Updated on April 13th, 2023 by Nikolaos Sismanis

The ‘holy grail’ of dividend growth investing is to find businesses that offer:

- Growth potential

- High dividend yields

- Consistent and safe operations

This blend of characteristics is difficult to find in the stock market. However, sudden hikes in interest rates lately have resulted in the share prices of many high-dividend stocks declining, boosting their yields. Hence, more stocks satisfy these criteria versus a couple of years ago when low rates persisted.

The trade-off between growth and dividends makes it difficult to find stocks with both a high payout ratio and solid growth prospects. The more a company pays out in dividends, the less it has to reinvest in growth.

Management must be very efficient with its capital allocation policies to have both a high dividend payout ratio and solid growth prospects. There is little room for error.

Finding businesses that consistently pay rising dividends and also have safe operations is difficult. Strong competitive advantages in the business world are rare.

For instance, there are currently only 68 Dividend Aristocrats. To be a Dividend Aristocrat, a company must:

- Be in the S&P 500

- Have 25+ consecutive years of dividend increases

- Meet certain minimum size & liquidity requirements

You can download an Excel spreadsheet of all 68 (with important financial metrics such as P/E ratios and dividend yields) by clicking the link below:

The list of Dividend Kings (50+ years of dividend increases) and the list of Dividend Achievers (10+ years of dividend increases) are also quite short, providing further evidence of the rarity of durable competitive advantages.

This article takes a look at quality dividend stocks with the following characteristics:

- Dividend yields above 4%

- At least 10+ consecutive years of dividend increases

- Dividend Risk Scores of ‘C’ or better

- Market capitalizations above $10 billion

Businesses with long dividend histories have proven the stability of their operations. This article analyzes 12 consistently high-paying dividend stocks, as ranked using expected total returns from the Sure Analysis Research Database.

Table of Contents

You can instantly jump to any specific section of the article by using the links below:

- Consistent High Yield Stock #12: Essex Property Trust Inc. (ESS)

- Consistent High Yield Stock #11: Verizon Communications (VZ)

- Consistent High Yield Stock #10: Walgreens Boots Alliance, Inc. (WBA)

- Consistent High Yield Stock #9: Magellan Midstream Partners, L.P. (MMP)

- Consistent High Yield Stock #8: Digital Realty Trust (DLR)

- Consistent High Yield Stock #7: Bank of Montreal (BMO)

- Consistent High Yield Stock #6: Brookfield Infrastructure Partners L.P. (BIP)

- Consistent High Yield Stock #5: Fifth Third Bancorp (FITB)

- Consistent High Yield Stock #4: Bank of Nova Scotia (BNS)

- Consistent High Yield Stock #3: Toronto-Dominion Bank (TD)

- Consistent High Yield Stock #2: 3M Company (MMM)

- Consistent High Yield Stock #1: Regions Financial (RF)

- Final Thoughts

Consistent High Yield Stock #12: Essex Property Trust Inc. (ESS)

- 5-year expected annual returns: 13.0%

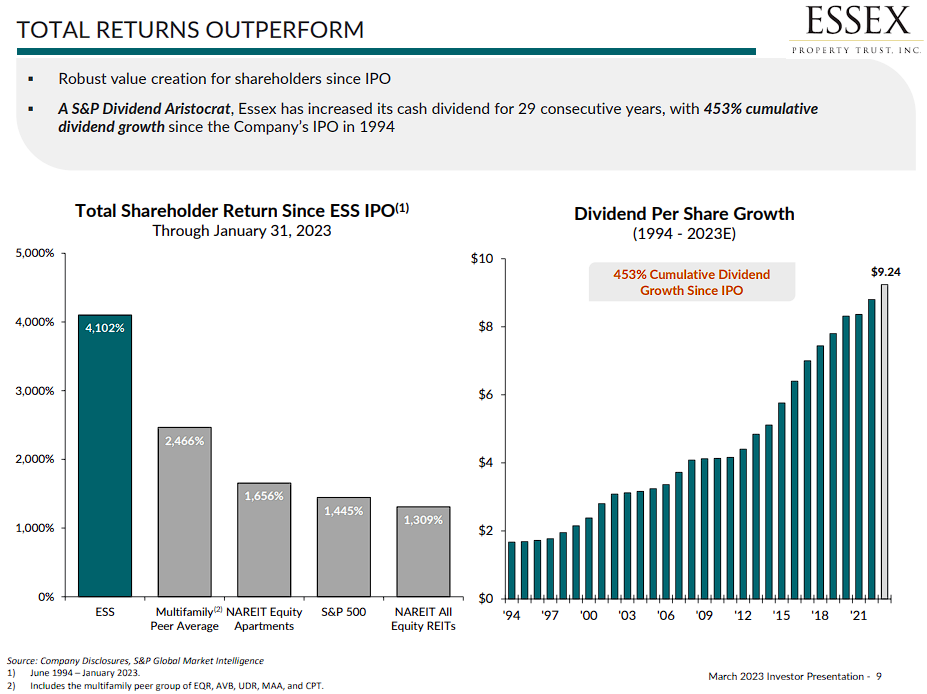

Essex Property Trust Inc. (ESS) was founded in 1971 and became a publicly traded real estate investment trust (REIT) in 1994. The trust invests in west coast multifamily residential proprieties where it engages in the development, redevelopment, management, and acquisition of apartment communities and a few other select properties. Essex has ownership interests in several hundred apartment communities consisting of over 60,000 apartment homes. The trust has about 1,800 employees and produces approximately $1.7 billion in annual revenue.

Essex Property Trust has been a strong outperformer in terms of total returns since it went public in 1994 due to a combination of good management and a tailwind from the fast-growing west coast property market on the back of a strong technology industry in the region.

Source: Investor Presentation

On February 7th, 2023, Essex announced its fourth quarter and full-year 2022 earnings results. Q4 FFO of $3.77 beat analyst estimates by $0.04. The trust achieved same-property revenue and net operating income growth of 10.5% and 13.3%, respectively, compared to the fourth quarter of 2021. As of February 6th, 2023, the Company had approximately $1.3 billion in liquidity via undrawn capacity on its unsecured credit facilities, cash, and marketable securities.

We expect annual returns of 13.0% for ESS stock, comprised of 4.4% FFO-per-share growth, a 4.4% dividend yield, and a 5.1% annual boost from an expanding P/FFO multiple.

