Updated on March 4th, 2026 by Felix Martinez

The Dividend Aristocrats are some of the best dividend stocks an investor will find. They are S&P 500 companies with 25+ consecutive years of dividend increases.

We believe the Dividend Aristocrats are among the highest-quality dividend growth stocks around. For this reason, we created a downloadable spreadsheet of all 69 Dividend Aristocrats, along with important metrics such as price-to-earnings ratios and dividend yields.

You can download the Excel sheet of all 69 Dividend Aristocrats by clicking the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

Each year, we review all of the Dividend Aristocrats. The next stock in the series is an insurance broker giant, Brown & Brown Inc. (BRO). BRO might not be a familiar stock for most investors, but it has certainly earned its place on the list.

BRO has now increased its dividend for 31 consecutive years. This article will discuss the company’s business model, growth outlook, and whether we view it as a buy today.

Business Overview

Brown & Brown Inc. is a leading insurance brokerage firm that provides risk management solutions to both individuals and businesses, with a focus on property & casualty insurance. Brown & Brown has a notably high level of insider ownership.

The company employs about 17,000 people and generated about $5.7 billion in revenue last year. It operates through four segments: Retail, National Programs, Wholesale Brokerage, and Services.

The company has been diversifying its business segments over the years, allowing it not to be 100% dependent on any single segment. Thus, these segments have performed very well relative to their peers, enabling BRO to achieve “best of breed” status in its industry.

Brown & Brown’s competitive advantage stems from its willingness to execute small, frequent acquisitions. This growth-by-acquisition strategy gives the company an enduring opportunity to continue growing its business for the foreseeable future.

Growth Prospects

Brown & Brown has a remarkable growth track record, including a decade-long compound annual earnings growth rate of more than 14%. The company’s book value per common share has grown at a similar rate, increasing by ~11% per year over the last 10 years.

The growth strategy is both simple and sustainable. Over the years, the company has actively acquired smaller insurance brokerage firms and integrated them into its broader operations.

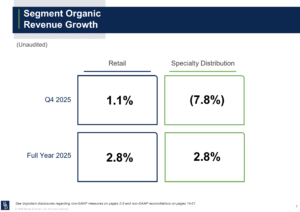

Brown & Brown posted fourth-quarter and full-year financial results on January 26th, 2025. The company reported strong top-line growth in Q4 2025, with revenue rising 35.7% to $1.6B, primarily driven by acquisitions, though organic revenue declined 2.8%. Net income increased 25.7% to $264M, while adjusted diluted EPS rose 8.1% to $0.93.

However, reported diluted EPS fell 19.2% to $0.59, reflecting the impact of acquisitions and share dilution. Adjusted EBITDAC increased 35.6% to $529M, with margins steady at 32.9%.

For full-year 2025, revenue grew 22.8% to $5.9B, with organic revenue up 2.8%. Net income rose 6.1% to $1.05B, and adjusted diluted EPS increased 10.9% to $4.26, despite reported diluted EPS declining 8.7% to $3.16.

Adjusted EBITDAC climbed 25.6% to $2.1B, and margins improved to 35.9%, reflecting scale benefits from acquisitions, including the Accession deal.

The company significantly expanded its balance sheet following acquisition activity, with total assets increasing to $30.0B from $17.6B in 2024. Operating cash flow reached $1.45B, while investing cash outflows of $7.9B primarily funded acquisitions. Management highlighted 2025 as a transformational year marked by strong adjusted earnings growth, margin resilience, and strategic expansion.

Source: Investor Presentation

We start 2026 with a strong earnings-per-share growth estimate of $4.50, as the company continues to see robust revenue growth, driving expanding margins.

We expect BRO to generate 9% annual earnings-per-share growth over the next five years.

Competitive Advantages & Recession Performance

Brown & Brown’s competitive advantage stems from its willingness to execute small, frequent acquisitions. This growth-by-acquisition strategy gives the company an enduring opportunity to continue growing its business for the foreseeable future.

BRO is also modestly recession-resistant. For example, BRO’s competitive advantages allow it to maintain consistent profitability each year, even during recessions.

BRO’s earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share of $0.68

- 2008 earnings-per-share of $0.59 (13% decline)

- 2009 earnings-per-share of $0.54 (8% decline)

- 2010 earnings-per-share of $0.56 (4% increase)

Further, during the COVID-19 pandemic, earnings grew from $1.40 per share in 2019 to $1.67 per share in 2020, representing a 19% increase year over year.

Source: Investor Presentation

Valuation & Expected Returns

Based on our expected 2026 EPS of $4.50, BRO stock trades at a price-to-earnings ratio of 16x, using today’s stock price of ~$72. BRO’s average price-to-earnings ratio was 23 over the past 10 years.

Today’s multiple is undervalued to our fair P/E of 24x, implying shares appear undervalued at their current price levels.

If the stock’s valuation multiple increases to our fair P/E of 24.0x, annual shareholder returns would increase by 8.4% over the next five years.

Also, earnings growth and dividends will positively impact future returns. First, we expect the company’s earnings per share to grow by 9% per year through 2031.

The stock also has a dividend yield of 0.9%. Putting it all together, a breakdown of our expected future returns is as follows:

- 9.0% expected earnings-per-share growth

- 0.9% dividend yield

- 8.4% multiple expassion

In this projection, total annualized shareholder returns could reach 18.3% through 2031. This is a good expected rate of return for this company.

Final Thoughts

BRO has endured a number of challenges over the past decade, including the Great Recession of 2008-2009 and the coronavirus pandemic of 2020. And yet, it continued to raise its dividend each year. Very few companies have this ability, making it a rare dividend growth stock.

BRO has a leadership position in the insurance industry and durable competitive advantages. These factors have positioned the company for growth in future years, making it highly likely that the company will continue to increase its dividend.

The company is a high-quality business and a dividend growth company. While the stock is undervalued, its low multiple helps it earn a buy rating from Sure Dividend at this time. Accordingly, we have assigned the stock a buy rating at its current price.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: