Updated on April 1st, 2026 by Felix Martinez

Investors are likely familiar with the standard real estate investment trusts, or REITs. Most REITs own physical real estate, lease the properties to tenants, and derive rental income, which is used to pay dividends.

However, investors may not be as familiar with a different set of REITs: mortgage REITs. These REITs do not own physical properties but rather buy mortgage securities.

Mortgage REITs typically have much higher dividend yields than standard REITs, but this does not necessarily make them better investments.

For example, Orchid Island Capital (ORC) is a mortgage REIT with an extremely high dividend yield of more than 20.5%. Orchid Island pays dividends monthly, making it a compelling combination of high yield and regular payments.

You can download our full Excel spreadsheet of all monthly dividend stocks (along with metrics that matter, like dividend yield and payout ratio) by clicking on the link below:

Orchid Island has an exceptionally high dividend yield and is among the highest-yielding stocks we cover.

However, the outlook for mortgage REITs is under pressure, and Orchid Island’s dividend yield may still be unsustainable despite multiple dividend cuts over the past several years.

This article will discuss why income investors should not be lured by Orchid Island’s extremely high dividend yield.

Business Overview

Whereas traditional REITs own a portfolio of properties, mortgage REITs are purely financial entities. Orchid Island is an externally managed specialty finance REIT that invests in residential mortgage-backed securities, either pass-through or structured agency RMBSs.

An RMBS is a debt instrument that pools cash flows from residential loans, such as mortgages, home-equity loans, and subprime mortgages. Mortgage-backed securities are investment products that represent a pool of mortgages.

As investors saw firsthand during the 2008 financial crisis, mortgage-backed securities can be highly volatile and risky. That said, mortgage REITs were among the biggest winners as interest rates fell during the aftermath of the Great Recession.

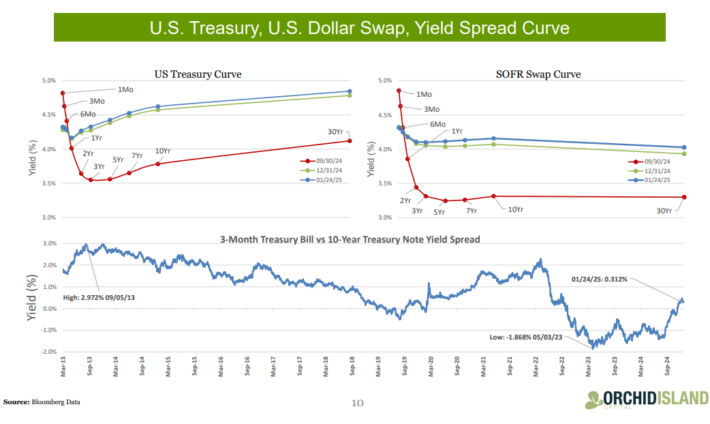

Growth Prospects

Mortgage REITs make money by borrowing at short-term rates, lending at long-term rates, and pocketing the difference, or the spread between the two.

When the spread between short-term rates and long-term rates compresses, profitability erodes. This is why mortgage REITs can be dangerous if short-term interest rates are about to increase.

Source: Investor Presentation

Orchid Island has not been able to produce meaningful growth in the past several years. The trust has experienced extreme earnings volatility over the past several years, with net losses in several years in the past decade and multiple years in which it barely generated a profit.

Orchid Island’s inability to perform well at zero interest rates makes it unlikely that the trust can regain its footing in the current higher-interest-rate environment.

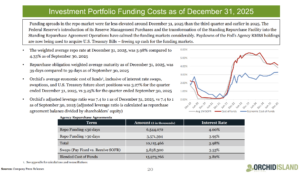

Dividend Analysis

Orchid Island’s deteriorating fundamentals have led to a significant decline in its dividend payments to shareholders over the past several years.

Orchid Island currently pays a monthly dividend of $0.12 per share, but this is still below the split-adjusted monthly dividend it paid before 2021.

Source: Investor Presentation

Looking back further, Orchid Island’s monthly dividend payout has been reduced multiple times since then.

The trust’s current dividend payout is $1.44 per share on an annualized basis. Based on its recent closing price, the stock offers a 19.3% dividend yield. This is a huge dividend yield, given the S&P 500 Index’s current average dividend yield of 1.3%.

However, there are too many red flags for Orchid Island to be considered an attractive investment, including the trust’s multiple dividend cuts over the past few years and inconsistent profitability. With an expected payout ratio of 110% for 2026, the risk for further dividend cuts is high.

In addition, Orchid Island has issued shares rapidly in recent years. Its share count has skyrocketed since 2013, but this comes at a steep cost to shareholders in the form of heavy dilution.

With a volatile dividend history, Orchid Island is not an appealing choice for investors seeking steady year-over-year dividend payouts.

Orchid Island stock appears to be the definition of a yield trap. The stock has badly lagged behind the S&P 500 Index, and we believe this underperformance will continue.

Final Thoughts

Sky-high dividend yields can be deceiving. Orchid Island’s 20.5% dividend yield is enticing, but this stock has all the makings of a yield trap.

The trust has a sizable amount of debt on the balance sheet and is issuing shares at an alarming pace. The outlook for mortgage REITs has deteriorated as the Federal Reserve continues to hold interest rates high. The trust’s most recent Q4 results show a significant decline in net interest income and per-share book value.

Orchid Island has cut its dividend several times in the past few years due to weak fundamentals. Investors should tread very carefully with mortgage REITs like Orchid Island. As a result, income investors would be better served by buying higher-quality dividend stocks with more sustainable payouts.

Don’t miss the resources below for more monthly dividend stock investing research.

- The Monthly Dividend Stocks List

- 20 Highest Yielding Monthly Dividend Stocks

- 10 Cheapest Monthly Dividend Stocks

- 10 Safest Monthly Dividend Stocks

- 3 Top ‘Hold Forever’ Monthly Dividend Stocks

And see the resources below for more compelling investment ideas for dividend growth stocks and/or high-yield investment securities.

- Dividend Kings: 50+ years of rising dividends

- Dividend Champions: 25+ years of rising dividends

- Dividend Aristocrats: 25+ years of rising dividends and in the S&P 500

- Dividend Achievers: 10+ years of rising dividends and in the NASDAQ

- High Dividend Stocks: 4%+ dividend yields

- Blue Chip Stock: Kings, Aristocrats, and Achievers

- MLPs: List of MLPs and more

- REITs: List of REITs and more

- BDCs: List of BDCs and more