Consistent High Yield Stock #11: Verizon Communications (VZ)

- 5-year expected annual returns: 13.1%

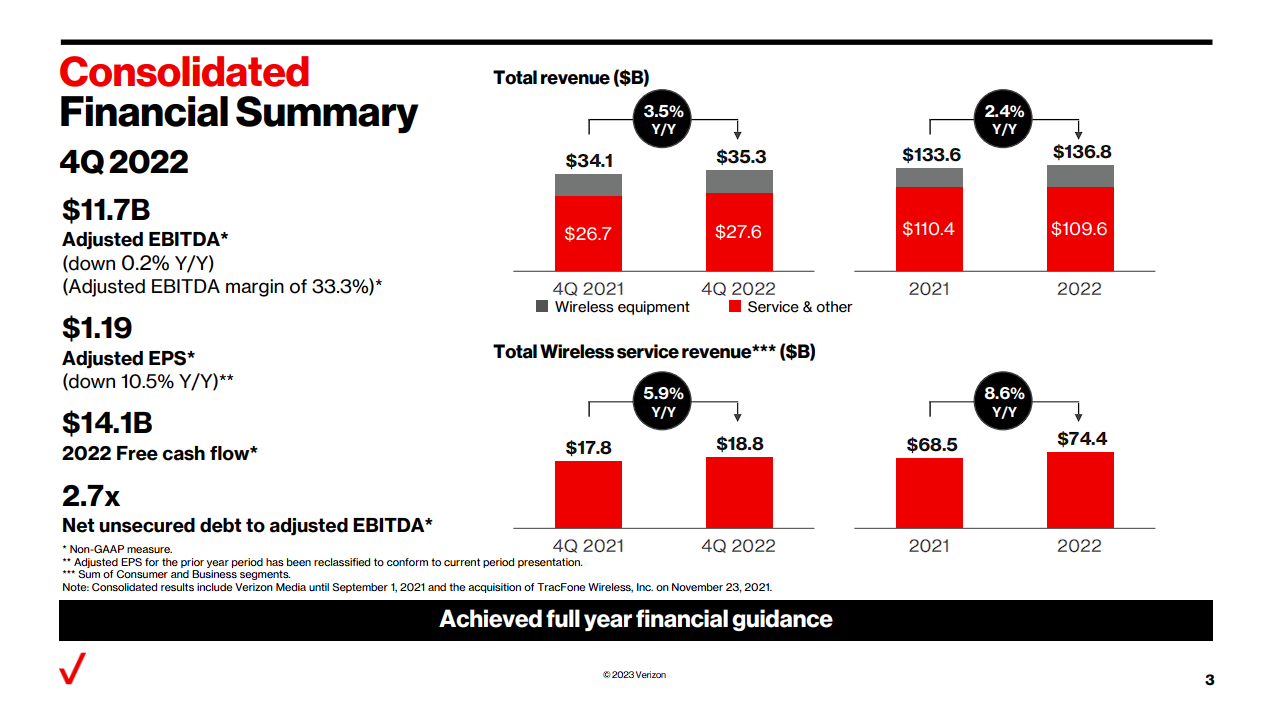

Verizon Communications was created by a merger between Bell Atlantic Corp and GTE Corp in June 2000. Verizon is one of the largest wireless carriers in the country. Wireless contributes three-quarters of all revenues, and broadband and cable services account for about a quarter of sales. The company’s network covers ~300 million people and 98% of the U.S.

On January 25th, 2023, Verizon announced earnings results for the fourth quarter and full year for the period ending December 31st, 2022. For the quarter, revenue grew 3.5% to $35.3 billion, which topped estimates by $160 million. Adjusted earnings-per-share of $1.19 compared unfavorably to $1.11 in the prior year but was in line with expectations.

For 2022, revenue improved by 2.4% to $136.8 billion, while adjusted earnings-per-share fell to $5.06 from $5.39 in the previous year. Verizon had postpaid phone net additions of 217K during the quarter, much better than just the 8,000 net additions in the third quarter.

Revenue for the Consumer segment grew 4.2% to $26.8 billion, again driven by higher equipment sales and a 5.9% increase in wireless revenue growth. Broadband had 416K net additions during the quarter, which included 379K fixed wireless net additions. Fios additions totaled 59K. Business revenue increased by 1.2% to $7.9 billion. Retail connections totaled 143 million, and the wireless retail postpaid phone churn rate was low at 0.89%.

Source: Investor Presentation

Verizon provided guidance for 2023 as well, with the company expecting adjusted earnings-per-share of $4.55 to $4.85 for the year. Wireless service revenue is projected to grow from 2.5% to 4.5%.

We expect annual returns of 13.1% over the next five years for Verizon Communications stock. Shares currently yield 6.7%, while we expect 2.5% annual EPS growth. Expansion of the P/E multiple could boost returns by 5.8% per year.

Consistent High Yield Stock #10: Walgreens Boots Alliance, Inc. (WBA)

- 5-year expected annual returns: 13.4%

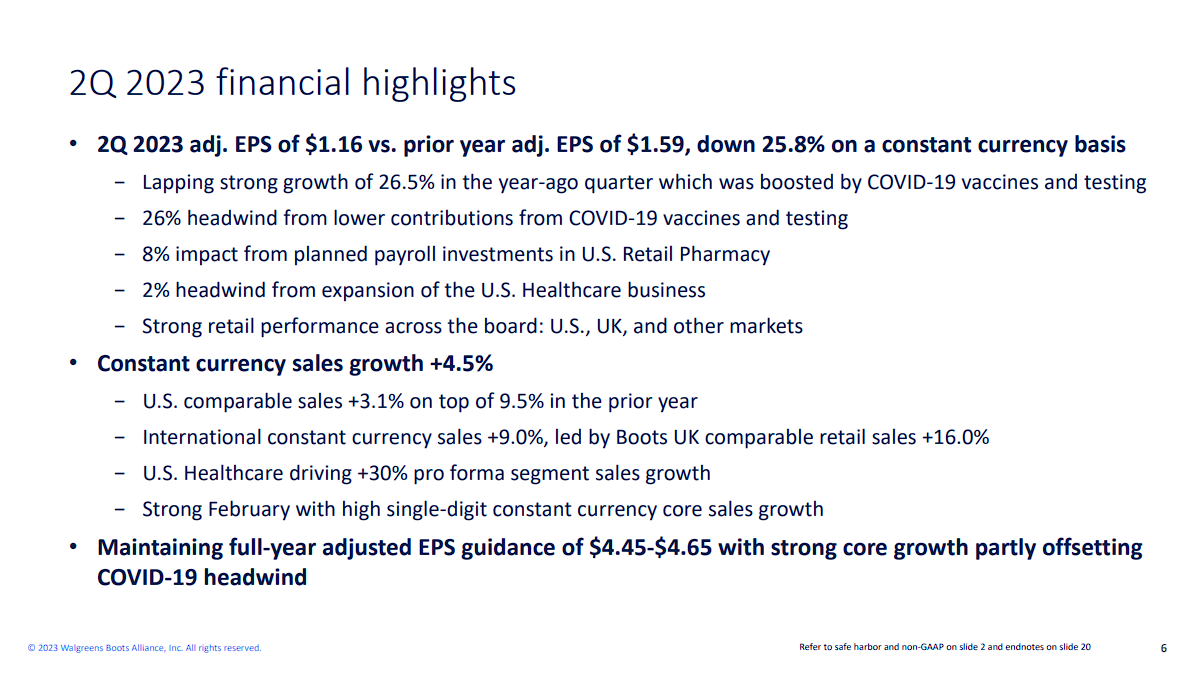

Walgreens Boots Alliance is the largest retail pharmacy in both the United States and Europe. Through its flagship Walgreens business and other business ventures, the $30 billion market cap company has a presence in more than nine countries, employs more than 315,000 people, and has more than 13,000 stores in the U.S., Europe, and Latin America.

