Updated on March 4th, 2026 by Nathan Parsh

Every year, we individually review all the Dividend Aristocrats. We view them as particularly appealing stocks for long-term dividend growth investors.

The Dividend Aristocrats are a select group of stocks in the S&P 500 that have had 25+ years of consecutive dividend increases.

You can see a full downloadable spreadsheet of all 69 Dividend Aristocrats, along with several important financial metrics such as price-to-earnings ratios, by clicking on the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

The next Dividend Aristocrat in our 2026 series is A.O. Smith (AOS), which has increased its dividend for 32 consecutive years.

This article will discuss A.O. Smith’s business model, growth prospects, and valuation.

Business Overview

A.O. Smith is a leading manufacturer of residential and commercial water heaters, boilers, and water treatment products. Two-thirds of its sales are in North America, and most of the balance are in China.

A.O. Smith was founded in 1874 and is headquartered in Milwaukee, WI. The company generates annual sales above $3.8 billion.

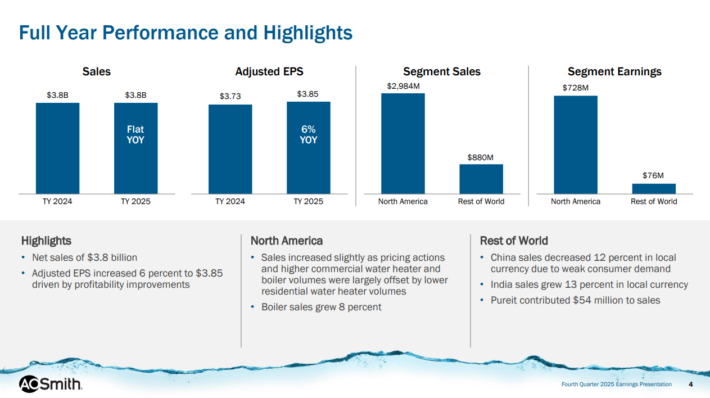

The company reported fourth-quarter earnings results on January 29th, 2026.

Source: Investor Presentation

For the quarter, revenue was unchanged at $913 million. North America sales improved a solid 3% while the international business suffered a revenue decline of 13%, mainly due to China sales being weaker.

A.O. Smith generated earnings-per-share of $0.90 during the quarter, which was a 6% improvement year-over-year. Flat revenues turned into very solid earnings growth thanks to higher margins and stock buybacks.

For the year, revenue inched higher by 0.3% to $3.83 billion while earnings-per-share of $3.85 compared to $3.73 in 2024.

North America sales were up 1% to $2.98 billion. Growth was driven by pricing and higher boiler and commercial water heater sales, offset by weaker residential water heater volumes. The Rest of the World segment fell 4% to $880 million due to much lower customer demand in China while India grew 13% and outpaced the market.

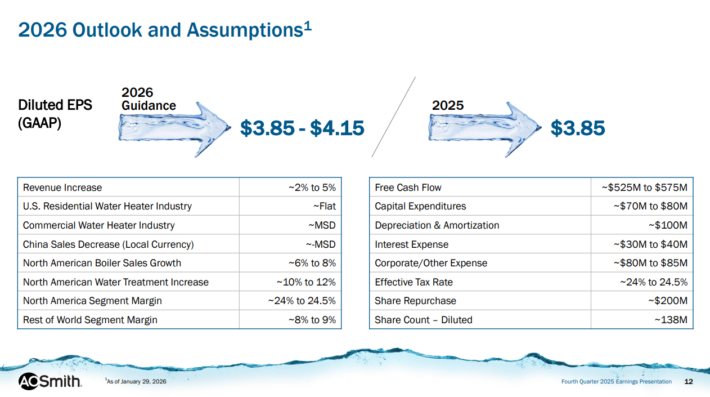

A.O. Smith also provided an outlook for 2026. The company forecasts earnings-per-share to be in a range of $3.85 to $4.15 for the year. At the midpoint, this would represent growth of 3.9% from 2025.

Growth Prospects

A.O. Smith’s growth catalysts in the U.S. include continued economic growth and increasing housing prices. As a manufacturer of water heating, water treatment, and air purification products, the company is reliant on a financially healthy consumer and housing market.

When home prices are rising, and unemployment is low, consumers with disposable income are much more willing to invest in upgrades like new water heaters.

The company has enjoyed consistent growth in the domestic market throughout most of the last decade.

Emerging markets such as China are set to drive A.O. Smith’s growth.

Source: Investor Presentation

China’s huge population, robust GDP growth, and booming middle class are major tailwinds in this important market even with weaker results last year. In addition, thanks to the country’s severe pollution, the demand for air purifiers should remain strong.

We expect A.O. Smith to grow earnings-per-share at a rate of 6% per year through 2031. The company should be able to achieve at least this level of growth due to organic revenue growth and share repurchases, with potential additional acquisitions adding further growth.

Competitive Advantages & Recession Performance

A.O. Smith’s strong growth is due to its competitive advantages, primarily its top market share. A.O. Smith has the #1 market share in U.S. water heaters. It holds over 30% of the domestic residential market share and over 40% of the commercial market share.

Possessing the top industry position gives A.O. Smith pricing power and high margins. In turn, this allows the company to generate a lot of cash flow, which enables it to invest in new product innovation.

One potential risk for A.O. Smith is a recession. As a manufacturer, the company is closely tied to the overall economy’s health. It is not a highly recession-resistant business model.

Earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share of $0.48

- 2008 earnings-per-share of $0.49 (2% increase)

- 2009 earnings-per-share of $0.57 (16% increase)

- 2010 earnings-per-share of $0.43 (25% decline)

- 2011 earnings-per-share of $0.60 (39% increase)

As you can see, the company performed very well during 2008 and 2009, the worst years of the recession. Earnings took a significant hit in 2010 but quickly recovered in 2011.

Overall, the company performed exceptionally well, since it was still able to grow earnings over the course of the recession.

Valuation & Expected Returns

Based on the current share price of ~$74 and the midpoint of 2026 EPS guidance of $4.00, A.O. Smith shares currently trade for a price-to-earnings ratio of 18.5. We believe a price-to-earnings multiple target of 19 is an appropriate fair value estimate for A.O. Smith’s stock.

As a result, A.O. Smith seems undervalued right now. If the P/E multiple were to increase to the fair value estimate of 19, it would increase annual returns by 0.5% over the next five years.

Earnings growth of 6% and the starting dividend yield of 1.9% will also boost shareholder returns, which together possible multiple expansion add up to 8.4% annualized returns over the next five years. Given the company’s strong dividend growth history and solid potential rate of return, we rate shares of A.O. Smith as a buy.

Final Thoughts

A.O. Smith is an industry-leading company. It has the top brand in its category, with compelling future growth potential. Its dominant market share of its industry allows the company to continue to overcome short-term difficulties. Over the long term, we believe the potential growth opportunities in emerging markets are highly attractive.

While the dividend yield is low, the company’s dividend growth pace and track record are impressive. The stock’s valuation also remains below our target. As a result, we view A.O. Smith as a relatively attractive stock to purchase.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: