Article updated on July 6th, 2026 by Bob Ciura

Spreadsheet data updated daily

The Dividend Aristocrats are a select group of 69 S&P 500 stocks with 25+ years of consecutive dividend increases.

They are the ‘best of the best’ dividend growth stocks. The Dividend Aristocrats have a long history of outperforming the market.

The requirements to be a Dividend Aristocrat are:

- Be in the S&P 500

- Have 25+ consecutive years of dividend increases

- Meet certain minimum size & liquidity requirements

There are currently 69 Dividend Aristocrats. You can download an Excel spreadsheet of all 69 (with metrics that matter such as dividend yields and price-to-earnings ratios) by clicking the link below:

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

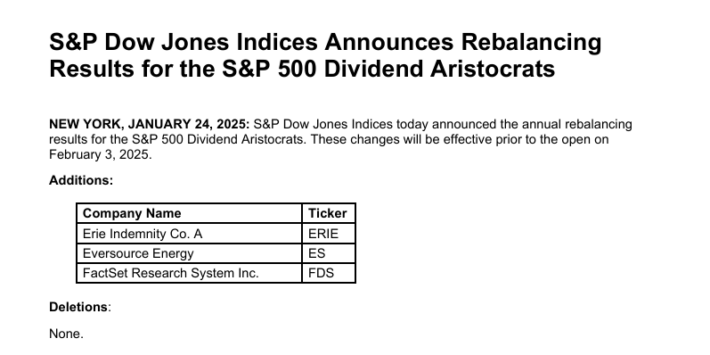

Note 1: On January 24th, 2025, Erie Indemnity (ERIE), Eversource Energy (ES), and FactSet Research System (FDS) were added to the list with no deletions, leaving 69 Dividend Aristocrats.

Source: S&P News Releases.

You can see detailed analysis on all 69 further below in this article, in our Dividend Aristocrats In Focus Series. Analysis includes valuation, growth, and competitive advantage(s).

Table of Contents

- How To Use The Dividend Aristocrats List To Find Dividend Investment Ideas

- Performance of the Dividend Aristocrats

- Sector Overview

- The 10 Best Dividend Aristocrats Now

- Dividend Aristocrats Analysis (The Dividend Aristocrats In Focus Series)

- Historical Dividend Aristocrats List (1989 – 2026)

- Frequently Asked Questions

- Final Thoughts

How to Use The Dividend Aristocrats List To Find Dividend Investment Ideas

The downloadable Dividend Aristocrats Excel Spreadsheet List above contains the following for each stock in the index:

- Price-to-earnings ratio

- Dividend yield

- Market capitalization

All Dividend Aristocrats are high-quality businesses based on their long dividend histories. A company cannot pay rising dividends for 25+ years without having a strong and durable competitive advantage.

But not all Dividend Aristocrats make equally good investments today. That’s where the spreadsheet in this article comes into play. You can use the Dividend Aristocrats spreadsheet to quickly find quality dividend investment ideas.

The list of all Dividend Aristocrats is valuable because it gives you a concise list of all S&P 500 stocks with 25+ consecutive years of dividend increases (that also meet certain minimum size and liquidity requirements).

These are businesses that have both the desire and ability to pay shareholders rising dividends year-after-year. This is a rare combination.

Together, these two criteria are powerful – but they are not enough. Value must be considered as well.

The spreadsheet above allows you to sort by trailing price-to-earnings ratio so you can quickly find undervalued, high-quality dividend stocks.

Here’s how to use the Dividend Aristocrats list to quickly find high-quality dividend growth stocks potentially trading at a discount:

- Download the list

- Sort by ‘Trailing PE Ratio,’ smallest to largest

- Research the top stocks further

Here’s how to do this quickly in the spreadsheet:

Step 1: Download the list, and open it.

Step 2: Apply a filter function to each column in the spreadsheet.

Step 3: Click on the small gray down arrow next to ‘Trailing P/E Ratio’, and then sort smallest to largest.

Step 4: Review the highest ranked Dividend Aristocrats before investing. You can see detailed analysis on every Dividend Aristocrat found below in this article.

That’s it; you can follow the same procedure to sort by any other metric in the spreadsheet.

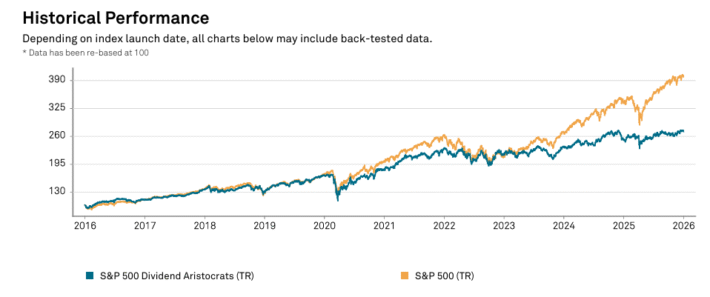

Performance Of The Dividend Aristocrats

In June 2026, the Dividend Aristocrats, as measured by the Dividend Aristocrats ETF (NOBL), registered a total return of 5.2%. It out-performed the SPDR S&P 500 ETF (SPY) for the month.

- NOBL generated returns of 5.2% in June 2026

- SPY generated returns of -1.0% in June 2026

Short-term performance is mostly noise. Performance should be measured over a minimum of 3 years, and preferably longer periods of time.

The Dividend Aristocrats Index has slightly under-performed the broader market index over the last decade, with a 10.14% total annual return for the Dividend Aristocrats and a 15.34% total annual return for the S&P 500 Index.

But the Dividend Aristocrats have exhibited lower risk than the benchmark, as measured by standard deviation.

Source: S&P Fact Sheet

Higher total returns with lower volatility is the ‘holy grail’ of investing. It is worth exploring the characteristics of the Dividend Aristocrats in detail to determine why they have performed so well.

Note that a good portion of the outperformance relative to the S&P 500 comes during recessions (2000 – 2002, 2008). Dividend Aristocrats have historically seen smaller drawdowns during recessions versus the S&P 500. This makes holding through recessions that much easier.

Case-in-point: In 2008 the Dividend Aristocrats Index declined 22%. That same year, the S&P 500 declined 38%.

Great businesses with strong competitive advantages tend to be able to generate stronger cash flows during recessions. This allows them to gain market share while weaker businesses fight to stay alive.

We believe dividend paying stocks outperform non-dividend paying stocks for three reasons:

- A company that pays dividends is likely to be generating earnings or cash flows so that it can pay dividends to shareholders. This excludes ‘pre-earnings’ start-ups and failing businesses. In short, it excludes the riskiest stocks.

- A business that pays consistent dividends must be more selective with the growth projects it takes on because a portion of its cash flows are being paid out as dividends. Scrutinizing over capital allocation decisions likely adds to shareholder value.

- Stocks that pay dividends are willing to reward shareholders with cash payments. This is a sign that management is shareholder friendly.

In our view, Dividend Aristocrats have historically outperformed the market and other dividend paying stocks because they are, on average, higher-quality businesses.

A high-quality business should outperform a mediocre business over a long period of time, all other things being equal.

For a business to increase its dividends for 25+ consecutive years, it must have or at least had in the very recent past a strong competitive advantage.

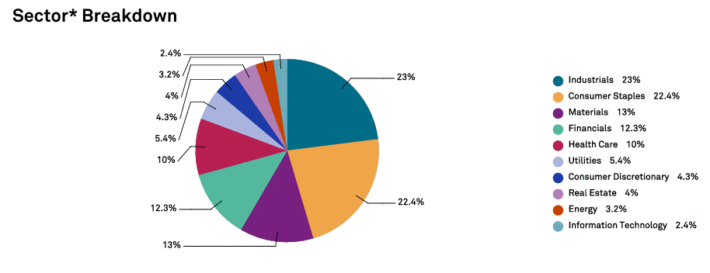

Sector Overview

A sector breakdown of the Dividend Aristocrats Index is shown below:

The Dividend Aristocrats Index is tilted toward Consumer Staples and Industrials relative to the S&P 500. These 2 sectors make up over 40% of the Dividend Aristocrats Index, but less than 20% of the S&P 500.

The Dividend Aristocrats Index is also significantly underweight the Information Technology sector, with a ~3% allocation compared with over 20% allocation within the S&P 500.

The Dividend Aristocrat Index is filled with stable ‘old economy’ blue chip consumer products businesses and manufacturers; the Coca-Cola’s (KO), and Johnson & Johnson’s (JNJ) of the investing world.

These ‘boring’ businesses aren’t likely to generate 20%+ earnings-per-share growth, but they also are very unlikely to see large earnings drawdowns as well.

The 10 Best Dividend Aristocrats Now

This research report examines the 10 best Dividend Aristocrats from our Sure Analysis Research Database with the highest 5-year forward expected total returns.

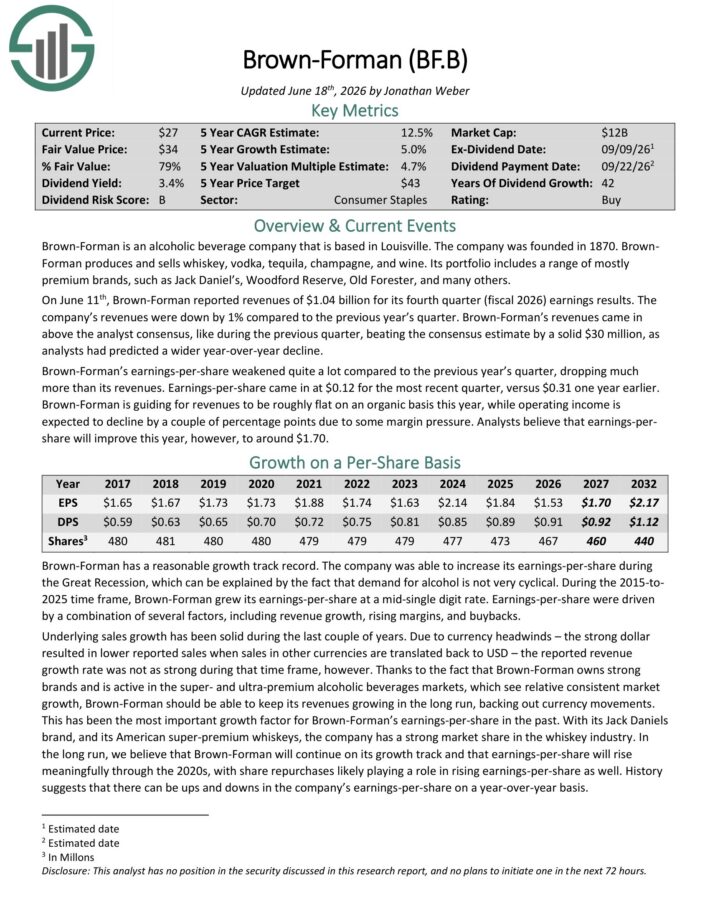

Dividend Aristocrat #10: Brown-Forman (BF.B)

- 5-year Expected Annual Returns: 13.2%

Brown-Forman is an alcoholic beverage company that is based in Louisville. The company was founded in 1870. It produces and sells whiskey, vodka, tequila, champagne, and wine.

Its portfolio includes a range of mostly premium brands, such as Jack Daniel’s, Woodford Reserve, Old Forester, and many others.

On June 11th, Brown-Forman reported revenues of $1.04 billion for its fourth quarter (fiscal 2026) earnings results.

The company’s revenues were down by 1% compared to the previous year’s quarter. Brown-Forman’s revenues came in above the analyst consensus, like during the previous quarter, beating the consensus estimate by a solid $30 million, as analysts had predicted a wider year-over-year decline.

Brown-Forman’s earnings-per-share weakened quite a lot compared to the previous year’s quarter, dropping much more than its revenues. Earnings-per-share came in at $0.12 for the most recent quarter, versus $0.31 one year earlier.

Brown-Forman is guiding for revenues to be roughly flat on an organic basis this year, while operating income is expected to decline by a couple of percentage points due to some margin pressure.

Click here to download our most recent Sure Analysis report on BF.B (preview of page 1 of 3 shown below):

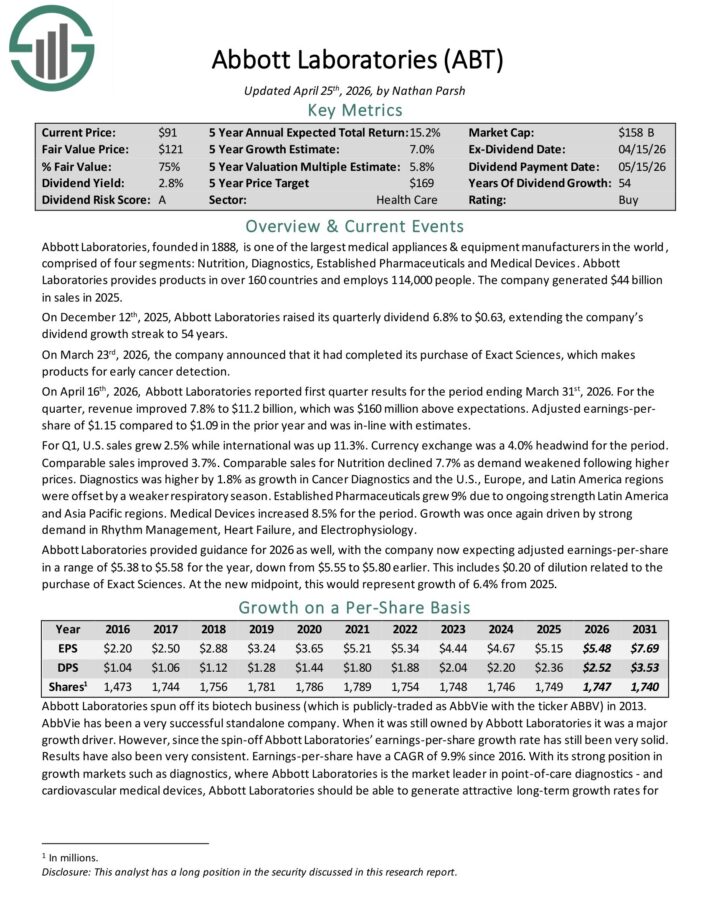

Dividend Aristocrat #9: Abbott Laboratories (ABT)

- 5-year Expected Annual Returns: 14.1%

Abbott Laboratories, founded in 1888, is one of the largest medical appliances & equipment manufacturers in the world, comprised of four segments: Nutrition, Diagnostics, Established Pharmaceuticals and Medical Devices.

Abbott Laboratories provides products in over 160 countries and employs 114,000 people. The company generated $44 billion in sales in 2025.

On December 12th, 2025, Abbott Laboratories raised its quarterly dividend 6.8% to $0.63, extending the company’s dividend growth streak to 54 years.

On April 16th, 2026, Abbott Laboratories reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue improved 7.8% to $11.2 billion, which was $160 million above expectations. Adjusted earnings-per-share of $1.15 compared to $1.09 in the prior year and was in-line with estimates.

For Q1, U.S. sales grew 2.5% while international was up 11.3%. Currency exchange was a 4.0% headwind for the period.

Comparable sales improved 3.7%. Comparable sales for Nutrition declined 7.7% as demand weakened following higher prices.

Abbott Laboratories provided guidance for 2026 as well, with the company now expecting adjusted earnings-per-share in a range of $5.38 to $5.58 for the year, down from $5.55 to $5.80 earlier.

At the new midpoint, this would represent growth of 6.4% from 2025.

Click here to download our most recent Sure Analysis report on ABT (preview of page 1 of 3 shown below):

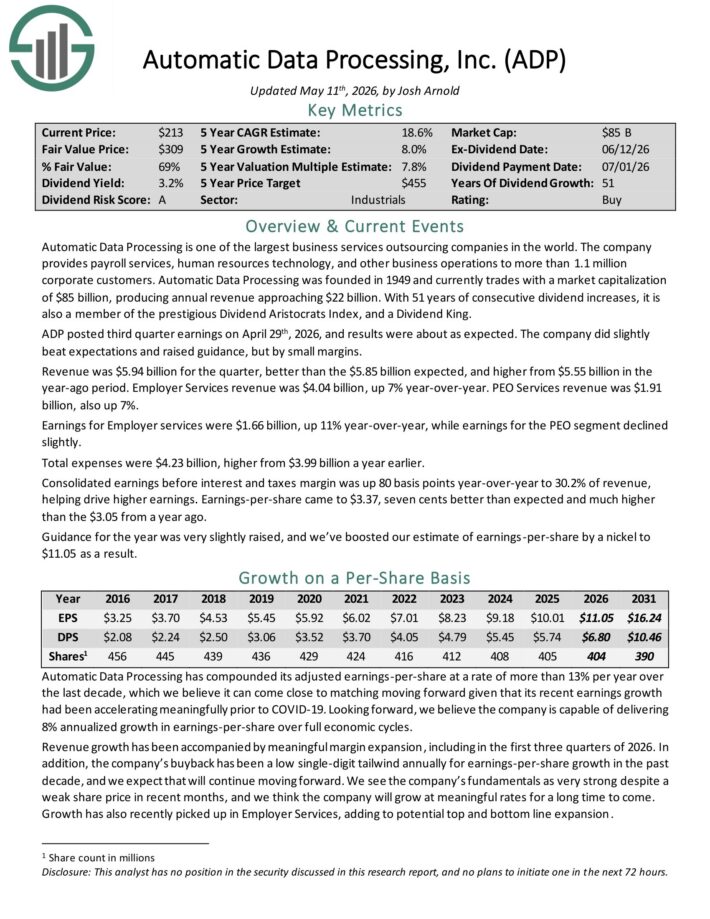

Dividend Aristocrat #8: Automatic Data Processing (ADP)

- 5-year Expected Annual Returns: 15.6%

Automatic Data Processing is one of the largest business services outsourcing companies in the world. The company provides payroll services, human resources technology, and other business operations to more than 700,000 corporate customers.

Automatic Data Processing is one of the largest business services outsourcing companies in the world.

The company provides payroll services, human resources technology, and other business operations to more than 1.1 million corporate customers.

With 51 years of consecutive dividend increases, it is also a member of the prestigious Dividend Aristocrats Index, and a Dividend King.

ADP posted third quarter earnings on April 29th, 2026, and results were about as expected. The company did slightly beat expectations and raised guidance, but by small margins.

Revenue was $5.94 billion for the quarter, better than the $5.85 billion expected, and higher from $5.55 billion in the year-ago period. Employer Services revenue was $4.04 billion, up 7% year-over-year. PEO Services revenue was $1.91 billion, also up 7%.

Earnings for Employer services were $1.66 billion, up 11% year-over-year, while earnings for the PEO segment declined slightly. Total expenses were $4.23 billion, higher from $3.99 billion a year earlier.

Consolidated earnings before interest and taxes margin was up 80 basis points year-over-year to 30.2% of revenue, helping drive higher earnings.

Click here to download our most recent Sure Analysis report on ADP (preview of page 1 of 3 shown below):

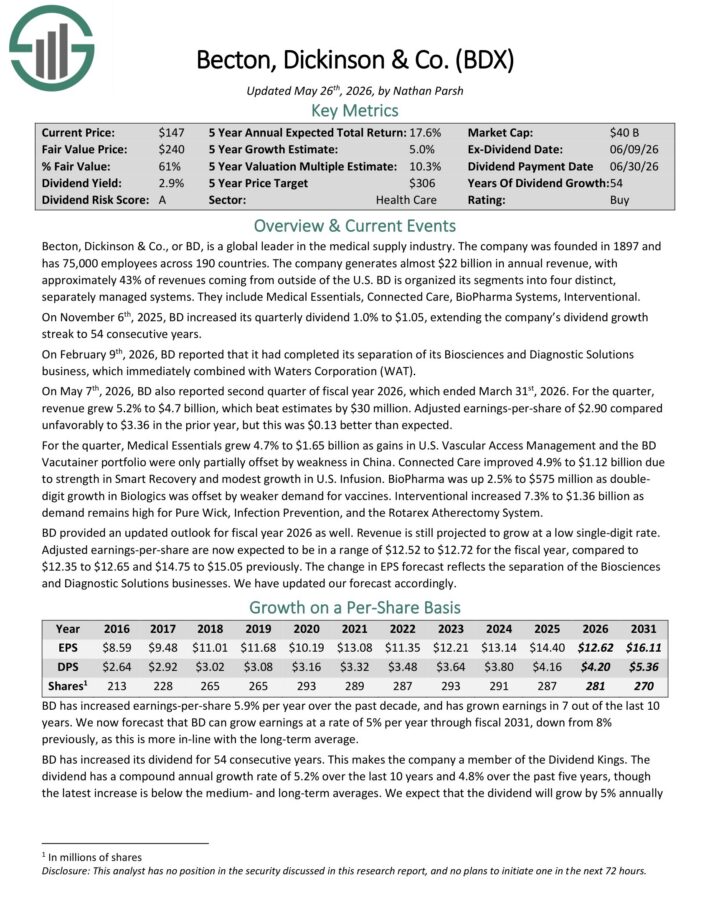

Dividend Aristocrat #7: Becton Dickinson & Co. (BDX)

- 5-year Expected Annual Returns: 15.9%

Becton, Dickinson & Co. is a global leader in the medical supply industry. The company was founded in 1897 and has 75,000 employees across 190 countries.

The company generates about $20 billion in annual revenue, with approximately 43% of revenues coming from outside of the U.S.

On November 6th, 2025, BD increased its quarterly dividend 1.0% to $1.05, extending the company’s dividend growth streak to 54 consecutive years.

On May 7th, 2026, BDX also reported second quarter of fiscal year 2026, which ended March 31st, 2026. For the quarter, revenue grew 5.2% to $4.7 billion, which beat estimates by $30 million.

Adjusted earnings-per-share of $2.90 compared unfavorably to $3.36 in the prior year, but this was $0.13 better than expected.

Click here to download our most recent Sure Analysis report on BDX (preview of page 1 of 3 shown below):

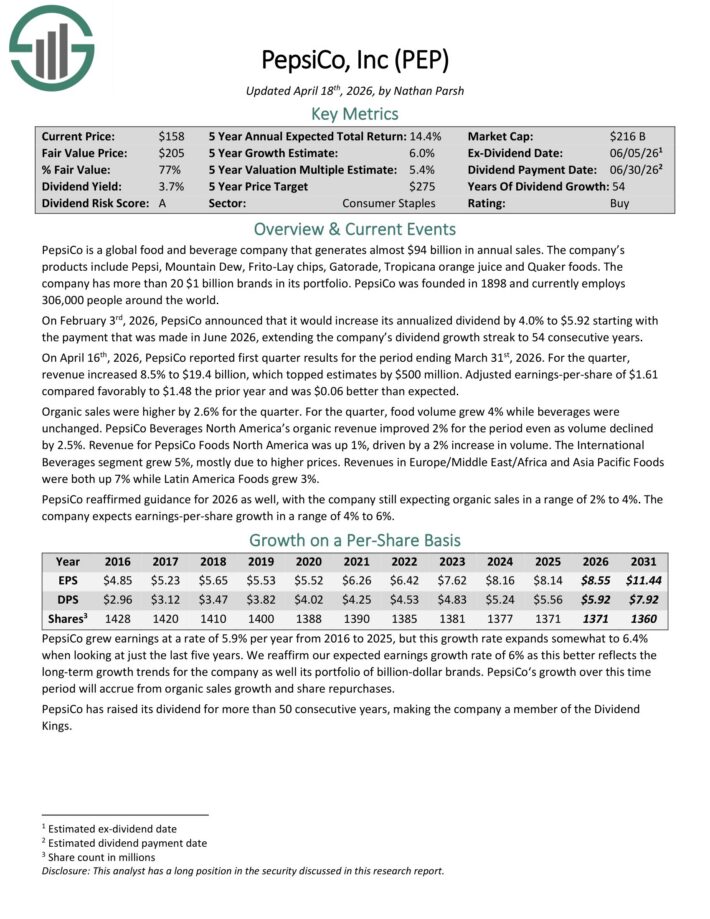

Dividend Aristocrat #6: PepsiCo Inc. (PEP)

- 5-year Expected Annual Returns: 16.6%

PepsiCo is a global food and beverage company that generates almost $94 billion in annual sales. The company’s products include Pepsi, Mountain Dew, Frito-Lay chips, Gatorade, Tropicana orange juice and Quaker foods.

The company has more than 20 $1 billion brands in its portfolio. PepsiCo was founded in 1898 and currently employs

306,000 people around the world.

On February 3rd, 2026, PepsiCo increased its annualized dividend by 4.0% to $5.92 starting with the payment that was made in June 2026, extending the company’s dividend growth streak to 54 consecutive years.

On April 16th, 2026, PepsiCo reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue increased 8.5% to $19.4 billion, which topped estimates by $500 million.

Adjusted earnings-per-share of $1.61 compared favorably to $1.48 the prior year and was $0.06 better than expected.

Organic sales were higher by 2.6% for the quarter. For the quarter, food volume grew 4% while beverages were unchanged.

PepsiCo Beverages North America’s organic revenue improved 2% for the period even as volume declined by 2.5%. Revenue for PepsiCo Foods North America was up 1%, driven by a 2% increase in volume.

The International Beverages segment grew 5%, mostly due to higher prices. Revenue in Europe/Middle East/Africa and Asia Pacific Foods were both up 7% while Latin America Foods grew 3%.

PepsiCo reaffirmed guidance for 2026 as well, with the company still expecting organic sales in a range of 2% to 4%. The company expects earnings-per-share growth in a range of 4% to 6%.