On March 28th, 2023, Walgreens reported results for the second quarter of fiscal 2023. Sales grew 3%, but adjusted earnings-per-share slumped -27% over the prior year’s quarter, from $1.59 to $1.16, mostly due to high COVID-19 vaccinations in the prior year’s period.

Earnings-per-share exceeded analysts’ consensus by $0.05. The company has beaten analysts’ estimates for 11 consecutive quarters. However, as the pandemic has subsided, Walgreens is facing tough comparisons. It thus reaffirmed its guidance for earnings-per-share of $4.45-$4.65 in fiscal 2023, implying a -10% decrease at the mid-point. The stock has plunged -35% off its peak in early 2022 due to the fading tailwind from the pandemic (2.4 million vaccinations in Q2-2023 vs. 11.8 million in Q2-2022) and somewhat more intense competition.

Source: Investor Presentation

We expect annual returns of 13.4% over the next five years for Walgreens Boots Alliance stock. Shares currently yield 5.4%, while we expect 4.0% annual EPS growth. Expansion of the P/E multiple could boost returns by 5.2% per year.

Consistent High Yield Stock #9: Magellan Midstream Partners, L.P. (MMP)

- 5-year expected annual returns: 13.1%

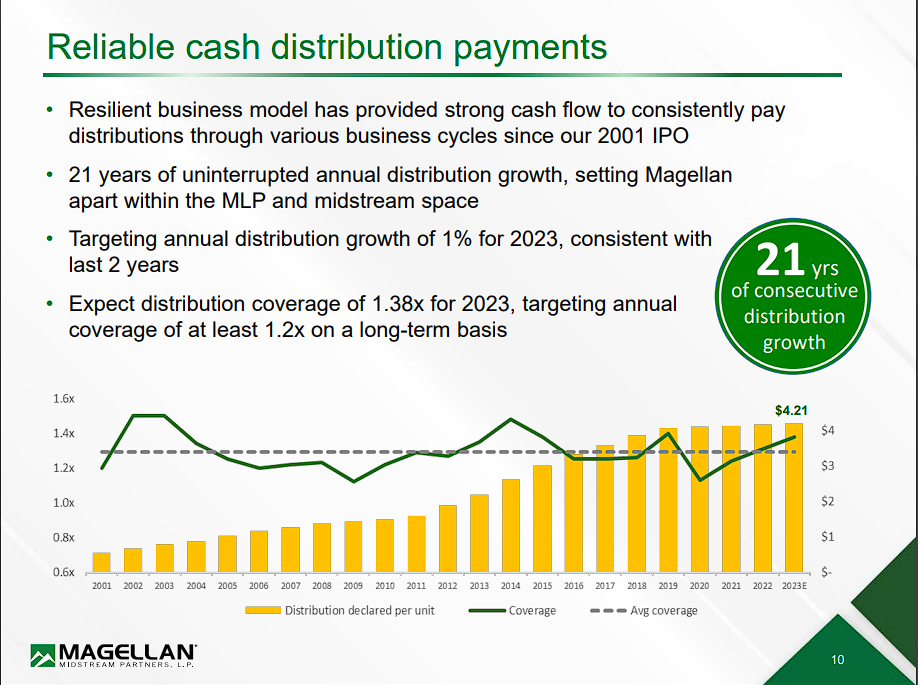

Magellan Midstream Partners has the longest pipeline system of refined products, which is linked to nearly half of the total U.S. refining capacity. This segment generates 65% of its total operating income, while the transportation and storage of crude oil generate 35% of its operating income.

MMP has a fee-based model; only ~9% of its operating income depends on commodity prices. That is why it exhibited impressive resilience in the downturn of the oil market between 2014 and 2017 and throughout the pandemic. MMP has a market capitalization of $11.3 billion.

During the last decade, MMP has invested about $6 billion in growth projects and acquisitions and has exhibited much better performance than the vast majority of MLPs. Most MLPs carry excessive amounts of debt, post poor free cash flows due to their capital expenses and dilute their unitholders to a great extent on a regular basis.

They also tend to have payout ratios near or above 100%. On the contrary, MMP has posted positive free cash flows for more than ten consecutive years and has a strong balance sheet. In addition, it does not dilute unitholders and maintains a healthy payout ratio. All these attributes confirm the discipline of its management, which invests only in high-return projects.

Source: Investor Presentation

In early February, MMP reported (2/2/23) financial results for the fourth quarter of fiscal 2022. Distributable cash flow grew 16% over the prior year’s quarter, mostly thanks to increased volumes of refined products and improved commodity margins. MMP has proved resilient to the pandemic and provided strong guidance for 2023.

It expects an annual distributable cash flow of $1.8 billion and a distribution coverage ratio of 1.4 for the full year. We also praise management for repurchasing shares when the stock price is suppressed, in contrast to most companies, which repurchase shares during boom times at elevated stock prices.

We expect annual returns of 13.1% over the next five years for Magellan Midstream Partners stock. Units currently yield 7.6%, while we expect 3.0% annual distributable cash flow per share growth. Expansion of the P/CF multiple could boost returns by 5.1% per year.

Consistent High Yield Stock #8: Digital Realty Trust (DLR)

- 5-year expected annual returns: 13.5%

Digital Realty Trust is a real estate investment trust (REIT) that is a leader in buying and developing properties for technological uses. Digital Realty’s properties are a combination of data centers that store and process information, technology manufacturing sites, and Internet gateway data centers that allow major metro areas to transmit data. The company operates over 300 facilities in 28 countries on six continents and has a market capitalization of $27.3 billion.

Digital Realty’s chief competitive advantage is that it is among the largest technology REITs in the world. This gives the REIT a size and scale advantage that competitors have difficulty matching. In addition, the company has proven to be able to utilize its balance sheet to fund acquisitions in order to grow FFO and revenues.

On March 3rd, 2022, Digital Realty declared a $1.22 quarterly dividend, marking a 5% increase and the company’s 17th straight year of increasing its payout.

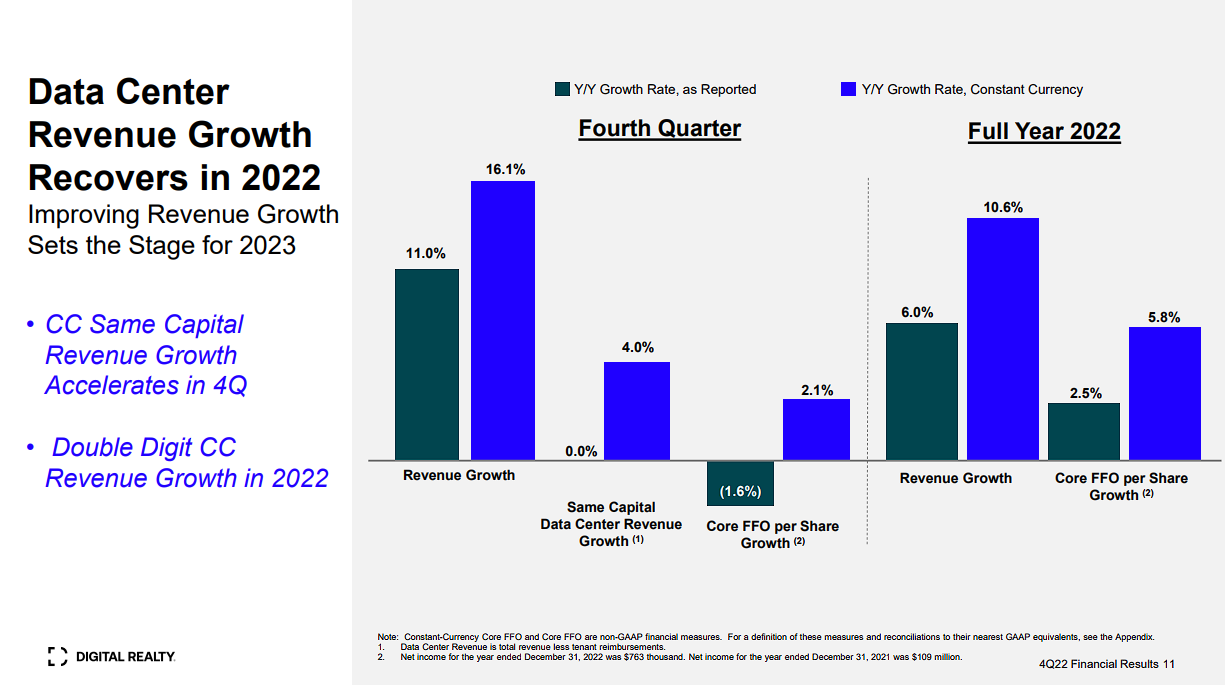

On February 16th, 2023, Digital Realty reported Q4 2022 results for the period ending December 31st, 2022. For the quarter, Digital Realty’s revenue came in at $1.2 billion, a 3% increase compared to Q4 2021. During the quarter, the company generated $1.65 in core FFO per share compared to $1.67 per share prior.

Source: Investor Presentation

Digital Realty also initiated 2023 guidance, anticipating $5.7 billion to $5.8 billion in revenue and $6.65 to $6.75 in core FFO.

We expect annual returns of 13.5% over the next five years for Digital Realty Trust. Shares currently yield 5.3%, while we expect 5.0% annual FFO growth. Expansion of the P/FFO multiple could boost returns by 4.2% per year.

Consistent High Yield Stock #7: Bank of Montreal (BMO)

- 5-year expected annual returns: 13.6%

Bank of Montreal was formed in 1817, becoming Canada’s first bank. The past two centuries have seen the Bank of Montreal grow into a global powerhouse of financial services and today, it has about 2,000 branches (including Bank of West branches) in North America. Bank of Montreal produces about C$14 billion in net income annually. It generates about 45% of its earnings from the U.S. (including Bank of the West) and the rest primarily from Canada. The bank is cross-listed in both New York and Toronto.

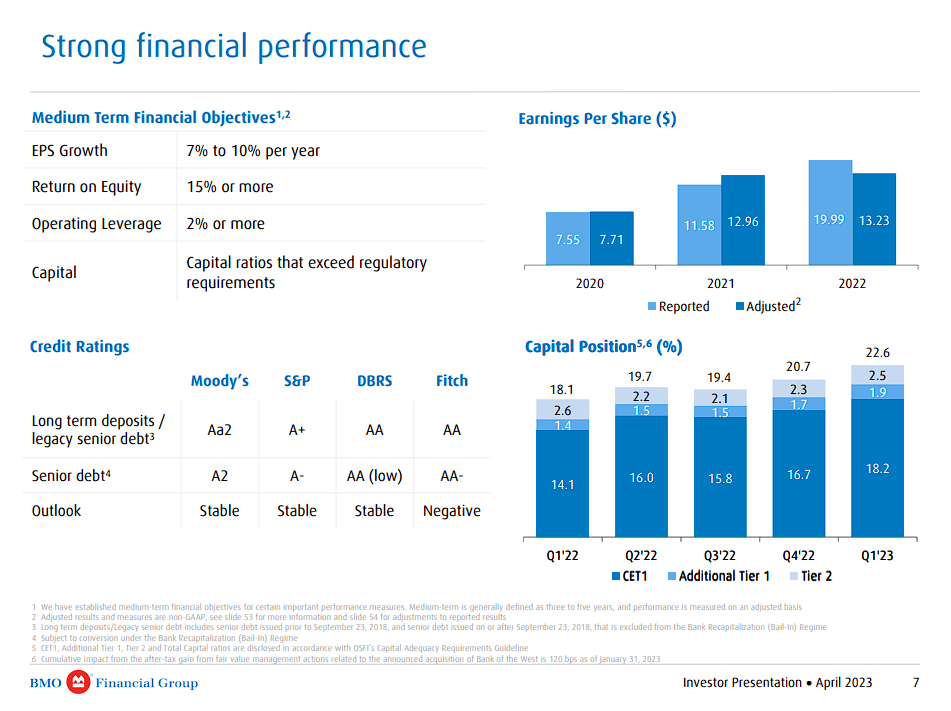

Bank of Montreal posted its fiscal Q1 2023 financial results on 2/28/23. For the quarter, compared to a year ago, adjusted net revenue increased 2.6% to C$7,294 million, and adjusted net income fell 12% to C$2,272 million. Adjusted diluted earnings per share (“EPS”) declined by 17% to C$3.22.

Source: Investor Presentation

For its Canadian Personal and Commercial Banking segment, it saw revenue growth of 9%, thanks to higher net interest income from higher net interest margins. However, adjusted net income declined by 2% to C$980 million. The U.S. Personal and Commercial Banking segment saw adjusted net income rise 3% to C$699 million thanks to a stronger U.S. dollar. Both segment results were weighed by higher expenses and higher provision for credit losses (PCL).

The Wealth Management segment’s adjusted net income declined 12% to C$278 million due to weaker global markets and higher expenses. The Capital Markets segment saw adjusted net income decrease 28% year over year to C$510 million primarily because the prior year’s quarter’s results were particularly strong. The bank’s common equity tier 1 ratio remained solid at 18.2%, up from 14.1% a year ago. The adjusted return on equity was still good at 13.4% versus 18.8% a year ago.

Executing its North American growth strategy, the bank completed the acquisition of Bank of the West from BNP Paribas on February 1, 2023, for a cash purchase price of $13.8 billion. The transaction doubled BMO’s U.S. footprint, particularly providing immediate scale in the highly attractive market of California, which has the largest population and economy in the U.S. In light of recent results, we lowered our fiscal 2023 EPS estimate to $9.95.

We expect annual returns of 13.6% over the next five years for Bank of Montreal. Shares currently yield 4.7%, while we expect 5.5% annual EPS growth. Expansion of the P/E multiple could boost returns by 4.1% per year.

Consistent High Yield Stock #6: Brookfield Infrastructure Partners L.P. (BIP)

- 5-year expected annual returns: 14.0%

Brookfield Infrastructure Partners L.P. is one of the largest global owners and operators of infrastructure networks, which includes operations in sectors such as energy, water, freight, passengers, and data. Brookfield Infrastructure Partners is one of the multiple publicly-traded listed companies under Brookfield Corporation (BN).

Brookfield Infrastructure Partners is a Bermuda-based limited partnership that is treated as a partnership for U.S. and Canadian tax purposes, and it reports financial results in U.S. dollars. It spun off Brookfield Infrastructure Corp. (BIPC, TSX: BIPC) in early 2020 for investors who prefer to invest in a corporation.

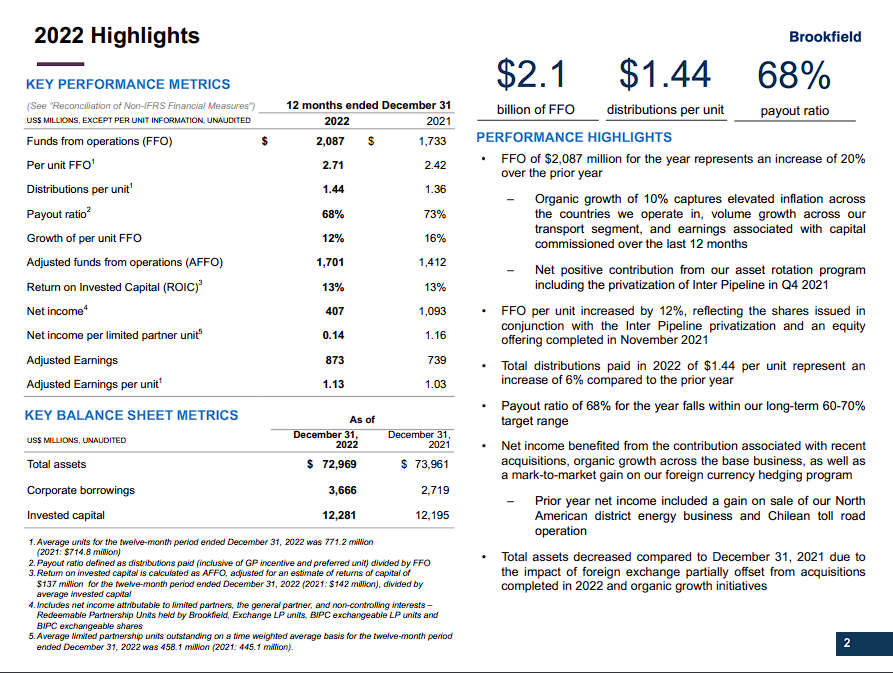

BIP reported positive Q4 2022 results on 02/02/23. For the quarter, its funds-from-operations (FFO) grew 14% to $556 million. On a per-unit basis, its FFO climbed 11% to $0.72.

The full-year results provide a bigger picture. In 2022, its FFO climbed 20% to $2,087 million. On a per-unit basis, FFO rose 12% to $2.71. FFO growth was driven by the midstream and transport segments, which saw growth of 51% and 13%, respectively. The utilities segment saw FFO growth of 5%, while the data segment’s FFO was essentially flat.

Source: Investor Presentation

BIP expects to close the sale of its Indian toll road portfolio and the sale of its 50%-owned port in Australia in the first half of 2023. Together, it projects to generate net proceeds of $260 million. It also has several sales in advanced stages, and a next round of asset sales that it expects will generate net proceeds of +$2 billion this year.

We expect annual returns of 14.0% over the next five years for Brookfield Infrastructure Partners. Units currently yield 4.4%, while we expect 7.0% annual FFO per share growth. Expansion of the P/FFO multiple could boost returns by 3.4% per year.

Consistent High Yield Stock #5: Fifth Third Bancorp (FITB)

- 5-year expected annual returns: 14.2%

Fifth Third Bancorp owns and operates banks in 12 midwestern and southern U.S. states, including Georgia, Florida, Michigan, and Ohio. The company has nearly 1,100 offices. Fifth Third Bancorp has a market capitalization of $18.2 billion and generates annual revenues of close to $9.3 billion.

Source: Investor Presentation

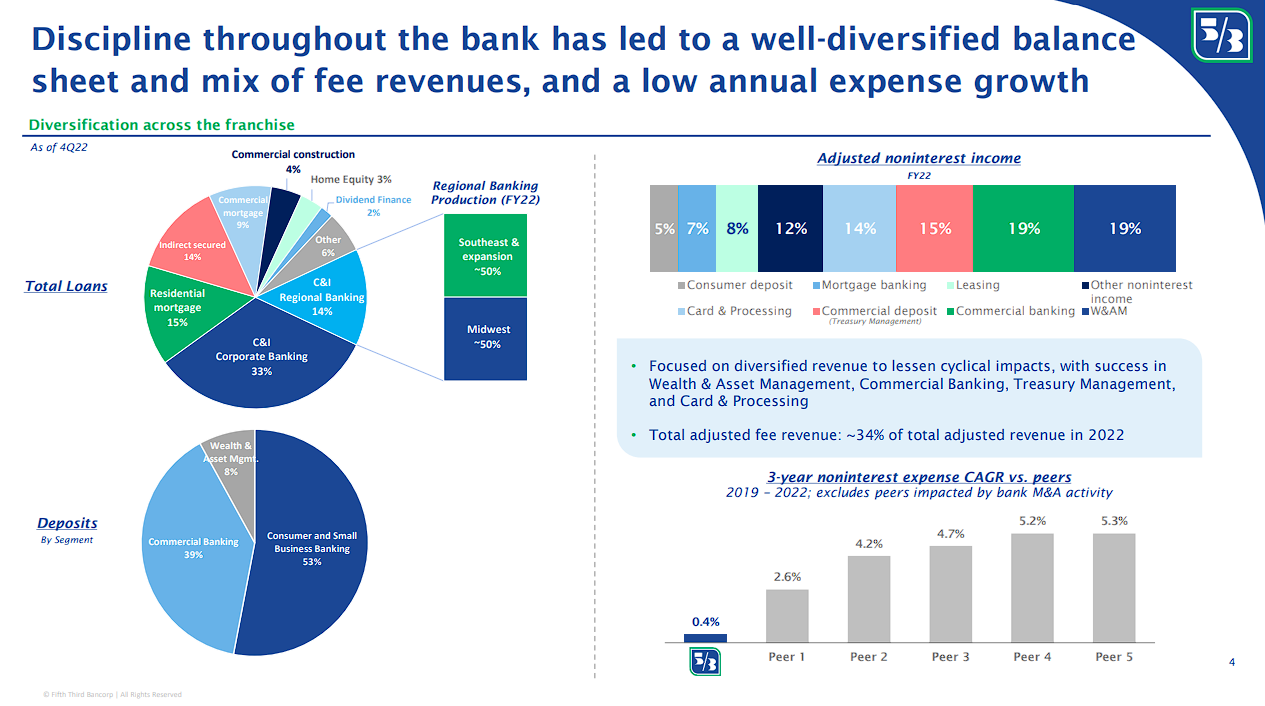

On January 19th, 2023, Fifth Third Bancorp reported fourth-quarter and full-year earnings results for the period ending December 31st, 2022. For the quarter, revenue grew 14.3% to $2.32 billion, which was $20 million less than expected. Earnings-per-share of $1.01 compared favorably to $0.91 in the prior year and was $0.01 above estimates.

