Updated on July 24th, 2026 by Nikolaos Sismanis

With contributions from Ben Reynolds

It’s no secret that the tobacco industry has long been in decline.

Cigarette volumes continue to fall across many developed markets.

And yet… The industry’s economics remain unusually resilient. The largest tobacco companies continue to benefit from:

- Strong brands

- Pricing power

- Low capital requirements

- Dependable cash flow

As a result, they have continued to support generous dividends and sizable share repurchases despite the steady decline in smoking rates.

We are not expecting cigarette consumption to recover.

Instead, the key question is whether pricing, cost savings, and growth in nicotine pouches, heated tobacco, and vaping can offset the decline in combustibles.

The answer differs by company.

Some stocks offer high yields but little growth, while others have stronger smoke-free momentum and trade at richer valuations.

Note: For investors looking for high yield stocks, don’t miss our free high dividend stocks list spreadsheet. It has our full list of ~200 individual securities (stocks, REITs, MLPs, etc.) with 4%+ dividend yields. It’s updated daily, and it includes key metrics like expected total returns, % fair value, Buy/Hold/Sell ratings, and more.

Spreadsheet Notes: Powered by the Sure Analysis Research Database. See our glossary for information on our metrics.

This article will analyze the prospects of the 6 largest tobacco stocks that we cover in the Sure Analysis Research Database.

Rankings are in order of projected total returns from lowest to highest.

Table of Contents

You can instantly jump to any individual stock analysis by clicking on the links below:

- Industry Overview: Declining Smoking Rates

- Tobacco Stock #6: British American Tobacco (BTI)

- Tobacco Stock #5: Altria Group (MO)

- Tobacco Stock #4: Imperial Brands plc (IMBBY)

- Tobacco Stock #3: Universal Corp. (UVV)

- Tobacco Stock #2: Philip Morris International (PM)

- Tobacco Stock #1: Turning Point Brands (TPB)

But first, we’ll take a look at the tobacco industry’s primary concern, which is declining tobacco usage.

Industry Overview: Declining Smoking Rates

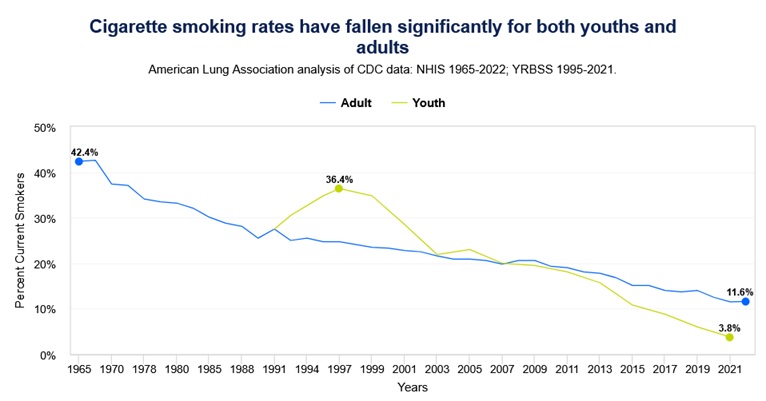

The tobacco industry faces a problem that has been building for decades.

Fewer people are smoking cigarettes, particularly in developed markets, as higher taxes, tighter regulation, smoking restrictions, public-health campaigns, and changing consumer habits continue to weigh on demand.

Source: American Lung Association

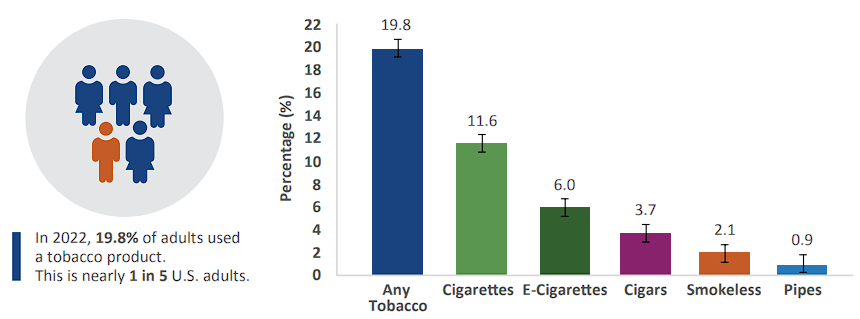

In 2022, 19.8% of U.S. adults used at least one tobacco product, according to the Centers for Disease Control and Prevention. Cigarettes remained the most widely used product, followed by e-cigarettes. The picture among younger consumers has changed even more.

Source: Centers for Disease Control and Prevention

In 2024, 10.1% of high-school students and 5.4% of middle-school students reported using a tobacco product. Student cigarette smoking fell to its lowest level on record, while e-cigarettes remained the most popular category and nicotine pouches moved into second place.

Nicotine use has not gone away, but the products people choose are clearly changing.

For years, the largest tobacco companies have managed falling cigarette volumes through higher prices, tighter cost control, and the strength of their premium brands.

That approach still generates significant cash flow, although it cannot fully offset the industry’s long-term decline.

Increasingly, growth will have to come from smoke-free products such as ZYN, IQOS, Velo, on!, and newer oral nicotine products offered by smaller competitors.

That means dividend yield alone does not tell the full story. We also need to consider regulation, debt levels, dividend safety, progress in smoke-free categories, and valuation.

The rankings below reflect our estimates for dividends, earnings growth, and potential valuation changes over the next five years.

Tobacco Stock #6: British American Tobacco (BTI)

- 5-year expected returns: 2.8%

British American Tobacco is one of the world’s largest nicotine companies. Its portfolio includes global cigarette brands such as Dunhill, Kent, Lucky Strike, and Rothmans, along with U.S. brands including Newport and Camel.

The company is also building its New Categories business around Vuse vapor products, glo heated tobacco, and Velo modern oral nicotine.

This diversification produces considerable cash flow, although currency and regulatory risks can create volatility.

In last year’s full-year results, adjusted diluted earnings per share increased 3.4%, and management raised the dividend 2.0% to 245.04 pence. BAT also announced a £1.3 billion share-repurchase program for 2026.

Its June trading update indicated that New Categories revenue growth was accelerating, supported by Velo and stronger U.S. performance.

Management continues to target 3% to 5% organic revenue growth and 5% to 8% adjusted EPS growth over the medium term, although 2026 is expected near the low end of those ranges.

Earlier this year, BAT recently its Fit2Win transformation program, which aims to generate approximately £600 million in annual savings by the end of 2028.

Those efficiencies and ongoing deleveraging are positives. However, the stock now trades above our fair-value estimate, producing a projected valuation headwind that largely offsets its high dividend yield and modest earnings growth.

That leaves BAT with the lowest expected return in this group.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on BTI.

Tobacco Stock #5: Altria Group (MO)

- 5-year expected returns: 7.2%

Altria is the leading U.S. tobacco company. Its core assets include Marlboro cigarettes, Copenhagen and Skoal moist smokeless tobacco, Black & Mild cigars, on! nicotine pouches, and the NJOY vapor business.

The company’s scale and pricing power make the smokeable-products segment highly profitable, but its concentration in the U.S. leaves it exposed to persistent cigarette-volume declines and domestic regulation.

Altria exited its former JUUL investment in 2023, so JUUL is no longer part of the company’s portfolio.

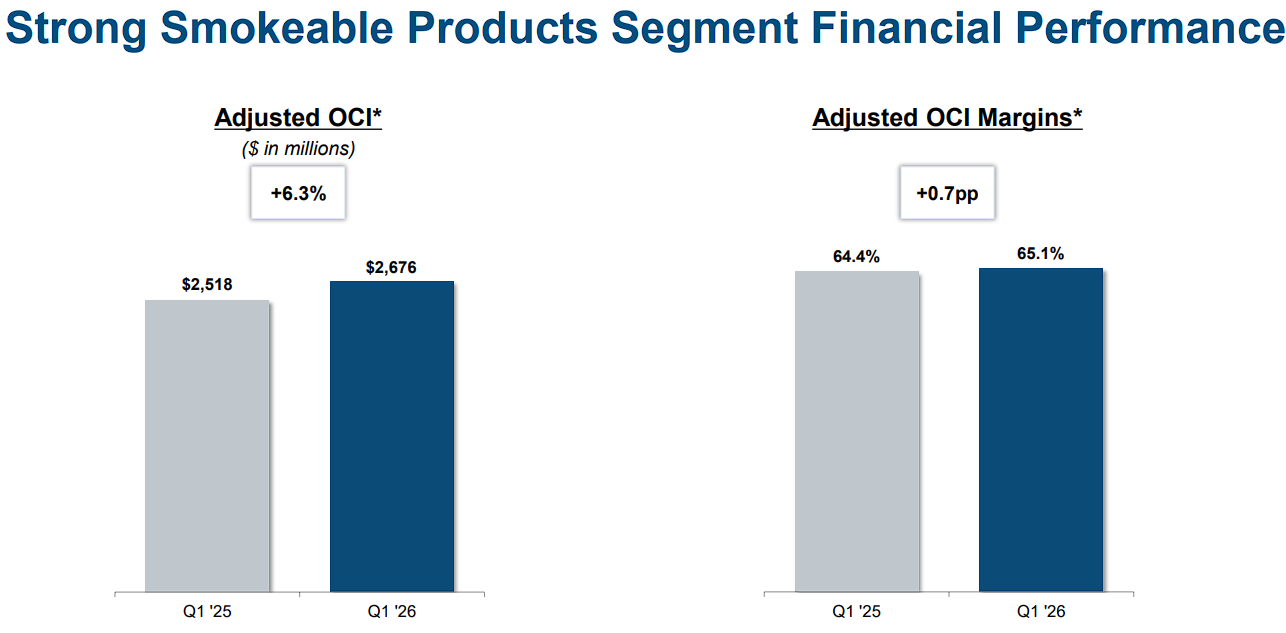

Altria’s first-quarter 2026 results were solid. Revenue net of excise taxes rose 5.3% to $4.8 billion, while adjusted diluted earnings per share increased 7.3% to $1.32.

Smokeable-products adjusted operating income increased 6.3%, and its margin expanded to 65.1%. Reported domestic cigarette shipments fell 2.4%, or an estimated 4% after inventory adjustments.

Meanwhile, on! shipment volume grew 17.6%, partly offsetting declines in Copenhagen and Skoal. Management reaffirmed 2026 adjusted EPS guidance of $5.56 to $5.72, representing growth of 2.5% to 5.5%.

The principal strategic issue is smoke-free execution. Altria assumes NJOY ACE will not return to the market during 2026, limiting its near-term vapor opportunity, while illicit disposable products remain a competitive challenge.

Even so, Marlboro’s economics, on!’s growth, and a well-covered dividend support the investment case. We project a 7.2% annual return through 2031, led primarily by the dividend yield and modest earnings growth.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on MO.

Tobacco Stock #4: Imperial Brands (IMBBY)

- 5-year expected returns: 7.7%

Imperial Brands is a global tobacco company with cigarette and fine-cut tobacco brands including Winston, Davidoff, JPS, and West.

It is smaller than British American Tobacco and Philip Morris International, but its focused-market strategy has supported pricing and cash generation.

Imperial is also developing next-generation products across vapor, heated tobacco, and oral nicotine.

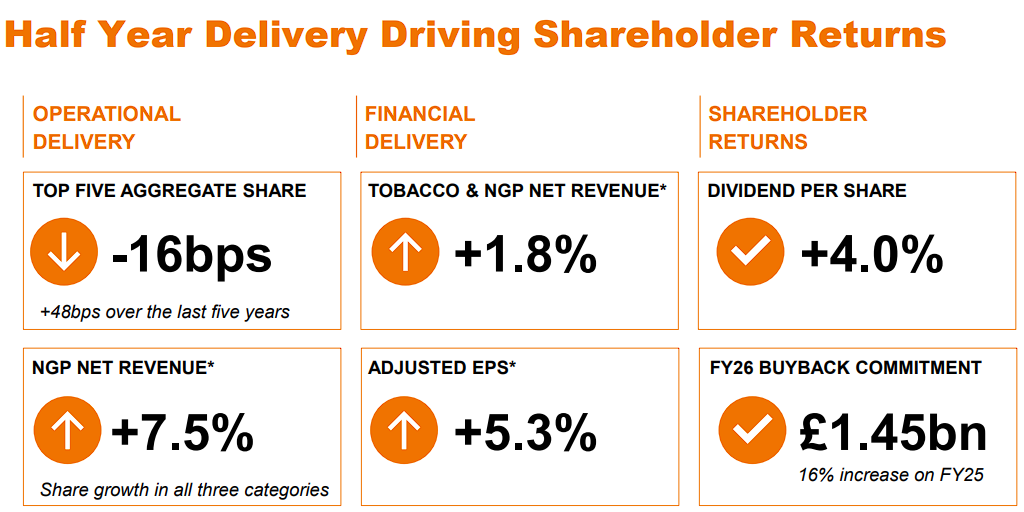

For the six months ended March 31, 2026, tobacco net revenue increased 1.5% at constant currency, while next-generation product revenue rose 7.5%.

Adjusted operating profit increased 0.6% at constant currency, and adjusted earnings per share advanced 5.3% to 127.7 pence.

Reported operating profit fell sharply because of a Delaware settlement and costs associated with the company’s 2030 Strategy, but twelve-month free cash flow remained strong at £2.6 billion, with 98% cash conversion.

Imperial completed £809 million of repurchases during the half and is proceeding with its £1.45 billion buyback for the year.

It also raised the interim dividend 4%. The major development is the 2030 Strategy, which includes a technology and operations partnership with Capgemini and targets about £320 million of annual cost savings by 2030.

These initiatives should support modest earnings growth and capital returns, but we note investors must weigh execution risk, foreign-exchange exposure, and the stock’s Dividend Risk Score of F.

We estimate annual returns of 7.7%, driven mainly by the dividend and earnings growth.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on IMBBY.

Tobacco Stock #3: Universal Corporation (UVV)

- 5-year expected returns: 8.0%

Universal Corporation differs from the other companies on this list because it does not own major consumer cigarette brands. Instead, it is the world’s leading independent leaf-tobacco supplier, sourcing, processing, and distributing tobacco to manufacturers around the globe.

Universal has also expanded into plant-based food and beverage ingredients.

Results can vary with crop quality, shipment timing, working-capital needs, and leaf supply. Universal’s fiscal 2026 results were pressured by excess tobacco inventory and weakness in ingredients.

Full-year revenue declined 1% to $2.92 billion, while adjusted operating income fell 13% to $211.3 million. Adjusted diluted earnings per share decreased to $2.64 from $4.63.

Results included $52 million of tobacco inventory write-downs and a $41.1 million goodwill impairment related to Shank’s. Ingredients revenue increased 3%, but segment operating income fell sharply.

The important issue for fiscal 2027 is normalization. Uncommitted tobacco inventory finished 27% above the company’s target, but management expects it to return to the desired range during the year.

Universal also reduced debt by $168.7 million and ended fiscal 2026 with roughly $1.3 billion of available liquidity.

The company’s 56-year dividend-growth record is a major attraction, although the elevated payout ratio and uneven recent earnings warrant attention.

We project an 8.0% annual return, consisting mainly of the 6.3% yield, modest growth, and a small valuation tailwind.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on UVV.

Tobacco Stock #2: Philip Morris International (PM)

- 5-year expected returns: 8.9%

Philip Morris International sells cigarettes and smoke-free nicotine products around the world.

Its portfolio includes Marlboro outside the United States, IQOS heated-tobacco products, and ZYN nicotine pouches, which it acquired through Swedish Match.

PMI has built the strongest smoke-free platform among the large tobacco companies. That transformation gives it a better growth profile than most peers, although the shares also trade at a premium valuation and offer a lower dividend yield than several competitors.

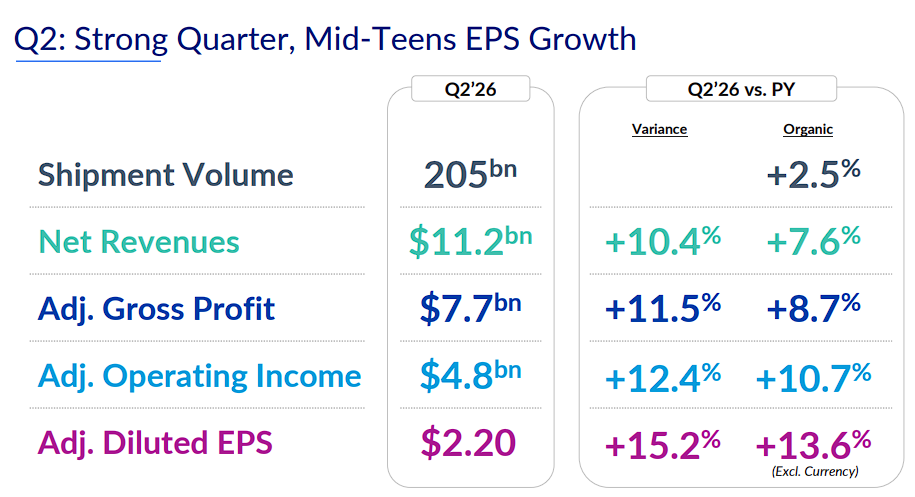

PMI’s second-quarter 2026 results showed continued momentum. Net revenue increased 10.4%, or 7.6% organically, to $11.2 billion.

Smoke-free product revenue rose 11.7% and represented 42% of total revenue. Adjusted diluted earnings per share increased 15.2% to $2.20.

IQOS heated-tobacco unit shipments rose 7.6%, while ZYN shipments grew 2% to 2.9 billion pouches.

Management raised its 2026 adjusted EPS outlook to $8.26 to $8.41.

During the quarter, the FDA issued modified-risk orders for 20 ZYN products, allowing Philip Morris to market them as presenting lower health risks than cigarettes.

The company also recorded a $511 million non-cash impairment related to its Canadian Rothmans, Benson & Hedges business.

PMI’s operating momentum is excellent, but its valuation creates a projected drag.

Nevertheless, we estimate an 8.9% annual return, supported by growth and dividends.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on PM.

Tobacco Stock #1: Turning Point Brands (TPB)

- 5-year expected returns: 9.6%

Turning Point Brands is a smaller, U.S.-focused tobacco and nicotine company. Its portfolio includes Zig-Zag rolling papers and related products, Stoker’s moist snuff and chewing tobacco, and an expanding Modern Oral segment.

The company does not have the scale or dividend yield of the global tobacco majors, but it offers a stronger growth profile. Modern Oral has become the driver of the investment case, while Zig-Zag and Stoker’s provide cash flow.

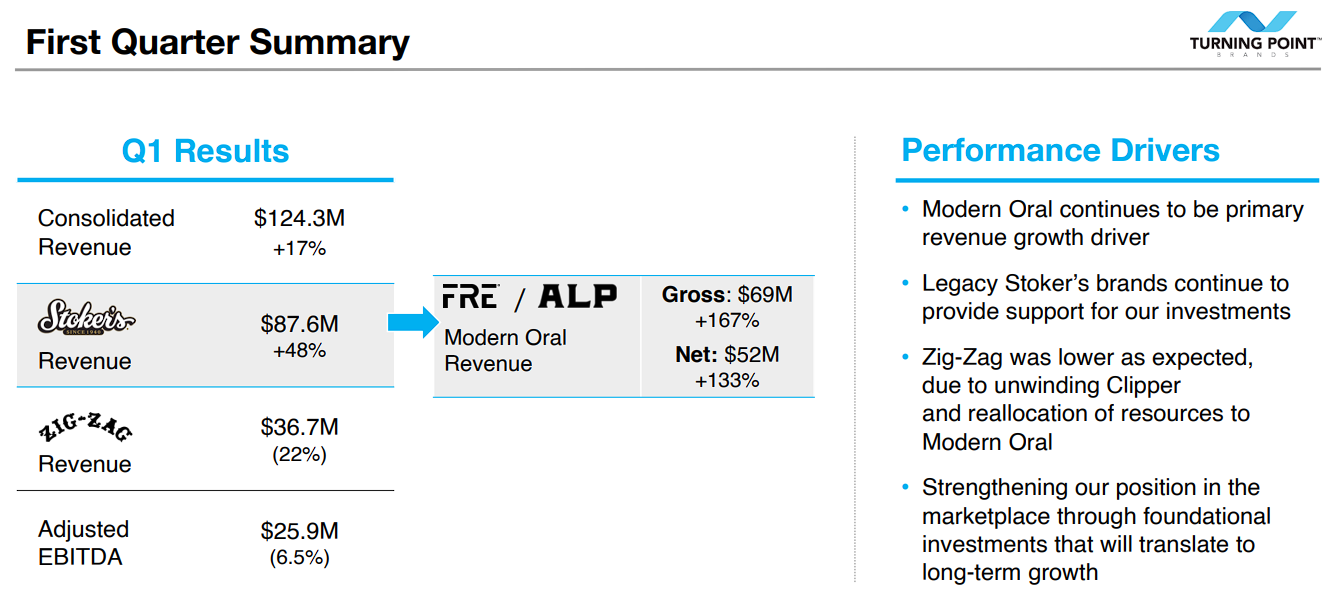

Turning Point’s first-quarter 2026 results demonstrated that tradeoff. Net sales rose 16.8% to $124.3 million, led by 133% growth in Modern Oral revenue to $52.0 million. Modern Oral represented 42% of company sales, up from 21% one year earlier.

However, adjusted EBITDA declined 6.5% to $25.9 million, and adjusted diluted earnings per share fell to $0.76 from $0.91, as management significantly increased marketing and growth investment.

Based on the strong start, Turning Point raised its 2026 Modern Oral gross-sales outlook to $280 million to $300 million and net-sales guidance to $210 million to $225 million.

Its partnership with TKO, including UFC-related marketing, should broaden awareness but also weighs on near-term margins.

TPB carries an A Dividend Risk Score, although its yield is only 0.4%.

We forecast 14% earnings-per-share growth, partly offset by valuation compression, for a 9.6% expected annual return—the highest among the six tobacco stocks covered.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on TPB.

Final Thoughts

Tobacco is not an easy industry to invest in. Cigarette volumes continue to decline, while tighter regulation and changing nicotine habits add another layer of uncertainty.

Even so, the leading companies still produce dependable cash flow and support generous shareholder returns.

The rankings show why yield alone does not tell the full story. BAT offers a high payout, but its valuation limits the upside. Turning Point ranks first because its Modern Oral business gives it a better growth outlook.

Philip Morris also stands out, mainly because of its strong smoke-free portfolio, although much of that strength is already reflected in the share price.

If you are focused on income, you may prefer Altria, Imperial Brands, Universal, or BAT. If you are looking for more growth, you may want to lean toward Philip Morris or Turning Point.

Still, given the risks across the sector, we recommend following developments closely and making sure you pay a reasonable price for these names.