Click here to download our most recent Sure Analysis report on PEP (preview of page 1 of 3 shown below):

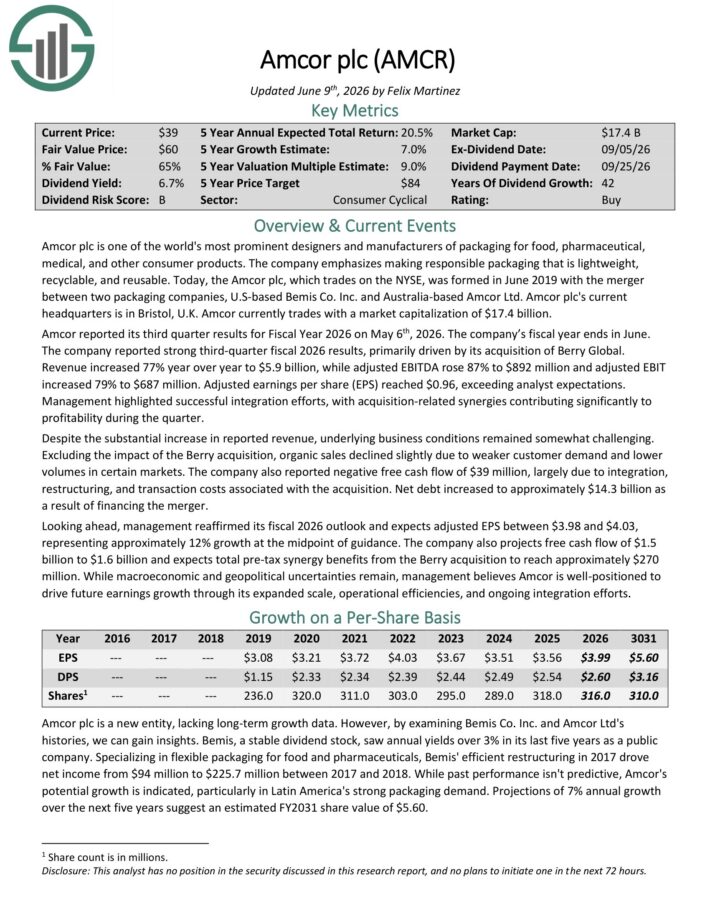

Dividend Aristocrat #5: Amcor plc (AMCR)

- 5-year Expected Annual Returns: 17.1%

Amcor plc is one of the world’s most prominent designers and manufacturers of packaging for food, pharmaceutical, medical, and other consumer products.

The company emphasizes making responsible packaging that is lightweight, recyclable, and reusable.

Amcor reported its third quarter results for Fiscal Year 2026 on May 6th, 2026. The company’s fiscal year ends in June. The company reported strong third-quarter fiscal 2026 results, primarily driven by its acquisition of Berry Global.

Revenue increased 77% year over year to $5.9 billion, while adjusted EBITDA rose 87% to $892 million and adjusted EBIT increased 79% to $687 million.

Adjusted earnings per share (EPS) reached $0.96, exceeding analyst expectations. Management highlighted successful integration efforts, with acquisition-related synergies contributing significantly to profitability during the quarter.

Click here to download our most recent Sure Analysis report on AMCR (preview of page 1 of 3 shown below):

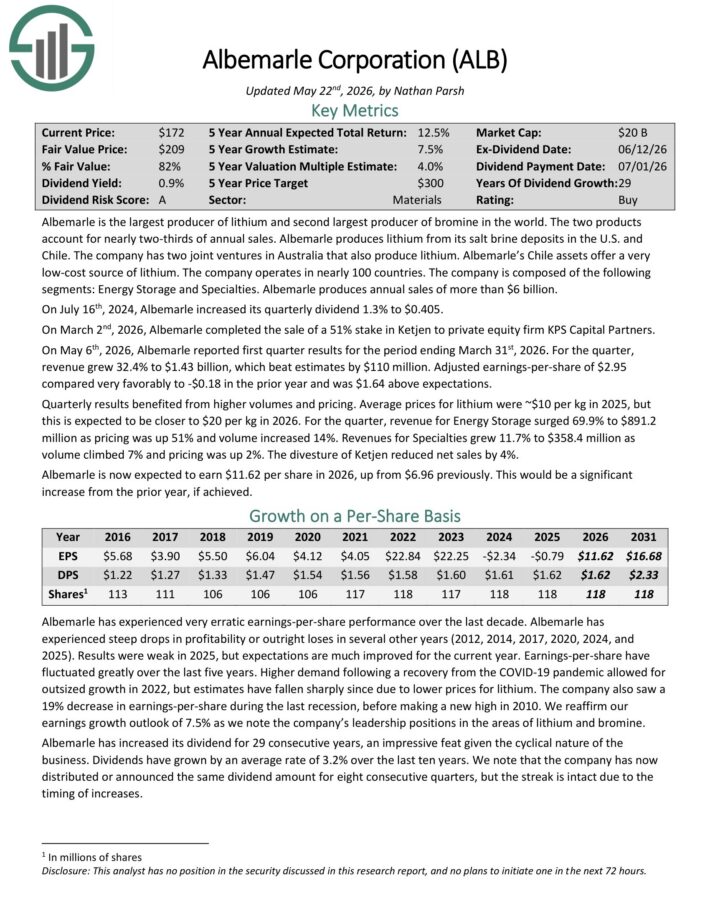

Dividend Aristocrat #4: Albemarle Corp. (ALB)

- 5-year Expected Annual Returns: 17.7%

Albemarle is the largest producer of lithium and second largest producer of bromine in the world. The two products account for nearly two-thirds of annual sales.

Albemarle produces lithium from its salt brine deposits in the U.S. and Chile. The company has two joint ventures in Australia that also produce lithium. The company operates in nearly 100 countries.

Albemarle produces annual sales of more than $6 billion.

On May 6th, 2026, Albemarle reported first quarter results for the period ending March 31st, 2026. For the quarter, revenue grew 32.4% to $1.43 billion, which beat estimates by $110 million.

Adjusted earnings-per-share of $2.95 compared very favorably to -$0.18 in the prior year and was $1.64 above expectations.

Quarterly results benefited from higher volumes and pricing. Average prices for lithium were ~$10 per kg in 2025, but this is expected to be closer to $20 per kg in 2026.

For the quarter, revenue for Energy Storage surged 69.9% to $891.2 million as pricing was up 51% and volume increased 14%.

Revenues for Specialties grew 11.7% to $358.4 million as volume climbed 7% and pricing was up 2%. The divesture of Ketjen reduced net sales by 4%.

Albemarle is now expected to earn $11.62 per share in 2026.

Click here to download our most recent Sure Analysis report on ALB (preview of page 1 of 3 shown below):

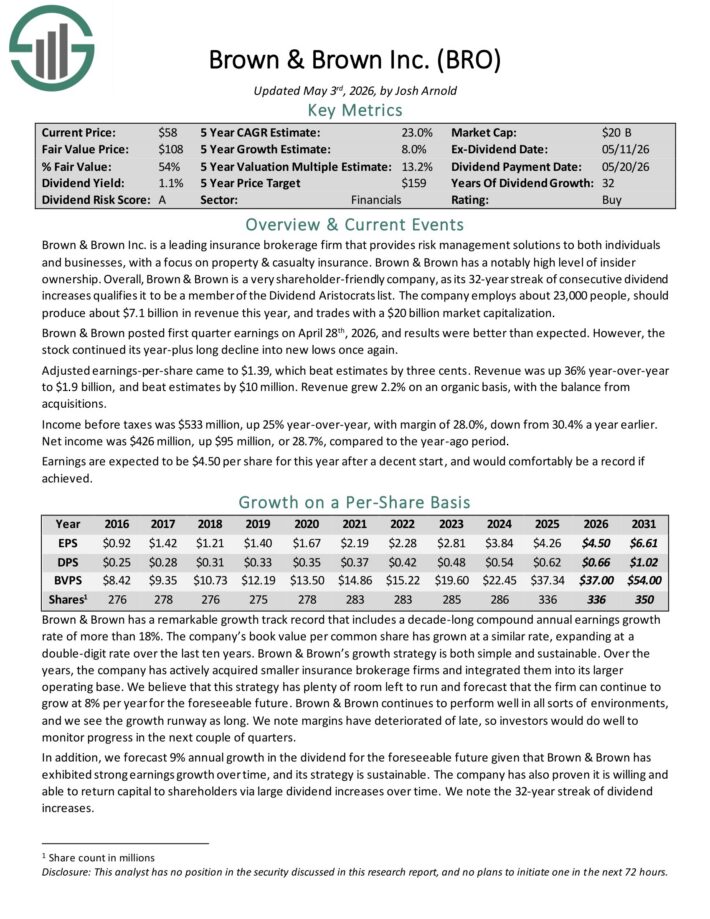

Dividend Aristocrat #3: Brown & Brown (BRO)

- 5-year Expected Annual Returns: 18.6%

Brown & Brown Inc. is a leading insurance brokerage firm that provides risk management solutions to both individuals and businesses, with a focus on property & casualty insurance.

Brown & Brown posted first quarter earnings on April 28th, 2026, and results were better than expected. However, the

stock continued its year-plus long decline into new lows once again.

Adjusted earnings-per-share came to $1.39, which beat estimates by three cents. Revenue was up 36% year-over-year to $1.9 billion, and beat estimates by $10 million. Revenue grew 2.2% on an organic basis, with the balance from acquisitions.

Income before taxes was $533 million, up 25% year-over-year, with margin of 28.0%, down from 30.4% a year earlier. Net income was $426 million, up $95 million, or 28.7%, compared to the year-ago period.

Click here to download our most recent Sure Analysis report on BRO (preview of page 1 of 3 shown below):

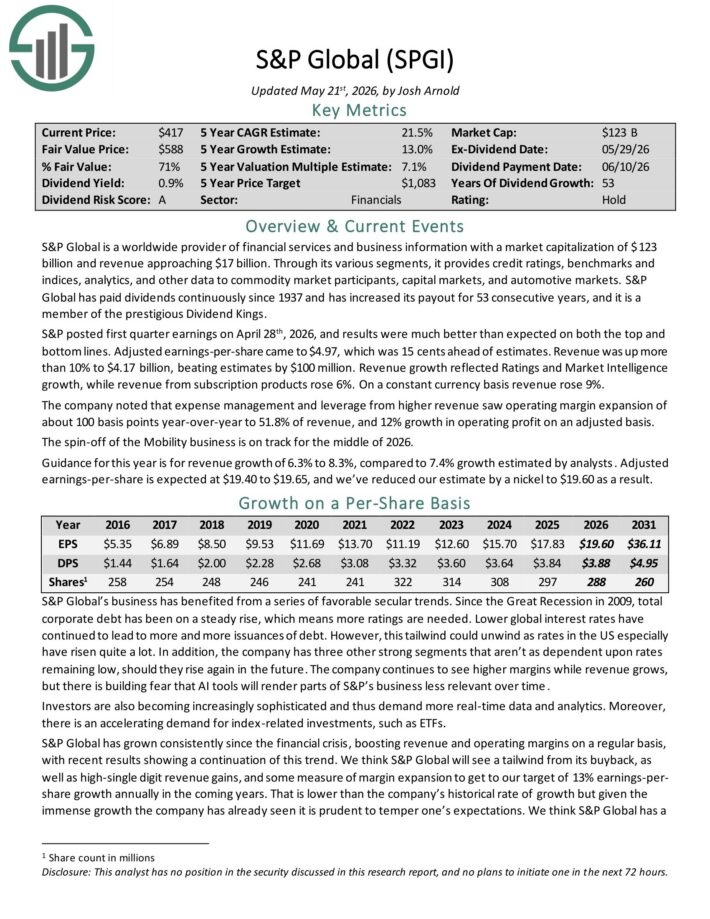

Dividend Aristocrat #2: S&P Global (SPGI)

- 5-year Expected Annual Returns: 20.4%

S&P Global is a worldwide provider of financial services and business information with revenue of about $16.5 billion.

Through its various segments, it provides credit ratings, benchmarks and indices, analytics, and other data to commodity market participants, capital markets, and automotive markets.

S&P Global has paid dividends continuously since 1937 and has increased its payout for 53 consecutive years.

S&P posted first quarter earnings on April 28th, 2026, and results were much better than expected on both the top and bottom lines. Adjusted earnings-per-share came to $4.97, which was 15 cents ahead of estimates.

Revenue was up more than 10% to $4.17 billion, beating estimates by $100 million. Revenue growth reflected Ratings and Market Intelligence growth, while revenue from subscription products rose 6%. On a constant currency basis revenue rose 9%.

The company noted that expense management and leverage from higher revenue saw operating margin expansion of about 100 basis points year-over-year to 51.8% of revenue, and 12% growth in operating profit on an adjusted basis.

The spin-off of the Mobility business is on track for the middle of 2026.

Guidance for this year is for revenue growth of 6.3% to 8.3%.

Click here to download our most recent Sure Analysis report on SPGI (preview of page 1 of 3 shown below):

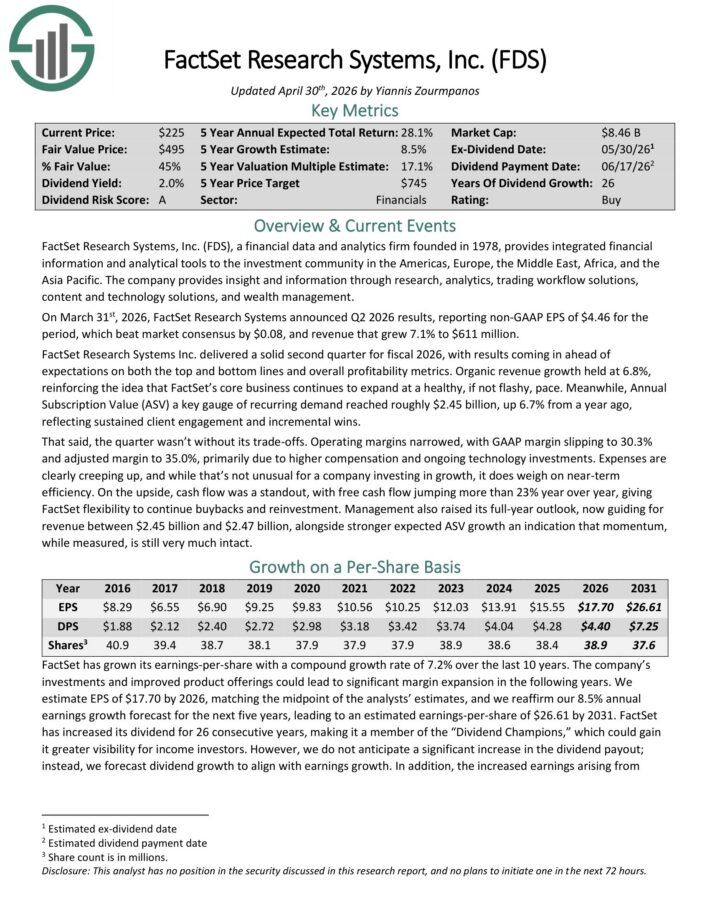

Dividend Aristocrat #1: Factset Research Systems (FDS)

- 5-year Expected Annual Returns: 25.4%

FactSet Research Systems, a financial data and analytics firm founded in 1978, provides integrated financial information and analytical tools to the investment community in the Americas, Europe, the Middle East, Africa, and Asia-Pacific.

The company provides insight and information through research, analytics, trading workflow solutions, content and technology solutions, and wealth management.

On March 31st, 2026, FactSet Research Systems announced Q2 2026 results, reporting non-GAAP EPS of $4.46 for the period, which beat market consensus by $0.08.

Revenue grew 7.1% to $611 million. Organic revenue growth held at 6.8%, while Annual Subscription Value (ASV) a key gauge of recurring demand reached roughly $2.45 billion, up 6.7% from a year ago.

Operating margins narrowed, with GAAP margin slipping to 30.3% and adjusted margin to 35.0%, primarily due to higher compensation and ongoing technology investments.

Free cash flow jumped 23% year over year, giving FactSet flexibility to continue buybacks and reinvestment.

Management also raised its full-year outlook, now guiding for revenue between $2.45 billion and $2.47 billion.

Click here to download our most recent Sure Analysis report on FDS (preview of page 1 of 3 shown below):

The Dividend Aristocrats In Focus Analysis Series

You can see analysis on every single Dividend Aristocrat below. Each is sorted by GICS sectors and listed in alphabetical order by name. The newest Sure Analysis Research Database report for each security is included as well.

Consumer Staples

- Archer-Daniels-Midland (ADM)

- Amcor (AMCR)

- Brown-Forman (BF-B)

- Colgate-Palmolive (CL)

- Church & Dwight (CHD)

- Clorox (CLX)

- Coca-Cola (KO)

- Hormel Foods (HRL)

- J.M. Smucker (SJM)

- Kimberly-Clark (KMB)

- McCormick & Company (MKC)

- PepsiCo (PEP)

- Procter & Gamble (PG)

- Sysco Corporation (SYY)

- Walmart (WMT)

Industrials

- Automatic Data Processing (ADP)

- A.O. Smith (AOS)

- C.H. Robinson Worldwide (CHRW)

- Cintas (CTAS)

- Dover (DOV)

- Emerson Electric (EMR)

- Expeditors International (EXPD)

- Fastenal Co. (FAST)

- Illinois Tool Works (ITW)

- Nordson Corporation (NDSN)

- Pentair (PNR)

- Roper Technologies (ROP)

- Stanley Black & Decker (SWK)

- W.W. Grainger (GWW)

- General Dynamics (GD)

- Caterpillar (CAT)

Health Care

- Abbott Laboratories (ABT)

- AbbVie (ABBV)

- Becton, Dickinson & Company (BDX)

- Cardinal Health (CAH)

- Johnson & Johnson (JNJ)

- Kenvue Inc. (KVUE)

- Medtronic (MDT)

- West Pharmaceutical Services (WST)

Consumer Discretionary

Financials

- Aflac (AFL)

- Brown & Brown (BRO)

- Cincinnati Financial (CINF)

- Erie Indemnity (ERIE)

- FactSet Research Systems (FDS)

- Franklin Resources (BEN)

- S&P Global (SPGI)

- T. Rowe Price Group (TROW)

- Chubb (CB)

Materials

- Air Products and Chemicals (APD)

- Albemarle (ALB)

- Ecolab (ECL)

- PPG Industries (PPG)

- Sherwin-Williams (SHW)

- Nucor (NUE)

- Linde (LIN)

Energy

Information Technology

Real Estate

Utilities

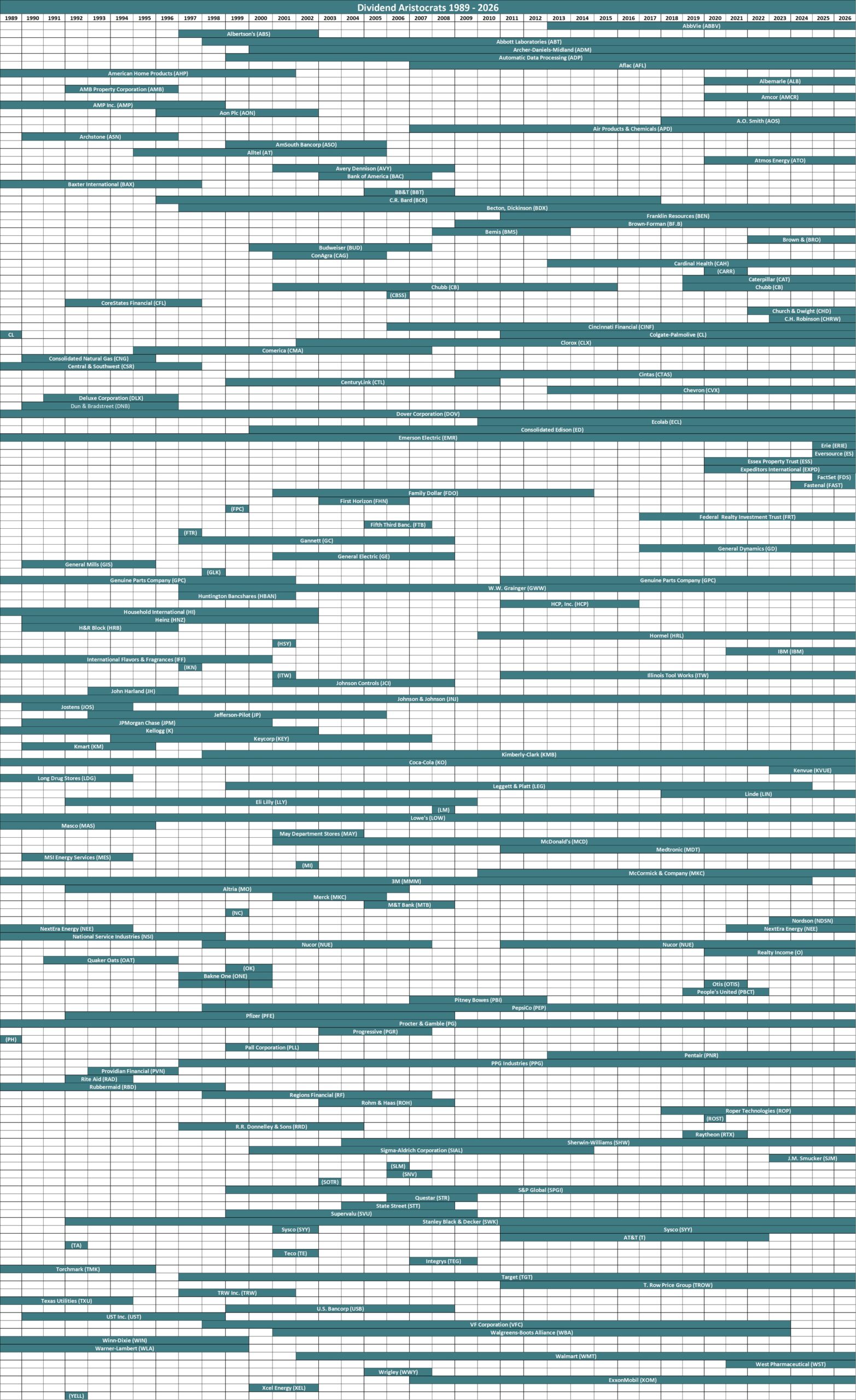

Historical Dividend Aristocrats List

(1989 – 2026)

The image below shows the history of the Dividend Aristocrats Index from 1989 through 2026.

Note: CL, GPC, and NUE were all removed and re-added to the Dividend Aristocrats Index through the historical period analyzed above. We are unsure as to why. Companies created via a spin-off (like AbbVie) can be Dividend Aristocrats with less than 25 years of rising dividends if the parent company was a Dividend Aristocrat.

Disclaimer: Sure Dividend is not affiliated with S&P Global in any way. S&P Global owns and maintains The Dividend Aristocrats Index. The information in this article and downloadable spreadsheet and image below is based on Sure Dividend’s own review, summary, and analysis of the S&P 500 Dividend Aristocrats ETF (NOBL) and other sources, and is meant to help individual investors better understand this ETF and the index upon which it is based. None of the information in this article or spreadsheet is official data from S&P Global. Consult S&P Global for official information.

This information was compiled from the following sources:

- 1989 – 1991: Dividend Growth Investor

- 1992 – 2015: NOBL Index Historical Constituents

- 2016: Sure Dividend update

- 2017 – 2026: Data from S&P press releases and tracking dividends

Frequently Asked Questions

This section will address some of most common questions investors have regarding the Dividend Aristocrats.

1. What is the highest-paying Dividend Aristocrat?

Answer: Amcor currently yields 5.8%.

2. What is the difference between the Dividend Aristocrats and the Dividend Kings?

Answer: The Dividend Aristocrats must be constituents of the S&P 500 Index, have raised their dividends for at least 25 consecutive years, and satisfy a number of liquidity requirements.

The Dividend Kings only need to have raised their dividends for at least 50 consecutive years.

3. Is there an ETF that tracks the Dividend Aristocrats?

Answer: Yes, the Dividend Aristocrats ETF (NOBL) is an exchange-traded fund that specifically holds the Dividend Aristocrats.

4. What is the difference between the Dividend Aristocrats and the Dividend Champions?

Answer: The Dividend Aristocrats and Dividend Champions share one requirement, which is that a company must have raised its dividend for at least 25 consecutive years.

But like the Dividend Kings, the Dividend Champions do not need to be in the S&P 500 Index, nor satisfy the various liquidity requirements.

5. Which Dividend Aristocrat has the longest active streak of annual dividend increases?

Currently, there are three Dividend Aristocrats tied at 70 years: Procter & Gamble, Genuine Parts, and Dover Corporation.

6. What is the average dividend yield of the Dividend Aristocrats?

Right now, the average dividend yield of the Dividend Aristocrats is ~2%.

7. Are the Dividend Aristocrats safe investments?

While there are never any guarantees when it comes to the stock market, we believe the Dividend Aristocrats are among the safest dividend stocks when it comes to the sustainability of their dividend payouts.

The Dividend Aristocrats have durable competitive advantages that allow them to raise their dividends each year, even during a recession.

Other Dividend Lists & Final Thoughts

The Dividend Aristocrats list is not the only way to quickly screen for stocks that regularly pay rising dividends.

- The Dividend Kings List is even more exclusive than the Dividend Aristocrats. It is comprised of 58 stocks with 50+ years of consecutive dividend increases.

- The Blue Chip Stocks List: stocks that qualify as Dividend Achievers, Dividend Aristocrats, and/or Dividend Kings

- The High Dividend Stocks List: stocks that appeal to investors interested in the highest yields of 5% or more.

- The Monthly Dividend Stocks List: stocks that pay dividends every month, for 12 dividend payments per year.

There is nothing magical about the Dividend Aristocrats. They are ‘just’ a collection of high-quality shareholder friendly stocks that have strong competitive advantages.

Purchasing these types of stocks at fair or better prices and holding for the long-run will likely result in favorable long-term performance.