For 2022, revenue grew 4.8% to $8.32 billion while earnings-per-share of $3.41 compared to $3.77 in the previous year. Average portfolio loans and leases improved 10.9% year-over-year to $121.4 billion. Provisions for credit losses were $180 million in the third quarter, compared to the benefit of $47 million in the prior year.

The non-performing asset ratio of 0.44% was a two basis point improvement from the third quarter of 2022 and 3 basis points below the same period a year ago. Average deposits declined 3.9% from the same period a year ago. Net interest income grew 5.3% sequentially and 32% year-over-year. The net interest margin of 3.35% was higher by 13 basis points quarter-over-quarter and was up 80 basis points year-over-year.

Compared to the prior year, Fifth Third Bancorp had a return on average tangible common equity of 29.2% versus 16.1%, a return on average common equity of 18.8% versus 12.2%, and a return on average assets of 1.42% versus 1.25%. Fifth Third Bancorp is expected to earn $3.82 per share in 2023.

We expect annual returns of 13.6% over the next five years for Fifth Third Bancorp. Shares currently yield 5.0%, while we expect 3.0% annual EPS growth. Expansion of the P/E multiple could boost returns by 7.6% per year.

Consistent High Yield Stock #4: Bank of Nova Scotia (BNS)

- 5-year expected annual returns: 14.3%

Bank of Nova Scotia (often called Scotiabank) is the third-largest financial institution in Canada, behind the Royal Bank of Canada (RY) and the Toronto-Dominion Bank (TD). Scotiabank reports in 4 core business segments – Canadian Banking, International Banking, Global Wealth Management, and Global Banking & Markets. The bank stock is cross-listed on the Toronto Stock Exchange and the New York Stock Exchange using ‘BNS’ as the ticker.

Scotiabank reported fiscal Q1 2023 results on 2/28/23. For the quarter, on an adjusted basis, revenue fell 1% to C$7,980 million, with expenses up 6% to C$4,443 million. Adjusted net income declined 14% to C$2,366 million, which translated to adjusted earnings-per-share (“EPS”) also falling 14% to C$1.85.

Source: Investor Presentation

The Canadian Banking business saw adjusted net income falling 10% to C$1,088 million due to higher provision for credit losses (PCLs), reflecting a less favorable macroeconomic outlook. For this segment, expenses rose faster than revenue as the bank blamed “higher personnel costs driven by staffing and inflation and technology costs.”

Revenue fell 7% for the Global Wealth Management segment because of lower fee income from lower trading volumes and lower assets under management. Management also explained that overall expenses rose from higher personnel costs, performance-based compensation, and costs to support business growth.

The adjusted return on equity was 13.4%, down from 15.9% a year ago. The bank’s capital position remained solid, with its Common Equity Tier 1 ratio at 11.5%. In light of the latest results, the bank stock dipped about 6% on the day. We update BNS’s fiscal 2023 EPS estimate to US$5.95.

We expect annual returns of 13.6% over the next five years for the Bank of Nova Scotia. Shares currently yield 6.1%, while we expect 4.8% annual EPS growth. Expansion of the P/E multiple could boost returns by 4.8% per year.

Consistent High Yield Stock #3: Toronto-Dominion Bank (TD)

- 5-year expected annual returns: 15.5%

Toronto-Dominion Bank traces its lineage back to 1855, when the Bank of Toronto was founded. The institution – formed by millers and merchants – has since blossomed into a global organization with approximately 90,000 employees and C$1.8 trillion in assets. The bank produces about C$17 billion in annual net income, which primarily comes from retail banking-focused businesses.

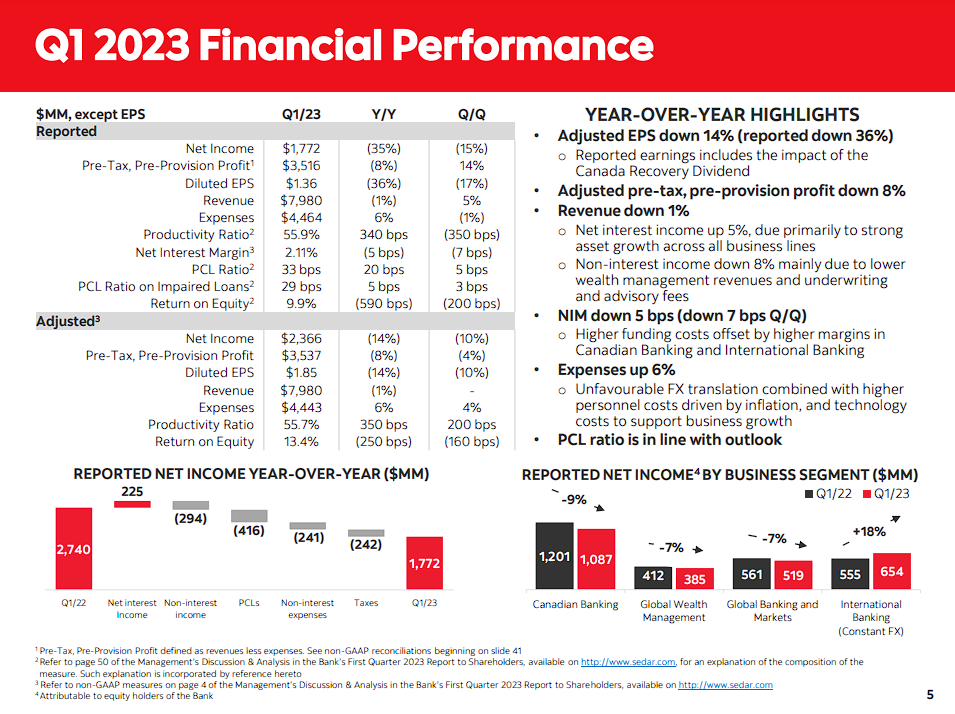

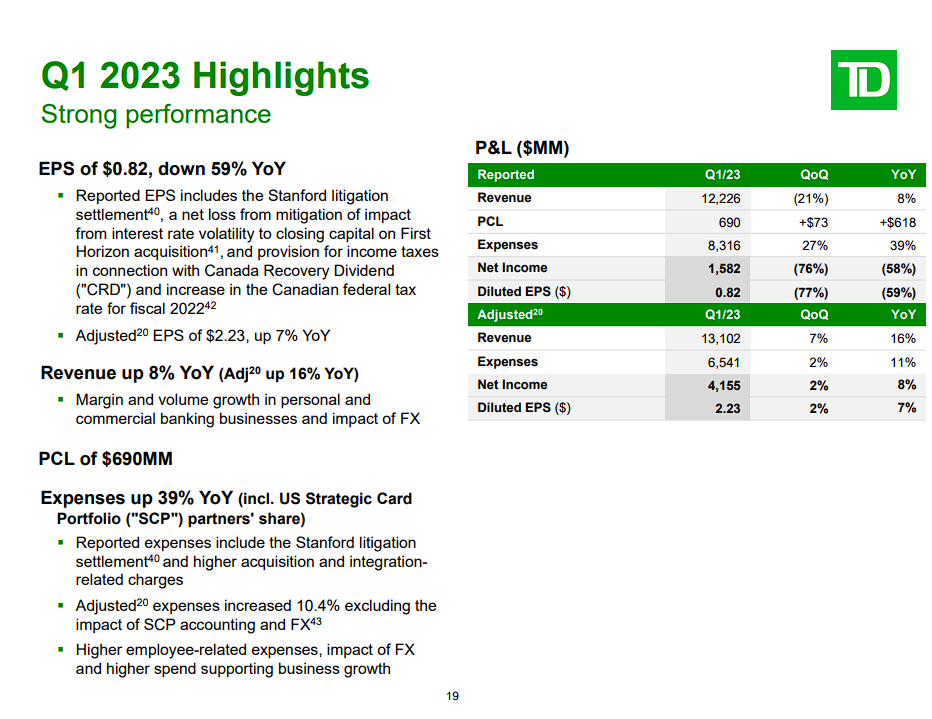

TD reported fiscal Q1 2023 earnings results on 3/1/23. For the quarter, TD reported revenue growth of 8.4% to C$12.2 billion, but net income came in 58% lower year over year (“YOY”) at C$1,582 million, leading to earnings per share (“EPS”) decline of 59% to C$0.82. Other than the bank being more cautious about the North American economy and setting higher provisions for credit losses (PCL), acquisition, and integration-related costs, the Stanford litigation settlement of C$1.6 billion, among other items, also weighed on reported net income.

Source: Investor Presentation

Specifically, PCL was C$690 million (versus C$72 million in fiscal Q1 2022) as the bank set aside a bigger reserve to prepare for a potentially higher percentage of bad loans. The adjusted net income is likely a better metric that is able to display the normal earnings power of the quality bank. After adjustments, the adjusted net income was C$4,155, up 8.4% YOY, while the adjusted EPS was C$2.23, up 7.2%. Adjusted non-interest expenses also rose 11% to C$6,541 million, weighing on the bottom line.

Its Canadian Personal and Commercial Banking segment saw revenue growth of 17% to C$4,589 million, leading to net income growth of 7% to C$1,729 million, reflecting higher margins and volume growth. The U.S. Retail businesses increased net income by 25% to C$1,589 million (in US$, it was a 17% increase to US$1,177 million). Due to challenging market conditions, the Wealth Management and Insurance business witnessed net income falling 14% to C$550 million.

The Wholesale Banking segment saw net income falling 24% to C$331 million because of higher non-interest expenses and PCL. Total deposits climbed 5.3% to C$1,220.6 billion, while total loans increased 12.5% to C$836.7 billion YOY. The bank’s capital position was strong, with a common equity tier 1 ratio of 15.5%, up from 15.2% a year ago. As well, its adjusted return on equity was 16.1% versus 15.7% a year ago.

We expect annual returns of 15.5% over the next five years for the Toronto-Dominion Bank. Shares currently yield 4.8%, while we expect 6.0% annual EPS growth. Expansion of the P/E multiple could boost returns by 5.7% per year.

Consistent High Yield Stock #2: 3M Company (MMM)

- 5-year expected annual returns: 16.3%

3M sells more than 60,000 products that are used every day in homes, hospitals, office buildings, and schools around the world. It has about 95,000 employees and serves customers in more than 200 countries.

3M is facing several lawsuits, including nearly 300,000 claims that its earplugs used by U.S. combat troops and produced by a subsidiary were defective.

On July 26th, 2022, 3M announced that Aearo Technologies had filed for bankruptcy as it looks to conclude lawsuits related to its combat earplugs.

On August 26th, 2022, a U.S. judge ruled that bankruptcy for Aearo would not stop lawsuits against the parent company.

On October 13th, 2022, a federal appeals court agreed to hear the company’s appeal related to the lower court’s ruling on bankruptcy for the subsidiary.

On July 26th, 2022, 3M announced that it would be spinning off its Health Care segment into a standalone entity, which would have had $8.6 billion of revenue in 2021. The transaction is expected to close by the end of 2023.

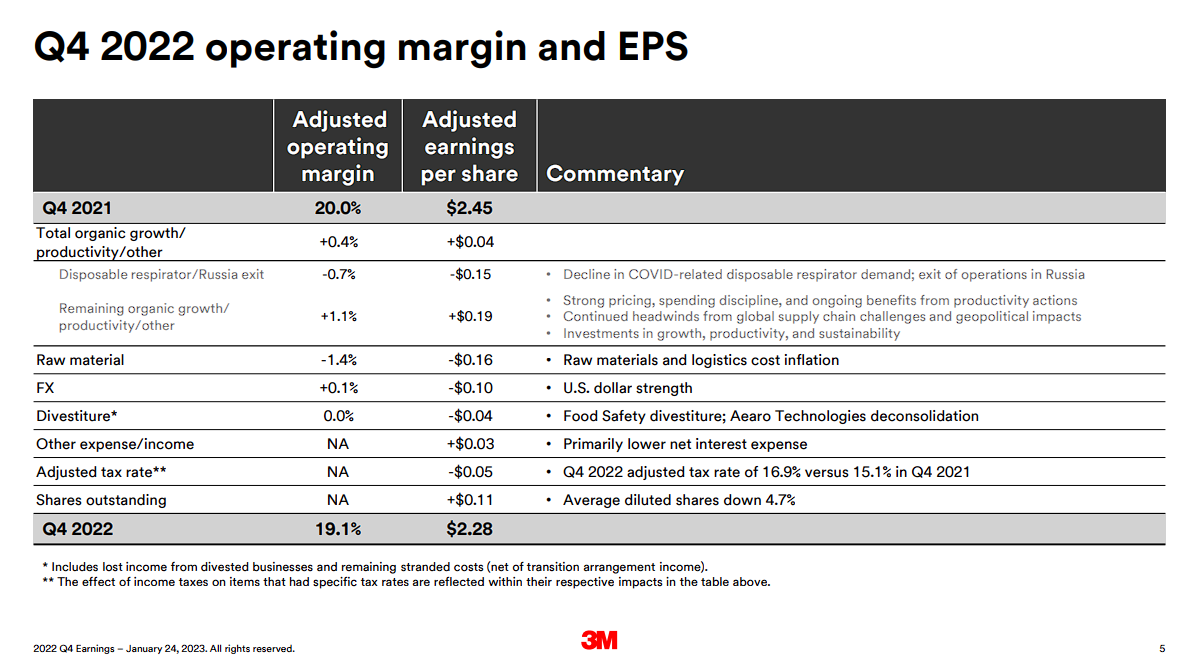

On January 24th, 2023, 3M announced earnings results for the fourth quarter and full year for the period ending December 31st, 2022. For the quarter, revenue declined 5.9% to $8.1 billion but was $10 million more than expected. Adjusted earnings-per-share of $2.28 compared to $2.31 in the prior year and was $0.11 less than projected.

Source: Investor Presentation

For 2022, revenue decreased by 3% to $34.2 billion. Adjusted earnings-per-share for the period totaled $10.10, which compared unfavorably to $10.12 in the previous year and was at the low end of the company’s guidance. Organic growth for the quarter was 1.2%. Health Care, Transportation & Electronics, and Safety & Industrial grew 1.9%, 1.4%, and 1.3%, respectively. Consumer fell 5.7%. The company will cut 2,500 manufacturing jobs.

3M provided an outlook for 2023, with the company expecting adjusted earnings-per-share in a range of $8.50 to $9.00. On a comparable basis, adjusted earnings-per-share for 2022 was $9.88.

We expect annual returns of 16.3% over the next five years for the 3M Company. Shares currently yield 5.7%, while we expect 5.0% annual EPS growth. Expansion of the P/E multiple could boost returns by 7.4% per year.

Consistent High Yield Stock #1: Regions Financial (RF)

- 5-year expected annual returns: 16.3%

Regions Financial Corporation is a financial holding company that provides banking services, as well as bank-related services, to individuals and corporations. Regions Financial splits its operations into three segments, Corporate, Consumer, and Wealth Management. Regions Financial operates about 1,300 banking offices in the South and Midwest regions of the US, as well as in Texas. Regions Financial was founded in 1970 and is headquartered in Birmingham, Alabama.

The company has paid dividends every year for 31 years, although the dividend was not raised during each of these years, and there was a dividend cut, which is why the company does not qualify as a Dividend Aristocrat.

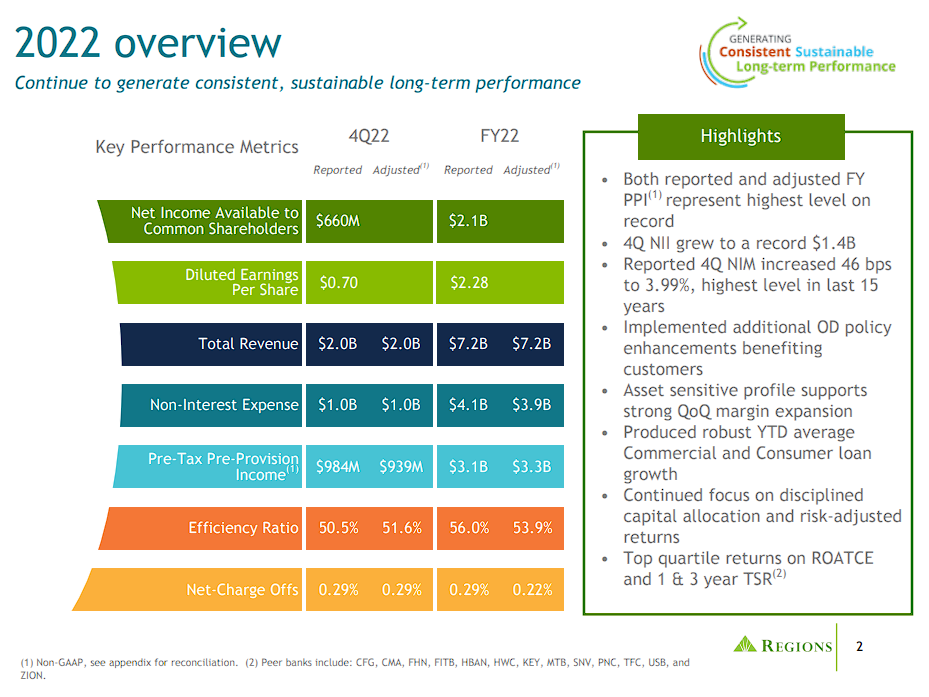

Regions Financial announced its most recent quarterly results for Q4 2022 on January 20th, 2023. Regions Financial generated revenues of $2.0 billion during the quarter, which represents an increase of 23% compared to the previous year’s period, which was slightly better than expected by the analyst community. Revenues being up can be explained by the fact that Regions Financial’s net interest income, as well as its non-interest income, e.g., through fees, were up compared to the previous year’s quarter.

Source: Investor Presentation

The bank’s net interest margin expanded by more than 40 basis points to 3.99%. Regions Financial was able to grow its loan portfolio by an attractive 10% over the last twelve months, which helped generate revenue growth and should have a positive impact on near-term net interest income growth.

Regions Financial generated earnings-per-share of $0.70 during the quarter, which beat analyst estimates by $0.04. Regions Financial did benefit from loan loss provisions being slightly lower than during the previous quarter, and there was no settlement charge. Due to lower loan loss provision releases, Regions Financial was not quite as profitable in 2022 relative to 2021. The company expects that 2023 will be a stronger year again on the back of growing interest margins.

We expect annual returns of 16.3% over the next five years for Regions Financial. Shares currently yield 4.4%, while we expect 5.0% annual EPS growth. Expansion of the P/E multiple could boost returns by 8.8% per year.

Final Thoughts

Finding stocks that have high dividend yields, long histories of steadily increasing dividend payments, and strong growth prospects can be challenging. While continuous interest rate hikes have resulted in the share prices of many high-dividend stocks declining, boosting their yields, there are still not many stocks matching our specific criteria.

The stocks featured in this article all have impressive dividend growth histories, attractive yields, and prospects for high total returns over the next five years. Each company is well-known among dividend growth investors and all stocks receive a buy recommendation from Sure Dividend at this time.

If you are interested in finding high-quality dividend growth stocks and/or other high-yield securities and income securities, the following Sure Dividend resources will be useful:

High-Yield Individual Security Research

- 20 Highest-Yielding BDCs

- 20 Highest-Yielding MLPs

- 20 Highest Yielding Dividend Kings

- 20 Best Ultra High-Dividend Stocks

- 20 High-Dividend Stocks Under $10

- 20 Undervalued High-Dividend Stocks

- 20 Highest-Yielding Dividend Aristocrats

- 20 Highest Yielding Monthly Dividend Stocks

- 20 Highest-Yielding Small Cap Dividend Stocks

- 20 Safe High Dividend Blue-Chip Stocks With Low Volatility

- 12 Long-Term High-Dividend Stocks To Buy And Hold For Decades

- 10 Super High Dividend REITs

- 10 Highest Yielding Dividend Champions

- 10 Highest Yielding Dow 30 Stocks | Dogs Of The Dow

- 10 High-Yield Dividend Stocks Trading Below Book Value

- 9 Highest Yielding Royalty Trusts

Other Sure Dividend Resources

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Monthly Dividend Stocks: Individual securities that pay out every month

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more