Updated on Febuaury 19th, 2026 by Felix Martinez

Automatic Data Processing (ADP) might not be a household name, but it should be for dividend growth investors. ADP has raised its dividend each year for 50 years in a row.

ADP is a member of the Dividend Aristocrats, a group of 69 stocks in the S&P 500 Index with 25+ years of consecutive dividend increases. ADP has one of the longest dividend-increase streaks among the Dividend Aristocrats.

We have created a full list of all 69 Dividend Aristocrats, along with important metrics like P/E ratios and dividend yields, which you can download by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

ADP’s long history of dividend growth is driven by a strong business model and durable competitive advantages. This has led to domination of its core markets for decades. To quote legendary investor Warren Buffett, ADP has a wide economic moat.

This article will review ADP’s fundamentals and discuss whether the stock is currently trading at an attractive enough valuation.

Business Overview

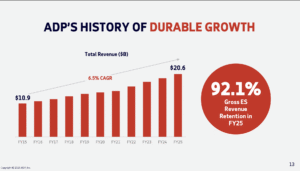

ADP is a business outsourcing services company. It was founded in 1949 and began with a single client. In the 75 years since, ADP has grown into the leading payroll and human resource outsourcing company. It has over 1 million clients in more than 140 countries worldwide.

ADP provides services to companies of all sizes, including payroll, benefits administration, and human resources management. These services are in high demand, as companies prefer to outsource these functions to better focus on their core business activities.

ADP has a leading position across its strategic pillars and a highly diversified client list.

The company has undergone significant restructuring in recent years. In 2014, ADP spun off its human capital management business, which now trades under the name CDK Global (CDK).

ADP posted fiscal second-quarter earnings on January 28th, 2026. ADP reported strong fiscal Q2 2026 results, demonstrating steady demand for payroll and human capital management services. Revenue increased 6% year over year to $5.4 billion (5% organic constant currency), while net earnings rose 10% to $1.1 billion.

Adjusted EBIT also grew 10% to $1.4 billion, with margin expansion of 80 basis points to 26.0%, reflecting operating leverage and disciplined cost control. Diluted EPS increased 11% to $2.62, supported by continued client growth and higher interest income on client funds.

Segment performance remained stable, with Employer Services revenue rising 6% and segment margin improving 50 basis points, while PEO Services revenue also grew 6%, supported by a 2% increase in average worksite employees to roughly 758,000.

Interest on client funds—a key profit driver—rose 13% to $309 million, as average client balances increased 6% to $37.6 billion and portfolio yield improved to 3.3%, benefiting from higher interest rates.

Management raised fiscal 2026 guidance, now expecting ~6% revenue growth, 50–70 basis points of EBIT margin expansion, and adjusted EPS growth of 9–10%. ADP also forecasts $1.31–$1.33 billion in client fund interest income, driven by 4–5% growth in client balances and higher yields near 3.4%.

The outlook reflects continued momentum from new business bookings, strong client retention (~92%), recurring revenue characteristics, and durable demand for outsourced HR solutions, all of which support consistent long-term earnings growth.

Source: Investor Presentation

Growth Prospects

Automatic Data Processing has compounded its adjusted earnings-per-share at a rate of more than 11% per year over the last decade, and we believe it can come close to matching that rate moving forward.

Beyond 2023, we believe the company can deliver 9% annualized earnings-per-share growth over full economic cycles. Much of this growth is likely to be driven by the company’s Professional Employer Organization (PEO) Services segment, which continues to perform strongly.

Importantly, this revenue growth has been accompanied by meaningful margin expansion, indicating that the segment’s growth has outpaced the firm’s bottom line.

In addition, share buybacks are a low single-digit tailwind to annual EPS growth, and we expect that to continue.

Source: Investor Presentation

Two key long-term growth catalysts for ADP are continued payroll increases and expanding regulations.

The number of employees on ADP clients’ payrolls continues to grow, and we believe this will continue for the foreseeable future. Next, the increasingly complex regulatory environment creates significant compliance costs for businesses, which also helps ADP achieve long-term growth.

Competitive Advantages & Recession Performance

Many competitive advantages fuel ADP’s growth. ADP has a deep connection with its customers and enjoys a strong reputation for customer service, which helps maintain very high customer retention.

ADP enjoys a tremendous scale that its competitors cannot match. As a global company, ADP is uniquely positioned to help companies with employees on multiple continents.

In addition, ADP benefits from a recession-resistant business model. ADP’s earnings-per-share during the Great Recession are shown below:

- 2007 earnings-per-share of $1.83

- 2008 earnings-per-share of $2.20 (20% increase)

- 2009 earnings-per-share of $2.39 (8.6% increase)

- 2010 earnings-per-share of $2.39 (flat)

ADP increased earnings per share in 2008 and 2009, a rare accomplishment. ADP’s continued growth during the Great Recession is because businesses still need payroll and human resource services, even during an economic downturn.

The company continued to perform relatively well in the 2020 economic downturn caused by the coronavirus pandemic. ADP remained highly profitable during the pandemic, which allowed it to maintain its streak of annual dividend increases.

The necessary nature of ADP’s services helps insulate the company from the effects of a recession. Given ADP’s size and scale, we believe it will perform well during the next recession.

Valuation & Expected Returns

We forecast adjusted earnings-per-share of approximately $11.00 for fiscal 2026. Based on the current share price of ~$215, the stock has a price-to-earnings ratio of 19.5x.

We see ADP’s fair value at 28 times earnings, suggesting the stock is undervalued. This implies a tailwind to total returns in the coming years from valuation expansion.

If the P/E multiple expands from 19.5x to 28x over the next five years, it would increase annual returns by 7.5% per year.

We expect ADP’s earnings per share to grow by 9% annually over the next five years. In addition, the stock has a current dividend yield of 3.1%.

The combination of earnings growth, dividends, and valuation expansion yields an expected total return of 19.6% per year over the next five years.

Given its strong fundamentals, ADP will almost certainly continue increasing its dividend for many years to come. ADP maintains a target payout ratio of 62% of annual earnings, so the payout is very safe, with room to grow.

Final Thoughts

ADP is a strong business. It maintains a large customer base and holds a leading position in the industry. This gives it a wide economic “moat,” a term popularized by investing legend Warren Buffett.

Indeed, ADP’s wide moat keeps competitors at bay, driving high profitability.

There should be plenty of growth going forward, both in terms of earnings and dividends. Regulations continue to become more complex.

And, as the economy expands, companies are adding employees and increasingly use ADP’s services. If a recession occurs, ADP should continue to increase its dividend, as customers will still need its services.

With an expected rate of return above 19.6%, we rate ADP stock a buy.

If you are interested in finding high-quality dividend growth stocks suitable for long-term investment, the following Sure Dividend databases will be useful:

- The Dividend Achievers List: a group of stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings List: considered to be the best-of-the-best among dividend growth stocks, the Dividend Kings are a group of exceptional dividend stocks with 50+ years of consecutive dividend increases.

- The Blue Chip Stocks List: contains stocks on either the Dividend Achievers, Dividend Aristocrats, or Dividend Kings list.

- The Monthly Dividend Stocks List: contains stocks that pay dividends each month, for 12 payments per year.

- The High Dividend Stocks List: high dividend stocks are suited for investors that need income now (as opposed to growth later) by listing stocks with 5%+ dividend yields.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: