Updated on Febuaury 18th, 2026 by Felix Martinez

The Dividend Aristocrats are among the best dividend-growth stocks available to investors. These companies are in the S&P 500 Index and have had 25+ consecutive years of dividend increases.

We believe the Dividend Aristocrats are among the highest-quality dividend-growth stocks. For this reason, we created a downloadable spreadsheet of all 69 Dividend Aristocrats, along with important metrics such as price-to-earnings ratios and dividend yields.

You can download the Excel sheet of all 69 Dividend Aristocrats by clicking the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

We review all of the Dividend Aristocrats each year. The next stock in the series is consumer staple giant Church & Dwight Co., Inc. (CHD).

Church & Dwight may not be as well-known as some of its consumer-staple competitors, such as Procter & Gamble (PG), Clorox (CLX), or Colgate-Palmolive (CL).

However, Church & Dwight has now increased its dividend for 30 consecutive years. The company’s dividend is also very safe.

This article will discuss Church & Dwight in greater detail.

Business Overview

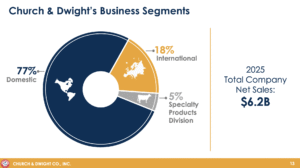

Church & Dwight is a diversified consumer staples company that manufactures and distributes products under several well-known names like Arm & Hammer, Trojan, OxiClean, Spinbrush, First Response, Waterpik, Nair, Orajel, and XTRA. The company was founded in 1846 and generates over $5 billion in annual revenue.

For more than 100 years, Church & Dwight was a baking soda company operating with only the Arm & Hammer brand. However, since 2001, the Company has acquired 13 of its 14 “power brands.”

Church & Dwight’s acquisitions of leading brands have diversified its reach across the household and personal care space. Also, Church & Dwight has paid quarterly dividends to shareholders for more than 120 years.

Source: Investor Presentation

Church & Dwight posted fourth-quarter earnings on January 30, 2026. The company delivered a solid Q4 2025, beating expectations with adjusted EPS of $0.86 (+11.7% YoY) and revenue of $1.64B (+3.9%). Adjusted gross margin expanded 90 bps to 45.5%, driven by productivity gains, favorable mix, and higher volumes, more than offsetting inflation and tariffs.

Organic sales grew 0.7% (about 1.8% excluding the exited vitamin business), with strength in International (+3.6% organic) and Specialty Products (+2.8%). Cash from operations surged 24% to $363M in the quarter, supporting continued brand investment and share repurchases.

For full-year 2025, Church & Dwight posted revenue of $6.2B (+1.6%), adjusted EPS of $3.53 (+2.6%), and operating cash flow of $1.22B (+5%), exceeding guidance despite portfolio exits. Looking ahead to 2026, management expects organic sales growth of 3–4%, ~100 bps gross margin expansion, and adjusted EPS growth of 5–8%, with reported sales down modestly due to divestitures.

Growth is expected to be driven by innovation (THERABREATH, HERO, ARM & HAMMER, TOUCHLAND), international expansion, and disciplined cost management, positioning the company for accelerating earnings momentum in the back half of 2026.

Growth Prospects

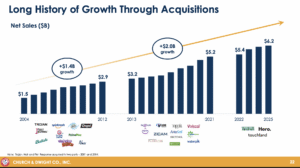

The biggest growth drivers for Church & Dwight will be continued organic sales growth and future acquisitions of strong brands. Acquisitions have been a major driver in the company’s historical growth.

Source: Investor Presentation

We believe it can achieve this, with average revenue growth in the mid-single digits and a small productivity gain helping to drive margins higher.

We also note that pandemic-related supply chain constraints have eased, and Church & Dwight has seen consistent margin improvement in recent results.

Competitive Advantages & Recession Performance

Church & Dwight’s competitive advantage stems from its willingness to pursue both acquisitions and organic growth. This growth-by-acquisition strategy gives the company an enduring opportunity to continue growing its business for the foreseeable future.

CHD is also modestly recession-resistant. For example, Church & Dwight’s competitive advantages enable it to maintain consistent profitability year over year, even during recessions.

Church & Dwight’s earnings-per-share during the Great Recession are below:

- 2007 earnings-per-share of $0.63

- 2008 earnings-per-share of $0.72 (13% increase)

- 2009 earnings-per-share of $0.87 22% increase)

- 2010 earnings-per-share of $0.99 (14% increase)

During the COVID-19 pandemic, earnings per share rose from $2.47 in 2019 to $2.83 in 2020, a 15% year-over-year increase.

CHD’s dividend payout is also recession-proof. Church & Dwight’s payout ratio has drifted below 40% in recent years. The dividend has been growing slightly more slowly than earnings per share, so over time, we expect the payout ratio to remain below 40% as the company continues to deliver meaningful earnings growth.

Valuation & Expected Returns

Based on the expected EPS of $3.75 for 2026, Church & Dwight’s stock trades for a price-to-earnings ratio of 26.4x. Over the past 10 years, CHD has averaged a price-to-earnings ratio of ~26.

We estimate a fair earnings multiple of 28.0. Consequently, based on its average valuation multiples, Church & Dwight’s stock appears to be undervalued.

If the company’s stock valuation multiple rises to our fair P/E of 28.0, it will increase annual shareholder returns by 0.8% over the next five years.

Earnings growth and dividends will positively impact future returns. First, we expect CHD to grow earnings per share by 7% per year over the next five years.

Lastly, CHD stock has a 1.2% dividend yield. Putting it all together, a breakdown of our expected future returns is as follows:

- 7.0% expected earnings-per-share growth

- 1.2% dividend yield

- 0.8% return from valuation expansion

In this projection, total shareholder returns could reach 9% annualized over the next five years.

Final Thoughts

Church & Dwight has many of the characteristics of a high-quality dividend investment. Most notably, the company’s portfolio of brands enables it to grow earnings in most years, regardless of the economic cycle.

Also, Church & Dwight shares its growth with its shareholders through consistent dividend increases.

The company’s growth-through-acquisition strategy is time-tested, and its management team has developed considerable expertise in scaling smaller brands through its existing infrastructure.

We forecast total returns accruing at 9% annually, giving CHD stock a hold rating.

Additionally, the following Sure Dividend databases contain the most reliable dividend growers in our investment universe:

- The Dividend Contenders List: 10-24 consecutive years of dividend increases.

- The Dividend Challengers List: 5-9 consecutive years of dividend increases.

- The Dividend Champions: Dividend stocks with 25+ years of dividend increases, including those that may not qualify as Dividend Aristocrats.

- The Dividend Achievers: dividend stocks with 10+ years of consecutive dividend increases.

- The Dividend Kings: considered to be the ultimate dividend growth stocks, the Dividend Kings list is comprised of stocks with 50+ years of consecutive dividend increases

If you’re looking for stocks with unique dividend characteristics, consider the following Sure Dividend databases:

- The Complete List of Monthly Dividend Stocks: stocks that pay dividends each month, for 12 payments over the year.

- The Blue Chip Stocks List: this database contains stocks that qualify as either Dividend Achievers, Dividend Aristocrats, or Dividend Kings.

The major domestic stock market indices are another solid resource for finding investment ideas. Sure Dividend compiles the following stock market databases and updates them monthly: