Article updated on August 5th, 2026 by Nikolaos Sismanis

Spreadsheet data updated daily

The Dividend Aristocrats are an elite group of 69 S&P 500 stocks with 25+ years of consecutive dividend increases.

The requirements to be a Dividend Aristocrat are:

- Be in the S&P 500

- Have 25+ consecutive years of dividend increases

- Meet certain minimum size & liquidity requirements

This research report includes the following valuable free Dividend Aristocrats resources.

Resource #1: The Dividend Aristocrats Spreadsheet List

This spreadsheet contains important metrics, including: years of dividend growth, dividend yields, payout ratios, buy/hold/sell ratings, fair value prices, expected total returns, and much more.

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Resource #2: The 10 Best Dividend Aristocrats Today

This research report analyzes the 10 best Dividend Aristocrats now as ranked by expected total return. Expected total returns include estimated earnings-per-share growth, dividends, and the impact of any valuation multiple changes.

This ranking is best used as a research shortlist rather than an automatic buy list. Click on the links below to jump to analysis for any of the Top 10.

- #10: Automatic Data Processing (ADP)

- #9: PPG Industries (PPG)

- #8: Becton, Dickinson & Co. (BDX)

- #7: PepsiCo (PEP)

- #6: Pentair (PNR)

- #5: Amcor (AMCR)

- #4: Brown & Brown (BRO)

- #3: Albemarle (ALB)

- #2: S&P Global (SPGI)

- #1: FactSet Research Systems (FDS)

Resource #3: Sure Analysis Reports On All Dividend Aristocrats

We cover all 69 Dividend Aristocrats in the Sure Analysis Research Database. All are updated quarterly. This resource has links to our most recent stand-alone analysis on each of the Dividend Aristocrats.

Click here to jump to this resource now.

Resource #4: Historical Dividend Aristocrats List

We have compiled a comprehensive image of Dividend Aristocrats dating back to 1989.

Click here to jump to this resource now.

Please keep reading for our Dividend Aristocrats analysis.

Dividend Aristocrat #10: Automatic Data Processing (ADP)

- 5-Year Expected Total Return: 12.8%

Automatic Data Processing is a leading provider of payroll, human-capital management, benefits, and compliance solutions.

Its services are deeply embedded in customers’ daily operations, supporting high retention, recurring revenue, and attractive margins.

ADP serves more than 1.1 million clients across over 140 countries.

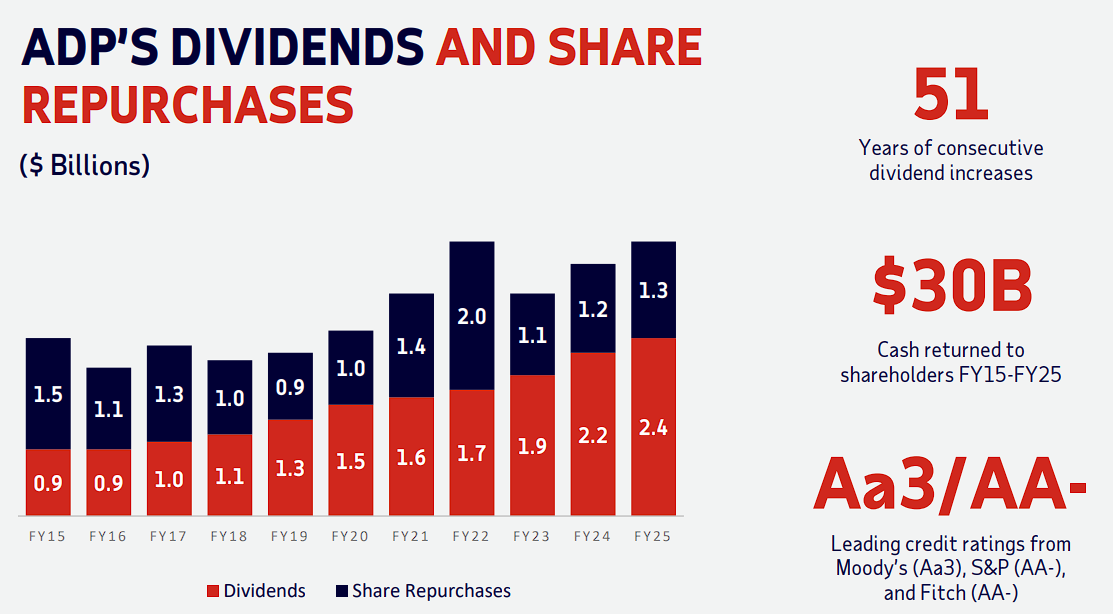

The company has also increased its dividend for 51 consecutive years, including a 10% increase to $1.70 per quarter, or $6.80 annualized.

Fiscal fourth-quarter 2026 revenue increased 7% to $5.47 billion.

Adjusted earnings per share rose to $2.64, while reported earnings per share increased to $2.45 from $2.23.

Management entered fiscal 2027 expecting revenue growth of 5% to 6% and adjusted earnings-per-share growth of 9% to 11%, reflecting continued operating leverage and the business’s resilience.

ADP’s growth strategy increasingly combines its large proprietary data set with artificial intelligence and next-generation platforms such as ADP Lyric.

The company is also integrating WorkForce Software to strengthen its global workforce-management capabilities.

Employment levels and client hiring activity can influence results, but recurring revenue and strong free cash flow limit volatility.

ADP’s yield is moderate, yet its combination of earnings growth, dividend growth, and a durable competitive position makes it a compelling long-term compounder.

Dividend Aristocrat #9: PPG Industries (PPG)

- 5-Year Expected Total Return: 14.2%

PPG Industries is one of the world’s largest coatings companies.

It supplies paints, coatings, and specialty materials to aerospace, automotive, industrial, packaging, and architectural customers.

Its technology, customer relationships, and global manufacturing footprint provide competitive advantages, although results remain exposed to industrial activity and raw-material inflation.

PPG recently raised its quarterly dividend from $0.71 to $0.74, extending its dividend-growth streak to 55 years. It has also paid dividends for 512 consecutive quarters.

Second-quarter 2026 net sales increased 7% to $4.50 billion.

Organic sales rose 4%, consisting of approximately 2% volume growth and 2% higher pricing.

Adjusted earnings-per-share edged up to $2.23 from $2.22, while year-to-date operating cash flow improved by roughly $220 million to nearly $600 million.

Management reaffirmed full-year adjusted earnings-per-share guidance of $7.70 to $8.10.

Performance was led by aerospace, packaging coatings, and Latin America, and eight of PPG’s nine businesses produced organic growth.

Pricing actions covered about 90% of cost inflation during the quarter, with full recovery expected by the fourth quarter.

That progress matters because margin improvement is central to the investment case.

PPG’s moderate payout ratio leaves room for further dividend increases as earnings and cash flow improve.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on PPG Industries (PPG).

Dividend Aristocrat #8: Becton, Dickinson & Co. (BDX)

- 5-Year Expected Total Return: 14.5%

Becton, Dickinson & Co. is a global medical-technology company whose products include needles, syringes, medication-management systems, catheters, and other essential healthcare supplies.

Much of its revenue is recurring because hospitals and laboratories continually consume these products.

BDX has increased its dividend for 54 consecutive fiscal years. The current quarterly payout is $1.05, or $4.20 annualized.

Second-quarter fiscal 2026 revenue increased 5.2% to $4.71 billion, or 2.6% on a currency-neutral basis.

Adjusted earnings-per-share were $2.90, up from a recast $2.79 in the prior-year period.

Management raised its full-year adjusted earnings-per-share outlook to $12.52 to $12.72.

The company also retired $2.1 billion of debt and initiated a $2 billion accelerated share-repurchase program, improving its capital structure following a major portfolio change.

That change was the separation of BD’s former Biosciences and Diagnostic Solutions operations and their combination with Waters.

The remaining company is more focused on medical essentials, connected care, biopharma systems, and interventional products.

The streamlined portfolio should improve BDX’s growth and margin profile over time, although execution and further debt reduction remain important.

The dividend consumes a manageable share of expected earnings, leaving room for continued annual increases even if near-term growth remains modest.

Dividend Aristocrat #7: PepsiCo (PEP)

- 5-Year Expected Total Return: 15.5%

PepsiCo owns a diversified portfolio of global snack and beverage brands, including Pepsi, Gatorade, Doritos, Lay’s, Quaker, and Cheetos.

Its scale, distribution network, and brand strength have produced durable cash flow across economic cycles.

PepsiCo has paid quarterly dividends since 1965 and has raised its annual payout for 54 consecutive years. The quarterly dividend is now $1.48, or $5.92 annualized, following a 4% increase.

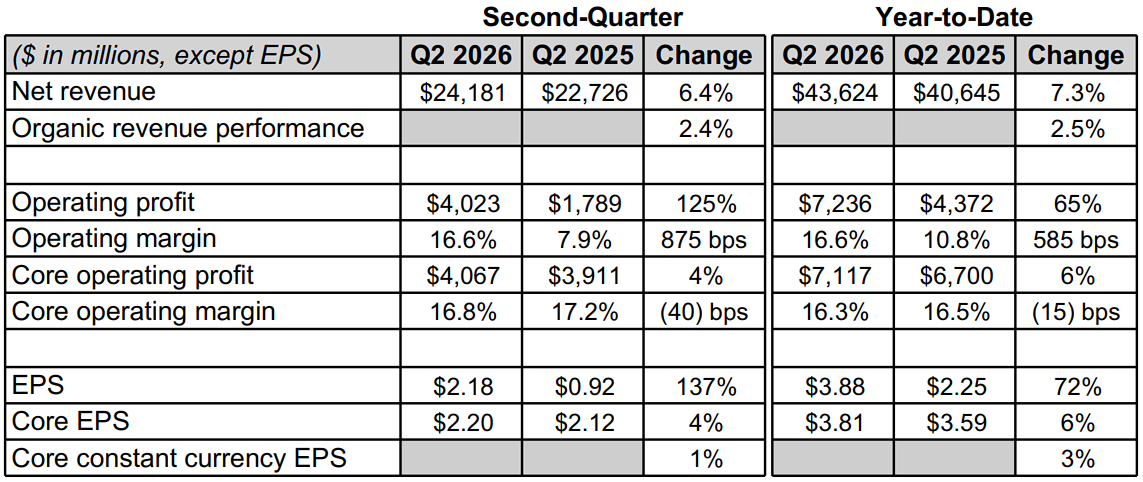

Second-quarter 2026 net revenue rose 6.4% to $24.18 billion. Core earnings-per-share were $2.20, while reported earnings-per-share were $2.18.

Constant-currency core earnings growth was modest, as productivity benefits and pricing were partly offset by input costs and uneven consumer demand.

Management nevertheless maintained its 2026 outlook for 2% to 4% organic revenue growth and 4% to 6% core constant-currency earnings-per-share growth.

The company is using automation, artificial intelligence, and a broad productivity program to simplify operations and improve margins.

These initiatives matter because North American consumers remain value-conscious, and restoring volume growth without excessive discounting is a key challenge.

PepsiCo offers one of the higher starting yields in this ranking, providing substantial income while management works to improve execution.

Its brand portfolio and geographic diversification remain significant strengths for long-term dividend investors.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on PepsiCo (PEP).

Dividend Aristocrat #6: Pentair (PNR)

- 5-Year Expected Total Return: 15.6%

Pentair provides water-treatment, flow-control, pool, and filtration products for residential, commercial, and industrial customers.

Its installed base creates recurring demand for replacement parts and aftermarket service, while long-term water-quality and efficiency needs support growth.

Pentair reached Dividend King status with its 50th consecutive annual increase, raising the quarterly dividend 8% to $0.27, or $1.08 annualized.

Near-term performance has been challenging. Preliminary second-quarter 2026 results called for sales of approximately $930 million, down 17% year over year, and adjusted earnings per share of about $1.12.

Pool-channel inventory destocking reduced estimated sales by roughly $170 million and segment income by about $105 million.

Management lowered its full-year sales outlook to a decline of 4% to 7% and adjusted earnings-per-share guidance to $4.60 to $4.80.

Flow and Water Solutions were generally in line with expectations.

The sharp disruption in Pool explains both the stock’s elevated expected return and its recovery potential.

Pentair repurchased approximately $150 million of shares during the quarter, and its board has authorized a new $1 billion repurchase program.

A normalization of distributor inventories could drive a meaningful rebound.

Meanwhile, the low payout ratio leaves ample room for continued dividend increases while management works through the inventory correction.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on Pentair (PNR).

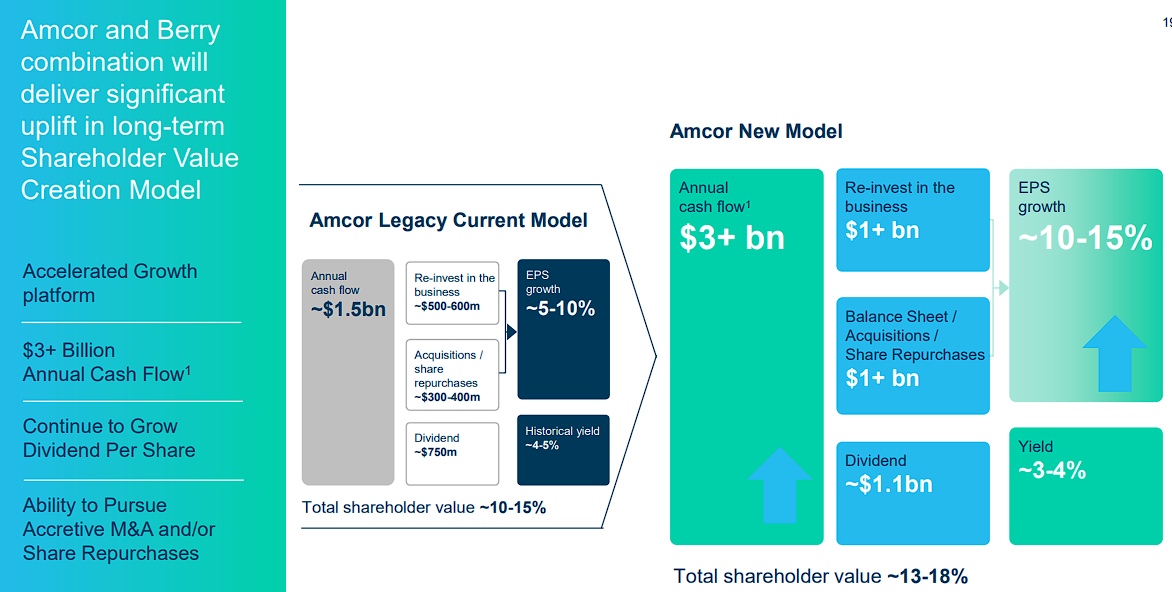

Dividend Aristocrat #5: Amcor (AMCR)

- 5-Year Expected Total Return: 16.0%

Amcor is a global packaging company serving food, beverage, healthcare, personal-care, and other consumer markets.

Demand for packaging tends to be relatively defensive, while the company’s scale and customer relationships support recurring volumes.

Amcor has increased its dividend for 42 consecutive years, including predecessor history.

Following its one-for-five reverse stock split, the current quarterly dividend is $0.65 per share, equivalent to $2.60 annually.

Fiscal third-quarter 2026 net sales increased 77% to $5.91 billion, primarily due to the Berry Global acquisition.

Adjusted EBITDA rose 87% to $892 million, adjusted EBITDA margin expanded to 15.1% from 14.3%, and adjusted earnings per share increased 6% to $0.96.

Amcor generated $77 million of acquisition synergies during the quarter, reaching the upper end of management’s expectations.

Integrating Berry is now the central driver of the investment case.

Management raised its full-year synergy expectation to approximately $270 million, while guiding for core earnings per share of $3.98 to $4.03 and free cash flow of $1.5 billion to $1.6 billion.

The larger platform should create purchasing, manufacturing, and commercial efficiencies, but leverage remains elevated, and volumes have been soft.

Successful integration and debt reduction could unlock meaningful upside, while the high dividend provides investors with a substantial return during that process.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on Amcor (AMCR).

Dividend Aristocrat #4: Brown & Brown (BRO)

- 5-Year Expected Total Return: 18.0%

Brown & Brown is one of the largest U.S. insurance brokerages.

The company earns commissions and fees by connecting customers with insurers, creating a capital-light business with recurring revenue and strong cash generation.

Acquisitions have supplemented steady organic expansion for decades.

Brown & Brown has increased its dividend for 32 consecutive years, and the current quarterly payment is $0.165 per share.

Second-quarter 2026 revenue increased 30.4% to $1.68 billion, primarily reflecting acquired businesses.

Net income rose 24.7% to $288 million, while adjusted earnings per share increased 3.9% to $1.07.

Adjusted EBITDAC grew 27% to $598 million, with a 35.7% margin.

Organic revenue declined 0.7%, although organic revenue including contingent commissions increased 0.7%, highlighting a softer underlying insurance-pricing environment.

The major development remains the integration of Accession Risk Management, which significantly expanded Brown & Brown’s scale and capabilities.

The transaction is driving strong reported growth, but the company must convert that added scale into renewed organic expansion and preserve margins as integration spending continues.

Brown & Brown’s dividend yield is low, yet its payout ratio is also very conservative.

That combination leaves considerable capacity for further dividend growth, acquisitions, and internal investment as operating momentum improves.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on Brown & Brown (BRO).

Dividend Aristocrat #3: Albemarle (ALB)

- 5-Year Expected Total Return: 20.6%

Albemarle is a leading producer of lithium and specialty chemicals used in electric vehicles, energy storage, semiconductors, flame retardants, and pharmaceuticals.

Its large resource base provides substantial long-term growth potential, but earnings can fluctuate sharply with lithium prices.

Albemarle has increased its dividend for 30 consecutive years. The quarterly payout is $0.405 per share, or $1.62 annualized.

First-quarter 2026 sales increased 33% to $1.43 billion as higher pricing and volumes benefited Energy Storage and Specialties.

Adjusted EBITDA surged 148% to $664 million, while adjusted earnings per share improved to $2.95 from a loss of $0.18.

Free cash flow was $248 million, supported by stronger earnings and lower capital spending.

Energy Storage sales increased 70%, reflecting 51% higher pricing and 14% volume growth.

Albemarle also completed the sales of its Eurecat joint venture and a controlling stake in Ketjen for combined net proceeds of $648 million.

Those proceeds helped fund $1.3 billion of debt reduction, lowering net leverage to approximately 1.0 times adjusted EBITDA.

The company’s expected return reflects both improving fundamentals and continued lithium-price sensitivity.

Cost reductions, a stronger balance sheet, and long-term battery demand create meaningful upside if lithium markets remain firm, while the dividend provides an additional element of shareholder return.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on Albemarle (ALB).

Dividend Aristocrat #2: S&P Global (SPGI)

- 5-Year Expected Total Return: 21.7%

S&P Global provides credit ratings, financial data, indices, benchmarks, and commodity-market intelligence.

Its businesses benefit from trusted brands, recurring subscription revenue, high switching costs, and network effects.

The company has paid a dividend every year since 1937 and has increased it for 53 consecutive years. The quarterly payout recently rose 1% to $0.97, or $3.88 annualized.

Second-quarter 2026 revenue increased 10% to $4.15 billion. Operating profit rose 17% to $1.81 billion, net income increased 14% to $1.22 billion, and diluted earnings per share advanced 18% to $4.12.

On a pro forma basis excluding Mobility, revenue grew 11% and adjusted earnings per share increased 23% to $4.83, illustrating the strength of the remaining portfolio.

S&P Global completed the spin-off of its Mobility business in July, creating a more focused company centered on data, analytics, ratings, and benchmarks.

Management expects mid-to-high-single-digit revenue growth and continued margin expansion, and it plans more than $7 billion of share repurchases in 2026.

Capital-markets activity can cause short-term volatility in Ratings, but recurring revenue across the broader portfolio provides stability.

The dividend yield is low, so the investment thesis relies primarily on earnings growth, buybacks, and valuation recovery.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on S&P Global (SPGI).

Dividend Aristocrat #1: FactSet Research Systems (FDS)

- 5-Year Expected Total Return: 23.2%

FactSet Research Systems provides financial data, analytics, workflow tools, and enterprise solutions to investment managers, banks, wealth managers, and corporations.

Its products are embedded in customers’ daily processes, producing recurring subscription revenue and retention above 95%.

FactSet increased its quarterly dividend 5.5% to $1.16 in May, marking its 27th consecutive year of dividend growth.

Fiscal third-quarter 2026 revenue increased 6.4% to $622.9 million, while organic revenue grew 7.0%. Adjusted earnings per share reached $4.53.

Organic annual subscription value increased 7.1% to $2.49 billion, marking a fifth consecutive quarter of acceleration, while the user count rose 12.4% to 247,766.

Adjusted operating margin declined to 34.0% from 36.8% because of higher compensation and technology spending.

FactSet is investing heavily in artificial intelligence, cloud infrastructure, and new data solutions to automate more of its clients’ research and investment workflows.

These expenses are weighing on margins today, but they should strengthen the platform’s value and support faster subscription growth over time.

The company continues to benefit from high switching costs and a capital-light model, leaving ample cash for dividends, buybacks, and product development.

FactSet’s combination of a depressed valuation, accelerating subscription growth, and rising dividends gives it the highest expected return among the current Dividend Aristocrats.

Deep Dive: Click here to download (for free) our most recent 3-Page Sure Analysis PDF report on FactSet Research Systems (FDS).

Sure Analysis Reports On All Dividend Aristocrats

You can download (for free) the most recent 3-page PDF Sure Analysis Research Database report for every Dividend Aristocrat at the links below. The Dividend Aristocrats are organized by sector for easy access.

Consumer Staples

- Archer-Daniels-Midland (ADM)

- Amcor (AMCR)

- Brown-Forman (BF-B)

- Colgate-Palmolive (CL)

- Church & Dwight (CHD)

- Clorox (CLX)

- Coca-Cola (KO)

- Hormel Foods (HRL)

- J.M. Smucker (SJM)

- Kimberly-Clark (KMB)

- McCormick & Company (MKC)

- PepsiCo (PEP)

- Procter & Gamble (PG)

- Sysco Corporation (SYY)

- Target (TGT)

- Walmart (WMT)

Industrials

- Automatic Data Processing (ADP)

- A.O. Smith (AOS)

- C.H. Robinson Worldwide (CHRW)

- Cintas (CTAS)

- Dover (DOV)

- Emerson Electric (EMR)

- Expeditors International (EXPD)

- Fastenal Co. (FAST)

- Illinois Tool Works (ITW)

- Nordson Corporation (NDSN)

- Pentair (PNR)

- Roper Technologies (ROP)

- Stanley Black & Decker (SWK)

- W.W. Grainger (GWW)

- General Dynamics (GD)

- Caterpillar (CAT)

Financials

- Aflac (AFL)

- Brown & Brown (BRO)

- Cincinnati Financial (CINF)

- Erie Indemnity (ERIE)

- FactSet Research Systems (FDS)

- Franklin Resources (BEN)

- S&P Global (SPGI)

- T. Rowe Price Group (TROW)

- Chubb (CB)

Health Care

- Abbott Laboratories (ABT)

- AbbVie (ABBV)

- Becton, Dickinson & Company (BDX)

- Cardinal Health (CAH)

- Johnson & Johnson (JNJ)

- Kenvue Inc. (KVUE)

- Medtronic (MDT)

- West Pharmaceutical Services (WST)

Materials

- Air Products and Chemicals (APD)

- Albemarle (ALB)

- Ecolab (ECL)

- PPG Industries (PPG)

- Sherwin-Williams (SHW)

- Nucor (NUE)

- Linde (LIN)

Consumer Discretionary

Energy

Real Estate

Utilities

Information Technology

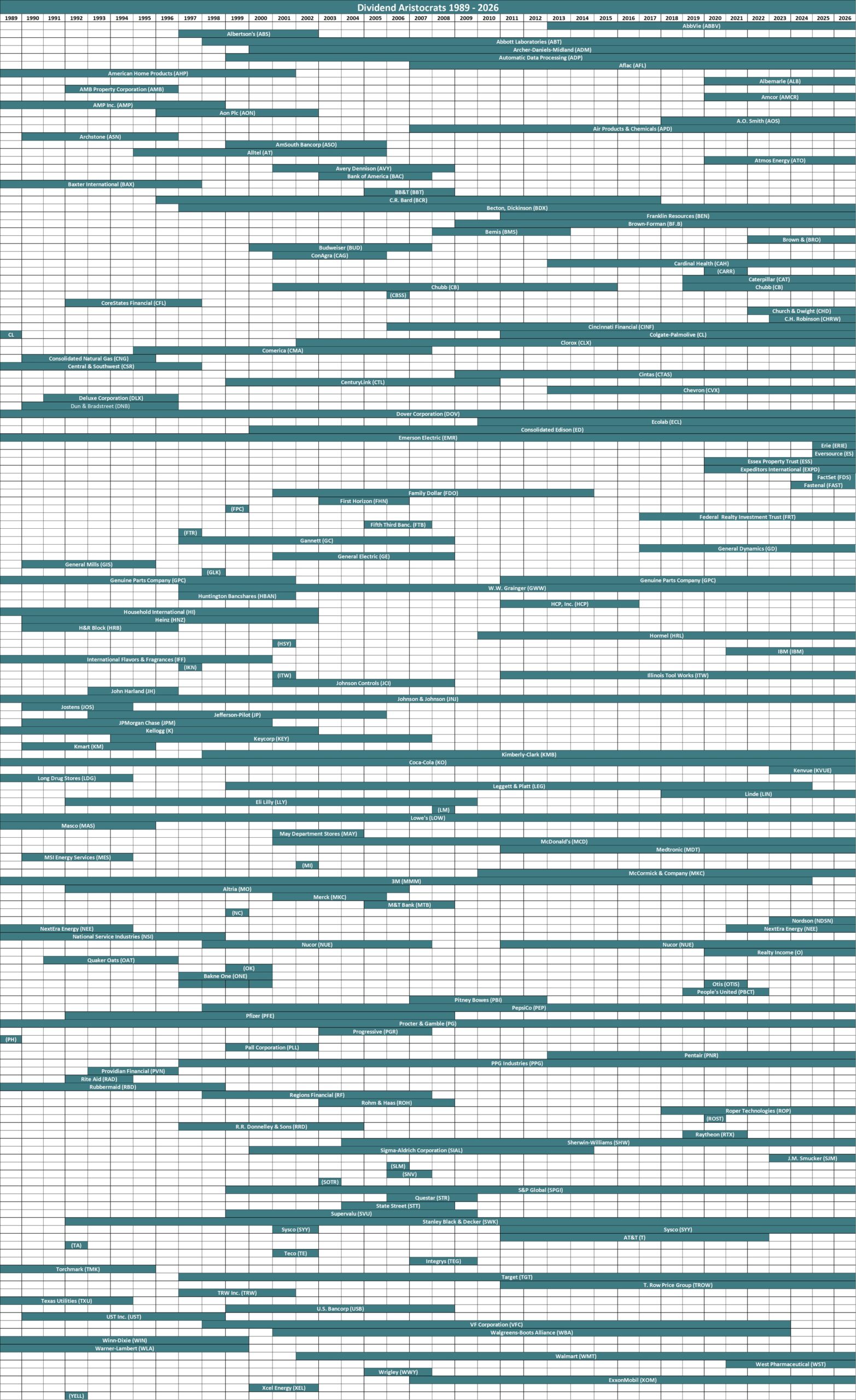

Historical Dividend Aristocrats List

(1989 – 2026)

The image below shows the history of the Dividend Aristocrats Index from 1989 through 2026.

Note: CL, GPC, and NUE were all removed and re-added to the Dividend Aristocrats Index through the historical period analyzed above. We are unsure as to why. Companies created via a spin-off (like AbbVie) can be Dividend Aristocrats with less than 25 years of rising dividends if the parent company was a Dividend Aristocrat.

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet and image below is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

This information was compiled from the following sources:

- 1989 – 1991: Dividend Growth Investor

- 1992 – 2015: NOBL Index Historical Constituents

- 2016: Sure Dividend update

- 2017 – 2026: Data from S&P press releases and tracking dividends

Final Thoughts

The Dividend Aristocrats are already a highly selective group.

Each company has increased its dividend for at least 25 consecutive years while also meeting the S&P 500’s size and liquidity requirements.

Their track records imply that they have passed the test of time, raising their dividends through recessions, inflationary periods, market crashes, and major industry changes.

That durability does not eliminate risk, but it provides strong evidence of resilient business models and shareholder-friendly capital allocation.

The 10 Aristocrats highlighted above also offer several different paths to attractive returns.

PepsiCo stands out for its combination of defensive demand and income, while Amcor offers a higher starting yield.

ADP, FactSet, and S&P Global are particularly well suited to long-term compounding through recurring revenue and steady earnings growth.

Brown & Brown adds an asset-light growth profile, while Albemarle and PPG Industries offer greater recovery potential if their cyclical headwinds ease.

Becton, Dickinson provides healthcare stability, and Pentair benefits from durable water-management demand.

If purchased at reasonable prices (and our analysis indicates that several are currently undervalued) their combination of earnings growth, rising dividends, and potential valuation expansion could produce strong long-term returns.

Additional dividend-stock resources include:

- The Dividend Kings List: stocks with at least 50 consecutive years of dividend growth.

- The High Dividend Stocks List: stocks with dividend yields of 4% or more.

- The Monthly Dividend Stocks List: stocks that make 12 dividend payments per year.