technology generates around $6 billion in annual revenues and is based in Chandler, Arizona.

On February 2nd, 2023, Microchip Technology raised its dividend by 9% and thus it has now raised its dividend for 22 consecutive years.

On the same day, Microchip Technology reported its Q3-2023 results for the quarter ending December 31st, 2022. Net sales were a record $2.17 billion, up 23.4% from the comparable period last year and 4.6% higher sequentially. Higher revenues were again powered by exceptional execution on delivering Microchip’s backlog and strong underlying demand, as well as improvements in the supply chain. Due to a higher production scale, GAAP gross margins reached a record of 67.8% for the quarter, leading to a record net income of $580.3 million or $1.04 per diluted share. On a non-GAAP basis, EPS was $1.56 versus $1.20 in Q3-2022.

Click here to download our most recent Sure Analysis report on MCHP (preview of page 1 of 3 shown below):

Semiconductor Stock #3: Qualcomm Inc. (QCOM)

- 5-year expected annual returns: 13.1%

“Quality Communications” was started in the living room of Dr. Irwin Jacobs in 1985. The company’s first product and service was a satellite used by long–haul trucking companies that could locate and message drivers. Qualcomm, as it is known today, develops and sells integrated circuits for use in voice and data communications. The chip maker receives royalty payments for its patents used in devices that are on 3G, 4G and 5G networks. Qualcomm has a current market capitalization of $139 billion and has annual sales of about $38 billion.

Qualcomm has raised its dividend for 20 consecutive years. On February 2nd, 2023, the company announced results for the first quarter of fiscal year 2023 for the period ending December 25th, 2022. Revenue decreased 11.6% to $9.46 billion, which missed estimates by $110 million. Adjusted earnings-per-share of $2.37 compared unfavorably to $3.23 in the previous year, but was $0.02 above expectations.

Guidance for the second quarter was set at a range of $2.05 to $2.25, which was below consensus estimates of $2.24. Qualcomm is now projected to earn $9.31 in fiscal year 2023, down from previous estimates of $10.23.

Click here to download our most recent Sure Analysis report on QCOM (preview of page 1 of 3 shown below):

Semiconductor Stock #2: Taiwan Semiconductor Manufacturing (TSM)

- 5-year expected annual returns: 13.8%

Taiwan Semiconductor Manufacturing is the world’s largest dedicated foundry for semiconductor components. The company is headquartered in Hsinchu, Taiwan. TSM has a market capitalization of US$432 billion.

In mid-January, Taiwan Semiconductor reported (1/12/23) financial results for the fourth quarter of fiscal 2022. Revenue grew 43% and earnings-per-share increased 78% over the prior year’s quarter thanks to sustained strength in the demand for 5-nanometer and 7-nanometer technology. The company posted excessive margins; gross margin of 62.2%, operating margin of 52.0% and net profit margin of 47.3%. Earnings-per-share exceeded the analysts’ consensus of $1.77 by $0.05. Taiwan Semiconductor has exceeded the analysts’ earnings-per-share estimates for 20 consecutive quarters.

Despite the all-time high earnings of the company amid strong demand for its chips in smartphones, vehicles and highperformance computing, the stock has plunged -37% in the last 12 months due to fears of an upcoming recession and a decrease in global demand for chips. We agree with the market’s fears for a slowdown but we expect global demand for chips to recover in late 2023 or 2024. The stock has bounced 40% off its bottom in November.

Click here to download our most recent Sure Analysis report on TSM (preview of page 1 of 3 shown below):

Semiconductor Stock #1: ASML Holding NV (ASML)

- 5-year expected annual returns: 16.4%

ASML Holding is one of the largest manufacturers of chip–making equipment in the world. The company’s customers include a wide variety of industries, and ASML is present in 16 countries with 30,000 employees. The company is headquartered in the Netherlands and is listed on both the Euronext Amsterdam and NASDAQ.

ASML has a current market capitalization of $241 billion and produces about $28 billion in annual revenue.

ASML reported fourth quarter and full-year earnings on January 25th, 2023, and results were better than expected on both the top and bottom lines. Earnings-per-share came to $5.00, which was 29 cents better than expected. In addition, revenue soared 29% year-over-year to nearly $7 billion, and was $54 million ahead of estimates. Quarterly net bookings in Q4 were $6.9 billion, about half of which was for the company’s proprietary EUV. Gross margin for the quarter was 51.5% of revenue.

Click here to download our most recent Sure Analysis report on ASML (preview of page 1 of 3 shown below):

Final Thoughts

Semiconductor stocks are risky, as their profits depend largely on the health of the broader economy. As always, investors should assess the individual risk factors before buying semiconductor stocks.

That said, many semiconductor stocks could generate strong returns, as the tech sector has promising growth prospects in the long run, despite its latest slowdown. Some of the major semiconductor stocks also pay strong dividends to shareholders, and raise their dividends each year.

Therefore, for investors willing to take the risk, the long-term potential of semiconductor stocks could be rewarding.

You may also be looking to invest in dividend growth stocks with high probabilities of continuing to raise their dividends each year into the future.

The following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Aristocrats:S&P 500 stocks with 25+ years of consecutive dividend increases.

- The Dividend Achievers:dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings:considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List:this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

Thanks for reading this article. Please send any feedback, corrections, or questions to support@suredividend.com.